How to Sell a Car with a Loan: Your Step-By-Step Guide

For many, there will eventually come a time when you need to part ways with a beloved car – even when you still owe money on it. Selling a car with an outstanding loan can seem daunting due to the added complexity of dealing with lenders. However, with a proper understanding of the process and careful planning, you can navigate the situation with ease. Here at CarEdge, we’re diving into how you can efficiently and effectively sell your car, even if the loan isn’t fully paid off yet.

Step One: Understanding Your Loan Details

When you’re considering selling a car that you still owe money on, the first crucial step is to fully understand the details of your loan. This knowledge is not only essential for setting the right sale price but also for ensuring that the transaction is handled legally and smoothly.

First thing’s first: understand your loan. That means digging up your login credentials to get into your online account with the lender. You may even need to give them a call, or hop on the live chat.

Here’s what to figure out before selling your car with a loan balance:

- Check Your Loan Balance: Log in to your account, or contact your lender to request the current balance and the official payoff amount of your loan. The payoff amount may be higher than the balance due to the inclusion of any prepayment penalties or accrued interest.

- Understand the Payoff process: Ask your lender about the specific steps required to pay off the loan. You need to know how long it takes for them to process payments and release the lien. This timing is critical, especially if you need to coordinate with a buyer.

- Lienholder Details: While your lender holds a lien on your vehicle, making them a key stakeholder, you don’t need their explicit permission to sell the car. However, you do need to pay off the loan. When you send the payoff check to your lender, include a signed payoff authorization form. This form authorizes the bank to send the lien release or the physical title directly to the new owner. By doing this, the buyer is protected, knowing that the necessary documents to prove ownership will be sent to them by the bank.

- Obtain a 10-Day Payoff Quote: Most lenders will provide a quote that is valid for 10 days, which includes the total amount required to pay off your loan in full as of that date, including any additional fees or accumulated interest. This quote will be vital when you finalize the sale and need to settle the loan balance.

Step Two: Valuing Your Car

Next, determine how much your car is worth. Use trusted resources like Edmunds or Kelly Blue Book, and use CarEdge’s valuation tool to see how much online buyers will pay.

If you decide to go the private seller route, it’s important to price your car thoughtfully. Remember, you’re trying to sell the car quickly while also covering your remaining loan balance. Setting the right price can help you attract buyers quickly while ensuring you don’t fall short financially.

Step Three: Finding a Buyer

You have two main avenues for selling your car: a private sale or a dealership trade-in. A private sale typically yields a higher return but requires more effort on your part in terms of marketing and negotiation. Platforms like Facebook Marketplace, Cars.com, and AutoTrader are great for reaching potential buyers. On the other hand, trading in your car at a dealership is less hassle but is highly unlikely to offer as much for your car, especially with an outstanding loan.

With a dealership trade-in, it’s common to be offered 20-30% less than your car is worth in a private sale. If you could really use that additional money, going through the longer, more tedious process of selling privately may be worth it.

👉 Learn more about your options for selling a car

Step Four: Handling the Financials

The financial aspect of selling a car with an outstanding loan can be tricky. But don’t give up now! If you’re eager to sell, it’s worth the hassle. Here’s how to handle it effectively:

- Escrow Services: Using an escrow service for a private sale is strongly recommended as it adds a layer of security for both parties. The escrow service will hold the buyer’s payment until the loan is paid off and the lien is released, ensuring that the buyer doesn’t hand over money without securing the title, and you don’t transfer the title without clearing the loan.

- Addressing Shortfalls: All payoff should be made with a cashiers check to further expedite the process. If the selling price doesn’t cover the loan payoff amount, you will need to provide the additional funds to clear the loan. Consider your options for covering this shortfall, such as a personal loan or a line of credit.

- Payment to Lender: If you go this route, be sure to confirm that the buyer is comfortable with it before sealing the deal. It’s possible to coordinate with the buyer on making the payment directly to the lender. However, with a properly filled out payoff authorization stipulating that the documents go to the buyer, this would not be necessary.

- Handling Overpayments: If the car sells for more than the payoff quote, plan how the surplus will be handled. Confirm with your escrow service (or with the buyer if they will pay your lender directly) to return the excess amount to you after the loan settlement.

- Documentation: Keep meticulous records of all communications and transactions related to the loan payoff and car sale. Documentation should include the final payoff receipt from your lender and any agreements made with the buyer.

Step Five: Transfer of Ownership

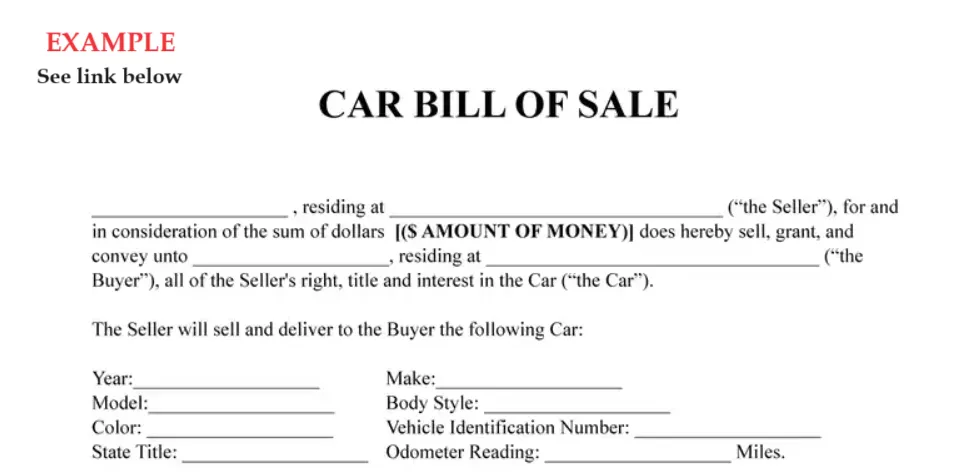

Transferring ownership involves a few small hurdles, but it’s nothing you can’t do! You must inform the buyer about the lien and ensure that the loan is fully paid before transferring the title. Even with a lien, you are legally required to provide the buyer with a bill of sale, documenting the transfer of ownership to the buyer. Alongside this, include a payoff authorization when you send the loan payoff to your lender. This authorizes them to release the lien or send the physical title directly to the new owner. Once you receive a lien release from your lender, you can complete the title transfer to the new owner.

Each state has different laws, so it’s important to check your local requirements. Check with your state DMV. The information should be easily found on their website.

If you want to avoid these hurdles, consider paying off the loan balance and securing the lien release before you sell the car. This approach eliminates many potential complications that could delay the sale.

Plan Ahead to Avoid Headaches (You’ve Got This!)

Selling a car with an outstanding loan requires careful attention to financial details and diligent record-keeping. With the right approach, you can sell your loan and transfer ownership without a hitch. Remember, knowledge is power in any transaction. Understanding how to handle this process can save you from potential financial pitfalls. For more insights and resources on managing car sales and ownership, keep it tuned to CarEdge.

👉 Want to become a car market pro? How about that and more for FREE?

Sign up for Deal School today, our free course for anyone interested in buying, selling, or simply owning a car the smart way.

Sponsored by Insurify

Are you overpaying for car insurance?

Compare rates from top carriers in under 5 minutes. CarEdge users save an average of $996/year on auto insurance.

*Disclosure: CarEdge may earn a commission when you compare insurance quotes through our partner, Insurify. This does not influence our editorial content.*