States eligibile for below invoice pricing and 100% free delivery:

Alabama, Arkansas, Texas, Oklahoma, Florida, Georgia, Kentucky, Louisiana, Maryland, Delaware, Mississippi, North Carolina, South Carolina, Tennessee, Virginia, and West Virginia.

Sign Up & Provide Info

1FTER4FHOPLE35495 · 3000 mi

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

Get access to the same vehicle valuation tool that dealers rely on. With Black Book, you’ll have insider data to accurately assess trade-in and purchase values—empowering you to negotiate the best possible deal.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

CarEdge, the best place to buy, sell, and own a car with confidence, recently surveyed 408 U.S. drivers to better understand how consumers are navigating the car market in 2025. The survey, conducted from May 16 to May 19, comes at a pivotal time. Following the implementation of U.S. auto tariffs on April 3, car prices, interest rates, and inventory levels have all been in flux. With uncertainty growing, CarEdge sought to answer a critical question: how are real drivers adapting their car buying behavior?

Survey participants represent a broad cross-section of car shoppers and owners, from those who’ve recently purchased to those holding off for the foreseeable future. The full survey is available at CarEdge.com. Below, we break down the most important findings from this May 2025 snapshot.

The survey responses paint a picture of a divided car market, shaped by mixed economic signals and widespread caution. Among all respondents, 16% reported purchasing a car after the April 3 tariff announcement, while another 12% said they had bought a vehicle shortly before the tariffs went into effect. A much larger share (52%) said they are still actively shopping for a car, while 20% said they have not purchased a vehicle in the past six months and do not plan to buy one in 2025.

Tariffs have clearly impacted perceptions. Interestingly, among those who bought their car before April 3, 38% acknowledged they made the purchase early specifically to avoid the risk of higher prices. Among those who purchased after April 3, 16% said they believe they paid more due to the tariffs, with the vast majority of post-tariff buyers (84%) saying they believe they did not pay more.

Looking ahead, half of respondents are still planning to buy a car before the end of 2025. Of those future buyers, about a third plan to purchase new, another third are shopping used, and the remaining 30% are still undecided.

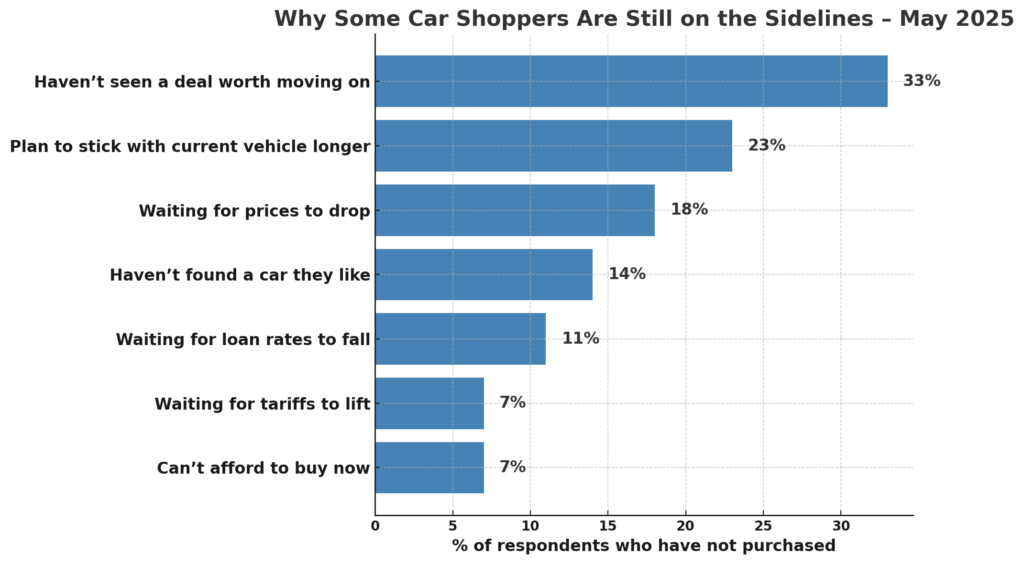

When it comes to what’s keeping people on the sidelines, affordability challenges and a lack of compelling deals top the list.

These are the barriers to buying (as a percent of all respondents who have not purchased):

With these top-line insights in mind, we next explore specific groups within the survey to uncover how recent and future car buyers are thinking about today’s market.

Survey respondents who purchased a car in the six months leading up to April 3 offer another layer of insight. Among these buyers, 61% purchased new and 39% purchased used.

What stands out most in this group is that more than a third (38%) said they intentionally bought their car early to avoid potential price hikes from tariffs. For the remaining 62%, tariffs didn’t factor into the timing of their purchase.

Income again played a role in how buyers approached the market. Among households earning $200K or more, just 22% said they made their purchase early in response to the looming tariffs. Nearly half (48%) of buyers earning between $100K and $199K did the same. In contrast, 39% of buyers earning under $100K said they bought early to avoid tariff-related price hikes.

