Upside-Down on Your Car Loan? How to Navigate Negative Equity

Diving into the world of car ownership can lead you into murky waters, especially when grappling with negative car equity. Imagine owing more on your car loan than the vehicle is worth – a situation many Americans face today. This comprehensive guide illuminates the shadowy depths of negative equity: exploring its causes, the impact of recent economic trends, and, most importantly, effective strategies to steer clear of or manage it if you’re already caught in its grip.

Understanding Negative Equity: How It Happens

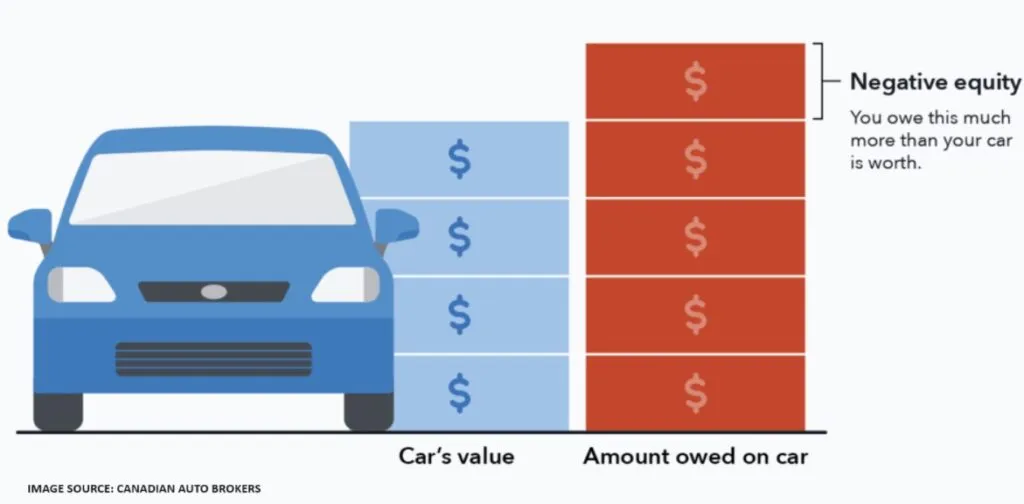

Negative equity, often described as being “upside-down” on a car loan, occurs when the loan balance surpasses the vehicle’s current market value. This financial quagmire can ensnare car owners due to:

- Depreciation: Cars depreciate the moment they’re driven off the lot. If the loan repayment lags behind this depreciation rate, negative equity can develop.

- Long-term Loans: Extending loan periods results in slower principal repayment, risking negative equity as cars depreciate faster than the loan diminishes.

- Small Down Payments: Minimal initial down payments increase the financed amount, heightening negative equity risks if the car’s value rapidly decreases.

- Rolling Over Loans: Incorporating remaining debt from a previous car into a new loan can immediately create negative equity.

Understanding these factors is key to avoiding or mitigating negative equity and ensuring a financially stable ownership experience.

The Rise of Negative Equity in Car Loans

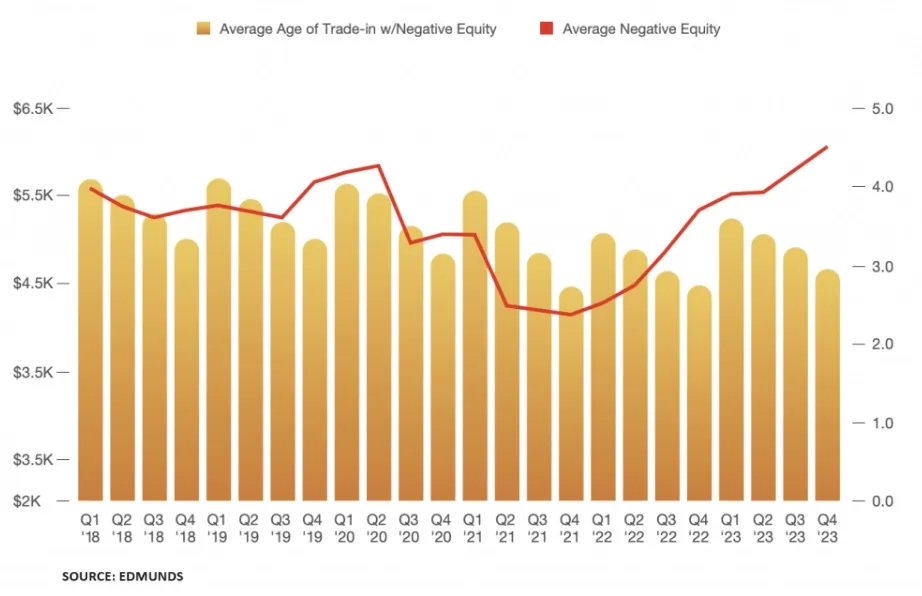

The phenomenon of negative car equity has been escalating, with recent Edmunds data revealing that 1 in 5 trade-ins have negative equity. The situation has become particularly pronounced in the new car market, where 20.4% of trade-ins are underwater, marking a significant jump from 14.9% in Q4 of 2021.

