The Death of the Affordable Car in America

Key Takeaways

-

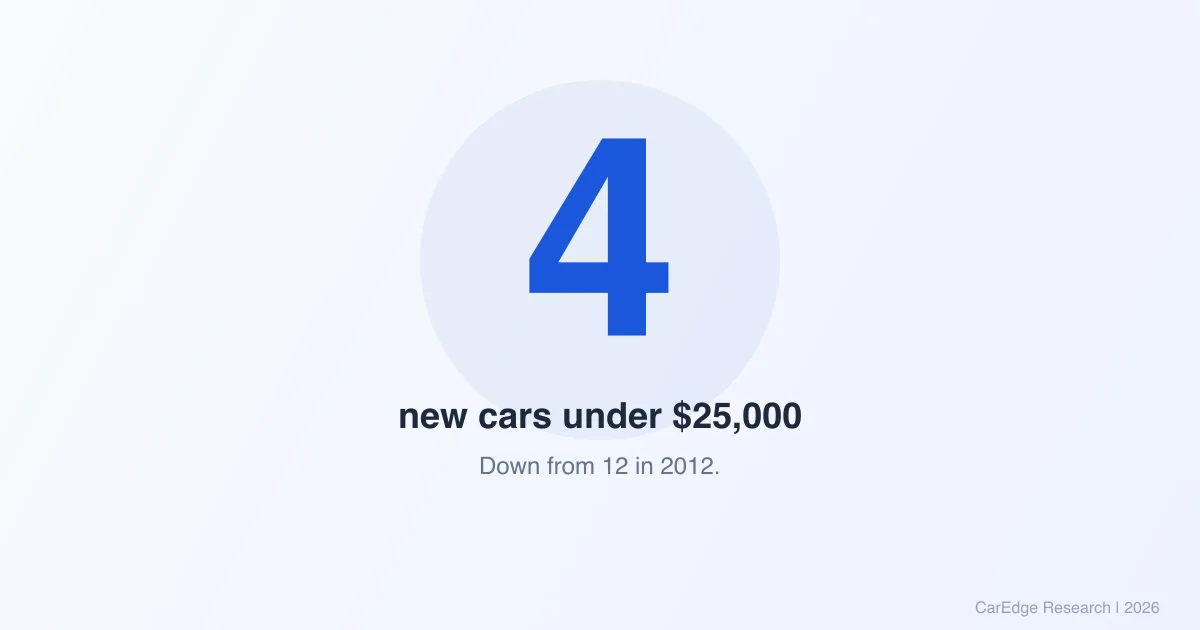

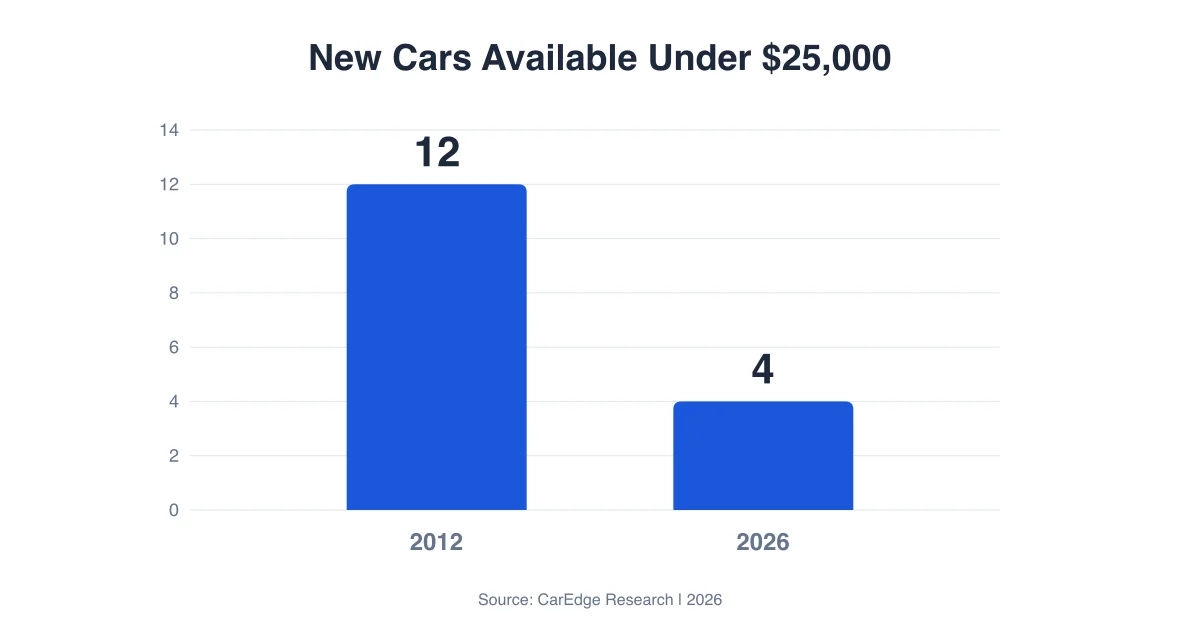

In 2012, roughly 12 new cars were available under $25,000 (inflation-adjusted). Today, only 4 remain — the affordable car is going extinct.

