Car Insurance Rates Soared 24% in 2023 – Here’s the forecast for 2024

As we step into 2024, American drivers are noticing a larger auto insurance bill with their policy renewals. Based on an analysis of 97 million auto insurance quotes from Insurify, a clear picture emerges of the key trends in car insurance prices for this year. We’ll examine the factors driving up costs, and take a look at how consumers and the industry are adapting.

Record-High Rates in 2023 Set the Stage For More Increases in 2024

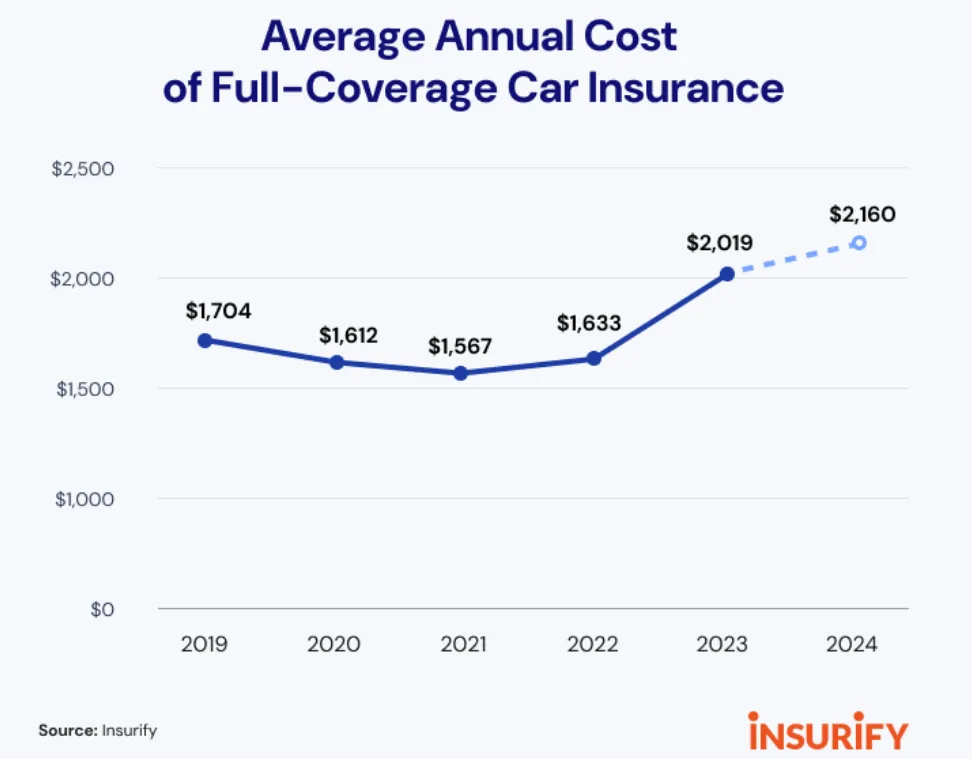

In 2023, auto insurance rates in the U.S. climbed 24% to an all-time record high. The spike in rates was driven by rising repair costs, natural disasters, and more frequent car accidents. This uptick in insurance costs led to record losses for insurers. The latest data suggests that car insurance premiums aren’t done climbing. Insurify projects that car insurance rates will increase by 7% in 2024. That’s almost double the typical annual rise.

The national average cost of a full-coverage policy now stands at $2,019 per year, amounting to 2.6% of the median household income. In comparison, state-minimum liability insurance averages at $1,154 annually.

The Wage-Insurance Gap Worsens

In 2023, car insurance rates increased by 638% more than the average wage growth. Nearly 62% of Americans reported a rise in their car insurance rates, and about 22% experienced more than one increase in the same year.

