Buying a Car with Bad Credit? What to Know About Loans, Down Payments, and More

Key Takeaways

- Buying a car with bad credit in 2025 comes with risks, but with proper planning, you can still get a fair deal.

- We cover what you need to know about down payments and credit history to buy a car.

- Need expert assistance? CarEdge can help, no matter your credit score.

Having bad credit doesn’t mean you can’t buy a car—it just means you need to be smart about it. In 2025, car prices remain high, and auto loan interest rates are even higher for buyers with low credit scores. But don’t worry—there are ways to navigate the car-buying process and secure financing, even with bad credit.

Whether you’re rebuilding your credit or buying a car with no credit history at all, this guide covers everything you need to know. From down payment requirements to the best lenders for bad credit, we’ll walk you through the steps to buy a car in 2025 without getting ripped off.

What Counts as Bad Credit for a Car Loan?

In the world of auto financing, lenders classify borrowers into different credit tiers. Here’s a breakdown:

| Credit Tier | Credit Score Range | Financing Impact |

|---|---|---|

| Prime | 660+ | Low interest rates (as low as 4-6%) |

| Near Prime | 620-659 | Moderate interest rates (8-12%) |

| Subprime | 580-619 | High interest rates (12-18%) |

| Deep Subprime | Below 580 | Very high interest rates (18-25% or more) |

If your credit score falls in the subprime or deep subprime category, you will likely face higher loan rates, larger down payment requirements, and stricter lender requirements.

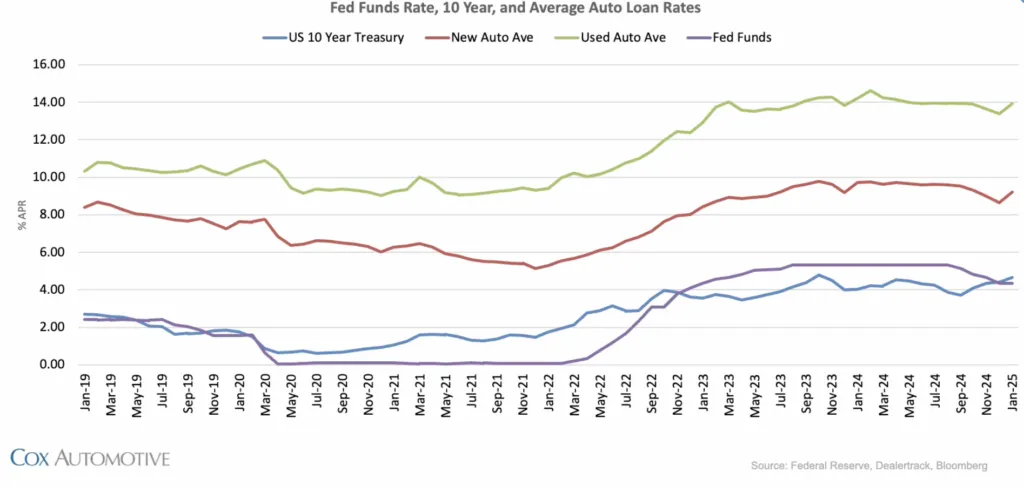

The national average used car loan rate for subprime borrowers is 16.78%, while deep subprime borrowers see rates above 20%. On a $20,000 car loan, that could mean paying thousands more in interest over time.

How to Buy a Car with Bad Credit in 2025

1. Save for a Bigger Down Payment

Why it matters: A larger down payment lowers your monthly payments, improves your loan approval chances, and reduces how much you pay in interest over time.

Here’s why a down payment is essential when buying with bad credit:

- Lenders see you as less risky if you have “skin in the game.”

- You borrow less money, which lowers your total interest paid.

- A larger down payment can offset a higher APR, reducing your long-term costs.

How much should you put down?

