CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

With gas prices moving higher, hybrid SUVs are a smart choice. But not all of your options get great fuel economy, and even fewer have stellar reliability ratings. We found six hybrid SUVs that offer a perfect combination of the highest miles per gallon and the best reliability ratings from Consumer Reports.

Fuel economy: 47 MPG city / 40 MPG highway

Consumer Reports reliability rating: 77/100

The 2026 RAV4 Hybrid is an all-new sixth-generation model, and for the first time, every RAV4 comes standard with a hybrid powertrain. The redesign brings more power (up to 236 horsepower in AWD trim), a towing capacity of up to 3,500 pounds, and Toyota Safety Sense 4.0 across the board. At 47 MPG in the city, it’s the most fuel-efficient option on this list, and its reliability score of 77/100 from Consumer Reports is the highest here as well.

See RAV4 Hybrid deals near you

Fuel economy: 43 MPG city / 36 MPG highway

Consumer Reports reliability rating: 61/100

The CR-V Hybrid remains a strong pick for city commuters, with 43 MPG in stop-and-go traffic and a capable 204-horsepower two-motor hybrid system. For 2026, Honda standardized wireless charging and a larger 9-inch touchscreen across the entire lineup, and added a new TrailSport trim for buyers who want more off-road capability. The CR-V faces stiff competition from the fully revamped 2026 RAV4.

See CR-V Hybrid deals near you

Fuel economy: 41 MPG city / 38 MPG highway

Consumer Reports reliability rating: 68/100

For buyers who want a luxury hybrid SUV without sacrificing efficiency, the NX Hybrid delivers. The 2026 NX 350h earns an impressive 38 MPG on the highway and pairs that efficiency with a well-appointed cabin featuring standard heated front seats, NuLuxe upholstery, and Lexus Safety System+ 3.0 across all trims. For 2026, Lexus added a new front-wheel-drive option and an F SPORT Handling trim to the hybrid lineup.

See Lexus Hybrid deals near you

Fuel economy: 35 MPG city / 34 MPG highway

Consumer Reports reliability rating: 63/100

The 2026 Forester Hybrid is a first for Subaru in the U.S. market, and it brings the brand’s trademark capability in line with hybrid efficiency. Standard Symmetrical All-Wheel Drive, 8.7 inches of ground clearance, and X-MODE with Hill Descent Control come standard making it the most off-road-capable pick on this list. The 194-horsepower hybrid powertrain delivers up to 581 miles of range per tank, and Subaru’s latest EyeSight Driver Assist Technology is standard across all trims.

See Forester Hybrid deals near you

Fuel economy: 35 MPG city / 34 MPG highway

Consumer Reports reliability rating: 68/100

The Highlander Hybrid is the traditional choice for families who need three-row seating without the bulk of a full-size SUV. Standard AWD, seating for up to eight, and a 3,500-pound tow rating give it real everyday utility, while 35 MPG combined keeps fuel costs manageable for a midsize three-row. Toyota Safety Sense 2.5+, the Toyota Audio Multimedia system, and an available JBL Premium Audio system are among the key highlights.

See Highlander Hybrid deals near you

Fuel economy: 37 MPG city / 34 MPG highway

Consumer Reports reliability rating: 73/100

If you need three rows and maximum fuel economy, the Grand Highlander Hybrid is the one to beat. It’s the most efficient three-row SUV on the market, returning 37 MPG in the city and earning a strong 73/100 reliability rating from Consumer Reports. The Grand Highlander’s stretched body gives it more passenger and cargo room than the standard Highlander, with up to 97.5 cubic feet of total cargo space — and seven USB-C ports throughout the cabin so no one in any row runs out of battery.

See Grand Highlander Hybrid deals near you

Not every hybrid SUV delivers on both efficiency and reliability. These six models earn their spots on both fronts. If fuel economy is your top priority, the RAV4 Hybrid is the clear winner in the compact class. Want luxury with your MPG? The Lexus NX Hybrid is tough to beat. And if you’re hauling a family of five or more, the Grand Highlander Hybrid gives you the most efficiency of any three-row on the market.

