Is It Better to Buy Or Lease a Car in 2025?

Key Takeaways

-

Leasing is Often the Better Deal in 2025: With high interest rates and fewer incentives, leasing offers better value for many car shoppers.

-

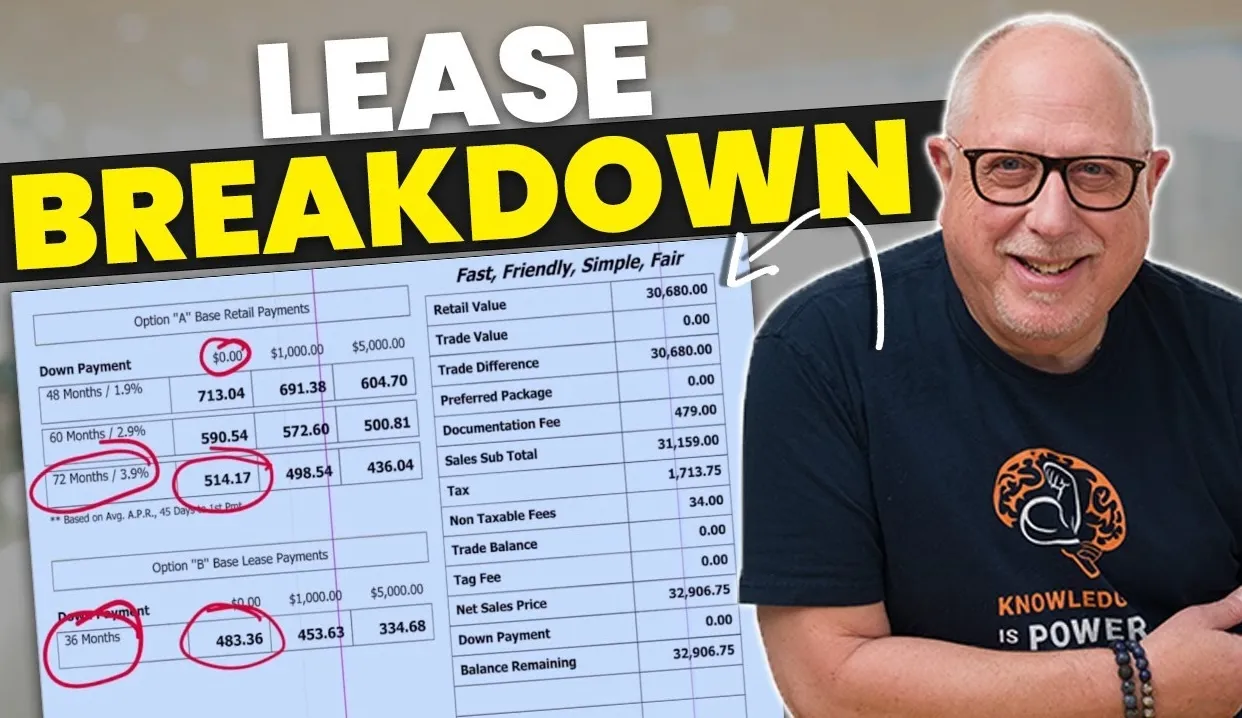

Always Read the Fine Print on Lease Offers: Advertised lease deals typically exclude taxes and fees.

-

Buying Still Makes Sense for Long-Term Owners: If you drive a lot, plan to keep your car for many years, buying may still be the smarter financial choice.

Choosing between buying and leasing a car remains one of the biggest decisions for car shoppers. In 2025, that question is even more relevant due to evolving market conditions, rising interest rates, and shifting manufacturer incentives. With insights from CarEdge Co-Founder Ray Shefska, we break down the pros and cons of buying versus leasing to help you navigate today’s car market with confidence.

Understanding Leasing in 2025

Leasing has historically been a popular option for drivers who want lower monthly payments and the ability to upgrade to a new car every few years. After a decline in popularity during the pandemic, leasing is once again on the rise in 2025—and for good reason.

How does leasing a car work? Leasing a car means you pay to use a vehicle for a set period—typically 2 to 4 years—by making monthly payments, but you don’t own it. At the end of the lease, you can either return the car, buy it for a predetermined price, or lease a new one.

