CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

In 2026, some SUVs and crossovers are being scooped up as soon as they hit the lot, while others are sitting unsold for more than a year on average. Whether you’re a buyer looking for a deal or a seller trying to time the market, understanding which SUVs are moving (or not) is essential.

We analyzed March car market data to find the SUVs with the lowest and highest market day supply (MDS). MDS is a measure of how many days it would take to sell through current inventory at the current sales pace. Here are the winners and losers in 2026’s SUV market.

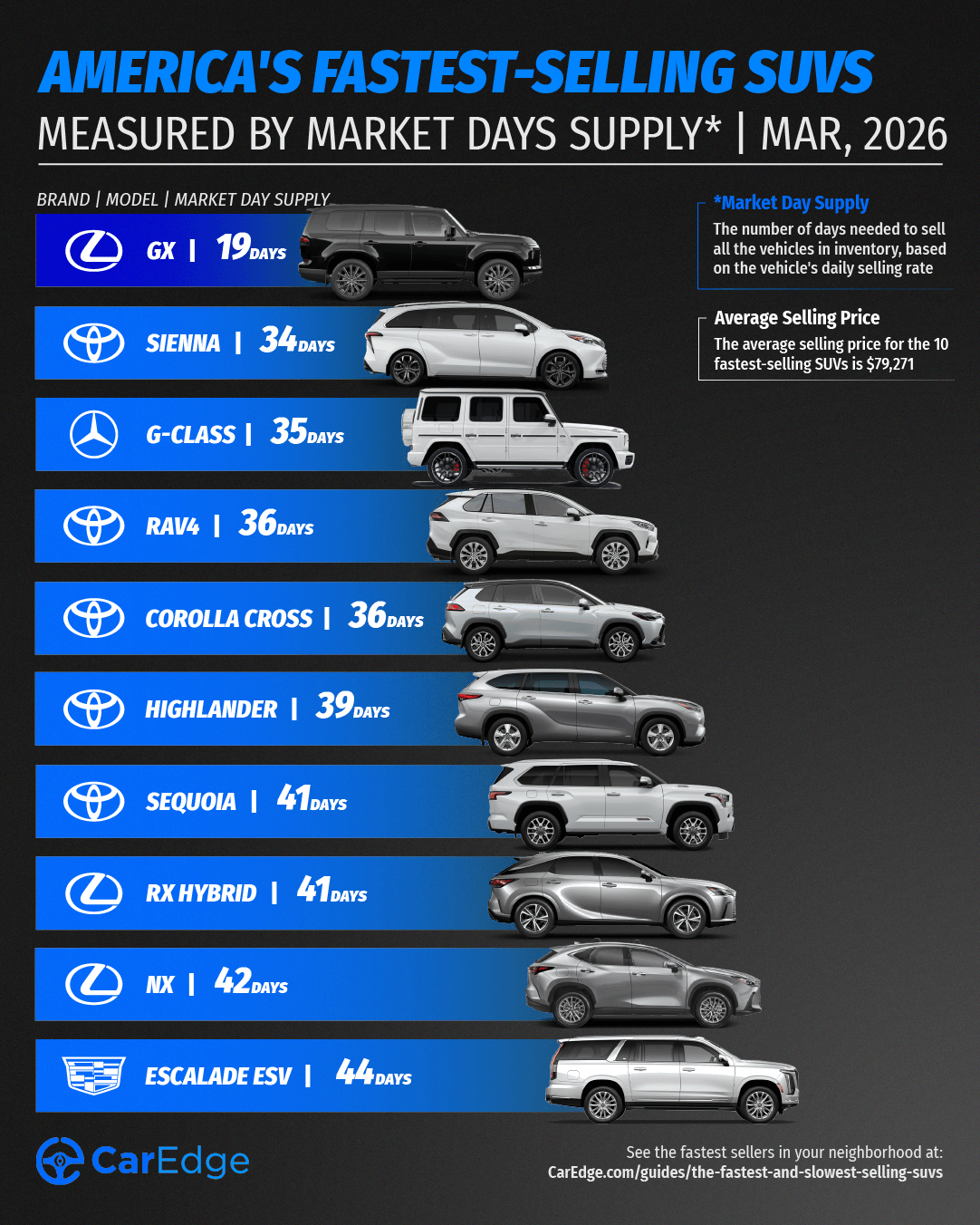

These are the fastest-selling SUVs and crossovers this month. These models have the lowest market day supply, which means they’re in high demand, and are likely harder to negotiate on due to limited availability.

| Make | Model | Market Day Supply | Total For Sale | 45-Day Sales | Average Selling Price |

|---|---|---|---|---|---|

| Lexus | GX | 19 | 1,634 | 3,821 | $81,327 |

| Toyota | Sienna | 34 | 11,277 | 15,032 | $52,582 |

| Mercedes-Benz | G-Class | 35 | 819 | 1,059 | $206,673 |

| Toyota | RAV4 | 36 | 24,644 | 30,490 | $37,950 |

| Toyota | Corolla Cross | 36 | 18,290 | 22,666 | $31,621 |

| Toyota | Highlander | 39 | 8,649 | 9,884 | $54,091 |

| Toyota | Sequoia | 41 | 4,584 | 5,001 | $84,707 |

| Lexus | RX Hybrid | 41 | 5,842 | 6,418 | $64,626 |

| Lexus | NX | 42 | 1,505 | 1,605 | $51,668 |

| Cadillac | Escalade ESV | 44 | 1,270 | 1,296 | $127,469 |

Source: CarEdge Pro

March is yet another month dominated by Toyota and Lexus. The 2026 Lexus GX is the fastest-selling SUV right now, with inventory sitting on the lot for just 19 days on average. The newly-redesigned RAV4 also makes an appearance on the top 10. Cadillac’s Escalade ESV is a quick seller, marking a bright spot for otherwise slow-selling GM models.