When gas prices rise, it’s only natural that interest in hybrid vehicles rises as well. Buying a hybrid should mean getting the best of both worlds: better fuel economy and a smart long-term investment. But not all hybrids deliver on that promise. Some combine below-average reliability with steep depreciation, which means you’re paying a premium up front and taking a loss on the back end.

Using Consumer Reports reliability scores and CarEdge’s Value Ratings, we identified six hybrids to avoid in 2026. These aren’t necessarily bad cars across the board, but for buyers who care about ownership costs and long-term value, these numbers should give you pause.

Consumer Reports Reliability: 20/100| Overall Score: 56/100| CarEdge Value Rating: C

The CX-90 PHEV is Mazda’s most expensive vehicle, with the plug-in hybrid version starting around $50,500. It drives beautifully and looks sharp, but Consumer Reports gives it a reliability score of just 20 out of 100 — the lowest on this list. Owners have reported recurring transmission roughness at low speeds, radar sensor errors, and technology glitches that required multiple dealer visits to diagnose. Mazda has issued recalls to address some of the transmission problems, but the issues persist across model years.

On resale, the CX-90 PHEV takes a significant hit early. Some owners have reported losing $10,000 to $13,000 in value within the first year. That kind of depreciation, combined with a reliability track record that’s still unproven for a relatively new platform, makes the plug-in hybrid variant a risky buy compared to the more proven gas-powered CX-90 trims. If you love the CX-90, the 3.3 Turbo models carry better reliability scores and similar driving dynamics.

Consumer Reports Reliability: 37/100| Overall Score: 58/100| CarEdge Value Rating: F

The Hornet R/T PHEV had a compelling pitch: 288 horsepower, 32 miles of electric range, and Dodge styling at a price closer to $40,000. But the real-world ownership experience for many buyers has been far less exciting. Consumer Reports gives it a 37 out of 100 for reliability, and owner forums are filled with reports of electrical failures, warning lights appearing at under 1,000 miles, chronic 12V battery drain, and software issues that dealers struggled to resolve.

The resale story is equally grim. A 2024 Dodge Hornet has depreciated 44% in just two years. CarEdge projects the PHEV variant to lose roughly 62% of its value over five years — one of the steepest depreciation curves in the compact SUV segment. It’s worth noting that Stellantis halted U.S. production of the Hornet for the 2026 model year due to tariffs on foreign-made vehicles, so new inventory is limited. Remaining units on dealer lots may come with incentives, but that doesn’t fix the underlying reliability concerns.

Consumer Reports Reliability: 39/100| Overall Score: 67/100| CarEdge Value Rating: D-

The Escape PHEV offers 37 miles of electric range and up to 105 MPGe, which are above average in the segment. But a Consumer Reports reliability score of 39 and a CarEdge Value Rating of D- reflect a pattern of ownership concerns that are hard to overlook. Common complaints from owners include infotainment failures, AWD system issues, and recurring recalls — with some owners reporting that their vehicles spent weeks at the dealer awaiting parts.

On depreciation, the Escape PHEV has been especially punishing. A 2024 Ford Escape Plug-in Hybrid depreciated 54% in just two years, leaving owners with a resale value of around $18,900. KBB notes the Escape’s resale value falls below segment leaders like the Honda CR-V, Toyota RAV4, and Subaru Forester. The 2026 model is also the last Escape before Ford transitions the nameplate, which adds uncertainty for long-term buyers. The all-new 2026 Toyota RAV4 Plug-In Hybrid, with an estimated 50 miles of electric range, makes for a compelling alternative.

Consumer Reports Reliability: 37/100| Overall Score: 73/100| CarEdge Value Rating: D+

The Lincoln Nautilus Hybrid is one of the better-scoring vehicles on this list in terms of overall quality — a 73 from Consumer Reports reflects a genuinely capable luxury SUV with a well-appointed interior and solid road manners. But reliability comes in at 37, and depreciation is a known weakness for Lincoln hybrids across the board.

