Predictions for 2023: Car Prices Fall as Dealers Suffer

What a year it has been. 2022 started with new and used car prices climbing to record highs, stubborn semiconductor chip shortages and a world at relative peace. As we wrap up the year and look forward to 2023, used car prices are tanking, new car inventory is rising, and global conflict has shaken everything from gas prices to automotive suppliers, in addition to affecting millions of lives. Our very own Ray Shefska has these 5 predictions for 2023, informed by over 40 years in the auto industry. Let’s dive in.

1. New Car Inventory Will Continue to Grow

As we head into 2023, new car inventory is the highest since May 2021. That was when the semiconductor chip shortage sprang out of pandemic shutdowns, throwing the automotive industry into a downward spiral. The latter half of 2022 saw automakers slowly but surely climb back from the brink of empty lots, but the recovery is still underway. Manufacturers can make more cars today than they could a year ago. (See the latest new car inventory numbers here.)

But it’s not just easing supply constraints giving us hope for more new car inventory. Consumers are holding back on discretionary spending, and in many cases, that includes shiny new cars. Others are simply getting priced out of the new car market as MSRPs continue to rise. Check out the biggest MSRP increases for the 2023 model year.

As more cars are produced with fewer buyers on the market, new car inventory will grow in 2023. Those dealer lots won’t be so empty in six months’ time.

