Unethical Car Dealer Practices to be Aware of Before You Buy a Car

Key Takeaways

- It's unethical to advertise a different car price based on your financing options.

- Most advertised dealer prices don't include the price of tags, title fees, and other related expenses.

- You're at greatest risk of unethical dealer practices in the finance and insurance office.

Some car dealers do everything they can to be honest and showcase their integrity. Others do whatever they can to make an extra buck. While we’d love to tell you about all the great car dealers out there, we’re here to be your advocate in the car buying process. A big part of advocating for you is arming you with information.

Today, we’re going to take a look at unethical car dealer practices that you absolutely should be made aware of before you buy a new car. Even if a friend recommends your car dealer, even if you have a friend who works there, you should know about these practices.

We’re about to cover unethical car dealer practices that occur at every stage in the car buying process, from advertising a price you’ll never get, to packing your loan payments, to getting kickbacks from lenders.

Unethical Car Dealer Practices: Advertising the Wrong Price

We recently received an email from a reader in which they linked us to a dealership that was advertising two different prices: one if you financed with them and one of you didn’t. Guess which price was higher?

If you decided to finance with them, they gave you the price advertised in big, bold letters. Otherwise, you paid $1,000 more to use your financing option. Essentially, you must finance at the dealership and agree to whatever rates and terms they set up for you, or you’ll pay more.

This practice is not exactly common, but it does tie into more common practices. Car dealers often advertise prices that aren’t even available to most customers. The advertised price includes every available rebate, such as a first responder or recent graduate rebate. Then, when you show up to buy the car, they tell you that you don’t qualify.

Another prevalent practice is not including the price of tags, title fees, and other related expenses that they could easily add to the advertised price.

Essentially, one of the primary unethical car dealer practices that you absolutely must know is that the advertised price is not always what you’ll end up getting. You should research the market price of any potential car before you even visit the dealership so that you know what you should be paying. In other words, do your homework.

Unethical Car Dealer Practices: Packed Payments

Let’s play out a scenario: you walk into a shady car dealership, and a salesperson starts asking you questions. One of the earliest questions they’ll ask is, “how much can you pay per month?”

If you say $350, you can be confident they’ll do mathematical gymnastics to make sure that you pay $350. The financing managers do this by tweaking the loan amount and the APR until it works out that you’re paying either the exact amount, or more, than what you said you could afford.

So, if the loan should’ve been $300 but they inch it up to $350, then you’ll end up paying an extra $2,400 over a four-year loan. That’s not a small amount of money that could otherwise be in your pocket.

This practice is called packing or loading payments, and it’s a hard practice to detect.

If you do end up agreeing to the packed loan, you better believe they’ll pull out any other tricks they have to squeeze you out of every dime. It’s better to push back and be firm on how much you will pay, and please, don’t be afraid to walk away from the dealer. You always have the option of walking away from a situation where it feels like they’re taking advantage of you.

Your best defense against having packed payments is to secure your financing from your bank or credit union. Other than that, you can also do plenty of research before you visit the dealership so that you know what your payments should be.

Unethical Car Dealer Practices: Pushing Leases Through Dishonesty

Leases are an essential revenue stream for most car dealerships. Always selling new cars is their primary revenue source, but the margins are tight, so they often opt to urge people to lease instead.

Sometimes, a dealership will attempt to coerce you into leasing instead of buying through dishonest practices. Typically, a car dealership will quote you high prices on purchasing a new car and then give you the much lower lease price that seems like a steal. The salesperson will make it seem like leasing is the best way to get the car you’re after. They might even make false promises about the lease, which can veer into illegal scam territory.

We have nothing against leases, but if you’re going to a car dealership to buy a car and the salesperson tries to push a lease on you, leave that dealership.