The average negative equity on car loans has surged to $6,054, setting a new record. This increase is partly attributed to the economic fluctuations during the pandemic when many consumers purchased vehicles at higher prices, leading to loans that exceeded the depreciating value of their cars. Consequently, drivers who bought cars during the pandemic are now facing the brunt of this financial imbalance.

What Negative Equity Means For You

Having negative equity on a car loan is more than just a numerical imbalance. It’s a predicament that can have lasting financial repercussions. Negative equity limits the owner’s flexibility, complicating efforts to sell or trade in the car without incurring losses.

For those looking to buy a new vehicle, negative equity means that the debt from the current car can roll over into the new loan. This leads to a cycle of increased debt that never seems to go away. Moreover, negative equity can affect credit scores and future loan conditions.

To combat these implications, car buyers should prioritize loan repayment strategies that target the principal amount. Also, consider shorter loan terms to align with the depreciation of the vehicle, and stay informed about the car’s current market value to make timely financial decisions. If you’d rather avoid the risk altogether, leasing is also an option.

Tackling Negative Equity

Navigating out of negative equity requires a proactive and strategic approach. Here are comprehensive steps and solutions to help you manage or eliminate negative car equity:

- Accelerate Loan Repayment: One of the most straightforward methods to reduce negative equity is to make additional payments towards the loan’s principal. This will decrease the loan balance faster than the standard amortization schedule.

- Refinancing the Loan: If you have good credit and interest rates have dropped since you took out your original loan, refinancing can be a smart option.

- Consider a Shorter Loan Term: When refinancing, opting for a shorter loan term can result in higher monthly payments but will significantly reduce the interest cost and speed up equity building.

- Lease a New Car: If you’re frequently facing negative equity with purchased vehicles, leasing might be a better option. Leasing a car can provide predictable monthly payments and eliminate the risk of negative equity, as you return the vehicle at the end of the lease term.

- Cash-Injection on Trade-In: When looking to trade in a vehicle with negative equity, consider making a cash payment to cover the gap between the vehicle’s value and the loan balance. This can prevent the negative equity from rolling into the new loan.

- Stay Informed About Your Car’s Value: Regularly check your vehicle’s current market value using tools like Sell With CarEdge, where you can receive multiple online offers at once. This awareness can help you make informed decisions about when to sell or trade-in the vehicle before the negative equity grows too large.

By employing these strategies, you can tackle negative equity head-on and work towards a more stable financial situation with your vehicle. Each approach has its considerations, so it’s important to evaluate your financial circumstances and car value carefully before deciding on the best course of action.

GAP Insurance and Negative Equity

(Related) 👉 Check out this guide to navigating the finance office like a pro!

GAP (Guaranteed Asset protection) insurance is indeed related to the topic of negative equity in car loans. Thus kind of insurance is designed to cover the difference between the actual cash value of a vehicle and the balance still owed on the financing (loan or lease) in the event that the car is totaled or stolen. Here’s how it connects to negative equity:

- protection Against Negative Equity: If a car is totaled or stolen, standard auto insurance policies usually cover only the current market value of the vehicle. If you owe more on your loan than the car is worth (negative equity), you would have to pay the difference out of pocket. GAP insurance covers this “gap,” preventing the financial strain of paying off a loan for a car you no longer possess.

- Financial Safety Net: For car owners who are in negative equity, GAP insurance acts as a safety net, ensuring that they are not financially burdened by the remaining loan balance in case of total loss or theft of the vehicle.

- Recommended for Long-Term Loans and Small Down Payments: For those who finance with long-term loans or small down payments, it’s smart to consider GAP insurance. It’s especially wise for leases and loans where the term extends beyond the standard three to four years.

In the context of managing negative equity, GAP insurance doesn’t reduce the loan balance or directly help in getting out of negative equity. However, it provides financial protection against the consequences of having negative equity in the event of an accident or theft.

Learn more about GAP insurance with this in-depth guide

Help Is Available

Negative car equity, while daunting, is manageable with smart decisions and strategic actions. Understanding its roots and applying tailored strategies can lead car owners from the depths of financial strain to the clearer waters of financial stability and equity.

Want to learn more about how your particular situation may impact your ability to buy or sell? Chat with a CarEdge expert today. We’re here to help!

Sponsored by Insurify

Are you overpaying for car insurance?

Compare rates from top carriers in under 5 minutes. CarEdge users save an average of $996/year on auto insurance.

*Disclosure: CarEdge may earn a commission when you compare insurance quotes through our partner, Insurify. This does not influence our editorial content.*