CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

Let’s clear the air right off the bat. December is the best time to buy a car if you’re in the market for one. At CarEdge, we’re all about doing what’s smart for your wallet. Even with the best offers in years, and prices slowly falling, it continues to make the most sense to keep driving the vehicle you have. But for those pondering buying now or holding off until 2024, here are three reasons why December is the car buying month you’ve been waiting for.

As we usher in December 2023, new-vehicle inventories have soared to levels not seen since spring 2021, marking a significant turnaround. Cox Automotive reports a robust 70-day supply of vehicles as we step into the month, a stark contrast to the inventory drought experienced just a year ago. New car inventory in America, now at about 2.5 million vehicles, has seen an additional increase of 100,000 in November alone.

This surge represents a gain of 890,000 vehicles compared to the previous year, and the highest new car inventory since the early months of 2021. Before the COVID-19 pandemic, new car inventory levels typically hovered between 3 million and 4 million vehicles in the U.S. The past year’s recovery, particularly evident from summer 2022, marks a pivotal shift in the availability of new vehicles for consumers.

Inventory has reached a 2-year high just as OEMs approach the new year, a time when they’re eager to sell 2023 model year vehicles to make way for incoming 2024s. This inventory rebound is a promising sign for buyers. When inventory rises, deals and incentives are sure to follow. And right on cue, massive deals are here.

See the Most and Least Negotiable New Cars Today

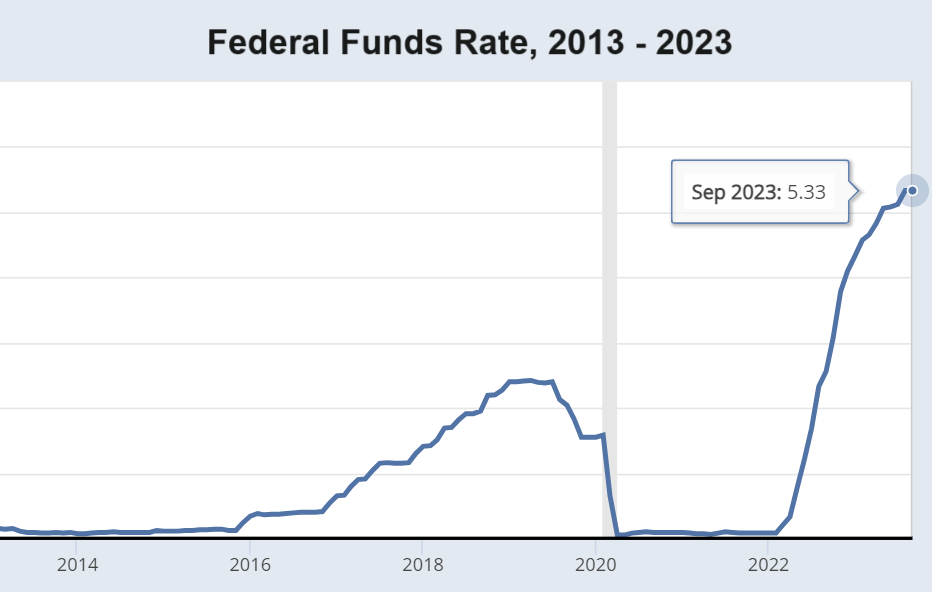

The cost of financing a car purchase hasn’t been this high since the late 1990s. In December, the average new car loan finance rate is 9.96% APR. Used car loan rates are even higher, nearing 14% APR.

Following the Federal Reserve’s recent decision to maintain the federal funds rate between 5.25 to 5.5 percent, many are wondering if we’re done with rate hikes. This marks the third time in the last four meetings that the Fed has opted for rate stability, despite having raised rates a total of 11 times in this economic cycle to counter high inflation.

However, the question looms: how will new car financing costs change in 2024? The answer lies in the word ‘incentives’.

As we enter the peak of December’s year-end car sales, automakers are rolling out their best financing offers of the year. But with borrowing costs at near 20-year highs, these attractive incentives from OEM’s captive lenders are likely to vanish come early January. Automakers aren’t offering low APR deals because they want to, they’re doing it because they need to sell cars before the new year arrives.