Luxury vehicles depreciate faster as a rule, and the Nautilus Hybrid is no exception. At a starting price north of $55,000, a D+ Value Rating from CarEdge signals that buyers aren’t getting much return on that investment. Shoppers cross-shopping in the luxury hybrid SUV space should check CarEdge’s depreciation calculator before committing, particularly if they plan to sell or trade within five years.

Consumer Reports Reliability: 42/100| Overall Score: 73/100| CarEdge Value Rating: D+

The Sorento Hybrid offers three rows, and Kia’s appealing warranty coverage. On paper, it’s easy to see why it attracts shoppers. But a reliability score of 42 and a D+ Value Rating put it in uncomfortable territory for a vehicle that starts around $40,000.

Depreciation has been a consistent issue for the Sorento Hybrid. Data shows the Sorento Hybrid losing value faster than the segment average, making it a less efficient long-term investment than its price point would suggest. Buyers interested in a three-row hybrid SUV with stronger reliability and resale value might find better options in the Toyota Venza or Kia’s own Telluride — though the Telluride doesn’t offer a hybrid powertrain, its reliability and resale are significantly stronger.

Consumer Reports Reliability: 39/100| Overall Score: 67/100| CarEdge Value Rating: C+

The Sonata Hybrid earns the strongest CarEdge Value Rating on this list at C+, and its overall Consumer Reports score of 67 reflects a genuinely capable mid-size hybrid sedan. It’s fuel-efficient, comfortable, and loaded with features for the price. So why is it here?

Because a reliability score of 39 and a five-year depreciation trajectory that leaves owners with roughly $14,300 in residual value on a $30,000+ purchase deserve attention. Consumer Reports flagged the 2026 Sonata Hybrid’s electronics and build quality as specific reliability concerns, and the model was recalled for the risk of the fuel tank melting. Yes, you read that right.

Hybrid shoppers have more options than ever, and plenty of them are excellent. But the seven vehicles above combine reliability concerns with poor long-term value in ways that matter to your wallet. Before buying any hybrid, use CarEdge’s free depreciation calculator to see what a vehicle is projected to be worth in three to five years — it’s one of the most important numbers most buyers never check. It’s also smart to see the latest Consumer Reports reliability rankings for any hybrid you’re shopping for.If you want expert help identifying which hybrid is actually worth buying for your budget and situation,CarEdge Concierge can do the research and price negotiation for you.