What does it all mean? If you plan to buy or lease any of the above SUVs, especially those from Toyota and Lexus, expect to have less negotiating power than if you were to shop one of the slower-selling cars on the market. That doesn’t justify paying for dealer markups or unwanted add-ons. Stay away from those traps. But for these fast-selling SUVs and crossovers, paying MSRP would be a fair deal in 2026’s SUV market.

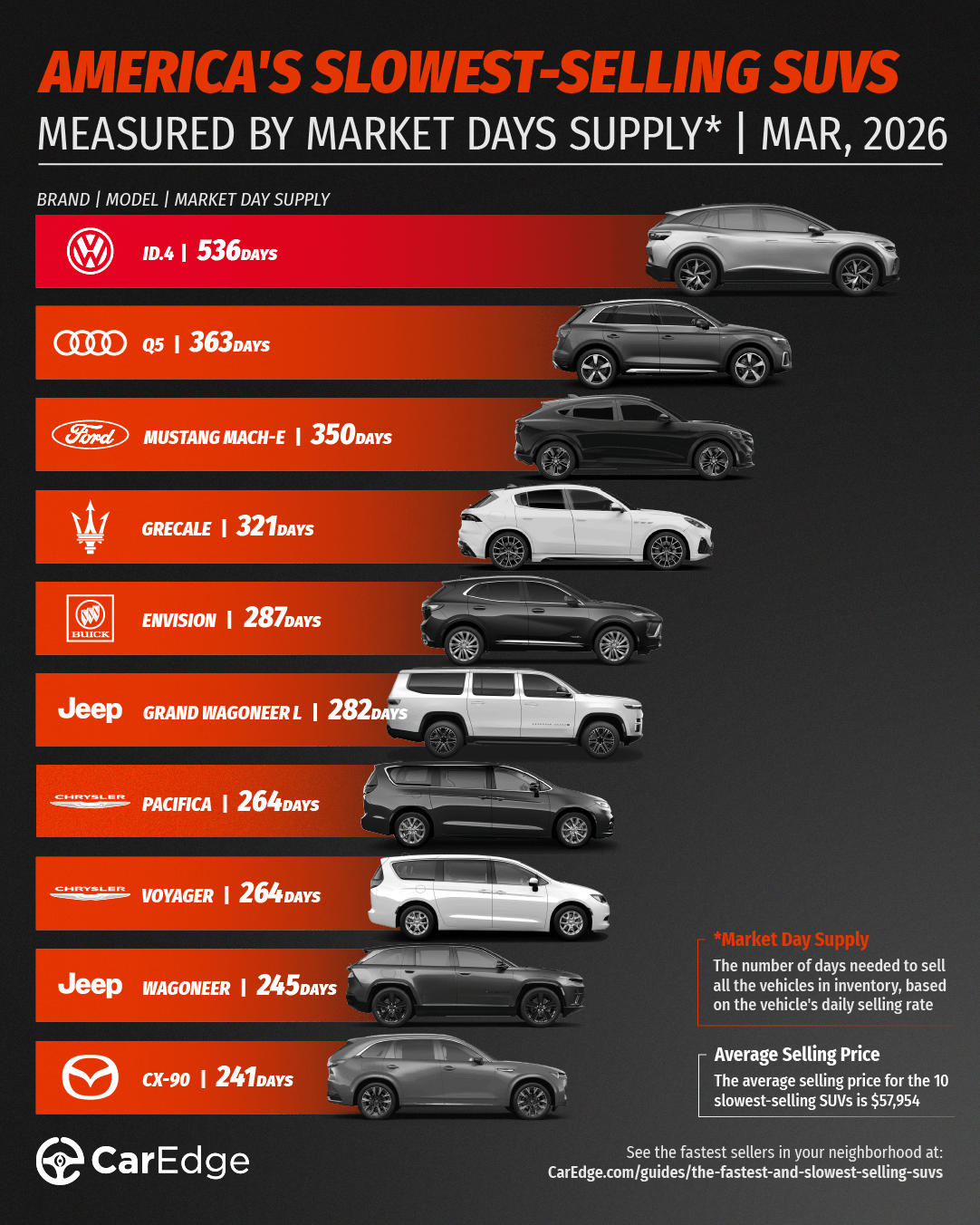

These SUVs have the highest market day supply, which means they’re sitting unsold for longer. Buyers may be able to score better deals on these slowest-selling SUVs in March, especially with this AI negotiator doing the work for you.

