How Much Should I Spend on a Car? Follow This Easy Rule.

For many, buying a car is the second most expensive purchase they’ll ever make. Buying a depreciating asset (a vehicle) for tens of thousands of dollars is a major financial commitment. If you’ve ever asked yourself, “How much should I spend on a car?” You’re not alone. Knowing how much you should spend on a car is an age old question, and one that we’re going to address today with the 10% rule.

If you search online, you’ll find many different opinions on how much you should spend on a car. There is no “right” answer, and there is no “wrong” answer. At the end of the day, you have to make a decision that you feel comfortable with.

That being said, we do have some advice we’d recommend you follow. We’re here to help you learn about the 10% rule, and how it helps you determine how much you should spend on your next car.

Assess your financial situation

First things first, to determine how much you should spend on a car, you need to assess your financial situation. This means auditing your monthly gross income. How much gross (before taxes) income do you make each month?

I say monthly income on purpose, because most car buyers are shopping for a monthly payment that meets their budget. This is as good a time as ever to mention that if you can afford to buy a car in cash, and you intend to keep it for decades, please do that. That is the most financially responsible car buying decision you can make (i.e. no interest payments).

Having said that, most of us aren’t in a position to pay for a car in cash upfront, and most of us want a little variety when it comes to what vehicle we’re driving in (we’ll get a different car in two or three years). If that’s you, then start this exercise by analyzing your monthly gross income.

Write that number down, we’re going to come back to it.

Ask yourself “why” you need a car

Are you buying a car because you need transport from point “a” to point “b,” or are you getting a car to make a statement?

I remember when I worked at an Acura dealership in the early 2000’s and a customer came in and purchased an Acura RL in the top trim. This was an expensive and luxurious car. The same day this customer took home his new car he came back. Why? Because his wife wanted him to buy a Lexus instead. To her, the Acura didn’t portray the image she wanted to her neighbors (it wasn’t “showy” enough).

In this case, the “why” behind purchasing a car was to make a material statement, not to simply get from point “a” to point “b.”

If you’re trying to make a statement, it’s my strong recommendation you figure out a cheaper, more fiscally responsible way to make that statement. Consider buying a watch, a house, a painting … literally anything other than a car — they simply lose value too quickly.