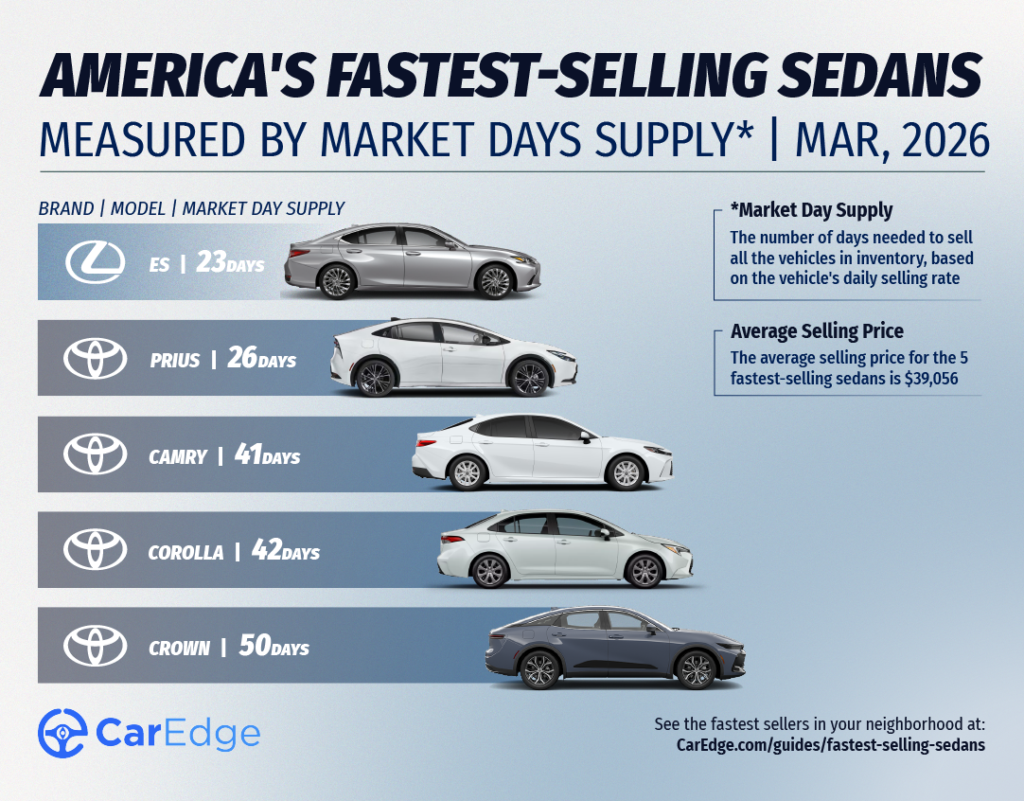

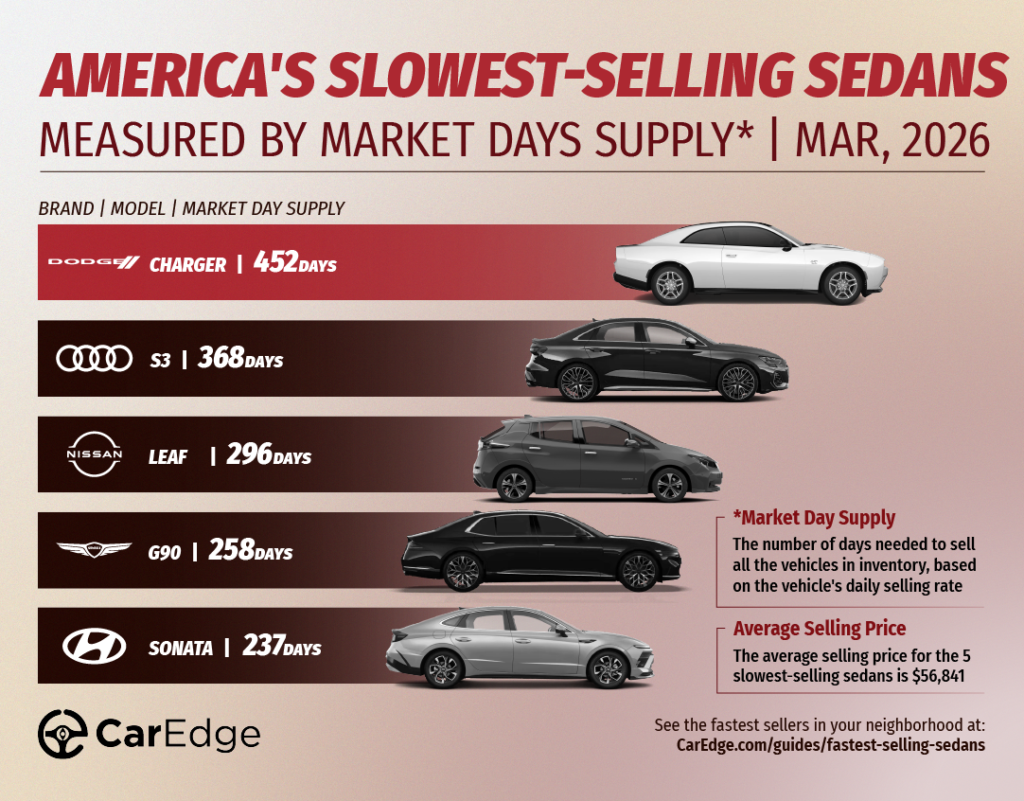

Toyota owns the sedan market right now. Four of the five fastest-selling sedans in America are Toyota or Lexus models. On the other end, the Dodge Charger, Audi S3, and Nissan LEAF are sitting on dealer lots for months at a time, giving buyers real leverage.

