CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

We dug through the latest new car lease offers to find you the very best lease deals for October 2025. Tariffs are poised to send prices higher, but there are still some great lease specials if you know where to look. Skip ahead to your preferred auto brand to see what their best lease deals are this month. Check back for updates, as automakers typically announce new offers during the first week of each month.

👉 Note that these advertised offers exclude tax, title, and any fees due at signing!

Check out the best lease offers this month by brand below. You might also find our new car lease calculator to be helpful. Estimate your lease payment in seconds:

👉 See offer details from Acura and browse local inventory

👉 See offer details from BMW and browse local inventory

👉 See offer details from Buick and browse local inventory

In October, Cadillac has great offers for electric crossovers.

2025 Cadillac Optiq: Current GM owners and lessees can lease the Optiq from $479/mo for 24 months with $4,929 due.

👉 See current lease offer details from Cadillac and browse local inventory

Chevrolet has some of the best lease offers right now, with multiple models available with little money down. These are the best offers in October 2025:

👉 See offer details from Chevrolet and browse local inventory

These are Ford’s best lease deals in October, featuring lease deals with under $500 due at signing:

👉 See offer details from Ford and browse local inventory

GMC offers the best loan terms to current GM lessees. If you’re not a returning lease customer, the amount due at signing is likely to be higher. These offers are for select markets. See offer details.

👉 See offer details from GMC and browse local inventory

For October, Honda is offering low payment lease deals:

👉 See Honda offer details and browse local inventory

Hyundai has some of the best budget lease offers that you’ll find for October:

👉 Browse local Hyundai listings with market insights

👉 See Jeep offer details and browse local inventory

Kia has some of the cheapest car leases this month, especially on their fast-charging, long-range EVs and SUVs.

👉 See Kia offer details or browse local inventory

These are the best Mazda lease deals for October 2025 as summer deals get underway:

Nissan has some of the best new car lease offers this month as the automaker combats rising inventory and sluggish sales.

👉 Browse local Nissan listings

The Subaru Crosstrek is Subaru’s best value lease in October.

Tesla is offering cheap lease deals in October. The recently redesigned Model 3 has an extremely low total cost of ownership, making it one of the best lease deals period.

See Tesla lease offers at Tesla.com.

Toyota has some of the best lease deals today, especially for buyers in search of a reliable car with less depreciation. Note that Toyota’s offers are regional, and may vary by state.

👉 See Toyota lease offer details and browse local listings

This month, Volkswagen’s Iease deals are less than stellar.

👉 See Volkswagen for details or browse local listings

Ready to outsmart the dealerships in 2025? Download your 100% free car buying cheat sheets today. From negotiating a deal to leasing a car the smart way, it’s all available for instant download. Get your cheat sheets today!

We dug through the latest new car lease offers to find you the very best lease deals for October 2024. It’s becoming clear that year-end car sales are almost here! Skip ahead to your preferred auto brand to see what their best lease deals are this month. Check back for updates, as automakers typically announce new lease deals during the first week of each month. We’ve highlighted the very best lease deals in bold.

See offer details from Acura and browse local inventory

See current lease offer details from BMW and browse local inventory

See current lease offer details from Buick and browse local inventory

The best Cadillac lease deal is for the highly-acclaimed Lyriq luxury EV.

See current lease offer details from Cadillac and browse local inventory

Chevrolet has some of the best lease offers in October, with multiple models available with little money down. These are the best offers:

See offer details from Chevrolet and browse local inventory

See offer details from Dodge and browse local inventory

Ford’s lease offers are no where near as good as Chevrolet’s this month. These are Ford lease deals for October:

See offer details from Ford and browse local inventory

GMC offers the best loan terms to current GM lessees. If you’re not a returning lease customer, the amount due at signing is likely to be higher.

See offer details from GMC and browse local inventory

In October, Honda is offering low payment lease deals:

See Honda offer details and browse local inventory

Hyundai has some of the best budget lease offers that you’ll find in October:

See Hyundai offer details and browse local inventory

See Jeep offer details and browse local inventory

Kia has some of the cheapest car leases this month, especially on their fast-charging, long-range EVs and SUVs.

See Kia offer details or browse local inventory

See Lexus for details or browse local inventory

These are the best Mazda lease deals for October 2024:

See offer details from Mazda and browse local listings

Nissan has some of the best new car lease offers this month as the automaker combats rising inventory and sluggish sales.

See offer details from Nissan and browse local listings

See the latest Ram lease deals from CarEdge.

See Subaru offer details and browse local listings

See Tesla lease offers at Tesla.com.

Toyota has the best lease deals for hybrids, trucks, and EVs in October. The popular 2024 Tacoma SR5 is now available as a rare zero down lease, a true gem in the truck market.