| Make | Model | Market Day Supply | Total For Sale | 45-Day Sales | Average Selling Price |

|---|---|---|---|---|---|

| Volkswagen | ID.4 | 536 | 1,464 | 123 | $48,489 |

| Audi | Q5 | 363 | 6,696 | 830 | $55,892 |

| Ford | Mustang Mach-E | 350 | 10,748 | 1,381 | $47,273 |

| Maserati | Grecale | 321 | 741 | 104 | $83,840 |

| Buick | Envision | 287 | 14,386 | 2,252 | $42,821 |

| Jeep | Grand Wagoneer L | 282 | 2,131 | 340 | $85,074 |

| Chrysler | Pacifica | 264 | 17,581 | 3,000 | $47,333 |

| Chrysler | Voyager | 264 | 2,349 | 400 | $40,670 |

| Jeep | Wagoneer | 245 | 6,717 | 1,234 | $79,818 |

| Mazda | CX-90 | 241 | 18,382 | 3,436 | $48,326 |

Source: CarEdge Pro

With the federal EV tax credit now over, the Volkswagen ID.4 is at the top of the list for the third month in a row, with well a year and a half of supply at current daily sales rates. The Ford Mustang Mach-E, previously a top-selling EV, is now taking about a year to sell. Several of the others fall into the luxury segment. With recent inflation and persistently high interest rates, buyers are thinking twice about buying luxury vehicles.

Five Stellantis models are in the bottom 10 this month. Maserati, Jeep, and Chrysler all make an appearance. Jeep’s Grand Wagoneer has been a slow-selling model for most of the past year, despite seeing major price cuts several months ago.

For any of these slow-selling SUVs, prices will be more flexible if you come equipped with negotiation know-how.

If you’re looking for a deal, start with the slowest sellers this month. High inventory levels mean dealers are likely motivated to talk pricing if you negotiate with confidence. It’s always best to take a look at the best incentives of the month, too.

“If you’re shopping for a slow-selling SUV, the ball is in your court,” says auto industry veteran Ray Shefska. “Dealers know those vehicles aren’t moving, and that gives you the upper hand in price negotiations.”

Shopping Toyota, Honda, or Lexus? Expect tighter inventory and less room for negotiation. You may need to move quickly if you find the right trim. However, this is no reason to pay for unwanted add-ons or dealer markups!

With CarEdge Concierge, our experts do the legwork for you, from researching inventory to negotiating with dealers. Already know what you want? Use our AI Negotiation Expert service and have CarEdge AI negotiate with car dealers anonymously!

Explore more free tools and resources with car buying guides, cost of ownership comparisons, and downloadable cheat sheets. There’s no reason to shop unprepared in 2026.

CarEdge is a trusted resource for car buyers, offering data-backed insights, negotiation tools, and expert guidance to help consumers save time and money. Since 2019, CarEdge has helped hundreds of thousands of drivers navigate the car-buying process with confidence. Learn how to buy a car the easy way at CarEdge.com.

The gap between the fastest and slowest-selling pickups is widening in 2026. With some trucks selling in just over a month, and others sitting unsold for over six months, knowing what’s hot (and what’s not) can make or break your next deal.

That’s why understanding Market Day Supply (MDS) is more important than ever for anyone buying or selling a truck in 2026. At CarEdge, we used real-time inventory and sales data to identify the fastest- and slowest-selling trucks each month.

MDS tells us how long it would take to sell all the current inventory of a particular model at the current sales pace, assuming no new units are added. A low MDS means a truck is selling quickly. A high MDS, on the other hand, signals oversupply, and that can mean buyers have more leverage at the dealership.

Whether you’re buying new or considering a trade-in, here’s what the latest market data from CarEdge Pro reveals about the best-selling and worst-selling trucks in America.