Whether you’re shopping for a new sedan or just want to know where the deals are, the data tells the story.

Market Day Supply (MDS) measures how many days it would take to sell all of a model’s current inventory at the current pace of sales. A low MDS means a car is moving fast. A high MDS means it’s sitting.

Under 60 days: Healthy, seller-friendly market. Less room to negotiate. 60-120 days: Balanced. Deals are possible. 120+ days: Oversupply. Buyers hold the leverage.

By the way, it’s smart to familiarize yourself with car buying jargon with our free guide to terms you should know!

| Make | Model | Market Day Supply | Total For Sale | 45-Day Sales | Avg Selling Price |

| Lexus | ES | 23 | 841 | 1,624 | $50,295 |

| Toyota | Prius | 26 | 2,691 | 4,609 | $35,263 |

| Toyota | Camry | 41 | 40,451 | 43,988 | $35,383 |

| Toyota | Corolla | 42 | 26,754 | 28,711 | $25,828 |

| Toyota | Crown | 50 | 1,510 | 1,356 | $48,509 |

The Lexus ES leads the pack with just 23 days of supply. At that pace, every ES on a dealer lot today could be gone in less than a month. The Toyota Prius isn’t far behind at 26 days, which is notable for a car that’s selling at an average of $35,263.

The Camry and Corolla are workhorses here. The Camry has over 40,000 units available, yet dealers are moving nearly 44,000 of them every 45 days. That’s remarkable volume for any vehicle. The Corolla tells a similar story at just $25,828 on average, one of the most accessible price points on this entire list.

The Toyota Crown rounds out the top five at 50 days. It’s a newer, pricier entry in Toyota’s lineup, averaging just over $48,000, yet it’s still selling briskly.

What this means for buyers: If you’re shopping any of these sedans, expect dealer inventory to move quickly and negotiating room to be limited. That said, there’s no excuse to accept forced add-ons or dealer markups. Check CarEdge’s dealer reviews and use our OTD price calculator to know what you should actually be paying before you walk in.

| Make | Model | Market Day Supply | Total For Sale | 45-Day Sales | Avg Selling Price |

| Dodge | Charger | 452 | 8,841 | 880 | $58,300 |

| Audi | S3 | 368 | 614 | 75 | $58,765 |

| Nissan | LEAF | 296 | 1,696 | 258 | $35,160 |

| Genesis | G90 | 258 | 631 | 110 | $101,850 |

| Hyundai | Sonata | 237 | 12,668 | 2,401 | $30,130 |

The Dodge Charger sits at a staggering 452 days of supply. There are nearly 9,000 Chargers on lots across the country, and dealers are moving fewer than 900 of them every 45 days. At $58,300 on average, buyers who walk into a Charger negotiation today have serious leverage.

The Audi S3 is in a similarly tough spot. With only 75 units selling over a 45-day window and 614 on lots, it’s nearing a year of market supply. The S3 is a niche performance sedan, and at nearly $59,000, the market has spoken.

The Nissan LEAF’s struggles are no surprise. Without the federal EV tax credit, EV demand has cooled significantly, and with Nissan holding back on deliveries of the all-new 2026 model, EV buyers aren’t taking it seriously. Nearly 300 days of supply says it all.

The Genesis G90 is an outlier in a different way. Just 110 units sold over 45 days, but that’s almost expected for a six-figure luxury flagship. The question for shoppers is whether dealers are willing to move on price, and with 258 days of supply, the answer is likely yes.

The Hyundai Sonata may be the most interesting data point on this list. It’s a mass-market sedan at $30,130 average, with nearly 12,700 units in inventory. But 237 days of supply means it’s moving slowly despite the affordable price tag. Buyers who want a practical, budget-friendly sedan should take a hard look here.

What this means for buyers: High inventory means more negotiating power. If you’re shopping a slow-selling sedan, come prepared. Use CarEdge Pro to pull real invoice prices and Market Day Supply data for your local market before you negotiate.

If you’re buying a slow-selling sedan, the ball is in your court. Dealers know those vehicles aren’t moving, and that gives you an edge in negotiations. Start by checking CarEdge Car Search to see what’s sitting in your local market.