-

Auto repos are up 43% since 2022 and projected to top 3 million by end of 2025 — Great Recession territory. The average car payment is now $749/month.

-

Don't overpay. Use CarEdge to see what others are actually paying for any car, check ownership costs, and negotiate from a position of strength.

The New York Times published an opinion piece this week called “The Death of the Econobox.” The headline is catchy. The problem is, it doesn’t go far enough.

The affordable car in America didn’t just die. It was killed — by 60 years of tariff protection, an industry-wide profit pivot to trucks and SUVs, and a regulatory structure that actively punishes automakers for building small, cheap vehicles. And the people paying the price aren’t the ones making these decisions. They’re the ones skipping oil changes because an $840 mechanic visit would wreck their checking account.

Here’s the full picture — by the numbers, by the policy, and by what you can actually do about it right now.

The Affordability Crisis, By the Numbers

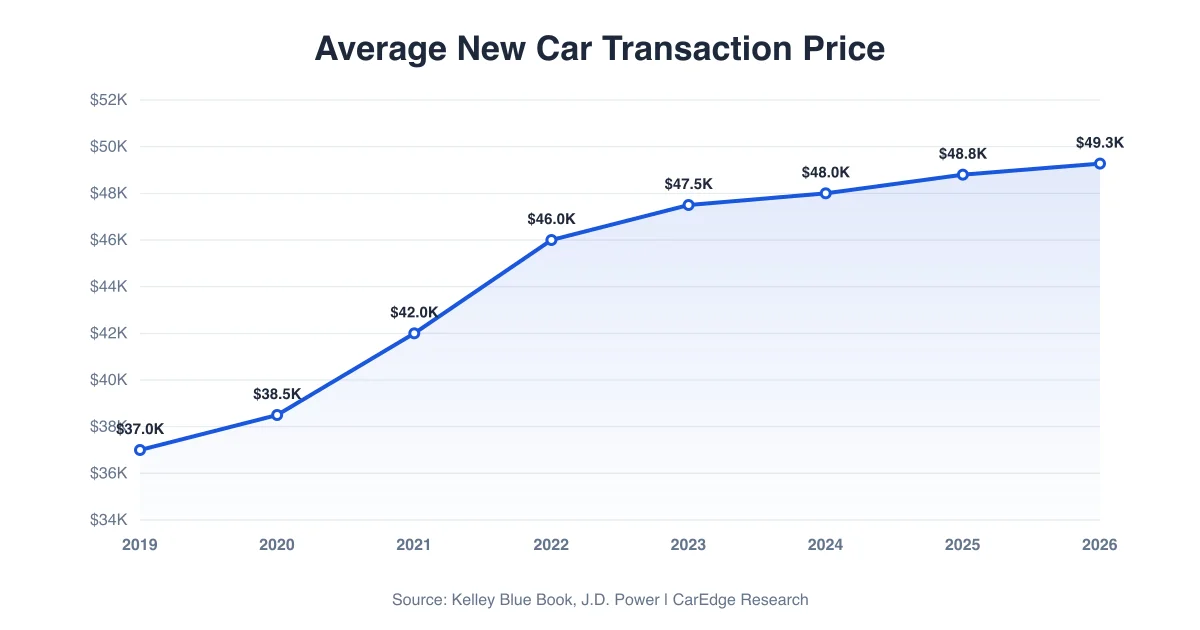

The average transaction price for a new car in America hit $49,275 in March 2026, according to Cox Automotive and Kelley Blue Book. That’s not MSRP — that’s what people are actually paying. A decade ago, the average was closer to $33,000. Adjusted for inflation, new cars have gotten meaningfully more expensive, not just nominally higher.

The monthly payment math is brutal. The average new car payment is $749 per month. One in five new car buyers is now committed to payments of $1,000 or more. Stack insurance on top — often $300 to $500 per month depending on the vehicle and your state — and you’re looking at $1,200 to $1,500 a month just to own and insure a car you haven’t even put gas in yet.

“Just buy used” isn’t the escape hatch it used to be. The average used car now costs ~$26,000, up 18% over five years. Interest rates on used car loans are running above 10% APR. The average used car monthly payment is $529. And the average used car for sale has over 70,000 miles on it. You’re paying more, for more miles, at a higher rate.