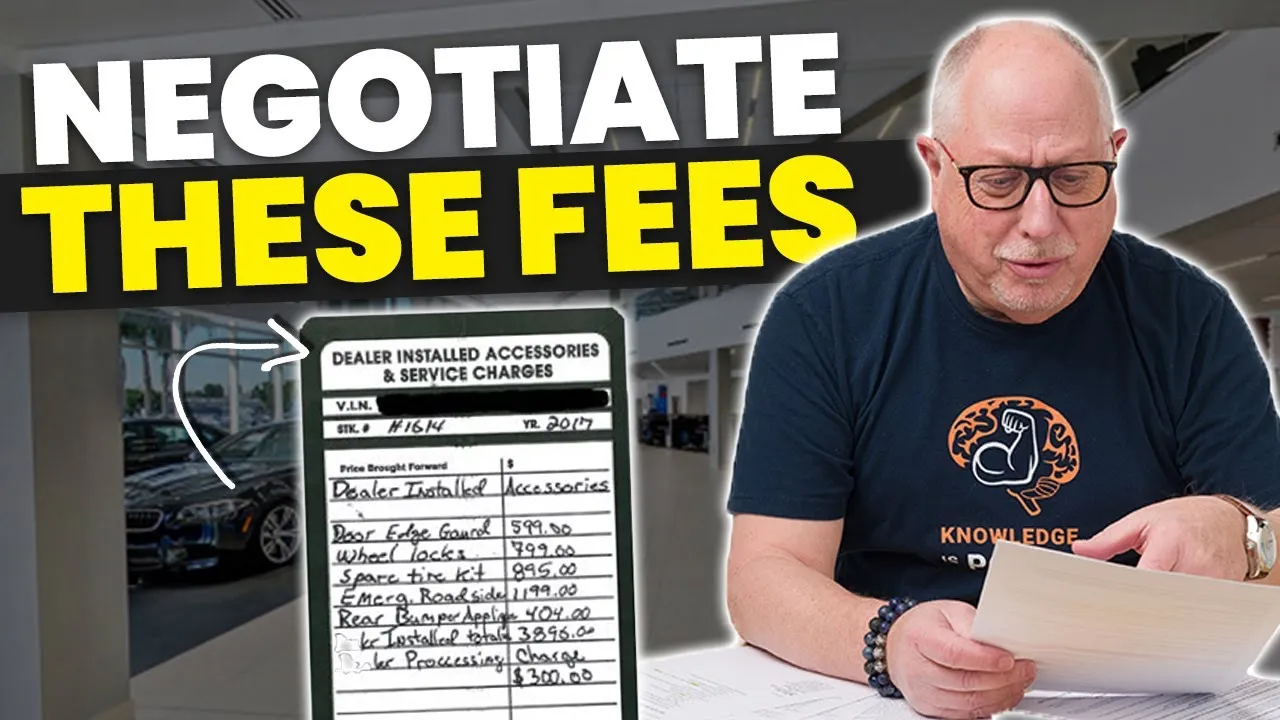

Unethical Car Dealer Practices: Adding Prep Fees to the Vehicle

If you owned a car dealership and had no moral compass, how would you make a quick profit without doing anything? Add a fee to every vehicle you sell. Just like that, you’re making an extra $500 to $1,000 per vehicle without any added effort.

That’s what prep fees are. Even above-the-board car dealerships have been known to do this. They’ll disclose the fee and say that it’s part of preparing your vehicle for you. Doing this almost seems fair at first glance.

What does a prep fee cover?

Some things it might cover include: peeling off plastic covering, vacuuming the interior, and adding fluids to the car. It’s about 2 hours of work, but they want you to pay $500 (and they’re probably paying the person that’s doing the prepping minimum wage).

Prep fees are entirely legal. The only thing you can do is ask that they credit you back the prep fee. That’s right; refuse to pay it. Get up and walk out if you need to. An extra $500 fee for adding oil to your engine just isn’t worth it!

Unethical Car Dealer Practices: Kickbacks for Loans

Let’s say you finance through the dealership, and the lender approves you at a 7% APR. However, you don’t know the exact number; it’s all done behind closed doors. After some waiting, the salesperson comes back and says they got you a 10% APR.

It’s a little higher than you had hoped, but you go for it. You sign with the lender for a 10% APR. Guess who gets that extra 3%? The dealership, through a payment from the lender.

This practice is known as an auto loan kickback. It’s one of the worst unethical car dealer practices because it can boost your monthly payments beyond what you had planned.

How do you protect against it? Get pre-approved for a loan through your bank or credit union. Doing so wholly avoids this unethical practice. If that isn’t an option, do plenty of research about what kind of an APR someone with your credit history should be getting. If they come back with a number higher than what you expected, say no.

Be Aware of These Types of Illegal Fraud

Not everything unethical is illegal. However, we can safely say that everything illegal is also unethical. As such, we absolutely must inform you about illegal fraud that some dealerships try to get away with:

- Yo-yo financing, which is the practice of having you drive off the lot believing that the loan is pending and then having you come back in to sign a different, pricier loan

- Stating that you will own a vehicle outright once the lease is paid for, which is always incorrect

- Dealer falsifying personal information to coerce you into agreeing to a higher interest rate, even though you should qualify for a lower one

- Not disclosing any material information, such as damage or malfunctions, about a vehicle

- A “rollback,” which is where the dealer will alter the car’s odometer

- Withholding information about a past accident, flood, or other damage

- Misrepresenting warranty coverage

- Underpaying or undervaluing a customer’s trade-in vehicle

- “Bait and switch” schemes, where an advertised deal is said to be no longer available, and then the salesperson tries to sell the same vehicle at a higher price

- Saying that some features are required when they’re really optional

- Boosting the price above the sticker price by including options the customer didn’t request or adding undisclosed fees

If you catch a dealership doing any of the above, they may be violating various consumer protection laws. We are not qualified to give legal advice, but we do believe you should seek a lawyer if you’ve been involved with any of these practices.

Be Open to Different Options to Avoid Bad Practices

You can do two things to protect yourself against unethical car dealer practices: arm yourself with information and be open to different vehicles.

The first one is this article’s purpose; to inform you about specific practices that car dealers try to get away with. The second is up to you. If you are less committed to one particular vehicle, especially a specific VIN, then it’ll be easier to walk away if you believe there is something unethical happening.

Unfortunately, you have to keep your head on a swivel to avoid being taken advantage of. Research loans and car values before you visit a dealership, and you’ll be in an excellent position to prevent these practices.

Sponsored by Insurify

Are you overpaying for car insurance?

Compare rates from top carriers in under 5 minutes. CarEdge users save an average of $996/year on auto insurance.

*Disclosure: CarEdge may earn a commission when you compare insurance quotes through our partner, Insurify. This does not influence our editorial content.*