The 2024 Toyota bZ4X electric crossover is available for just $359/month with $0 due at signing. Despite some reviewer complaints about charging and range, this EV is the perfect lease for commuting and ride-sharing.

See Toyota lease offer details and browse local listings

This month, Volkswagen finally has attractive lease offers:

See Volkswagen for details or browse local listings

Ready to outsmart the dealerships? Download your 100% free car buying cheat sheets today. From negotiating a deal to leasing a car the smart way, it’s all available for instant download. Get your cheat sheets today!

Buying a car is tricky in today’s market, and even leasing can feel like three-dimensional chess these days. Although 2022 isn’t the best time in history to buy or lease a car, some shoppers don’t have a choice. It doesn’t help that the average new car payment is a bank-draining $650 a month in 2022. Fortunately, leasing provides a window of opportunity for those who don’t mind what is essentially a long-term rental. These are the best car lease deals in 2022. All examples assume a 5% down payment at signing.

Not sure where to start? Head over to our CarEdge complete guide to leasing to find out what leasing a car is, and when it’s a good idea.

The plug-in hybrid (PHEV) version of the Mitsubishi Outlander sells for an average MSRP of $40,356 depending on the trim. If leasing is an option, you can get into this versatile SUV for $412 per month with an allowance of 12,000 miles a year. How does a plug-in hybrid work? The Outlander can drive 24 miles on pure electricity (which is much cheaper than gas), and then can drive another 300 miles as a regular hybrid system with the help of a combustion engine. It’s kind of the best of both worlds, especially for a lease.

The Kona EV made our CarEdge list of the five best electric cars you can get for under $50,000. The Hyundai Kona EV has an average MSRP of about $40,000, and you can lease one for just $401 a month. The Kona is a great alternative for those considering the Chevy Bolt. Plus, it comes with Hyundai’s unbeatable 10 year, 100,000 mile battery and electric powertrain warranty. This front-wheel drive subcompact crossover gets 258 miles on the charge, exceptional range for a budget EV. Some owners get over 275 miles on a single charge.

If you can find one that’s not marked up, the 2022 Toyota Tundra 4WD is $51,400 at MSRP. If you’re open to leasing, you can sign up for $525 a month for 36 months and 36,000 miles. That’s $125 less per month than today’s average monthly finance payment. The downside? The Tacoma gets 14 miles per gallon when gas prices are well over $4 per gallon.

Last year, the Toyota Tacoma won Best Buy of the Year award from Kelly Blue Book in the mid-size truck category, and now you can lease a 2022 model for under $400 a month. If you buy, the 2022 Tacoma has an average MSRP of $36,300. If you lease, monthly payments are as low as $361.

With an MSRP of $41,900, it’s a pleasant surprise that you can get into a Civic Type R lease for just $410 a month. Over 300 horsepower propels this budget racer to 60 mph in just 5.3 seconds. The challenge is finding one on a dealer lot.

Pre-facelift, the 2021 Chevy Bolt was the least ‘sexy’ electric vehicle on the market. It may look bland, have slow charging, and be subject to one of the most scrutinized recalls in recent memory, but you can lease one for cheap. The 2021 Chevrolet Bolt sells for $38,567 (average MSRP across trim levels), but you can lease one for $367.63 a month. Just make sure that you have proof from the dealer that your Bolt has already had the recall fix. Learn more about the Chevy Bolt recall and vehicle specs here.

The 2022 model year gets a refreshed, modernized front fascia and improved interior. Sadly, driving range figures for the 2022 year remain the same. At least it doesn’t look like a cheap appliance anymore. Here’s the great news: the 2022 Chevrolet Bolt has a lower MSRP than the 2021 model. GM electric vehicles no longer qualify for the federal EV tax credit, so GM must have felt compelled to keep pricing competitive. Whether you go for a 2021 or 2022 Bolt, ensure that the car has had all of the mandatory fire-related recall fixes completed.

You can lease a 2022 Chevy Bolt for $312 a month for 36 months. If you’re considering buying, remember that the $33,595 price tag will not get any help from the federal tax credit. State and local incentives may apply, depending on where you live. Here’s everything you need to know about the 2022 Chevrolet Bolt.

The Bolt EUV is the slightly larger new sibling to the regular Chevy Bolt EV. The EUV sells for $36,245, but you can lease one for just $341 per month. Range is 247 miles, but charging isn’t that great. Learn more about the Bolt here.

The 2022 Kia Niro EV has an average MSRP of $43,500, but it can be all yours (for 36 months) for just $395 with a lease. There’s generous lease support for the Niro for a few reasons. The Kia Niro is about to receive a major upgrade in 2022, and it’s being overshadowed by the new Kia EV6 electric crossover. The Niro can make it 239 miles on a charge, and charging from 0-80% takes about one hour at a DC fast charger. However, if you plug it in at home, it should work just fine for those who drive less than 50 miles a day.