The supply of truly affordable used vehicles — the under-$15,000 cars that first-time buyers and working families depend on — has a 38-day supply. That’s tight. Those cars sell fast because there are so many people competing for so few of them.

Read our full breakdown: Car Market Update for Spring 2026

Four Cars. That’s It.

In 2012, roughly 12 new car models were available for under $25,000 in inflation-adjusted dollars. Hatchbacks, sedans, compacts — you had choices. Today, that number is 4. The Nissan Versa, Nissan Kick, Mitsubishi Mirage, and Kia Forte are essentially the last affordable new cars standing in America.

That’s not a market. That’s a rounding error.

For context: in 1973, you could buy a brand-new Honda Civic for $2,100 — about $15,100 in today’s dollars. Today’s Civic starts at over $28,000. The car that democratized reliable transportation in America is now firmly a mid-range purchase. The average F-150 Platinum Plus will run you roughly $90,000. A basic F-150 in 1990, adjusted for inflation, was around $29,000.

The vehicles didn’t just get more expensive. The cheap ones disappeared entirely. And that didn’t happen by accident.

How We Got Here: 60 Years of Protecting Profits Over People

The death of the affordable car is a policy story as much as it is a market story. Three forces converged over decades to kill cheap cars in America.

The Profit Pivot to Trucks and SUVs

Automakers figured out something in the 2000s that changed the industry permanently: trucks and SUVs have dramatically higher profit margins than sedans. A $60,000 F-150 might generate $15,000 or more in profit per unit. A $22,000 Fiesta might generate $1,500. The math was obvious.

Ford killed the Fiesta, Focus, Fusion, and Taurus. GM dropped the Cruze, Sonic, Spark, and Impala. Chrysler hasn’t had a competitive sedan in years. The industry collectively decided that building affordable cars wasn’t worth the effort — not when they could sell $50,000+ crossovers instead.

Six Decades of Tariff Protection

American automakers have been shielded from foreign competition on trucks and commercial vehicles since 1963, when the so-called “Chicken Tax” imposed a 25% tariff on imported light trucks. Originally a retaliatory measure against European tariffs on American chicken, it became the most durable protectionist policy in modern automotive history. For 60 years, it guaranteed that Ford, GM, and Chrysler could dominate the truck market without serious import competition.

The protection didn’t stop there. In the 1980s, the Reagan administration imposed “voluntary” import quotas on Japanese automakers, capping the number of vehicles they could ship to the U.S. The quotas pushed Japanese brands upmarket — Toyota created Lexus, Honda created Acura, Nissan created Infiniti — and reduced the supply of affordable imports.

The Trump and Biden administrations added new layers: 25% tariffs on Chinese vehicles, 100% tariffs on Chinese EVs, and 25% tariffs on imported auto parts. Each round of protection raised the floor price of vehicles available to American consumers while shielding domestic automakers from having to compete on affordability.

The Fuel Economy Loophole

Here’s the one almost nobody talks about. Federal fuel economy standards (CAFE) have long used a formula that gives larger vehicles — trucks and SUVs — more lenient targets based on their “footprint.” The bigger the vehicle, the easier the standard. This created a perverse incentive: automakers could meet their fleet-wide fuel economy obligations more easily by selling bigger vehicles and killing smaller ones.

When Ford discontinued the Fiesta and Focus, it wasn’t just a profit decision. It was a regulatory one. Every small, efficient car they sold made the math harder. Every F-150 made it easier. The regulations designed to promote fuel efficiency actually accelerated the death of the small car.

The Human Cost

The statistics are alarming enough on their own. But what does this actually mean for real people?

Repossessions are surging. Auto repos jumped 43% between 2022 and 2024, according to Cox Automotive, and are projected to exceed 3 million by end of 2025. That’s Great Recession territory. Millions of Americans are losing their cars — and in most of the country, losing your car means losing your ability to get to work, pick up your kids, and keep your life together.

Repair costs are crushing. Auto repair costs are up 15% year-over-year, with the average repair visit running about $840. Forty percent of Americans can’t cover that with cash on hand. So the car sits. Or the credit card comes out. Or the car gets traded in for something with a fresh payment and a fresh set of problems.

There’s a shame component to this that doesn’t get talked about enough. In most of America, not having a car isn’t a lifestyle choice — it’s a crisis. Public transit covers a fraction of the country. Employers expect you to show up. Schools expect you to pick up your kids. The entire infrastructure of American life assumes car ownership, and yet the cost of that ownership has moved beyond what tens of millions of people can sustain.

Check the real cost of owning any vehicle before you buy — insurance, maintenance, depreciation, and fuel costs vary wildly by model.

