When Will Auto Loan Rates Go Down? New Car Buyers To Benefit Sooner

Key Takeaways

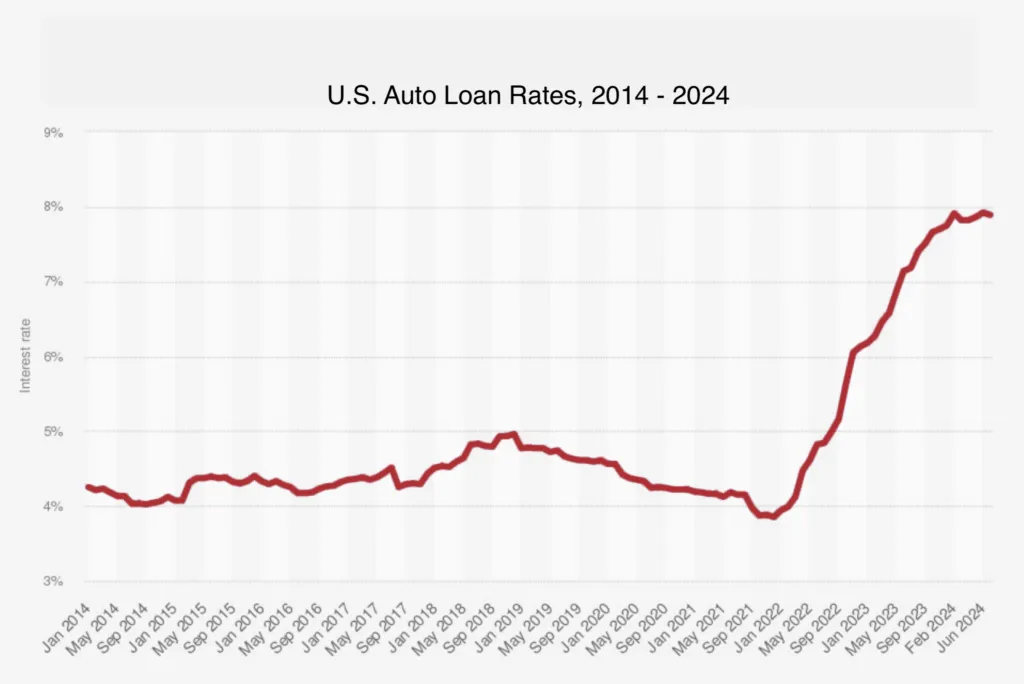

- Auto loan rates are notoriously "sticky", even as mortgage rates and bond yields move quicker.

- New car loan rates will go down before used car loans will. It all comes down to risk assessment.

- With auto finance on shaky ground, banks will delay lowering rates for as long as possible.

As the Federal Reserve begins to lower interest rates for the first time in years, many car buyers are wondering when they’ll see relief in auto loan rates. While the Fed’s recent 50 basis point cut is a positive sign, the impact on auto loan rates may take a little longer to materialize. Here’s why consumers should be patient and what they can expect in the coming months.

Interest Rates Don’t Drop Overnight

The recent 50 basis point cut by the Federal Reserve has sparked hope for auto loan rates to go down, but the reality is that those rate reductions won’t happen overnight. Car shoppers can plan their purchase accordingly by understanding how car loan rates are expected to move in the weeks and months ahead.

According to Cox Automotive, while the Fed’s interest rate cut marks the start of a broader easing cycle, it will take several weeks or even months for consumers to see significant drops in auto loan rates. The Fed doesn’t directly control auto loan rates, which are determined by market factors and lenders. In fact, auto loan rates tend to be “sticky” on the way down, meaning they’re slow to follow reductions in other market sectors, such as mortgage rates.

One key reason is that lenders are cautious about reducing the interest spreads on auto loans. Lenders continue to see shaky performance in the auto loan market, with higher delinquency rates and defaults. This makes lenders hesitant to lower rates too quickly. Auto loans represent a greater risk compared to other financial products, and lenders will wait to see sustained improvement in consumer financial behavior before they pass on lower rates to borrowers.

No sign of falling rates… yet

Cox Automotive notes that despite a decline in mortgage rates, auto loan rates have actually increased slightly in September. The average new car loan rate in September was 9.63%, while the average used car loan rate remained near recent highs at 13.95%. It may take several more weeks for car loan rates to slide downward.

Eventually, auto loan rates will go down, but consumers will likely see better deals on new vehicle financing first. Automakers work with ‘captive lenders’ to offer financing incentives. These banks are closely tied to the automaker. Captive finance companies are motivated to subsidize loan rates and drive sales.

As a result, we’ll see new car APR offers improving in the weeks ahead. As auto loan performance improves and credit spreads narrow, we’ll begin to see better rates for used cars, which have been hardest hit by recent increases in borrowing costs. It’s likely that the new year will arrive before used car loan rates fall significantly.

How Low Will Rates Go In 2025?

Most economists agree that rates won’t return to the lows we saw four years ago, when the Fed’s benchmark rates dropped to near zero. Instead, leading economists forecast a more realistic drop to the 3.00% to 3.50% range by the end of 2025. However, this forecast is subject to change if economic conditions worsen and the U.S. enters a recession, which could prompt the Fed to lower rates even further.

For car buyers, the path forward is clear. Car buyers looking for the lowest APRs should shop new car incentives. The average used car loan rate remains near multi-year highs, meaning drivers can save big by opting for new car incentives. Even today, new car offers often feature low-APR or even zero percent interest rates.

With year-end sales just around the corner, many automakers will offer aggressive financing deals to close out their oversupply of 2024 inventory. As we approach 2025, these deals are poised to get even better. Consumers who time their purchases right can maximize their savings.

Better Days Ahead

While auto loan rates won’t drop overnight, the upcoming months will bring better financing options for all car buyers. The Fed is on track to lower the benchmark rate several more times between now and late 2025. By late 2025, we could be looking at average APRs dropping below 6% for new car loans. Used car loans may finally fall back below 10% APR.

Lower rates will arrive in the new car market first, perhaps as soon as October. Used car buyers should expect more of a delay, but lower APRs are coming. In the meantime, use this opportunity to improve your credit score and overall financial picture. Lenders offer the best rates to the borrowers with the least amount of risk. Check out these expert tips on how to qualify for the best car loan rate possible, and how to keep your monthly payments low.

Sponsored by Insurify

Are you overpaying for car insurance?

Compare rates from top carriers in under 5 minutes. CarEdge users save an average of $996/year on auto insurance.

*Disclosure: CarEdge may earn a commission when you compare insurance quotes through our partner, Insurify. This does not influence our editorial content.*