Click here for our FREE auto finance cheat sheet!

It’s becoming clear that interest rates will hardly budge in 2024. The median of financial industry’s projections predicts that the Federal Funds Rate at 5.1% at the end of 2024, representing just one 25 basis point interest rate cut for all of next year.

In other words, December 2023 will feature more low-APR offers than we should expect to see until this time next year. The generous 0% APR to 1.9% APR deals from brands like Mazda and Hyundai are expected to be short-lived.

In the new year, new car shoppers should expect more 3.9% to 4.9% APR offers, and far fewer zero percent financing incentives.

This December, car buyers are presented with a rare opportunity: securing low-interest rates through manufacturer incentives, complemented by some exceptionally lucrative cash offers and great lease deals. The increasing cost of borrowing is driving automakers and dealerships to entice buyers with more attractive financing options, even as these rising rates add to the pressure on dealerships to offload their inventory.

Automakers don’t mind leasing their new car inventory one bit. When a car is leased, a third-party financer takes ownership of the vehicle, so the car dealer and automaker still get the benefit of ‘selling’ the car.

In December, there are some truly amazing lease offers. Here are a few of the standout lease deals this month:

See ALL of the best lease offers in December

Leading the charge with zero percent financing on select models are automakers like Mazda, Nissan, and Hyundai. Once a staple in the auto market, 0% APR deals have become a rarity in today’s high-interest rate climate. Not far behind are brands like Kia, Honda, and several Mazda models, offering enticing 0.9% APR deals. Plus, there are’s an abundance of 1.9% APR offers from General Motors, including for the Silverado 1500.

This array of year-end sales provides an unmatched opportunity for car buyers looking for value in a turbulent market.

Explore all the best year-end car sales here.

At CarEdge, December is the month we’ve all been waiting for. The combination of high inventories, appealing year-end deals, and the likelihood of returning to high financing rates creates a unique window for securing a great deal on a new vehicle.

Ready to approach car buying with behind-the-scenes market insights? Try CarEdge Data for local price and inventory updates in real-time. CarEdge Data equips you with negotiation leverage like never before!

Ready to outsmart the dealerships? Download your 100% free car buying cheat sheets today. From negotiating a deal to leasing a car the smart way, it’s all available for instant download. Get your cheat sheets today!

Honda’s new car inventory has risen 38% in just two months. Just in time for the best year-end car sales in ages, an oversupply of both new and used Honda models presents a rare opportunity to negotiate a great deal. We’ll take a look at which new and used Honda cars and SUVs are the most negotiable today, and how you can make a data-powered deal in December.

Snapshot:

Read on for the latest details and money-savings tips.

December is always the best time to buy a car. This is especially true for new Honda inventory in 2023. What’s so special about 2023’s year-end car deals? In a high interest environment, the biggest sales of the year are a long time coming. With automakers and dealers eager to sell remaining 2023 inventory, and everyone eyeing an end-of-year bonus, phenomenal deals are everywhere you look.

Today’s car buyers have options. For those willing to master car buying the smart way, thousands of dollars in savings await. Sure, you could simply browse the best Honda deals this month, or you could negotiate like a boss with the added leverage of Honda inventory numbers. CarEdge is here to help you get there.

First, let’s talk about the inventory trends of new Honda models in the U.S. Back in October, Honda was just beginning to climb out of the inventory lows that had plagued the automaker for a few years. Ever since the pandemic supply chain shortages pummeled Honda and other Asian automakers with record-low inventory levels, the beloved brand has been struggling to return to normal.

Finally, in late 2023, Honda’s supply of new cars is rising, to the benefit of holiday car shoppers.

By using a behind-the-scenes industry metric, we can see exactly how negotiable new or used cars are today. This metric is called Market Day Supply. Market Day Supply takes into account the existing inventory of a new or used vehicle, and the selling rate over the last 45 days. What you get is the number of days it would take to sell ALL vehicles in stock at current selling rates, assuming no new inventory was added. In simple terms, MDS reflects the level of demand for a car.