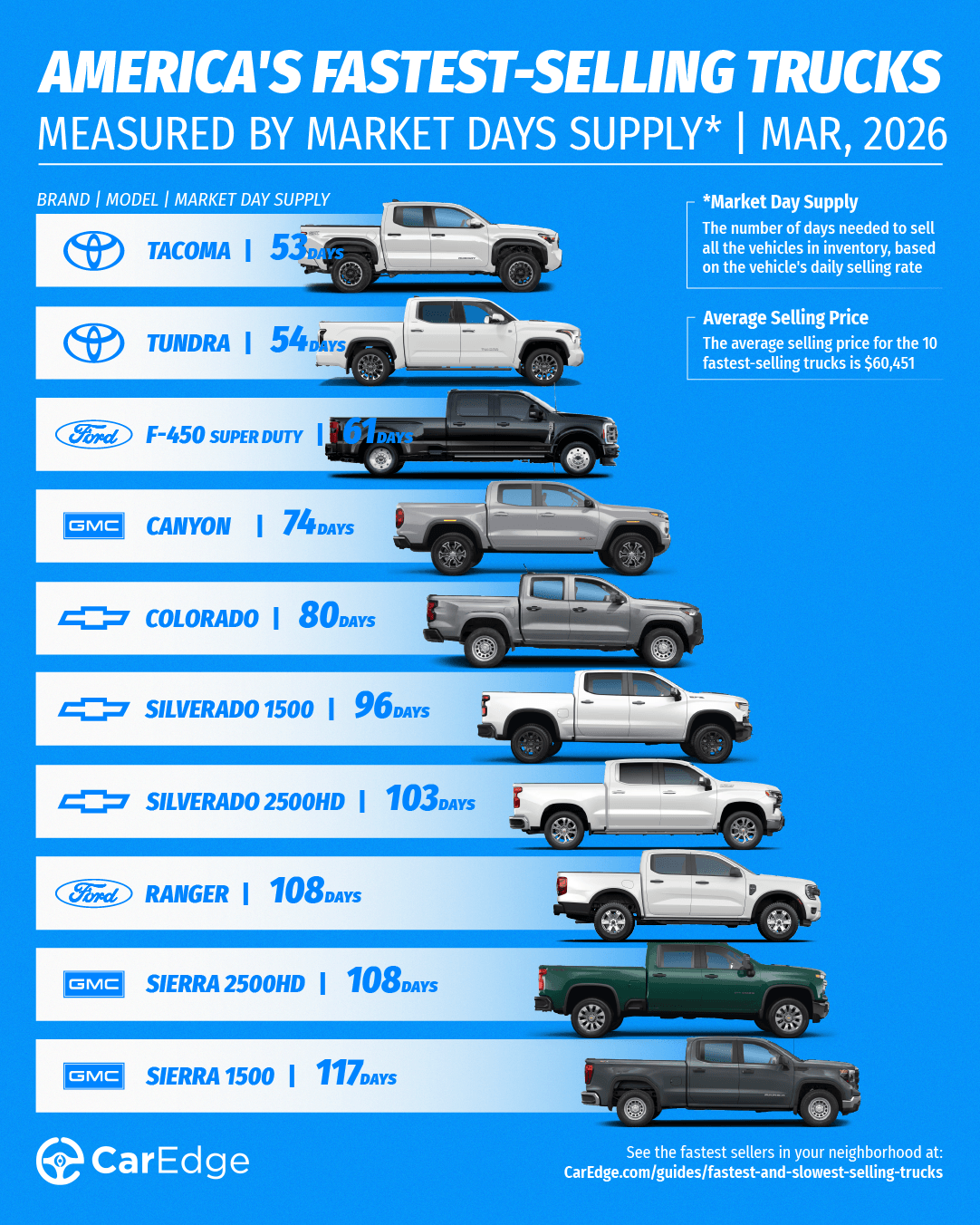

These trucks are in high demand and selling quickly. But if you’re hoping to negotiate a deal on one of these, don’t count on much wiggle room unless you work with a pro.

| Make | Model | Market Day Supply | Total For Sale | 45-Day Sales | Average Selling Price |

|---|---|---|---|---|---|

| Toyota | Tacoma | 53 | 57,692 | 49,012 | $46,088 |

| Toyota | Tundra | 54 | 32,123 | 27,006 | $63,936 |

| Ford | F-450 Super Duty | 61 | 1,459 | 1,084 | $98,065 |

| GMC | Canyon | 74 | 8351 | 5062 | $48,580 |

| Chevrolet | Colorado | 80 | 14,751 | 8,347 | $41,844 |

| Chevrolet | Silverado 1500 | 96 | 60,578 | 28,333 | $52,911 |

| Chevrolet | Silverado 2500HD | 103 | 23,205 | 10,174 | $66,488 |

| Ford | Ranger | 108 | 17251 | 7215 | $42,842 |

| GMC | Sierra 2500HD | 108 | 17027 | 7116 | $81,410 |

| GMC | Sierra 1500 | 117 | 51,631 | 19,941 | $62,347 |

Source: CarEdge Pro

The Toyota Tacoma is the fastest-selling pickup truck in March 2026. On average, this heavy duty pickup truck sits on the lot for a little under two months before finding a buyer. Toyota’s Tundra and the Ford F-450 Super Duty are in second and third place, with trucks from GM far behind.

These trucks will be less negotiable as demand exceeds what’s typical for the truck market. Still, never agree to dealership markups or forced add-ons. Remember, informed shoppers always get the best deals.