Shopping a fast-mover like the Camry or ES? You may have less leverage, but you can still protect yourself. Avoid markups, skip the unnecessary add-ons, and lean on CarEdge Concierge if you want an expert to handle the negotiation for you.

The timing couldn’t be worse for Honda. On March 12, the automaker announced it is canceling three electric vehicles that were set to debut later this year: the Honda 0 Series SUV, the 0 Series Saloon, and the Acura RSX. Honda is warning of losses up to $15.8 billion as it overhauls its EV strategy entirely.

In a press release, Honda explained the math behind the decision: “Honda determined that starting production and sales of these three models in the current business environment where the demand for EVs is declining significantly would likely result in further losses over the long term.”

Honda CEO Toshihiro Mibe was blunt about the situation. “Our first priority is to stop the bleeding,” he said. “Then, rebuilding Honda’s future business competitiveness and delivering results is our paramount responsibility.” Mibe added: “Ultimately, the responsibility lies with me. Precisely because of this, without further delay, and to avoid leaving significant liabilities for the future, I made the agonizing decision.”

The company pointed to U.S. market conditions as a key factor, noting that EV demand has slowed “due to several factors including the easing of fossil fuel regulations and revisions to EV incentives.”

That leaves the Honda Prologue as the only fully electric vehicle Honda sells in the United States, after the Acura ZDX was already discontinued. Going forward, Honda says its focus will shift to hybrid powertrains.

Honda acknowledged the broader consequences plainly: “Honda automobile business has fallen into an extremely challenging earnings situation due to various factors, including its inability to respond flexibly to these changes in the business environment.”

Meanwhile, chief rival Toyota is doing the exact opposite.

Since the start of 2026, Toyota has debuted four new electric vehicles for the U.S. market: the all-electric Highlander, the CH-R, the bZ Woodland, and a revamped bZ. Early reviews of models like the 2027 Highlander EV have been strong across the board, and the launches are drawing comparisons to Toyota’s dominance of the hybrid segment, where the RAV4 and Camry are now sold exclusively as hybrids.

Toyota’s patient approach to EVs has long been criticized as slow. Now it’s starting to look like a strategy that paid off. While Ford, GM, and now Honda have taken massive write-downs chasing early EV market share, Toyota built its brand on hybrids, maintained profitability, and is entering the EV market on its own terms with vehicles that are generating genuine enthusiasm.

If you’re shopping for a Honda and want a fully electric vehicle, your only option right now is the Prologue, and its long-term future isn’t exactly certain given Honda’s revised priorities. CarEdge’s total cost of ownership research finds that the Prologue is among the worst EVs for your wallet, earning a D- rating as of 2025. Hybrid shoppers are in better shape: Honda’s hybrid lineup across Accord, CR-V, and others remains strong.

But Honda’s abrupt retreat from EVs raises real questions about its competitiveness over the next decade. Toyota now has a growing EV portfolio backed by a hybrid customer base that trusts the brand on electrification. Honda is starting over.