2. Used Car Affordability Will Continue to Keep Sales Volume Down

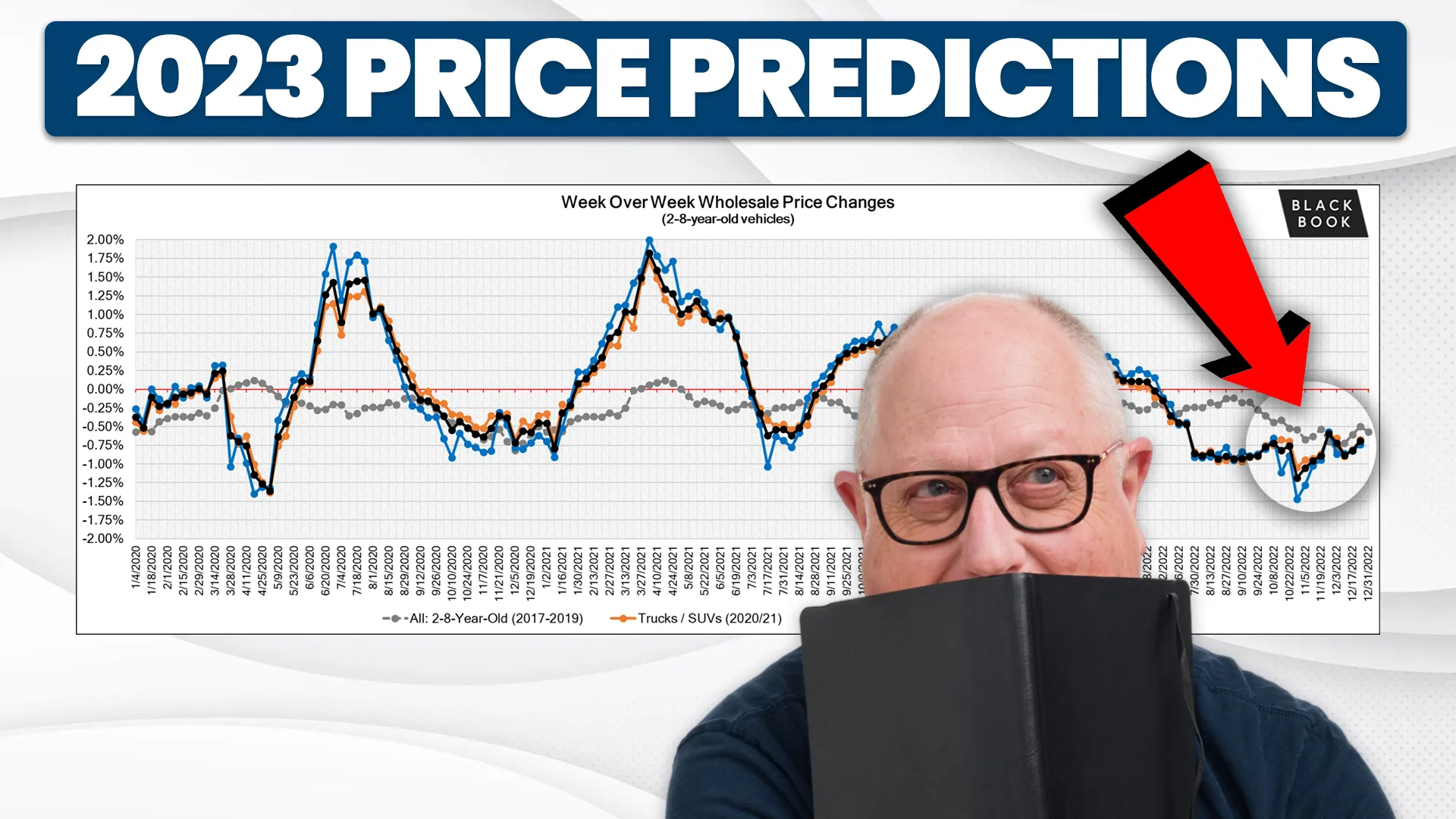

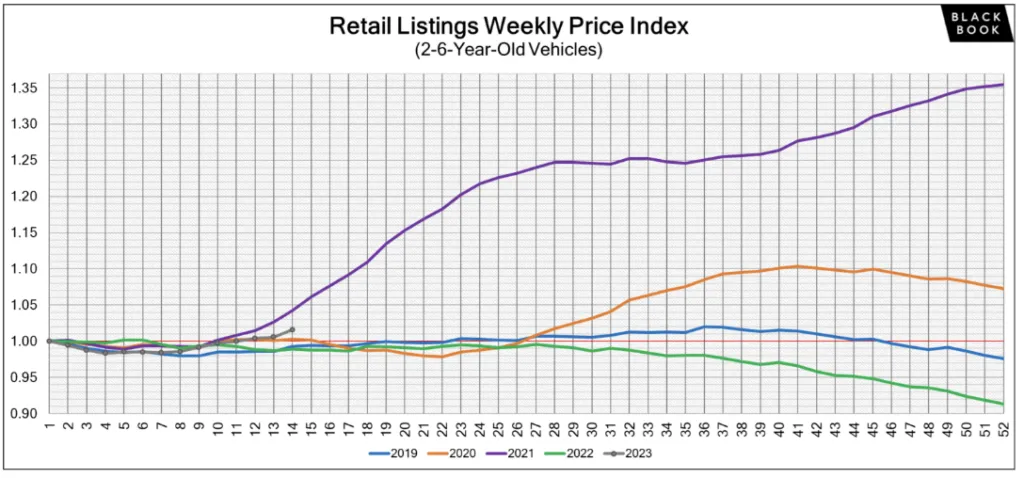

From early 2021 to mid-2022, used cars became so absurdly overvalued that even with 5-10% price drops in recent months, they still have very far to fall before prices are anywhere near historical norms. Lower prices and reduced dealer profit margins will be unable to overcome higher loan interest rates enough to offset affordability.

Dealers are making less money with each used vehicle sold, and they’re going to be doing their very best to squeeze every additional dollar out of used car sales, even as we transition from a seller’s market to a buyer’s market.