Factor in all cost of ownership expenses

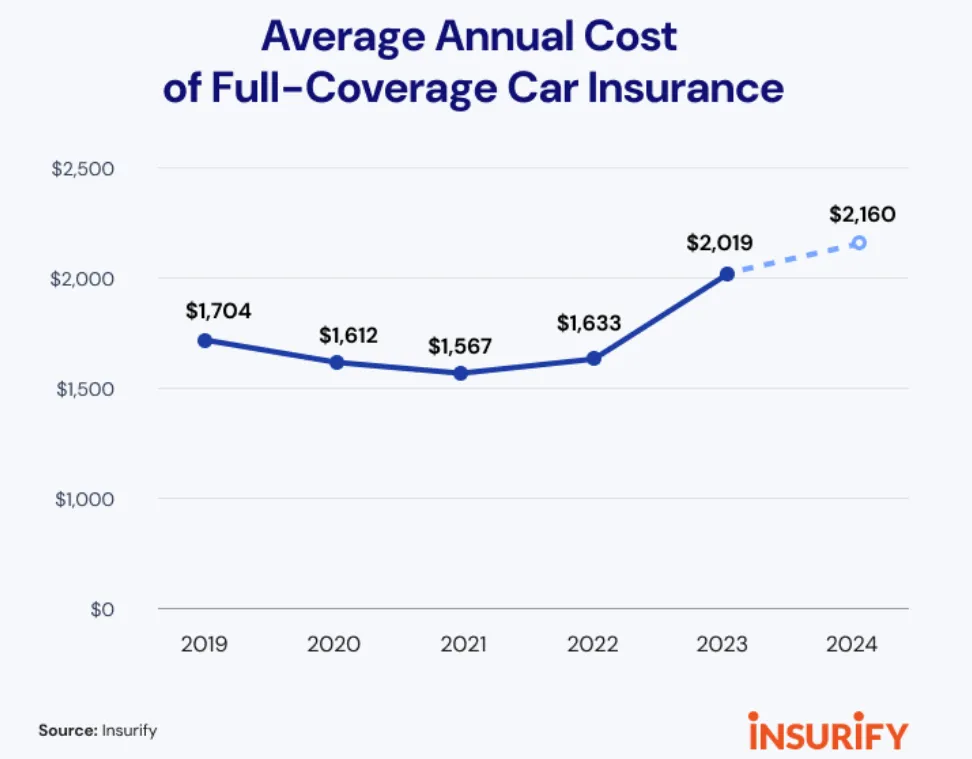

Buying a car entails a lot more than making a monthly car payment. Insurance, gas, maintenance, depreciation, the list goes on and on. If you’ve ever owned a car before, you know just how expensive it is. Plus, insurance costs are rising quickly.

That being said, it’s critically important to consider the total cost of ownership when thinking, “How much should I spend on a car?” Your monthly car payment should include:

- The lease or loan payment;

- Insurance;

- Maintenance;

- Wear and tear; and

- Depreciation.

When you factor each of these items into your monthly car payment you see that a $500/mo car payment is actually $1,000/mo. And this is where the 10% comes in. I counseled all of my clients over 43 years to consider spending 10% of their gross income on their car.

That means that if you make $60,000 per year ($5,000 per month), you can aim for up to $500 per month to go towards your car payment. That doesn’t mean you can afford any car that has a monthly payment of $500, it means the combined cost of the payment, the insurance, and the maintenance (I purposefully leave out depreciation from the 10% rule because if I included it you wouldn’t be able to afford a car) all needs to be $500 or less.

Some personal finance gurus suggest that you can afford to spend much more than 10% of your gross income on a car, and banks will even loan you the money you need to purchase a car so long as your debt to income ratio is below 40%. The 10% rule isn’t a commandment, it’s simply a suggestion. Spending more than 10% of your monthly gross income on a depreciating asset is a tough pill to swallow, but for some it’s worth it.

Don’t buy, lease instead

I highly recommend you consider leasing a car instead of buying it. Leasing has some distinct advantages compared to purchasing; mainly you know exactly what you are signing up for. The cost of depreciation and maintenance are built into the lease, whereas when you buy a car outright neither of those factors are known.

The 10% rule applies to leasing. For example, I am retired (sort of), and my monthly income is a bit more than $4,000. My Mini Cooper lease is $380/mo, and when you factor in insurance and gas costs, I am just a bit over the 10% rule. Just like you, I’m human, and I want things that I can’t necessarily afford. In this case, I made the conscious decision to bump the 10% rule to 12%, and I am happy.

👉 Our (free) Consumer Guide to Leasing

Leasing allows for a certain level of cost certainty since most lease terms are in the 36 to 48 month range and most cars are under warranty for most, or all of that time. Some brands even include free scheduled maintenance during your lease term, essentially making the monthly payment and the cost of fuel and your insurance premium your total car expenses. Trust me, cost certainty is a beautiful thing, once you experience it you will wonder how you ever lived without it.

A car is NOT an investment!

Ultimately how much you spend on a car comes down to how much money you are willing to set aside on a monthly basis. Additionally, always remember that when you buy a car, it will lose value. These are not investments.

How do you play it smart then? My recommendation is that you follow the 10% rule. It’s fair, it’s reasonable, and it’s not overly constrictive. Plus, when you drive somewhere in your new car, if you follow the 10% rule, you’ll still have some money in your pocket to pay for things when you get there!

You can drive a really nice car, and you might not be able to afford to enjoy the other aspects of your life. Or, you could drive an inexpensive car and you can afford all kinds of things, but you hate what you drive. My suggestion is to find a balance that allows you to do both, and for many people who ask themselves “How much should I spend on a car?” The 10% rule does the trick.

Sponsored by Insurify

Are you overpaying for car insurance?

Compare rates from top carriers in under 5 minutes. CarEdge users save an average of $996/year on auto insurance.

*Disclosure: CarEdge may earn a commission when you compare insurance quotes through our partner, Insurify. This does not influence our editorial content.*