This suggests that low- to middle-income consumers were more likely to act on policy changes and proactively adjust their buying timeline. Higher-income households, on the other hand, may not have been as concerned about the possible impact of tariffs on car prices this spring.

For respondents who bought a car after the April 3 tariff rollout, the data reveals a blend of resilience and skepticism. Among this group, 81% purchased a new vehicle, while 19% opted for a used one.

Despite the added costs associated with the new tariffs on imported vehicles, most post-April 3 buyers didn’t feel the sting. A strong majority—84%—said they don’t believe they paid more as a result of the tariffs. Still, 16% acknowledged they believe they did.

Among buyers who purchased after the April 3 tariff implementation, a different pattern emerged. Higher-income households were more likely to believe tariffs increased the price they paid. Specifically, 27% of households earning over $200,000 said they believed they paid more because of tariffs. In contrast, only 11% of households earning between $100,000 and $199,999 felt the same. Meanwhile, 17% of buyers with incomes under $100,000 said they believed tariffs had raised their purchase price.

These results suggest that while tariffs haven’t universally discouraged buyers, those with tighter budgets and those with a keen eye on policy changes are the most attuned to their potential impact.

Among those still planning to buy a car in 2025, the data reveals a thoughtful and strategic group of shoppers. Less than half (44%) of active shoppers expect to make their purchase within the next three months, while a majority (56%) plan to buy later this year.

When it comes to what they’re looking for, 54% say they’re in the market for a new car. About 19% are shopping for used vehicles, while just over a quarter are still unsure.

As for why these shoppers haven’t yet moved forward, deal quality remains the leading barrier. Respondents were asked to select all reasons why they have yet to purchase in 2025. 50% say they haven’t seen an offer worth acting on, while 30% are waiting for prices to come down. Another 21% say they haven’t found a car or truck they like. A smaller group is holding out for lower loan rates (18%), while tariffs were cited by just 11% of active shoppers.

One-fifth of active shoppers said that their decision to keep their current vehicle for longer was a factor in delaying their purchase.

Looking at the income distribution of active shoppers, the data continues to reflect a largely middle-income profile. The majority fall between $50K and $149K in household income, suggesting that many of these buyers are financially capable, but remain cautious in an uncertain economy.

Among drivers who have neither purchased a car in the past six months nor plan to buy one in 2025, a few clear themes emerge. This group is not driven by fear of rising costs or policy uncertainty, but rather by satisfaction with their current vehicle, and a lack of appealing options in today’s market.

The majority of these respondents (71%) say they’re sticking with their current vehicle longer, a sign that many Americans are adopting a “wait and see” approach to the market. Beyond that, 23% haven’t seen a deal worth moving on, while 9% say they haven’t found a car or truck they like. Price sensitivity remains a factor, with 20% waiting for prices to drop and 14% holding out for lower loan rates.

Concerns about tariffs are present, but not widespread. Among those on the sidelines right now, the reasons cited are roughly the same for all income segments. About one quarter say that they’re keeping their current vehicle for longer, while roughly 20% say they haven’t seen any deals worth acting on yet. The third most common reason for sitting out today’s car market is waiting for prices to come down. Only 7% cited tariffs as one of their reasons for not planning to buy a car in 2025.

The 2025 CarEdge Consumer Survey shows that the American car market remains fractured and cautious in the wake of economic headwinds and new policy shifts like auto tariffs. While some shoppers are moving forward with confidence, many are hesitant, skeptical, or simply waiting for conditions to improve.

The overarching takeaway? The car market in 2025 is no longer defined by pent-up pandemic demand or rapid inflation. Instead, it is being shaped by deal quality, interest rates, and policy awareness. For automakers, dealers, and car buyers alike, understanding these shifting motivations is key to navigating what’s shaping up to be one of the most complex car buying environments in recent history.

Founded in 2019 by father-and-son team Ray and Zach Shefska, CarEdge is a leading platform dedicated to empowering car shoppers with free expert advice, in-depth market insights, and tools to navigate every step of the car-buying journey. From researching vehicles to negotiating deals, CarEdge helps consumers save money, time, and hassle. Join the hundreds of thousands of happy consumers who have used CarEdge to buy their car with confidence. With trusted resources like the CarEdge Research Center, Vehicle Rankings and Reviews, and hundreds of guides on YouTube, CarEdge is redefining transparency and fairness in the automotive industry. Follow us on YouTube, TikTok, X, Facebook, and Instagram for actionable car-buying tips and market insights.

Negative equity, or owing more on a car loan than the vehicle’s market value, continues to rise as inflationary pressures and long loan terms take their toll on car buyers. CarEdge, in partnership with Black Book, surveyed 474 drivers in Q4 2024 to uncover the state of vehicle equity. Here are the highlights and the broader implications for drivers, car buyers, and the automotive industry.

👉 Download the complete report

In Q4 2024, 39% of drivers who financed their vehicles were underwater—up from 31% in Q3, a 25% jump. For cars purchased since 2022, the situation is even worse: 44% of these buyers owe more than their car is worth. As depreciation accelerates and long-term loans become the norm, the risk of negative equity continues to grow. This trend highlights a troubling financial burden on drivers and poses risks for the broader auto market.