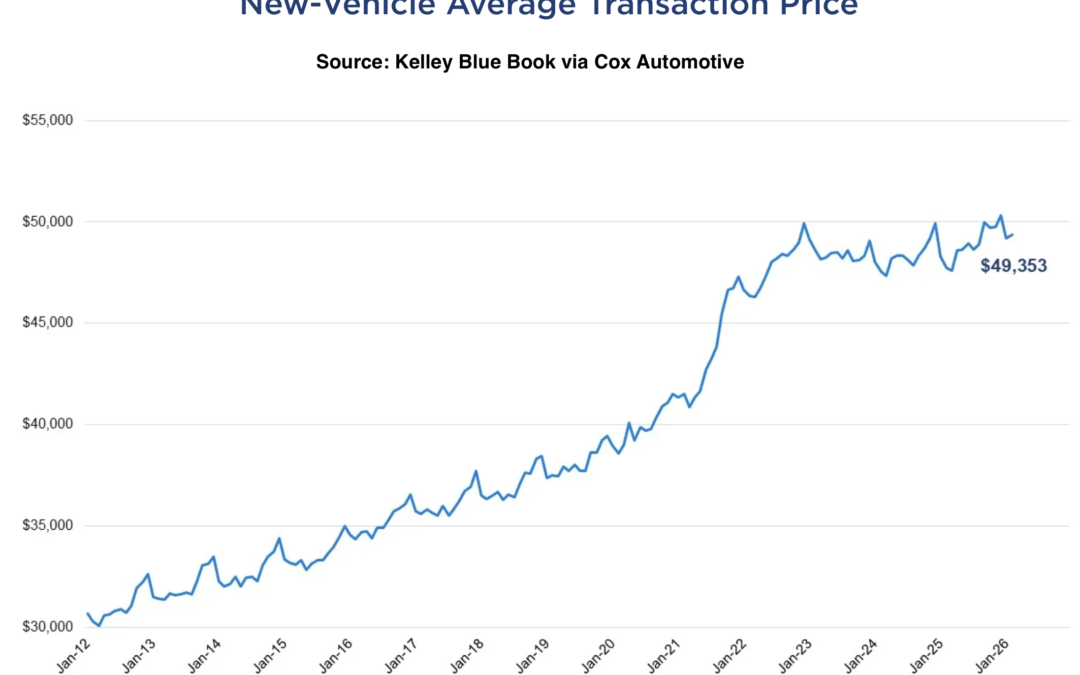

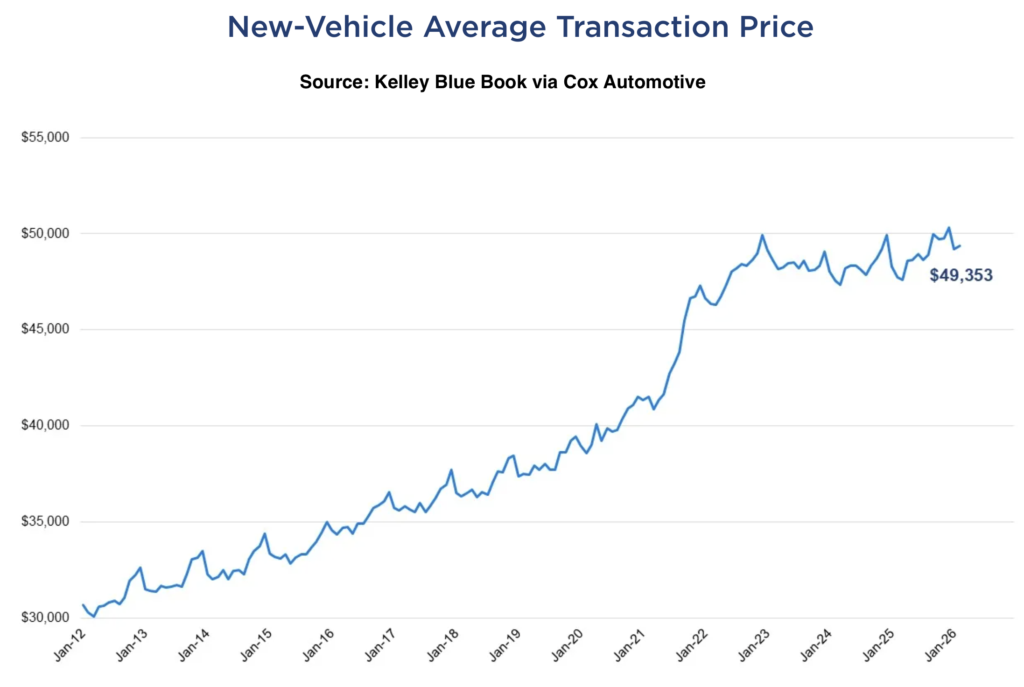

If you’ve seen the headlines this week, you might think buying a new car just got a lot more expensive. According to the latest data from Kelley Blue Book, the average new vehicle transaction price hit $49,353 in February, a 3.4% jump since last year, and one of the bigger annual gains in recent memory.

