Avoid 84-Month Car Loans, Even As Rates Fall

Key Takeaways

- 71% of drivers with 84-month car loans are underwater.

- Seven-year car loans made up a record 18% of new cars financed in Q3 2024.

- With free depreciation data available, drivers have tools to see how risky longer loans are.

As car prices remain high, many buyers are opting for longer car loans to keep their monthly payments manageable. According to new data from Edmunds, 84-month loans are on the rise. In fact, 84-month car loans have grown from 15.8% of new loans in Q1 2024 to 18.1% in Q3 2024. The average car loan term is now 68.8 months, remaining near all-time highs.

While these extended loan terms might lower monthly payments, they come with serious risks that could impact your finances for years to come. Here’s what you need to know, and how to play it smart when financing your car.

1 in 3 Drivers Have Underwater Car Loans

84-month loan terms are becoming popular, but that doesn’t mean they’re a good idea. In fact, far from it. As auto loan rates begin to fall, more car buyers are warming up to the idea of longer loan terms. This is a bad sign of things to come in 2025, unless consumers begin to think-twice about extending auto loans.

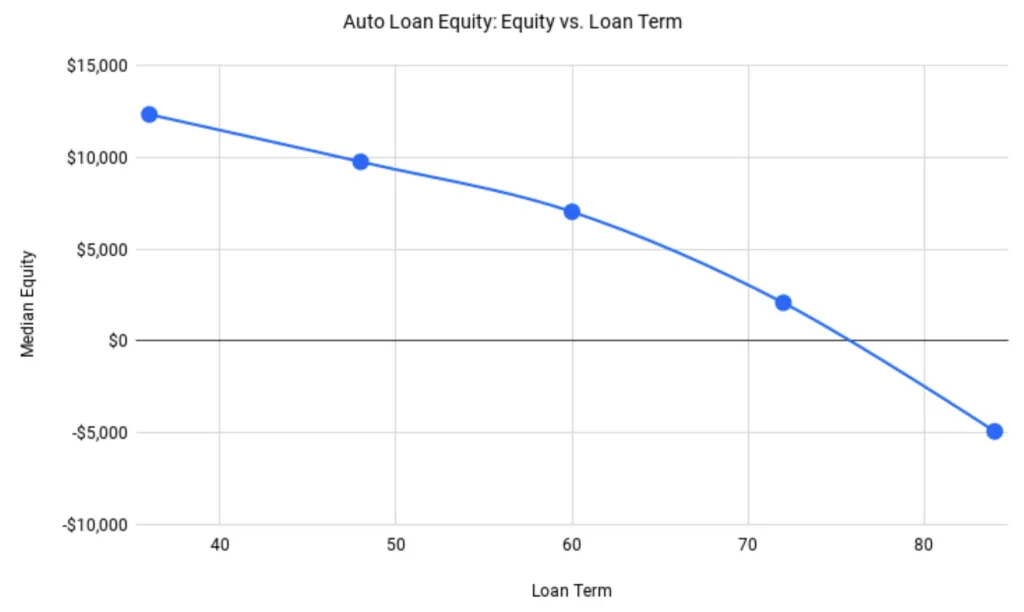

Our Q3 2024 CarEdge Negative Equity Report shows that 31% of drivers who financed their vehicle are underwater on their loans. The situation is worse for those with loans longer than 60 months, especially 84-month terms, which lead to slower equity growth and higher chances of negative equity. Among the survey respondents with 84-month loan terms, an astounding 71% are underwater. Clearly, longer loan terms increase the likelihood of negative equity for car owners.

One of the main reasons for this is depreciation. With long loan terms, cars lose value faster than the loan is paid off, leaving borrowers owing more than their vehicle is worth. With a longer loan, the gap between loan balance and vehicle value grows wider, putting drivers in a financially vulnerable position.

Why You Should Avoid 84-Month Loans:

- Negative Equity Risk: Longer loans increase the likelihood of being underwater, especially as depreciation outpaces loan payments.

- Higher Interest Costs: Even with a lower monthly payment, you’ll end up paying more in interest over time.

- Limited Flexibility: Being stuck in a long loan makes it harder to trade in or sell the car, especially if you’re upside down on the loan.

Smart Car Buying Tips:

- Opt for a loan term no longer than 60 months to build equity faster.

- Consider saving for a larger down payment to reduce the loan amount.

- Shop for the best interest rates and avoid stretching your budget just to lower monthly payments.

protect Yourself From Long-Term Financial Risks

While the allure of lower monthly payments with an 84-month loan can be tempting, the long-term risks far outweigh the benefits. Negative equity, higher interest costs, and lack of financial flexibility are all too common with extended loan terms. To protect your financial future, it’s smart to opt for shorter loan terms, build equity faster, and avoid stretching your budget just to secure a lower payment.

For more in-depth information on auto depreciation, maintenance costs, and total cost of ownership for hundreds of models, visit the CarEdge Research Hub. It’s 100% free!

Sponsored by Insurify

Are you overpaying for car insurance?

Compare rates from top carriers in under 5 minutes. CarEdge users save an average of $996/year on auto insurance.

*Disclosure: CarEdge may earn a commission when you compare insurance quotes through our partner, Insurify. This does not influence our editorial content.*