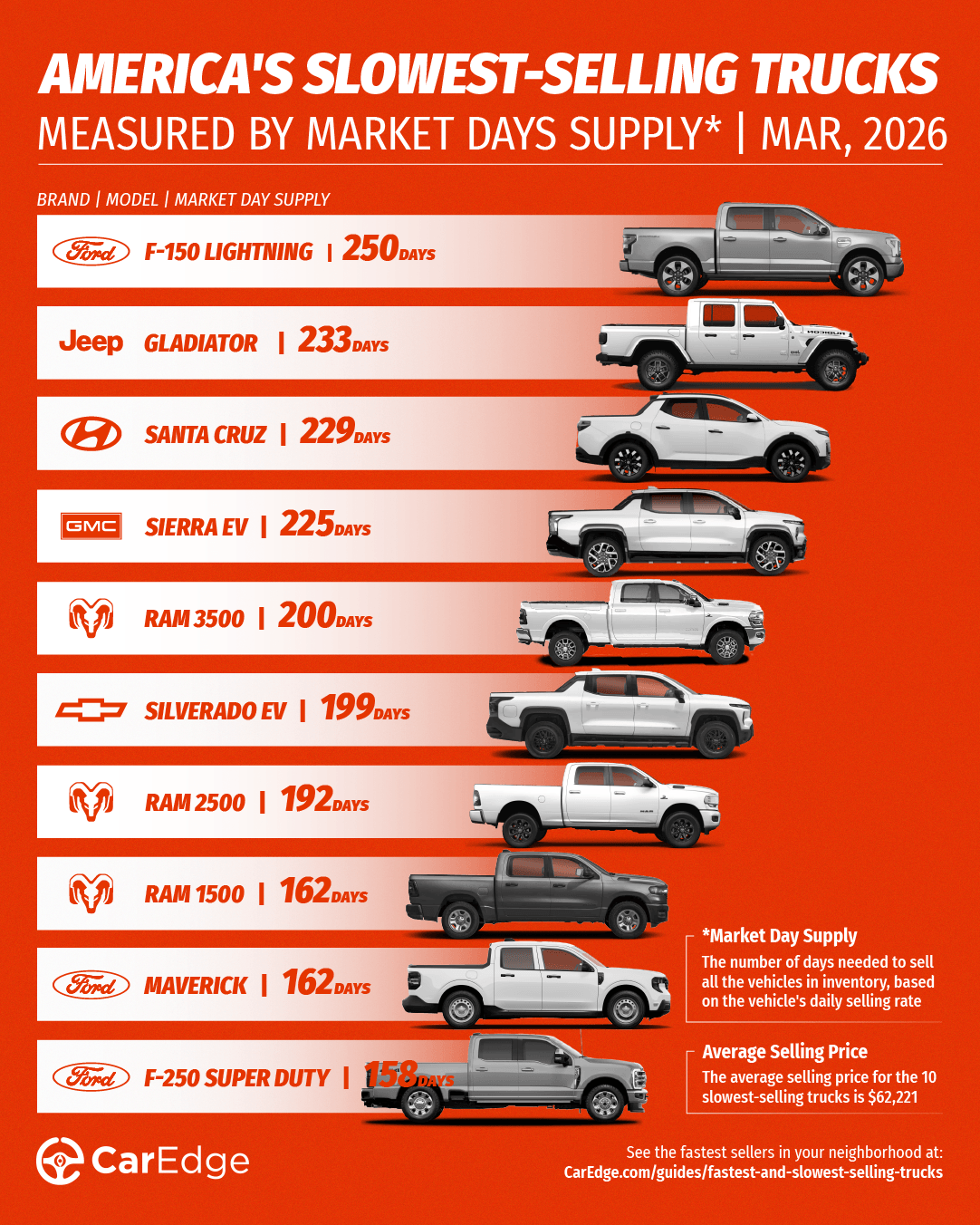

On the flip side, these trucks are struggling to move. Some of these trucks are taking more than six months to sell on average. If you’re in the market, these pickup trucks offer room for negotiation, especially with DIY market insights.

| Make | Model | Market Day Supply | Total For Sale | 45-Day Sales | Average Selling Price |

|---|---|---|---|---|---|

| Ford | F-150 Lightning | 250 | 3,931 | 707 | $67,631 |

| Jeep | Gladiator | 233 | 21,173 | 4,090 | $48,732 |

| Hyundai | Santa Cruz | 229 | 9,641 | 1,892 | $36,439 |

| GMC | Sierra EV | 225 | 2,611 | 522 | $81,439 |

| Ram | Ram 3500 | 200 | 12021 | 2702 | $77,020 |

| Chevrolet | Silverado EV | 199 | 1,897 | 429 | $74,864 |

| Ram | Ram 2500 | 192 | 32,561 | 7,646 | $68,554 |

| Ram | Ram 1500 | 162 | 70,156 | 19,469 | $60,056 |

| Ford | Maverick | 162 | 43,056 | 11,948 | $33,930 |

| Ford | F-250 Super Duty | 158 | 40,633 | 11576 | $73,547 |

Source: CarEdge Pro

In March, the F-150 Lightning is the slowest-selling truck in America. Ford recently announced that the fully-electric version will be replaced with a different electrified option for the next model year. The Hyundai Santa Cruz is also one of the slowest-selling pickups, a truck that was recently sent to the graveyard. Trucks from Stellantis brands (Ram and Jeep) take up four of the bottom 10 spots in March. Sellers can expect these slow-selling trucks to sit on the lot for at least four months, but this creates great chances to negotiate savings for buyers.

As the truck market ebbs and flows, it’s easy to become overwhelmed. Luckily, there are new tools and services available that take the hassle out of buying a truck entirely. Here’s how CarEdge can help.

👉 Negotiate anonymously with CarEdge (NEW!)

👉 Have a pro negotiate your deal with CarEdge’s Car Buying Service

Most car buyers negotiate with one dealer at a time. They find a car they like, visit the lot, sit across from a salesperson, and try to talk the price down. It rarely works well, and there’s a simple reason why.