However, the latest CarEdge analysis of mainstream car prices shows that market averages can be a little misleading. Let’s take a look at the latest new car price updates, and what they mean for car buyers this spring.

Each month, Kelley Blue Book and Cox Automotive publish average transaction price data across the entire new vehicle market. In February, that industry-wide average came in at $49,353, up 3.4% from a year ago. For context, the average annual price increase over the past three years has been closer to 0.9%, so February’s gain stands out.

The average sticker price crossed $50,000 for the eleventh month in a row, landing at $51,440.

On the incentives front, automakers nudged discounts slightly higher. The average incentive package worked out to 6.9% of transaction price in February, up from 6.5% in January. But compared to a year ago, when incentives averaged 7.0%, buyers aren’t actually getting meaningfully more relief. The deals are about the same.

A few segments worth noting:

On the EV side, prices continued to fall. The average EV transaction price dropped 1.4% year over year to $55,300. But automakers are leaning hard on incentives to move them, with the average EV discount now sitting at 14.2% of transaction price. That’s more than double the industry average, which tells you something about where demand actually stands.

Here’s the thing about industry-wide averages: they include everything. Low-volume luxury sedans, six-figure SUVs, exotic sports cars — they all get folded into the same number. When the average gets pulled up by vehicles that represent a small slice of total sales, it can paint a skewed picture of what most car buyers are actually facing.

This kind of headline doesn’t reflect the reality for most shoppers. The cars Americans are actually buying — in massive numbers, month after month — tend to transact well below $49,000.

So what are people actually paying? That’s where our own new car price tracker, the CarEdge Popular 20 comes in.

Every month, CarEdge tracks real transaction prices on the 20 best-selling vehicles in America.

The result is the CarEdge Popular 20, a monthly index that tells you what the market actually looks like for the vehicles most people are shopping for.

The CarEdge 20 isn’t meant to replace the years of great data from the likes of KBB, Cox Automotive, and Edmunds, but it serves as a new datapoint that may provide a better read on the market most consumers are in.

In February, the average transaction price of the 20 top-selling models in America was $42,016, roughly $7,300 below KBB’s industry-wide figure. In March, it nudged up slightly to $42,149, a 0.32% increase. That’s a stable, modest move, not the dramatic price surge the industry-wide average might suggest.

And several of the most popular cars in the country are transacting well under $30,000:

Eight additional models are well under $40,000. These are among the best-selling cars in America, and buyers are getting into them for prices that look a lot different than the $49K headline from KBB.

Within the CarEdge Popular 20, there are a few trends worth watching this month.

The Subaru Outback has seen the biggest price increase since January, up 2.06% to $41,717. The new 2026 Outback didn’t just receive the full SUV treatment for the first time, it also saw a $5,000 increase in the base MSRP.

The Ford Explorer is moving in the opposite direction, with average selling prices down 1.0% to $49,455 in one month.

Trucks are telling a split story. The Ram 1500 is trending up, rising to $60,867 since January. The Ford F-150 is also creeping higher at $61,469. Meanwhile, the Chevrolet Silverado 1500 and GMC Sierra 1500 are both pulling back slightly.

It’s also worth noting that even our Popular 20 truck prices — which average around $59,000 across the four full-size models — are meaningfully below KBB’s full-size pickup segment average of $66,157. That gap likely reflects heavy-duty trims and higher configurations inflating the segment average in KBB’s average price data. The trucks most people are actually buying are cheaper than the headlines imply.

The $49,000 average transaction price from KBB shows just how much new car prices have risen since 2021. It’s especially useful for comparing long-term trends. But the vehicles Americans are actually buying most are transacting around $42,000 on average, and if you’re shopping for a compact SUV, sedan, or subcompact, you’re likely looking at something closer to $30,000 to $38,000.

Knowing what others are actually paying is the most powerful tool you have when you sit down at a dealership. That’s what CarEdge is built to give you.

Want to see what people are paying for the car you’re shopping? Check local car market data on CarEdge before you buy.