For starters, a ‘healthy’ MDS in the car market is somewhere between 45 and 60 days of supply. Anything below 20 days is a real shortage, and anything above 80 is a serious oversupply. Today, Honda averages a healthy 47 days of supply. For Honda, this is quite high. It’s all relative, though. If this was one of the domestic brands (Ford or Chevrolet, for example), 47 days of supply would be below average. For Honda, it’s higher than normal.

With the power of understanding market conditions in mind, let’s take a look at how much Honda’s new car inventory has risen in late 2023:

| Model | Year | October Market Day Supply | December Market Day Supply |

|---|---|---|---|

| Accord | 2024 | N/A (new model) | 56 |

| Accord | 2023 | 30 | 58 |

| Civic | 2024 | N/A (new model) | 50 |

| Civic | 2023 | 34 | 62 |

| CR-V | 2024 | 24 | 34 |

| CR-V | 2023 | 12 | 99 |

| HR-V | 2024 | 47 | 58 |

| HR-V | 2023 | 151 | 891 |

| Odyssey | 2024 | N/A (new model) | 45 |

| Odyssey | 2023 | 31 | 120 |

| Passport | 2024 | N/A (new model) | 55 |

| Passport | 2023 | 45 | 30 |

| Pilot | 2024 | N/A (new model) | 45 |

| Pilot | 2023 | 26 | 45 |

| Ridgeline | 2024 | N/A (new model) | N/A (new model) |

| Ridgeline | 2023 | 39 | 53 |

Overall, Honda’s new car inventory has risen from 34 market days of supply in October to 47 days of supply in December, an increase of 38% in just two months.

The jump in supply has been notably greater for some Honda models, such as the CR-V, and Accord. The selling rates of the Accord and HR-V are greatly skewed by a seatbelt recall that has affected 2023 and 2024 models. Dealers can’t sell affected HR-Vs and Accords until a fix is implemented.

However, with 2024 just days away, dealers will be eager to sell 2023 Accords and HR-Vs as soon as a recall fix is installed, making them particularly negotiable in the weeks ahead.

See new Honda listings with the power of local market data

With negotiation know-how, today is the ideal time to use local market data as leverage for negotiating a bargain of a deal.

Honda’s used cars are popular for several reasons. With great reliability ratings and high driver satisfaction, pre-owned Hondas are always quick to sell.

In December of 2023, used Honda inventory is rising. What could be behind this unusual trend? The culprit is clear: high interest rates. Today, the average used car loan rate is hovering around 14% APR. More and more car shoppers are opting for new car deals as opposed to forking over extra cash for interest on a used car loan.

Here’s a look at how hard Honda’s used inventory is being hit in today’s high-interest environment.

| Model | Year | October Market Day Supply | December Market Day Supply |

|---|---|---|---|

| Accord | 2022 | 49 | 60 |

| Accord | 2021 | 49 | 54 |

| Civic | 2022 | 50 | 60 |

| Civic | 2021 | 53 | 58 |

| CR-V | 2022 | 45 | 60 |

| CR-V | 2021 | 47 | 62 |

| HR-V | 2022 | 59 | 48 |

| HR-V | 2021 | 52 | 54 |

| Odyssey | 2022 | 74 | 79 |

| Odyssey | 2021 | 61 | 62 |

| Passport | 2022 | 56 | 76 |

| Passport | 2021 | 60 | 71 |

| Pilot | 2022 | 52 | 71 |

| Pilot | 2021 | 48 | 59 |

| Ridgeline | 2022 | 57 | 63 |

| Ridgeline | 2021 | 61 | 64 |

7 out of 8 used Honda models are seeing rising inventory in December. Does that mean that you should buy used instead of new? Not exactly. Honda is offering attractive APR deals in December, ranging from 1.9% to 3.9% APR. You will NOT be able to secure an auto loan rate anywhere near that low for a used car right now. With an average of nearly 14% APR, used car buyers with an excellent credit score will be lucky to qualify for anything under 7%.

If you can afford the higher sticker price, we recommend giving new Honda cars and SUVs a serious thought in today’s car market. You’ll save thousands in interest over the life of your loan.