- 10% down = minimum recommended

- 20% down = ideal for better loan terms

- 25%+ down = recommended for subprime borrowers

👉 Example: If you’re looking at a $15,000 car, here’s how different down payments impact your financing:

| Down Payment | Loan Amount | Example Monthly Payment (16.5% APR, 60 months) |

|---|---|---|

| $0 | $15,000 | $370/month |

| $1,500 (10%) | $13,500 | $333/month |

| $3,000 (20%) | $12,000 | $296/month |

Pro Tip: Trade in your current vehicle to boost your down payment! Even a low-value trade-in can help.

2. Get Pre-Approved Before You Shop

In 2025, the average used car loan rate is hovering around 14% APR. However, this includes car buyers across all credit scores. Drivers with bad credit are qualifying for loans with APRs between 15% and 20% in 2025. However, those who play it smart and shop around are guaranteed to save serious money. Here’s what you need to know.

Why it matters: Getting pre-approved for a car loan puts you in control. It allows you to:

✔️ Know your real budget before walking into a dealership

✔️ Avoid getting ripped off by dealer financing✔️ Compare multiple lenders for the best rates

Where to get pre-approved:

- Local credit unions (best rates, more flexible terms for bad credit borrowers)

- Online lenders (fast approval, some specialize in bad credit loans)

- Traditional banks (may require higher credit scores)

🚨 What to avoid:

- “Guaranteed Approval” dealerships – These often have sky-high interest rates and fees.

- Multiple hard credit inquiries – If you apply with too many lenders at once, your credit score could take a hit.

Check your credit report before applying. You can get a free credit report at AnnualCreditReport.com to see if there are any errors dragging your score down.

3. Choose the Right Car (And Keep It Practical!)

Why it matters: Lenders won’t approve just any car for buyers with bad credit. They prefer reliable, affordable vehicles that hold their value well.

Avoid luxury cars, sports cars, and high-mileage vehicles. These are harder to finance and come with higher insurance costs.

Best cars to finance with bad credit:

- Toyota Corolla & Camry – High resale value, low maintenance costs

- Honda Civic & Accord – Reliable and fuel-efficient

- Mazda CX-30 & CX-50 – Affordable with great safety ratings

- Subaru Outback & Legacy – Often cheaper to insure

📌 Target vehicles priced under $20,000. Cars under this price point sell quickly, so act fast when you find a good deal. However, keep in mind that securing a loan for under $10,000 is possible but can be challenging. Loans under $5,000 are next to impossible. Keep these realities in mind before you buy.

Talk to a local bank or credit union about their lending policies before heading out to buy a car.

4. Know Your Loan Terms & Avoid Scams

Why it matters: Dealerships make a fortune off bad credit buyers with overpriced loans, sneaky fees, and unnecessary add-ons.

**What to watch out for:**🚩 “Yo-Yo Financing” scams – A dealer lets you take the car home before financing is finalized, then calls back saying you need a higher interest loan. Make sure financing is finalized before you drive home in your new car.

🚩 “Packing the Payment” tricks – They sneak in warranties and add-ons without telling you. Despite what the salesperson or finance manager may say, none of these products are required. Read the product contract before agreeing to anything.

🚩 “Spot Delivery” fraud – You sign a contract, but later they claim financing fell through and demand a higher interest rate.

**Before signing anything, ask:

**❓ What’s my APR? (Aim for as low as possible)

❓ What’s the Out-the-Door Price of the car? (Don’t just focus on the monthly payment!)

❓ Check the loan terms: Can I pay extra or refinance later without penalties?

5. Improve Your Credit Score Before You Buy

Why it matters: Even a small credit score boost can save you thousands on your car loan. Even if your credit score is deep in the subprime category, a slight improvement could save you hundreds of dollars in interest.

**How to improve your score in 30-90 days:

**✔️ Lower your credit card balances (improves credit utilization)

✔️ Look for errors on your credit report (resolving them could boost your score fast!)

✔️ Make all payments on time (even utilities and rent matter!)