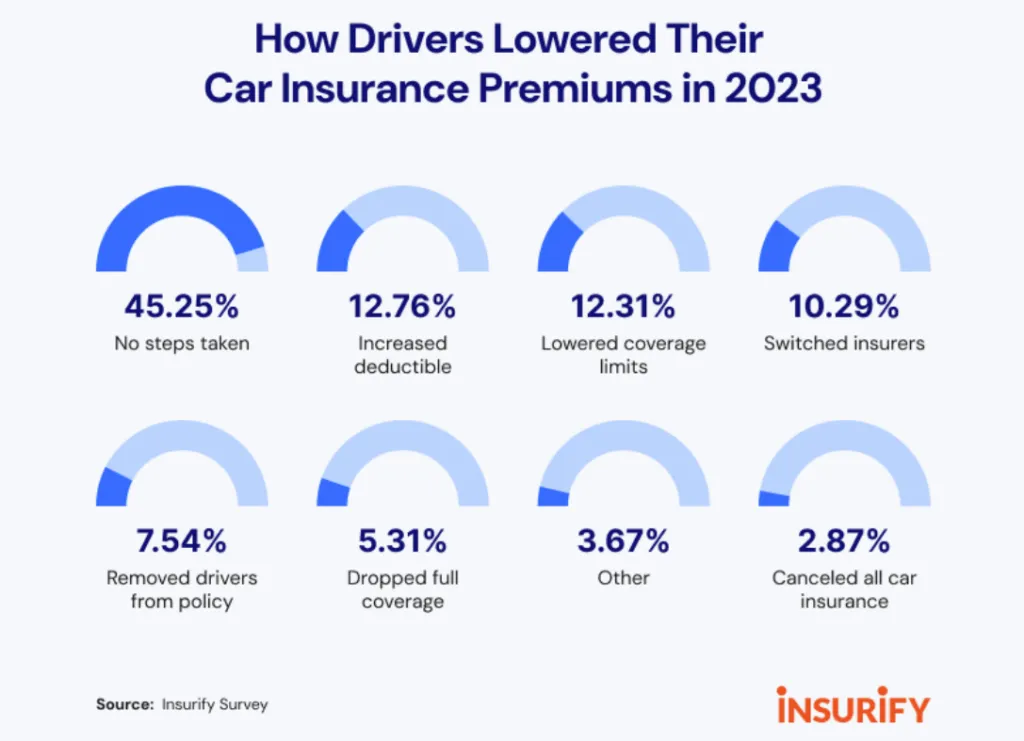

To combat these hikes, many drivers opted to lower their coverage limits or increase their deductibles. Insurify’s data shows that most drivers took action to reduce their premiums, often accepting more risk in exchange for lower monthly premiums.