See used Honda listings with the power of local market data

In closing, with Honda’s inventory hitting a peak and used car supply also on the rise, December 2023 is shaping up to be a buyer’s paradise. Whether you’re eyeing a new CR-V or considering a pre-owned Accord, the current market dynamics offer a unique opportunity for negotiation. Armed with the latest data and understanding of market trends, savvy shoppers are in a prime position to secure some of the best deals on Honda models before we ring in 2024. Don’t miss this chance to drive home value like never before!

See local market insights with CarEdge Data, the ultimate car buying toolkit.

Ready to outsmart the dealerships? Download your 100% free car buying cheat sheets today. From negotiating a deal to leasing a car the smart way, it’s all available for instant download. Get your cheat sheets today!

As we head into 2024, the automotive industry in the U.S. is at a pivotal crossroads. High interest rates, rising inventory, and online sales are just a few of the factors bringing change to car buying. To gain deeper insight into these evolving dynamics, we spoke with Zach Shefska, Co-Founder and CEO of CarEdge, to understand his perspective on where the car market is headed in the coming year. Finally, normalcy may be on the horizon for some of the car market.

A key driver in the 2024 car market is the elevated interest rates, now hovering around 10% for new cars and exceeding 14% for used vehicles. This hike in rates is squeezing consumer budgets, making it challenging to find affordable monthly payments.

On the dealer side, soaring floor plan expenses – up by 200% year-over-year in some cases – are turning once profitable inventory holdings into burdensome financial obligations. One dealer reported that their inventory floorplanning expenses have jumped from $49,000 to $670,000 per month as interest rates soared and manufacturers shipped more cars to their lots.

CarEdge’s Zach Sheska reminds us that it isn’t just buyers who hurt when interest rates rise. “80% of car buyers finance their purchase, a statistic that is falling as buyers who can afford to pay cash pay in full to avoid interest. However, it’s important to note that smart dealers will be more open to negotiating prices once they encounter a buyer with car market knowledge. They’re feeling the pain of interest too, and are incentivized to move inventory quickly.”

👉 Master car buying strategies with Deal School, our 100% FREE car buying course!

The automotive industry is undergoing a reversal of sorts. In both new and used car markets, we’re seeing a gradual but pronounced ‘return to normalcy’ reminiscent of the pre-pandemic state of affairs.

New car inventories have made a remarkable recovery from their pandemic lows, soaring to 2.40 million from a mere 0.9 million. This substantial increase in inventory, along with the urgency to address rising floor plan expenses, is compelling dealers to adopt lower pricing and more assertive sales tactics.

Is it a buyer’s market? If 2024 will be a buyer’s market remains to be seen. The good news is that market forces are headed in the right direction.

OEMs are offering the best sales and incentives in years, aiming to increase sales volumes to achieve yearly and quarterly sales goals. These developments, coupled with heightened operational costs and the reintroduction of cash and finance incentives, are clear indicators of a market that is stabilizing and adjusting to the challenges faced during the chip shortage and production interruptions of the past years.

The average cost of new and used cars remains high, exacerbating the affordability crisis for consumers. Today, the average price of a new car has fallen ever so slightly to $47,936, and used car prices average $26,533. In 2019, the average new car sold for $36,000, and used cars averaged $23,000.

👉 We track new car prices monthly

Historically, the most popular used car segment was vehicles under $20,000 with less than 50,000 miles on the odometer. That’s becoming harder to find these days. Recently, iSeeCars found that in 2023, only 11 percent of the used car market is priced between $15,000 and $20,000. The average listing in this price range has over 63,000 miles. On top of paying a higher sticker price, the average used car loan rate is now at a 20-year high of 14%.

However, increasing supply and growing dealer incentives are beginning to ease price pressures, offering some relief in a rising rate environment. To get a sense of where used car prices are headed in 2024, we can look at the best leading indicator that we have: wholesale used car price trends. At wholesale car auctions, used car prices have dropped 9% in two months. Some segments, such as used vans, compact sedans, and luxury crossovers, have dropped by 15% or greater.

See this week’s used car market update

Retail used car prices have been slower to fall, but are dropping nonetheless. “What’s changed more profoundly is negotiability in the used car market. CarEdge Coaches say that today, dealers are more willing to negotiate on prices and add-ons today than at any point in 2023. For car buyers willing to put in the work, a much better deal can be earned,” noted Zach.