When you’re negotiating with one dealer, you’re on their turf and playing by their rules. But when multiple dealers know they’re competing for your business, the dynamic flips completely. The buyers who consistently get the best deals aren’t better negotiators. They just know how to create competition.

Here’s exactly how to do it.

A lot of buyers go into the process already defeated, assuming the price is the price and there’s nothing to be done. That’s not how dealerships work in 2026.

Back in 2021-2022, dealers had the upperhand as car inventory was thinned out due to the semiconductor shortage. But those days are well behind us.

In 2026, the car market has mostly normalized. Every dealer has monthly sales targets to hit, and pressure from the manufacturer to move units. As sales for several brands slow, many are even battling their own floorplanning costs on aging inventory. When the right conditions are in place, dealers have very real motivation to compete on price. The key is making sure they know they have to.

A dealer who believes you’re ready to sign today is a different animal than one who knows you’re getting quotes from three other stores down the road. Your job is to be the second kind of buyer.

Playing dealers against each other only works if you know what a fair price looks like. Otherwise you can’t tell a good offer from a mediocre one.

When shopping new car lots, start with the dealer invoice price. This is what the dealer actually paid the manufacturer for the vehicle, and it’s the number your negotiation should be anchored to — not the sticker price. When you know the invoice price, you know how much room the dealer has to move and whether the offer they’re presenting you is reasonable or inflated. CarEdge publishes invoice prices for free, because that information shouldn’t only be available to dealers. For slow-selling cars, you should be able to get close to the invoice price. Dealers have other ways of making money on each vehicle, so don’t hesitate to work towards that goal.

Regardless of whether you’re buying new or used, check how long the car has been sitting on the lot, and the local Market Day Supply for that year, make, and model. This metric measures how many days current inventory would last at the current rate of sales. A model sitting at 90-plus days of supply is one where dealers are motivated and inventory is plentiful. A car with 20 days of supply is flying off lots, and you’ll have far less leverage. Knowing this before you make a single call tells you how hard to push and whether your expectations are realistic.

Next, check CarEdge Dealer Reviews. Not every dealer negotiates in good faith, and walking into a store with a reputation for bait-and-switch tactics or high-pressure sales puts you at a disadvantage before you say a word. CarEdge Dealer Reviews surface real buyer experiences so you can identify which dealers in your area are worth your time and which ones to skip.

This prep work takes 15 minutes and changes everything about how the conversations go.

Once you know the market and have a short list of reputable dealers, contact at least three of them, and even more if the car you want is in high demand.

Do this by email or text, not phone. Written communication keeps everything documented, removes the time pressure that phone calls create, and makes it easy to share competing offers later. Be straightforward in your message: tell them you’re shopping the same vehicle at multiple dealerships, you’re ready to move when the price is right, and you’d like their best out-the-door price.

Some dealers will come in strong right away to win your business early. Others will lowball hoping you’ll bite. Either way, you now have real numbers to compare.

Here’s where it gets effective: once you have two or three quotes in hand, go back to your preferred dealer with the lowest competing offer. This could be the dealer with the nicer car, or simply the one with the nicer salesperson. Most will match or beat it rather than lose the sale to a competitor down the street. That’s not a negotiating trick. It’s just how business works, and savvy buyers have been doing it for decades.

Market Day Supply is worth revisiting once you’re in active negotiations. If the model you want has high supply nationally, push hard. Dealers on slow-moving inventory are motivated, and below-MSRP pricing is a realistic outcome.

If supply is tight on your first choice, consider whether a different trim, a different color, or a comparable model with more inventory might serve you just as well. Walking away from a low-supply vehicle and coming back in two weeks is a legitimate strategy. So is simply walking away. Dealers know that buyers who leave often return, and they’ll sometimes call with a better number before you do.

Fortunately for consumers, it’s quite easy to get car dealerships to compete for your business. Here’s.a quick rundown of what you can do to make negotiating savings easier than you could imagine:

1. Check the invoice price so you know what the dealer actually paid and what a fair target looks like.

2. Look up Market Day Supply to gauge how much leverage you have before you contact anyone.

3. Research dealers using CarEdge Dealer Reviews to filter out bad actors before you waste time on them.

4. Contact at least three dealers by email or text and ask for their best out-the-door price.

5. Take the lowest competing offer back to your preferred dealer and ask them to match or beat it.

If supply is tight on your first choice, be willing to pivot — different trim, color, or model — or simply walk away and revisit in a few weeks. No matter what, NEVER be a monthly payment shopper. Always get the written out-the-door price including all taxes and fees.

If this process sounds like more work than you want to take on, that’s a fair read. CarEdge Concierge exists for exactly this reason.

The Concierge team runs the multi-dealer process on your behalf — contacting dealers, collecting quotes, and negotiating pricing without you ever sitting in a showroom. They also know from experience which dealers are straightforward to work with and which ones aren’t worth the trouble.

It’s the same strategy outlined above, handled by people who do it every day. On average, CarEdge Concierges save drivers between $2,000 – $3,000 through expert negotiations.

Learn more about our Car Buying Service to see if it’s right for you.