What’s the impact of a higher credit score? Take a look at the following real-world examples. Pay close attention to how much interest is paid at each of the different loan rates.

| Credit Score | Example APR (60 months) | Interest Paid on $15,000 Loan |

|---|---|---|

| 720+ | 6.5% APR | $2,610 |

| 660-719 | 10.5% APR | $4,450 |

| 600-659 | 14.9% APR | $6,240 |

| 500-599 | 20.0%+ APR | $9,190+ |

Even raising your score from 580 to 620 could cut your APR by half! That would keep hundreds of dollars in your wallet over the life of your loan.

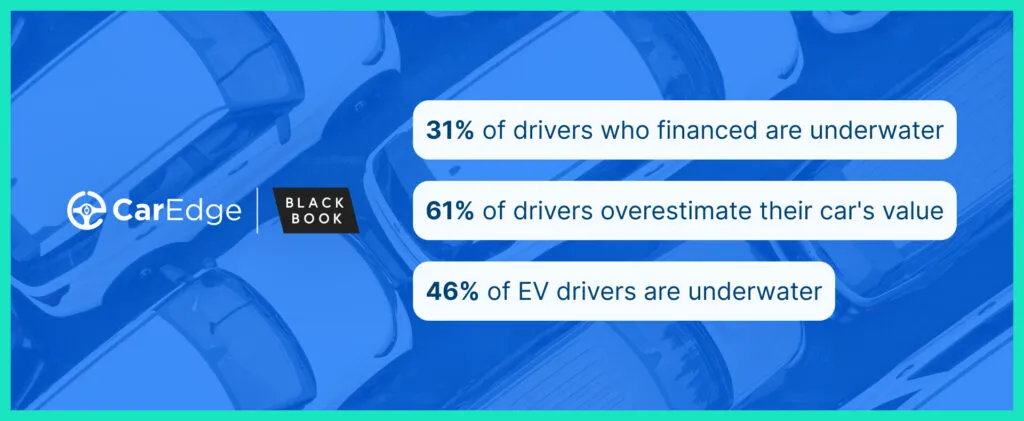

New Car Buyers Beware: The Negative Equity Trap

For those considering buying a new car with bad credit, be extra cautious. New car prices are still near record highs, and financing costs are extremely expensive—even for buyers with good credit. With average used car loan rates at 14% and new car loan rates often exceeding 10% for subprime borrowers, it’s easy to end up in a negative equity situation, where you owe more than the car is worth.

That’s why buyers with bad credit should avoid financing expensive new cars and instead look for reliable used cars under $20,000. This strategy will help you avoid excessive interest costs and reduce the risk of negative equity down the road.

Learn more about how to protect your finances and avoid negative equity.

Final Thoughts: Should You Buy Now or Wait?

As spring car buying season approaches, used car prices are already starting to rise. Historically, March, April, and May are some of the most expensive months for used cars due to higher demand from tax refund buyers.

If you’re looking for the best deal on a used car, waiting 90 days could save you hundreds—or even thousands—of dollars. By late spring and early summer, inventory levels will improve, and demand will start to cool off, making it the ideal time to buy.

However, if you must buy now:✔️ Stick to used cars under $20,000 to avoid overpaying✔️ Save 10-25% for a down payment to reduce interest costs**✔️ Get pre-approved BEFORE going to a dealership to secure a better loan****✔️ Avoid dealer scams by** knowing which fees are legit

✔️ Use these Free Car Buying Calculators to know what to expect

🚗 Ready to find the best car deals? Get your FREE Car Buyer’s GuideWant a pro to negotiate for you? Let CarEdge handle everything!

Sponsored by Insurify

Are you overpaying for car insurance?

Compare rates from top carriers in under 5 minutes. CarEdge users save an average of $996/year on auto insurance.

*Disclosure: CarEdge may earn a commission when you compare insurance quotes through our partner, Insurify. This does not influence our editorial content.*