On the new car front, year-end deals end soon. With rising new car inventory and 2024 models arriving daily, dealers and OEMs alike are eager to sell cars before the end of the year. Hyundai, Mazda, Nissan, and Honda are all offering limited 0% financing for select models. General Motors, Ford, and Kia offer financing at 1.9% APR. With the average APR approaching 9%, anything under 5% APR is a great deal.

👉 See the best new car deals this month (financing, cash offers, and leases)

A significant headline moving into 2024 is Amazon’s partnership with Hyundai to sell new vehicles through Amazon.com. At first glance, this would seem to indicate a shift towards online retail in the automotive sector. However, challenges remain, particularly in the relationship dynamics between auto manufacturers and car dealers.

Zach says that a reality check may be in store. “Amazon is about to find out the hard way that for legacy car brands, dealerships have the final say in vehicle pricing and customer service. Amazon’s strategy of partnering directly with OEMs may face hurdles due to the historically complex relationships between these OEMs and their dealers. Dealers will push back, especially if the Amazon partnership targets their profit centers.”

Automotive News outlined the many questions that remain unanswered about the Amazon-Hyundai partnership. Right now, there are more questions than answers.

Here at CarEdge, we’re taking a different route to ‘fixing’ car buying, one that’s guaranteed to have more immediate impacts. By pre-negotiating fixed pricing directly with car dealers, CarEdge has introduced a new level of transparency never before seen in the new car market.

With nationwide shipping, anyone can buy a new car with fair and transparent pricing, all without the hassle of talking to a dealership salesperson. CarEdge’s team of industry experts takes care of it all. Will Amazon find a way to provide a customer experience that’s equally stress-free and pro-consumer? That remains to be seen.

Learn more about buying with CarEdge.

Last month, U.S. electric vehicle sales surpassed 1 million annual sales for the first time ever. EV sales now account for 8% of all new cars sold in America. By 2024’s end, we expect that figure to be closer to 12%, and maybe a tad higher.

As charging infrastructure improves, more car buyers are willing to make the switch. Tesla will continue to dominate with over 50% of EV sales, but the likes of Hyundai, Kia, Ford, and GM will continue to grow in market share.

One year ago, EV transaction prices averaged 20% higher than the overall new car market. Today that price gap has narrowed to 14%. Automakers and dealers alike make less profit per EV sold than they’re historically used to with ICE vehicle sales. If EV sales continue to grow, that will put pressure on every facet of auto sales. How will the industry respond to narrowing profits? Will dealers and manufacturers simply recoup profits by raising prices in ALL vehicle segments? 2024 will shed light on that, too.

Rising interest rates, evolving market dynamics, and online car buying platforms are reshaping the way we buy cars. The gradual return to pre-pandemic norms and shifting consumer preferences hint at a market ripe with opportunities for informed buyers. While challenges like affordability persist, the increase in manufacturer and dealer incentives are promising signs.

With that said, surprises will introduce wildcards to the market. From economic recession to geopolitics, it’s impossible to know where the world will stand in 12 month’s time. Staying on top of the latest market updates will be key to making smart purchasing decisions in the evolving automotive world of 2024.

Ready to outsmart the dealerships? Download your 100% free car buying cheat sheets today. From negotiating a deal to leasing a car the smart way, it’s all available for instant download. Get your cheat sheets today!

What do the top states for year-end car deals in 2023 have in common? It’s simple: the best states for December bargains have affordable, popular models with high inventory this month. We can’t say it enough: where there’s high new car inventory, opportunities for negotiation offer the chance for major savings. With today’s high interest rates, saving a thousand dollars means more than ever.

It’s important to keep in mind that today’s new car market is dynamic, with inventory levels, manufacturer incentives, and dealer’s willingness to negotiate constantly in flux. That’s why the latest data is critical for car buyers on the hunt for deals in December. Using CarEdge Data, we’ve looked at the market day supply of new cars in all 50 states to uncover opportunities for extra savings.