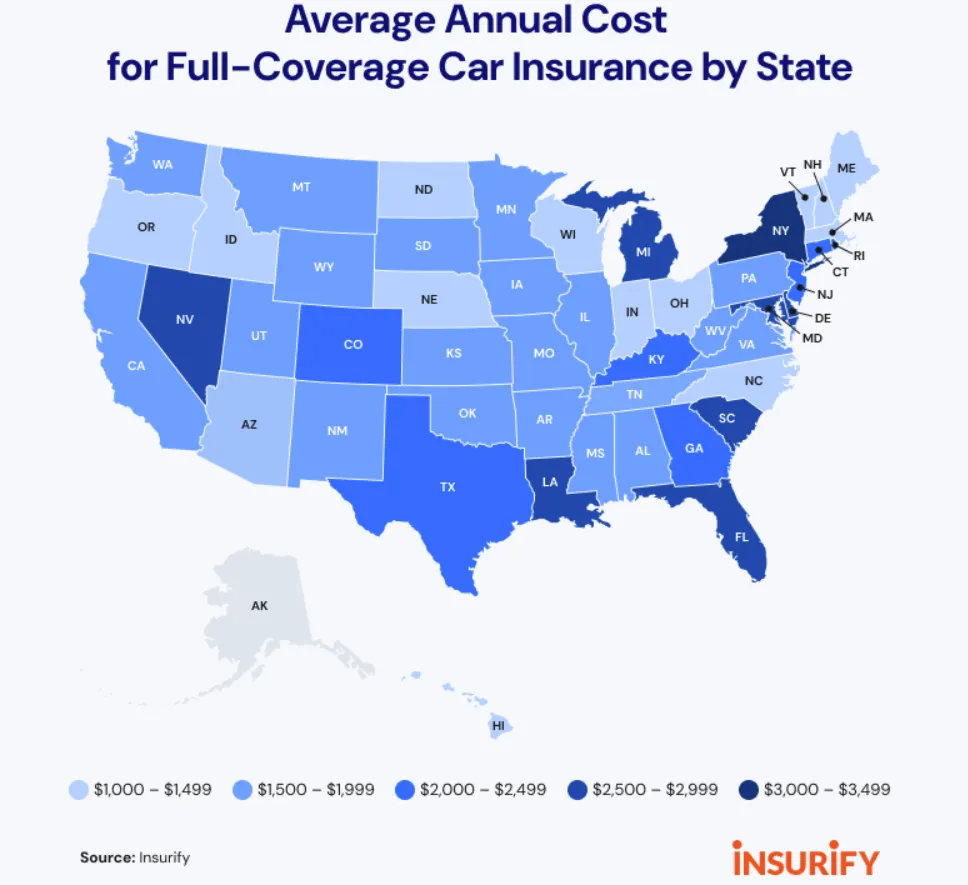

New York stands out with the highest car insurance costs in the country, averaging $3,374 annually for a full-coverage policy.

States with lower incomes are feeling the brunt of these insurance cost increases. Drivers in these states spend a larger portion of their earnings on car insurance, exacerbating the financial strain on households already facing economic challenges.

The Insurance Industry Is In Trouble

The past few years have been tough for the insurance industry. After suffering a $3.8 billion net underwriting loss in 2021, losses deepened to $26.9 billion in 2022. 2023’s numbers are still pending, but there were some signs of a recovery late in the year.

The rising costs of maintenance and repairs, increased severity of accidents, and pandemic-induced market fluctuations have all contributed to these losses. The Bureau of Labor Statistics reported an 8.46% increase year-over-year in auto repair costs as of November 2023.

Advanced vehicle technologies and electric vehicles bring new challenges, with repair costs for high-tech cars and EVs like Tesla being substantially higher. Insurance companies are increasingly forced to choose between writing a check for a $20,000 repair bill after a seemingly minor accident, or writing the car off altogether.

How Can Drivers Save On Auto Insurance in 2024?

In light of the rising car insurance rates, here are some practical recommendations for car buyers looking to save money on their auto insurance in 2024:

- Compare Insurance Quotes: Before settling on a policy, compare quotes from multiple insurance providers. Rates can vary significantly, so shopping around can lead to substantial savings.

- Increase Your Deductible: Opting for a higher deductible can lower your insurance premiums. However, ensure that you can afford the deductible in case of a claim.

- Choose Your Vehicle Wisely: If you’re in the market to buy, here’s where you have a chance to make a big difference in your insurance bill. The type of vehicle you drive impacts your insurance rates. Cars that are cheaper to repair or are known for their safety features typically have lower insurance costs. Research the insurance costs for different models before making a purchase. Compare maintenance costs for new and used vehicles here.

- Maintain a Good Credit Score: Many insurers use credit scores to determine premiums. A higher credit score can lead to lower insurance rates, so it’s beneficial to maintain good credit.

- Drive Safely: Safe driving not only reduces the risk of accidents but can also lower your insurance rates. Many insurers offer discounts for a good driving record or for participating in defensive driving courses.

- Look for Discounts: Always ask about available discounts. Common discounts include those for multiple vehicles, no claims history, low annual mileage, having safety features on your vehicle, and bundling auto insurance with other policies like homeowners insurance.

- Consider Pay-Per-Mile Insurance: If you drive infrequently, explore pay-per-mile insurance options. These policies base premiums on the number of miles you drive and can be a cost-effective choice for low-mileage drivers.

By following these recommendations, car buyers can make more informed decisions and potentially save money on their auto insurance in 2024, despite the overall trend of rising rates.For more information on the latest auto insurance trends, check out Insurify’s latest update.

Free Car Buying Help Is Here!

Ready to outsmart the dealerships? Download your 100% free car buying cheat sheets today. From negotiating a deal to leasing a car the smart way, it’s all available for instant download. Get your cheat sheets today!

Sponsored by Insurify

Are you overpaying for car insurance?

Compare rates from top carriers in under 5 minutes. CarEdge users save an average of $996/year on auto insurance.

*Disclosure: CarEdge may earn a commission when you compare insurance quotes through our partner, Insurify. This does not influence our editorial content.*