The Chinese Car Question

This is where the conversation gets uncomfortable for the industry.

BYD, China’s largest automaker, currently sells a vehicle called the Seal that is a direct competitor to the Tesla Model 3. The BYD Seal costs roughly $20,000 less than the Model 3 while offering more horsepower and a larger battery. In markets where both are available, the Seal is outselling Tesla.

Americans can’t buy one. The 100% tariff on Chinese EVs makes it economically impossible for BYD or any other Chinese automaker to import vehicles at competitive prices. But the rest of the world is moving on. Canada recently cut tariffs on certain Chinese EVs from 100% down to 6.1%. Europe has Chinese EVs on its roads. Southeast Asia, South America, the Middle East — BYD is now the world’s largest EV seller.

Trump himself floated the idea of Chinese automakers building factories in the United States during his Detroit Economic Club remarks. Ford CEO Jim Farley has publicly driven a Chinese-made Xiaomi SU7 and discussed the possibility of joint ventures. The question isn’t whether Chinese cars will come to America. It’s when, and on whose terms.

If a company can build a quality EV for $25,000 and sell it profitably — and BYD has demonstrated that it can — then the 100% tariff isn’t protecting American consumers. It’s protecting American automaker profit margins on $50,000 trucks.

For more on this: Will Chinese Cars Enter the U.S. Market in 2026?

What You Can Do Right Now

The policy environment is what it is. Tariffs aren’t coming down tomorrow. Automakers aren’t going to start building $18,000 sedans out of the goodness of their hearts. But you’re not powerless. Here’s how to play the hand you’re dealt.

Negotiate on Out-the-Door Price, Not Monthly Payment

This is rule number one and dealers violate it constantly. When a salesperson asks “What monthly payment are you comfortable with?” — that’s the setup. They can hit any monthly number by extending the loan term, burying negative equity, or padding the back end with warranties and add-ons. Always negotiate on the total out-the-door price including taxes, fees, and documentation charges. Then figure out the payment yourself.

Get Pre-Purchase Inspections on Used Cars

The average used car for sale has 70,000+ miles. You’re buying someone else’s problems unless you verify the condition independently. A $150–$200 pre-purchase inspection from a trusted mechanic can save you thousands. Never skip this. Don’t let a dealer tell you “our cars are inspected” — get your own.

Use CarEdge Data to See What Others Are Paying

Before you walk into any dealership, check CarEdge to see what other buyers in your area are actually paying for the vehicle you want. Know the market day supply. Know the depreciation curve. Know the real cost of ownership. Information is leverage, and most buyers leave thousands on the table because they negotiate blind.

Look at Overlooked Sedans and Leftover 2025 Models

The best deals right now are on vehicles nobody’s talking about. Sedans like the Nissan Altima, Hyundai Elantra, and Chevrolet Malibu are sitting on lots with real incentives. There are still nearly 580,000 leftover 2025 model year vehicles on dealer lots with manufacturer financing as low as 0% APR for qualified buyers. Those are the deals hiding in plain sight.

Call Your Lender Before You Miss a Payment

If you’re struggling with your current car payment, call your lender before you fall behind. Most lenders have hardship programs — deferments, extensions, modified payment plans — but they’re only available if you’re proactive. Once you miss a payment and the repo process starts, your options shrink dramatically. A five-minute phone call can be the difference between keeping your car and losing it.

The Bottom Line

The affordable car didn’t die of natural causes. It was killed by an industry that found better margins elsewhere, protected by 60 years of tariff policy that insulated domestic automakers from having to compete, and buried by regulations that inadvertently rewarded building bigger, more expensive vehicles.

The result is an America where the average car payment approaches $750 a month, repos are at crisis levels, and there are exactly four new cars left under $25,000 — none of which are particularly good.

That’s not a free market. It’s a market that’s been engineered to extract maximum profit from consumers who have no alternative but to drive.

We’re going to keep tracking these numbers, keep calling it out, and keep building tools that give buyers an edge. Because somebody has to.

Use CarEdge before your next car purchase. See real transaction prices, ownership costs, and depreciation data for every vehicle on the market. The data is free. The leverage is priceless.

— Zach & Ray

Data sources: Cox Automotive, Kelley Blue Book, CarEdge Research, The New York Times, Edmunds, Bureau of Labor Statistics. All figures reflect the most recent data available as of April 2026.

Sponsored by Insurify

Are you overpaying for car insurance?

Compare rates from top carriers in under 5 minutes. CarEdge users save an average of $996/year on auto insurance.

*Disclosure: CarEdge may earn a commission when you compare insurance quotes through our partner, Insurify. This does not influence our editorial content.*