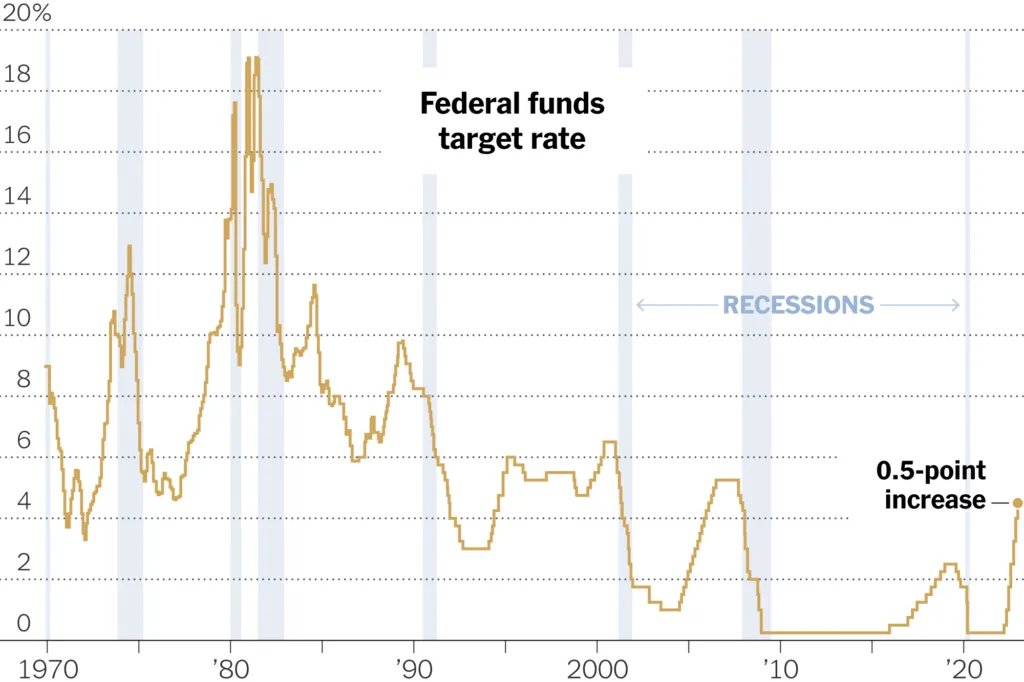

3. Rising Interest Rates Will Lower Demand and Worsen Affordability

Interest rates for auto loans have doubled since 2021. As of late December 2022, the average used car loan APR was close to 10%, while used car loan APRs averaged 5%. Just how much does a bump up from 5% to 10% APR matter? Let’s run through some frightening math.

According to data from Experian, the average amount financed reached $41,665 for new vehicles and $28,506 for used vehicles in the third quarter of 2022. Let’s meet halfway at $35,000.

At 5% APR with a 72 month loan (we suggest sticking to 60 months or less), total interest paid comes out to $5,584. At 10% APR, this same loan will charge the borrower $11,685 in interest. Cars get a whole lot more expensive when taking the cost of borrowing money into account.

The Federal Reserve has indicated additional interest rate hikes are likely, although they could be smaller than the most recent 50 basis point increase. In a best case scenario, auto loan interest rates could peak at some point later in 2023.

4. Manufacturer Incentives Will Increase

Simply put, auto manufacturers will be looking for more ways to drive up demand for their new cars in 2023. It doesn’t take a genius to see that the easiest way to do that is to lower prices, especially following month after month of MSRP hikes.

Analysts at Cox Automotive found that the average incentive spend in November 2022 was $1,066, a 43% decrease since November 2021. Who will offer incentives first, the dealer or the manufacturer? We think 2023 will bring a bit of both as demand continues to soften.

We track the best new car incentives, updated monthly. Be sure to bookmark these pages if you’ll be in the market to buy or lease in 2023!

The Best Auto Loan Rates Right Now

The Best New Car Lease Deals This Month

5. Cash Is King in 2023

All-cash car purchases are expected to climb to levels not seen in decades this year. It’s all about interest. Borrowing money is so expensive right now that a cash purchase is by default preferred by money-savvy consumers. Others are financing with the dealer to get a better trade-in value, only to pay off the loan weeks later. But there’s another dynamic at play here.

The post-pandemic economic recovery has been characterized by a new phenomenon that some economists are calling a ‘k-shaped recovery’. Essentially, some Americans are doing better financially now than ever before. They were fortunate enough to stay employed in 2020-2021, and with a whole lot less to do (and spend money on), their bank accounts are looking healthy. Others are still struggling to get back to where they were financially before COVID.

The result of the ‘k-shaped recovery’ can be seen in 2022’s healthy luxury sales, despite a shaky economy.

A Buyer’s Market in 2023?

Taken together, does this mean it will be a buyer’s market in 2023? With interest rates soaring to levels not seen in over a decade, it’s not the type of buyer’s market we’d like to see, but it’s an improvement.

The good news is that in 2023, car buyers will have more negotiating power than in 2022. And we’re here to help!

Not sure where to start? Check out these no-strings-attached free guides:

Car Buying Cheat Sheet: Former Dealer Shares How to Negotiate Car Prices Confidently

How to Challenge Forced Front-End Add-Ons At a Dealership

The Best (and Worst) Electric Cars in 2023

The Car Buyer’s Glossary of Terms, Lingo, and Jargon

What do you think? What surprises are in store for vehicle ownership in 2023? Please, share your thoughts below!

Sponsored by Insurify

Are you overpaying for car insurance?

Compare rates from top carriers in under 5 minutes. CarEdge users save an average of $996/year on auto insurance.

*Disclosure: CarEdge may earn a commission when you compare insurance quotes through our partner, Insurify. This does not influence our editorial content.*