Car Payments Hit Record Highs in 2023: The Latest Numbers, and How to Save

The average car payment has been on an upward trajectory for some time, and 2023 is no exception. Today, we’re dissecting what the average car payment looks like and why it’s been rising. We’ll explore how average monthly car payments crossed the $1,000 threshold, and how you can navigate this landscape to spend less.

The Average Car Payment in 2023 Ticks Higher

| (New Cars) | 2023 Q3 | 2023 Q2 | 2023 Q1 |

|---|---|---|---|

| Average Term | 68.4 | 68.5 | 68.8 |

| Monthly Payment | $736 | $733 | $730 |

| Amount Financed | $40,149 | $40,356 | $40,468 |

| Average APR | 7.4% | 7.1% | 7.0% |

| Down Payment | $6,907 | $6,823 | $6,956 |

According to Edmunds’ latest data, the share of $1,000+ monthly car payments has hit an all-time high. The rise is attributed to various factors: high interest rates, increased automaker prices, and dealer practices.

Reaching a new record, 17.5% of new car loans in Q3 2023 required a monthly payment of $1,000 or more. That’s up from 17.1% in Q2 2023 and a massive increase from the meager 4.3% back in 2019.

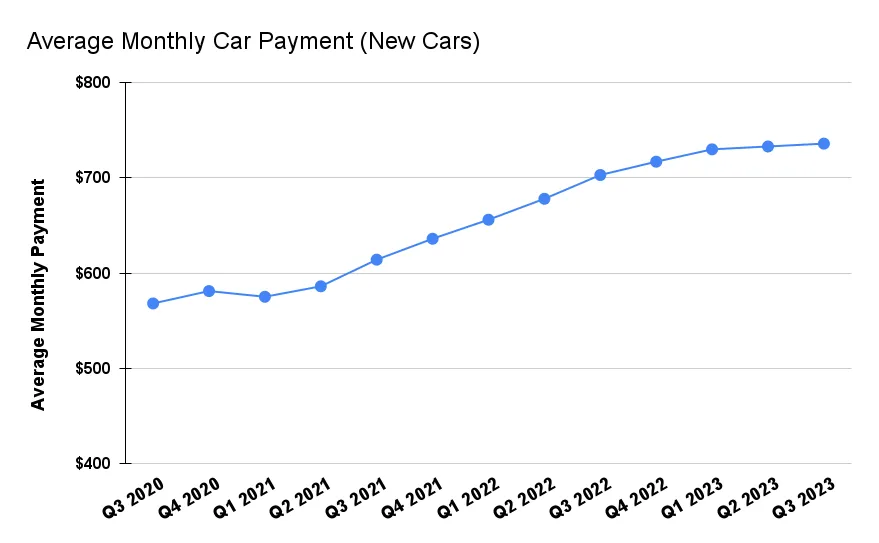

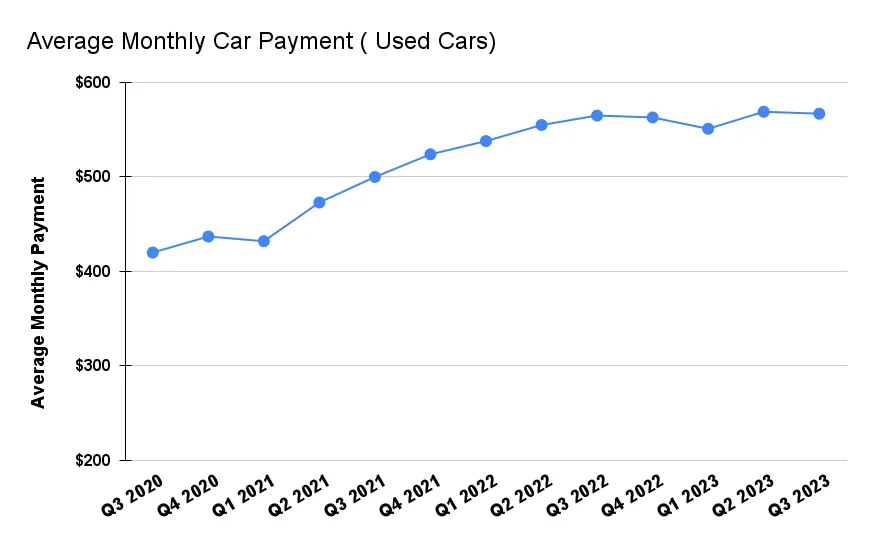

The average car payment in Q3 2023 reached a record high of $736 per month for new cars, up 4.5% since Q3 2022, and a 32% increase from 2019. Meanwhile, the average monthly car payment for used cars is $567, marking a 46% rise from 2019, but up less than 1% from Q3 2022.

Take a look a the average new car payment over time:

Data source: Edmunds. Graph by CarEdge.

The average monthly payment for used cars has followed a similar path upward, as we can see here:

Data source: Edmunds. Graph by CarEdge.

In pre-pandemic times, there was a slow but steady rise in car payment amounts. As the auto industry came out of the pandemic recession and the following chip shortage, car prices went through the roof, bringing average monthly payments along with them.

Let’s talk about why car payments are so high right now, and what you can do about it.

Average Car Prices in 2023

So, how much have car prices gone up? The average transaction price for a new car is $48,451 in 2023, a 25% increase since 2019. For used cars, it stands at $28,381, still 37% higher than in 2019, despite a slight decrease from the previous year. To make matters worse, interest rates for used car loans are commonly over 10% these days.

We track used car prices weekly. See the latest data!