When you walk into a dealership, the sticker price on the window isn’t the starting point. It’s usually somewhere in the middle. Dealers pay one price for a car and charge you another, and sometimes padded with extras you never asked for.

Here’s a breakdown of how new car pricing actually works, where markups stand today, and how to use that knowledge to your advantage.

Every new car has two key prices worth knowing.

The invoice price is what the dealer paid the manufacturer for the vehicle. It’s not a secret, but dealers rarely advertise it. CarEdge publishes free invoice prices because we believe buyers deserve to know what they’re negotiating against.

The MSRP (Manufacturer’s Suggested Retail Price) is the sticker price. It’s set by the manufacturer and already includes a built-in profit margin for the dealer. Most buyers think of MSRP as the ceiling of negotiation. In reality, it’s often just the floor.

On top of the MSRP, many dealers add on extras — paint protection packages, wheel locks, nitrogen-filled tires, window tinting — that cost them very little but get bundled into the deal for $500 to $2,000 or more. Always ask for an itemized breakdown before you sign anything, and check out our guide to dealer add-ons to watch out for.

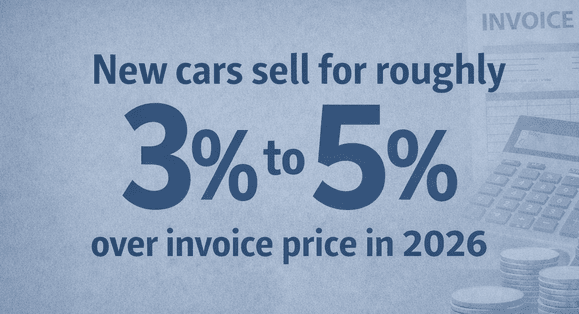

Across the board, new cars are selling for roughly 3% to 5% over invoice price in 2026.

For mainstream brands like Toyota, Honda, Ford, and Chevrolet, most models are sitting around 3% over invoice. High-demand models like the new Toyota RAV4, a Honda Civic, or a top trim of the Ford F-150 can push that closer to 5%.

For most new cars, that equals between $1,000 and $4,000 over invoice to land at the advertised MSRP, assuming there are no dealership add-ons. More on that in a bit.

Luxury and sports cars are a different story. Brands like BMW, Mercedes-Benz, and Volvo tend to land at 5% over invoice or higher, and because the base prices are already elevated, the dollar amounts get significant fast. We can also see higher markups for high-end trucks like the F-150 Raptor, Ram 1500 TRX, or any model listed over $80,000.

CarEdge Concierge Jamer Heasley sees this play out regularly: “It’s common to see new cars priced $2,000 to $3,000 over MSRP. For luxury brands like Volvo, Mercedes-Benz, and BMW, 5% over invoice is common, and with higher prices, that often ends up in the $4,000 to $6,000 range.”

Here’s the part most buyers don’t hear: plenty of new cars are sitting on lots, and dealers with slow-moving inventory are often willing to deal.

CarEdge co-founder Ray Shefska, who spent years on the dealer side before starting CarEdge, puts it this way: “For the slowest-selling cars in America, it’s common to negotiate well below MSRP. A great deal is anything close to invoice price, or for last year’s models, even below the invoice price.”

A good indicator of how much leverage you have is Market Day Supply. MDS is a measure of how long current inventory would last at the current sales pace. A car with 90-plus days of supply is one where you hold the cards. A car with 20 days of supply? The dealer knows you’re competing with other buyers.

The best negotiators walk in knowing more than the salesperson expects. Here’s how to get there.

Know the invoice price. CarEdge publishes invoice data for free. See your invoice price here. Start every negotiation with that number in mind, especially for slower-selling models, or any car that’s been sitting on the lot for months.

Check Market Day Supply. Before you fall in love with a specific car, look up how it’s selling nationally. High supply means more room to negotiate. Low supply means you may need to adjust your expectations or consider alternatives. CarEdge Pro makes it easy.

Make dealers compete. Contact multiple dealers and let them know you’re shopping around. Email works well here — it keeps things documented and removes the pressure of a showroom.

Separate your trade-in. Dealers often blend the trade-in and new car numbers to obscure what you’re actually paying. Negotiate the new car price first, then talk trade. Take our trade-in checklist with you.

Watch for add-ons and fake fees. If a dealer says certain packages are “already installed,” ask for an itemized list and push back on anything you didn’t request. Here’s what to watch out for.

If you’d rather skip the back-and-forth entirely, CarEdge Concierge handles the negotiation for you. Jamer and the team work directly with dealers on your behalf to secure below-MSRP pricing, saving buyers $2,200 on average.

Schedule your free Concierge consultation today

In 2026, dealers are marking up new cars 3% to 5% over invoice on average, with luxury and high-demand models pushing higher. That gap is real money — often thousands of dollars. But it’s also negotiable, especially if you know the numbers going in.Check invoice prices and Market Day Supply for free on CarEdge before your next car purchase. Or let our Concierge team handle it for you.