Why does market day supply matter to car buyers everywhere? If you like to save money on your car purchase, you should start paying attention to this little-known industry metric. Market Day Supply (MDS) is calculated by dividing the current inventory of a specific car model by the average number of units sold per day. In a ‘normal’ healthy market, MDS averages somewhere between 40 and 60 days of supply for mainstream models. Today, the nationwide average for new cars is 83 days of market supply. In states with the highest negotiability, MDS figures are MUCH higher.

With the power of local market data, we now have a clear picture of where the greatest oversupply of new cars is today. Without further ado, here’s a look at the best states for year-end car deals in 2023.

Vermont

New car market day supply: 101 days

The most negotiable new cars right now: Ford Mustang Mach-E (238 days of supply), Jeep Wrangler Unlimited (194 days of supply), Ford Escape (129 days of supply), Ram 1500 (129 days of supply)

Louisiana

New car market day supply: 97 days

The most negotiable new cars right now: Dodge Charger (453 days of supply), Ford F-150 (194 days of supply), Ram 1500 (181 days of supply), Ford Explorer (175 days of supply), Chevrolet Silverado 1500 (154 days of supply)

Nebraska

New car market day supply: 97 days

The most negotiable new cars right now: Ram 1500 (219 days of supply), Ford F-150 (176 days of supply), Chevrolet Silverado 1500 (93 days of supply)

Oklahoma

New car market day supply: 82 days

The most negotiable new cars right now: Dodge Charger (444 days of supply), Jeep Grand Cherokee (387 days of supply), Ford Edge (374 days of supply), Ram 1500 (186 days of supply), Ford F-150 (168 days of supply)

Montana

New car market day supply: 96 days

The most negotiable new car right now: Chevrolet Silverado 1500 (136 days of supply)

Washington

New car market day supply: 89 days

The most negotiable new cars right now: Ram 2500 (444 days of supply), Jeep Wrangler Unlimited (353 days of supply), Ram 1500 (296 days of supply), Ford Mustang Mach-E (295 days of supply)

👉 Can you buy a car in another state? Yes! Here’s how.

Remember, the key to unlocking great year-end deals lies in understanding local market dynamics. States with higher-than-average Market Day Supply (MDS) are your hotspots for negotiation. Whether you’re in the Northeast looking at a Mustang Mach-E, or in the West Coast market for a Jeep Wrangler Unlimited, the end of the year presents a unique window of opportunity.

Don’t miss the best year-end manufacturer incentives, from 0% APRs to phenomenal leases.

Ready to outsmart the dealerships? Download your 100% free car buying cheat sheets today. From negotiating a deal to leasing a car the smart way, it’s all available for instant download. Get your cheat sheets today!

Northeast Region

| State | Market Day Supply (December) |

|---|---|

| Connecticut | 91 |

| Delaware | 80 |

| Maine | 89 |

| Maryland | 76 |

| Massachusetts | 85 |

| New Hampshire | 74 |

| New Jersey | 85 |

| New York | 81 |

| Pennsylvania | 85 |

| Rhode Island | 84 |

| Vermont | 101 |

| Virginia | 84 |

Southeast Region

| State | Market Day Supply (December) |

|---|---|

| Alabama | 83 |

| Arkansas | 81 |

| Florida | 77 |

| Georgia | 79 |

| Kentucky | 86 |

| Louisiana | 93 |

| Mississippi | 85 |

| North Carolina | 77 |

| South Carolina | 78 |

| Tennessee | 80 |

| Virginia | 84 |

| West Virginia | 87 |

Southwest Region

| State | Market Day Supply (December) |

|---|---|

| Arizona | 82 |

| New Mexico | 82 |

| Texas | 80 |

| Oklahoma | 82 |

Midwest Region

| State | Market Day Supply (December) |

|---|---|

| Illinois | 85 |

| Indiana | 80 |

| Iowa | 91 |

| Kansas | 84 |

| Michigan | 87 |

| Minnesota | 81 |

| Missouri | 86 |

| Nebraska | 97 |

| North Dakota | 85 |

| Wisconsin | 79 |

Interior West

| State | Market Day Supply (December) |

|---|---|

| Colorado | 80 |

| Montana | 96 |

| Wyoming | 92 |

| Utah | 87 |

| Nevada | 82 |

| Idaho | 83 |

Pacific Coast

| State | Market Day Supply (December) |

|---|---|

| California | 83 |

| Oregon | 89 |

| Washington | 89 |

If you’ve been holding off on a used car purchase due to record high used car prices, December brings good news for buyers. So far, market declines have been largely confined to wholesale auctions. Will wholesale price drops finally translate to lower sticker prices? Let’s dive in and talk about why December 2023 is different.