Our survey reveals that 60% of drivers believe their car is worth more than its actual trade-in value. Of these, 18% overestimate by $5,000 or more, and 7% by over $10,000. This disconnect leads many to carry negative equity into their next car purchase, perpetuating financial strain.

When drivers attempt to trade in or sell their vehicles, they often face the harsh reality of lower-than-expected offers, which can derail their car-buying plans. Unfortunately, many choose to roll over the remaining debt into their next loan. This practice, while common, leads to higher monthly payments and extended loan terms, keeping buyers in a cycle of financial vulnerability.

Loan terms significantly impact vehicle equity. Borrowers with 84-month loans face a median negative equity of -$8,485, while those with shorter 36-month terms have a positive median equity of $7,783. While longer loans make monthly payments more affordable, they also leave buyers trapped in equity-negative positions for years.

For many buyers, the appeal of lower monthly payments outweighs the long-term risks. However, as loan balances decrease more slowly with longer terms, these borrowers are more likely to face financial strain when attempting to sell or trade in their vehicles. Buyers who opt for shorter terms and make larger down payments tend to build equity more quickly, putting them in stronger financial positions.

Electric vehicle owners face the highest negative equity rates, with 54% underwater and a median equity of -$2,345. This makes EVs particularly vulnerable compared to gas and hybrid vehicles, which are more likely to have positive equity.

The rapid depreciation of EVs is a key driver of this trend. EV technology can become outdated quickly as newer models with improved range, charging speeds, and driver assistance features enter the market. Additionally, concerns about costly battery replacements and limited resale demand have led many buyers to prefer new EVs with warranties and a known history, further impacting the resale value of used EVs.

For EV buyers, understanding depreciation trends and factoring in long-term costs is critical to avoiding significant negative equity. Opting for shorter loan terms and considering potential incentives or tax credits can help offset some of the financial risks. Buyers who plan to hold on to their EVs for longer than just a few years are less likely to be impacted by negative equity with their auto loans.

As we head into 2025, the issue of negative equity looms large for both consumers and the auto industry. For car buyers, rolling over negative equity into new loans can lead to long-term financial stress, reducing their purchasing power and limiting options. For the auto industry, high levels of negative equity could dampen trade-ins and slow new car sales, forcing automakers and dealerships to adjust their strategies.

Car dealers also face challenges when appraising trade-ins with negative equity. To close deals, dealers may need to discount new vehicles more aggressively or offer creative financing solutions, which can erode profit margins. Over time, high levels of negative equity in the market can disrupt the typical sales cycle

The Q4 2024 Negative Equity Report paints a clear picture of a growing issue in the car market. Drivers, car buyers, and the auto industry alike must address the challenges posed by rising negative equity.

CarEdge remains committed to empowering consumers with tools and insights to navigate today’s challenging car market. To avoid falling into the negative equity trap, car buyers should prioritize shorter loan terms, be familiar with expected car depreciation, and monitor used car values with tools like Black Book. Overcoming negative equity is possible when drivers make informed car buying and ownership decisions.

Negative equity, or being “underwater” on a car loan, is becoming a growing issue for many drivers in today’s market. As vehicle prices soar and depreciation accelerates, more car owners are finding themselves owing more on their loans than their cars are worth. CarEdge, in partnership with Black Book, surveyed nearly 1,000 drivers to understand the extent of this problem in Q3 2024. Here are the key findings.

👉 Download the complete report

According to our survey, 31% of drivers who financed their vehicles are currently in negative equity. This number rises to 39% for vehicles purchased since 2022, indicating that newer car buyers are especially vulnerable. As vehicle prices increase and long loan terms become more common, the risk of being underwater is higher than ever.

A staggering 61% of surveyed drivers overestimate how much their cars are worth, with 17% believing their vehicle is worth at least $5,000 more than its true trade-in value. This disconnect can lead to unpleasant surprises when drivers try to trade in or sell their cars, often rolling over negative equity into their next auto loan and perpetuating the cycle.

Our data shows that loan terms directly impact vehicle equity. Car owners with 84-month loan terms are nearly $5,000 underwater on average, while those with 36-month loans typically have $12,340 in equity. Although longer loans reduce monthly payments, they also increase the likelihood of negative equity in the long term.

Electric vehicle owners are significantly more likely to be underwater. Of the EV owners we surveyed, 46% are currently in negative equity, with a median loan-to-value (LTV) ratio of 0.94—higher than the broader market’s 0.73. Luxury car brands like Tesla and BMW also see higher rates of negative equity compared to budget brands like Toyota and Honda.

As more drivers find themselves underwater on their car loans, the negative equity issue is poised to become a major challenge for car owners and the auto industry alike. While budget car buyers may fare better, EV and luxury car owners are disproportionately affected.

CarEdge remains committed to providing insights and tools to help consumers navigate today’s car market. To learn more about vehicle equity and stay informed on auto news and market trends, visit CarEdge for expert analysis and guidance. For more information about Black Book’s industry-leading data and analytics, visit BlackBook.com.

Notifications