Estimate your monthly lease payment with this new and improved Car Lease Calculator:

Leasing is increasingly the better deal for many shoppers in today’s market. With interest rates still elevated and new car prices impacted by global tariffs and supply challenges, leasing offers a more affordable path to driving a new vehicle. For many, lease programs are the best way to bypass the high financing costs associated with buying.

There’s also a strategic reason why automakers are doubling down on lease offers: it keeps customers engaged with the brand. When lease terms end, customers return to the dealership, increasing the chance of a repeat sale and building long-term loyalty.

As CarEdge’s Ray Shefska notes, many manufacturers are now working hard to increase lease penetration due to the benefits for both dealers and customers. While leasing once made up around 30% of new car transactions, that number fell to 17–18% during the downturn. In 2025, manufacturers are rolling out some amazing lease offers to reverse that trend. For buyers, this means now is a great time to take a serious look at leasing.

Important Note: Be aware that advertised lease deals typically do not include taxes and fees. If you’re not planning to pay these upfront, your actual monthly payment could be significantly higher than what’s promoted.

The Benefits of Leasing a Car

Leasing in 2025 presents several notable advantages:

-

Lower Monthly Payments: In a high-interest environment, lease deals often feature better terms than financing, making it possible to drive a better-equipped vehicle for less per month.

-

Access to Newer Technology: Leasing allows you to drive the latest models every few years with the newest tech, safety features, and fuel efficiency improvements.

-

Flexibility: When your lease ends, you can walk away, upgrade, or even purchase the car if you’ve grown attached.

-

Inventory Turnover Benefits: As leases come to an end, dealerships benefit from a steady influx of quality used vehicles, improving options in the used market.

The Benefits of Buying a Car in 2025

Buying remains a solid option—especially for drivers who keep their cars for the long haul or who rack up high mileage annually. Here are the core benefits of purchasing:

-

No Mileage Limits: Unlike leases, buying a car comes with no mileage restrictions, which is ideal for commuters and road-trippers.

-

Long-Term Financial Value: Every loan payment builds equity. Once the loan is paid off, you own the car outright—no more monthly payments.

-

Freedom to Modify: Ownership gives you the freedom to customize or modify your car as you wish, without lease restrictions.

-

Stability Over Time: If you plan to keep your car for 5+ years, buying can offer better value than leasing. But if you’re considering selling after just a few years, be cautious—depreciation hits hard, and the math may not work in your favor.

Making the Right Choice in 2025

Whether to buy or lease a car in 2025 comes down to your personal goals, driving habits, and financial situation. Ray advises, “Customers should check the manufacturer website and see what kind of sales and lease offers are available in their area before heading to the dealership.” He also recommends comparing insurance quotes across models before finalizing your choice.

👉 See This Month’s Best Leasing and Financing Offers

When Does Buying Make Sense?

-

You drive a lot and want to avoid mileage limits.

-

You plan to keep the car for 5+ years.

-

You want to build equity and eventually eliminate monthly payments.

-

You like the freedom to modify or customize your car.

👉 Compare the best-value cars and trucks with CarEdge Research [Free]

When Does Leasing Make Sense?

-

You want lower monthly payments and more car for your money.

-

You like driving a new vehicle every few years.

-

You don’t want to worry about long-term maintenance costs.

-

You want to avoid high interest rates and take advantage of lease-specific deals.

-

You’re okay returning the car in original condition and staying under mileage limits.

👉 Check Out Our Complete Guide to Leasing in 2025

What It All Boils Down To

In today’s market, with leasing incentives improving and financing rates remaining high, leasing is often the smarter move—especially if you’re seeing limited financing deals. Just be sure to read the fine print on lease offers and understand how upfront taxes and fees impact the monthly cost.

By doing your homework and staying informed, you can make the decision that best fits your lifestyle and budget in 2025’s fast-changing auto landscape.

Looking for help negotiating your car lease? Learn more about CarEdge’s white-glove Car Buying Services, now more affordable than ever.

Sponsored by Insurify

Are you overpaying for car insurance?

Compare rates from top carriers in under 5 minutes. CarEdge users save an average of $996/year on auto insurance.

*Disclosure: CarEdge may earn a commission when you compare insurance quotes through our partner, Insurify. This does not influence our editorial content.*