For much of 2023, there has been an unusually wide gap between auto auction price trends and the listing prices we’ve seen on dealer lots. However, with changes accelerating over the past month, it looks like retail used car prices are finally about to take a dive.

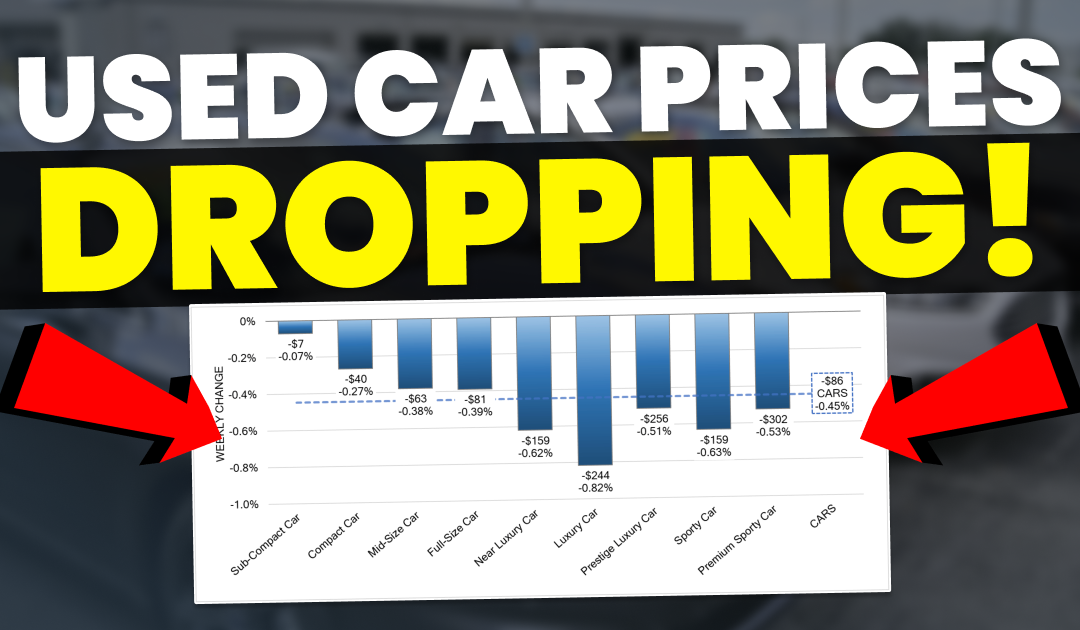

In November alone, used car prices were down -5.47% at wholesale auctions, according to Black Book weekly updates. The magnitude of this downward trend isn’t normal. In fact, prices are dropping at 5x to 6x the normal rate for some vehicle segments.