The days of affordable new cars are almost over. In a market where the average new car now costs nearly $50,000, a small window of opportunity still exists for buyers hunting for a bargain. According to CarEdge data, there are 3,027 new cars currently listed for sale under $20,000 across the country. These are all leftover 2025 (and even 2024) models that dealers are discounting below MSRP to clear out, creating a rare and fleeting opportunity to save.

No automaker is currently producing a new vehicle with an MSRP under $20,000. These are the last ones.

Here’s a complete breakdown of every new car for sale under $20,000 right now, according to CarEdge Car Search. These are all unsold 2024-2025 models listed below MSRP:

| Model | Units Available | Priced As Low As |

| 2025 Nissan Versa | 2,381 | $15,249 |

| 2025 Nissan Sentra | 254 | $16,732 |

| 2025 Nissan Kicks | 223 | $16,820 |

| 2024 Mitsubishi Mirage | 67 | $13,995 |

| 2025 Kia Soul | 65 | $18,452 |

| 2025 Hyundai Elantra | 55 | $18,540 |

| 2025 Hyundai Venue | 27 | $18,321 |

The Nissan Versa alone accounts for nearly 80% of available inventory. The Mitsubishi Mirage, listed as low as $13,995 and below its original MSRP, is the most affordable new car you can buy in America right now. But with only 67 units left nationwide, you’ll need to act fast.

Finding a car listed under $20,000 is only half the battle. Dealer markups and add-ons can quickly push that price well above your budget before you ever sign anything.

Here’s how to protect yourself:

Always ask for the out-the-door price. The advertised price is rarely what you’ll actually pay. The out-the-door (OTD) price includes all taxes, fees, and dealer charges specific to your zip code. That’s the number that matters, not the sticker, not the online listing. Get the OTD price in writing before you set foot in a dealership.

Check out our free OTD price calculator to estimate what you’ll be spending.

Call ahead to confirm availability. With only a few thousand of these cars spread across thousands of dealers nationwide, inventory can move fast. Before making the trip, contact the dealer directly to confirm the car is still on the lot.

Watch out for forced add-ons. Some dealers will advertise a shockingly low price, then load the deal with thousands in extras: paint protection, fabric coating, tire and wheel packages, and more. These add-ons are almost always negotiable or refusable. If a dealer insists on bundling them, walk away. Here’s a list of common dealership add-ons to watch out for.

Get pre-approved financing before you shop. Even on a $16,000 car, the finance office is where dealers make money. Come in with a pre-approved offer from your bank or credit union. It gives you leverage and keeps the focus on the OTD price rather than monthly payments. If the dealership can beat your offer from the bank, there’s no harm in financing with them.

Don’t fall for the monthly payment trap. With a high interest rate, a $19,000 car stretched over 84 months can cost you more in interest than the car is worth. Focus on the total cost, not the monthly payment. Stick to loan terms of 60 months or fewer on a vehicle in this price range.

Price isn’t the only thing that matters. For many budget shoppers, it may be worth it to spend a little more for a safer vehicle, especially since these are compact cars and hatchbacks.

Hyundai Elantra is the standout. It earned an IIHS Top Safety Pick+, the highest designation IIHS awards, along with a 5-star overall NHTSA rating, and it comes standard with a full suite of driver-assist features. For buyers who want the most car for their money from a safety standpoint, the Elantra is the easy recommendation.

Nissan Versa and Nissan Kicks are solid but not top-rated. The Versa earns “Good” scores in its IIHS-tested categories and a 5-star NHTSA overall rating. The Kicks comes standard with Nissan’s Safety Shield 360 across all trims, including automatic emergency braking, blind spot warning, and rear cross traffic alert, and scores well in IIHS crash tests. Neither earned a Top Safety Pick designation, but both are reasonable choices.

Mitsubishi Mirage deserves a direct warning. At $13,995, it’s the cheapest new car in America right now, and that price is tempting. But the Mirage hatchback has recorded 13.6 fatal accidents per billion miles traveled, roughly 4.8 times the national average and one of the worst real-world fatality rates of any vehicle currently on the road. IIHS crash tests show poor scores.

This isn’t a reflection of failed crash tests so much as basic physics: small, light cars are at a significant disadvantage in collisions with the larger trucks and SUVs that dominate American roads. If safety is a priority, the Mirage’s low price comes with a real tradeoff.

Kia Soul and Hyundai Venue fall somewhere in the middle. Neither earned a 2025 IIHS Top Safety Pick, and the Venue has a concerning real-world fatality record similar to the Mirage. The Soul is the better of the two from a safety perspective, but neither matches the Elantra.

Bottom line: If you’re shopping this list and safety matters to you, spend the extra few hundred dollars and get the Hyundai Elantra, or something larger (with high crash test ratings) that’s a little over the $20,000 threshold. The Honda Civic is one example worth the test drive.

2026 will go down as the last year a buyer can walk into a dealership and drive home a brand-new car for under $20,000. No manufacturer currently has a sub-$20K model in production, and with rising material costs, labor expenses, and tariffs keeping new car prices elevated, there’s no sign that will change.

These remaining vehicles will likely be gone by summer. If buying a new car under $20,000 is your goal, now is the time to act.

Use CarEdge’s free tools to check dealer invoice prices, local inventory, and get the out-the-door price before you shop.