Why are average monthly car payments and overall prices rising so fast? The auto industry can’t simply blame it on inflation, as we’ll get into below. But first, let’s talk about financing.

Borrowing Gets Expensive, Down Payments Increase

Car buyers are making larger down payments as the cost of borrowing money increases. The average auto loan rate is now 7.4% APR for a new car loan, and 11.2% APR for a used car loan. These are the highest auto loan rates the market has seen since 2007.

When will car loan rates go down? Simply put, it’s up to the Fed. The Federal Reserve sets the ‘Federal Funds Rate’, which largely determines how much it costs for banks to borrow money from each other, ultimately driving consumer loan rates.

Raising interest rates is a tool used to combat inflation. The thinking goes that when borrowing gets too expensive, excessive spending will be discouraged, and in turn demand for goods and services will cool down to the point that inflation slows.

Car loan rates will remain high until The Federal Reserve begins to lower interest rates at their Board meetings. Inflation needs to cool down for that to happen. Things are headed in the right direction, but we’re not there yet.

How to Save on Auto Loan Interest

FREE Resource: How to Finance a Car Like a Pro: The Ultimate Auto Financing Cheat Sheet

Even with auto loan rates at 20-year highs, there ARE ways you can lock in big savings on loan interest. Here are the most effective ways to save on interest, according to our CarEdge team of experts:

- Improve your credit score: Before shopping for a new car, check your credit score and work on improving it. Paying off outstanding debts, making timely payments, and keeping your credit utilization low can all help boost your score.

- Shop around for rates: Don’t limit yourself to the dealership’s financing options. Shop around for car loans from banks, credit unions, and online lenders to find the best interest rates.

- Opt for a shorter loan term: While a longer loan term may result in lower monthly payments, it also means you’ll pay more interest over the life of the loan.

- Make a larger down payment: A larger down payment can help you save on interest by reducing the loan amount and demonstrating to lenders that you’re financially responsible. Aim for a down payment of at least 20% of the car’s purchase price

Check out our deep dive into the many ways you can spend less on auto loan interest. With today’s interest rates, these tips could save you hundreds of dollars! Don’t forget to print this auto finance cheat sheet and bring it with you!

Budgeting for Your Car Payment: What the Experts Say

Our team of Car Coaches is made up of professionals who have decades of experience in the auto industry. Rather than squeeze more money out of every sale at the dealership, these car pros help drivers SAVE money with their auto. We spoke to our team of Coaches to learn how much money today’s car buyers should aim to spend on their monthly car payment.

The consensus was broad: the CarEdge team advises keeping your monthly car payment below 10% of your monthly take-home pay. With gas, insurance, and maintenance, it should ideally be well below 20% of your monthly income. It’s worth noting that negotiation can play a pivotal role in ensuring you spend less on your car.

Here are a few essential FREE resources to help you budget for your car purchase:

Browse cars with expert help just a click away with CarEdge Car search.

Use this Free Out-the-Door Price Calculator to more accurately estimate how much your car will cost once taxes and fees are included.

Here’s a Free Car Payment Calculator that will help you understand what price range you can afford with your down payment. It’s most useful if you have an idea of what loan rates you might qualify for.

The Road Ahead

Most automakers have an oversupply of new cars right now. Over the past year, we’ve seen dealer lot inventory climb above and beyond what we typically see in a healthy, stable car market. Automakers and dealers like to have roughly a 60 day supply of new cars on their lots. Today, we see more and more models well above a 100 day supply. For some, like the Ford Mustang Mach-E, Jeep Renegade and Ram 1500 truck, inventory exceeds 200 days.

Something has to give. Floorplanning costs mean that the car dealers themselves pay interest for every day that a car sits on their lot. Plus, no one wants a two-year old ‘new’ car. With each passing day, dealers are incentivized to move their inventory off the lot.

We’re seeing used car prices fall rather quickly, yet new car prices are more complicated. Listing prices remain high (and in some cases outrageous), but our team of CarEdge Coaches is seeing greater negotiability on the new car market.

Dealers are more willing to lower their prices and remove add-ons and markups. However, in most cases, this is only true when the buyer is prepared to put some work into the deal with negotiation know-how. Don’t expect softball deals in today’s new car market. But don’t fret: we’re here to help.

How to Negotiate and Save

Our team of Car Coaches created this 100% free guide to negotiating a car purchase with one goal: to save you time and money. Print it and bring it with you to the dealership!

Negotiate Car Prices With This Cheat Sheet

Looking for more car buying help? Search our free guides, and join the CarEdge Community today! We’re here to help you negotiate car prices confidently. When it comes to car buying, knowledge certainly is power.

Ready to work 1:1 with your own car buying coach? Learn more about CarEdge Coach, your path to ultimate savings! Looking for more of a DIY route to savings? We created CarEdge Data just for you. For the first time ever, behind-the-scenes market data is at your fingertips, empowering car buyers everywhere to negotiate with confidence.

Remember, the secret to smart car buying isn’t solely about discovering the car that captures your heart. It also involves understanding the market you’re shopping in. Despite escalating prices, opportunities remain for those willing to undertake comprehensive research and exhibit patience.

Stay informed, be patient, and you might find that the perfect deal is just a stone’s throw away. We’re here to help!

Sponsored by Insurify

Are you overpaying for car insurance?

Compare rates from top carriers in under 5 minutes. CarEdge users save an average of $996/year on auto insurance.

*Disclosure: CarEdge may earn a commission when you compare insurance quotes through our partner, Insurify. This does not influence our editorial content.*