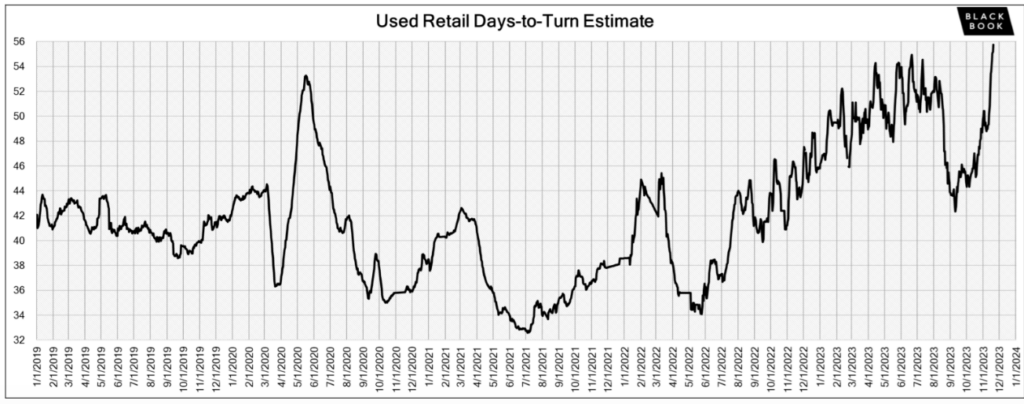

Retail days-to-turn, a metric indicating how long it takes for used cars to sell, has reached a 5-year high at 55 days. This statistic suggests that used cars are staying longer on dealership lots, giving buyers more options and potentially putting pressure on dealers to make sales.

The stage is set for a buyer’s market in the used car industry, offering consumers greater choice and increased bargaining power.

Just how quickly are used car prices dropping? A closer look at the last month’s wholesale prices reveals shocking trends. The decline in used car prices is not uniform across all segments. Here’s how some of the most volatile used car segments fared in November:

Compact Vans: Down 13.98%

Full-size Trucks: Down 6.49%

Compact Cars: Down 6.98%

Full-size Luxury SUVs: Down 5.11%

Remember, these price drops occurred in only four weeks. Normally, price changes are measured in the tenths of a percentage point. These significant price changes indicate that certain vehicle categories are experiencing rapid depreciation. With negotiation know-how, car buyers have more leverage than at any other point in 2023.

👉 Enroll in Deal School to master car buying today. It’s 100% free!

The allure of new car incentives is pulling buyers away from used car lots. As more buyers opt for new cars, the used car market is experiencing increasing downward pressure on prices. This trend indicates that used car buyers are very likely to see better deals in December. However, a used car purchase may not make sense for everyone. Let’s talk about why.

At a time when the average used car loan rate is at 14% APR, shoppers are second guessing a used car purchase with good reason. But that doesn’t mean you must hold off on buying altogether. Consider this: the best new car offers feature low and even zero percent financing offers. Our CarEdge Coaches are recommending that all used car shoppers consider low APR new car deals before committing to high interest used car loans.

👉 See the best year-end car sales today.

For more on how new car deals will impact used car prices, check out our deep dive.

Car dealers don’t typically own their lot inventory outright. They actually finance their inventory when they buy cars at the auction, and pay monthly ‘floorplanning costs’. With interest rates at 20-year highs, car dealers are feeling the pain like the rest of us. What does it all mean for used car buyers? Buyers should know that dealers are motivated to sell their inventory sooner rather than later, even if they try to act like they don’t need to. You certainly have negotiating power, especially in December of 2023.

CarEdge’s Ray Shefska offers some valuable insights into the changing landscape of the used car market:

“We’re finally seeing a real correction in wholesale used car prices. My expectation is that we’ll soon see this translate to retail prices too. But even with stubbornly high dealership prices, you have MUCH more negotiating power today after a month of steep declines at the wholesale auctions that they buy cars from. Don’t hesitate to show the car salesperson that you’re aware of the recent used car price trends. Heck, print out the latest numbers if you have to. Not all car dealers will be willing to budge, but the smart ones will. You can always shop elsewhere.”

In conclusion, if you’re in the market for a used car, December 2023 may be the ideal time to make a purchase. High interest rates, increased inventory, slow used car sales, and enticing new car incentives have given used car dealers multiple reasons to lower their prices or at least display a willingness to negotiate. Interestingly, these same reasons are enticing more buyers to the new car market, especially with low APR offers featuring unmatched savings.

👉 If you’re in the market for a used car, bookmark this to stay on top of the latest: Used Car Price Trends (Updated Weekly)

Last month, the average used car selling price was $26,752. With what we’re seeing in today’s market, we wouldn’t be surprised if that figure is 10% less by the time we see the December data. December is the best time to buy a car in ages, for both new and used shoppers alike.

Here’s our car market forecast for 2024. We don’t expect the great deals to last into the new year!

Ready to outsmart the dealerships? Download your 100% free car buying cheat sheets today. From negotiating a deal to leasing a car the smart way, it’s all available for instant download. Get your cheat sheets today!