Why is the 2021 BMW i3 such a phenomenal deal in 2022? It was recently discontinued, but it’s still a great option if you’re looking for an affordable, low-emissions way to get around town. Keep in mind that it’s no Tesla. The i3 gets 200 miles of range, 153 of which are on pure electricity. Not to be confused with the new BMW iX3, the 2021 i3 has an optional range extender (on the BMW i3 REX version). All trims considered, the 2021 BMW i3 has an average MSRP of $48,970 while supplies last.

If you’re looking for an all or mostly-electric bargain lease, you can lease the 2021 BMW i3 for $425/month. That’s well under the budget-friendly 10% threshold for a smart lease.

Have questions or comments about the best car lease deals in 2022? Or maybe you’d simply love to connect with fellow car buyers and auto enthusiasts? Check out the CarEdge Community at caredge.kinsta.cloud!

Buying a new car is rarely a wise financial decision. Truthfully, cars are depreciating assets (unless there’s a chip shortage and car prices appreciate). That means from the moment you drive off the lot with your shiny new wheels, you’re actually losing money.

For some car buyers, leasing is a great way around depreciation. However, leasing isn’t for everyone. For many consumers, it’s worth asking the question “what does it mean to lease a car?”. In this guide to leasing a car, we’ll explain all there is to know about leasing, and how to shop smart in 2025.

The last time a car commercial grabbed your attention with an attractive lease deal, it probably included a whirlwind of rates, payments and terms crammed into thirty seconds. What exactly is a car lease? An auto lease is a long term rental agreement for a vehicle that is subject to specific terms and conditions. The lease terms are agreed upon by the customer and dealership (or automaker in the case of Tesla, Rivian and Lucid), and a third-party leasing company who actually takes ownership of the vehicle (and then leases it to you).

There are four parts to a lease:

1) The capitalized cost (which is the out-the-door price on a lease)

2) The residual value of the vehicle

3) The money factor

4) The state sales tax

These four factors determine the total cost of the lease, and in turn the monthly payment. Let’s talk about the details.

Instead of negotiating an out-the-door price (which is the price of the vehicle plus all taxes and fees), you negotiate the capitalized cost (also referred to as the “cap cost”) of the lease. The cap cost is the amount that the leasing company is paying for the vehicle. This will include:

Some of these charges are negotiable. For example, you don’t need nitrogen-inflated tires or security etching that you didn’t ask for billed on your lease agreement. For every $1,000 in additional cap cost, that will roughly translate to $27 a month in payment on a 36 month lease. Take a long, hard look at the itemized invoice before signing anything!

👉 Here’s a guide to which dealer fees are legit, and which you can negotiate.

Residuals are a percentage of the MSRP as set by the leasing company, and they are not negotiable. The residual value is the vehicle’s projected value at the end of the lease term. When you lease, you pay for the amount of depreciation that will occur over the course of the lease term.

For example, if the residual on a 36 month lease is .75 (or 75%), your lease will include payment that covers the 25% expected loss in value over the course of 36 months.

Residual values are not negotiable and they are set by the leasing company based on allotted annual miles to be driven. Specifically, 7,500, 10,000, 12,000 or 15,000 are the standard mileage amounts that are normally offered.

Dealers cannot modify or adjust the residual percentages other than for additional annual miles allowed to be driven. Check out an example of how residual values fit into leasing here. The residual value is disclosed on the lease as the amount that you can purchase the vehicle for at lease end.

The money factor is set by the lender and can be marked up to the consumer, much like on a car loan. When a buyer finances a car, the dealer works with a number of lenders behind the scenes to get an attractive rate. However, that’s not the rate that the salesperson closing the deal will quote. Dealers markup loans, and pocket the difference. Fascinating and distressing, right? Here are all the ways that dealers make money when selling you a car.

With a car lease, dealers make money by marking up the money factor on a lease. The lender charges the dealer a money factor of say, .00125, and the dealer marks it up 50, 75 or even 100 basis points. The difference between the buy rate (what the lender charges the dealer) and the marked up rate (what you’re quoted) is additional backend profit on the lease for the dealer.

You should always try to negotiate the money factor to the buy rate or as close to the buy rate as you can get!

Taxes in most states are added to the total price of the lease. NY, NJ, MN, OH, and GA charge sales tax upfront on the total amount of the lease payments. VA, MD, and TX charge sales tax on the total selling price of the vehicle (the cap cost). In all other states, sales tax is simply factored into your monthly payment.

Sales tax is not negotiable, but it does vary from state to state.

Simply put, the leasing company owns the vehicle that you are leasing from them. In most cases that will either be that brand’s captive lender or an outside bank. The vehicle will be registered in both the leasing company’s name and your name as the lessee. You will be responsible for registration renewals, maintenance and all insurance.

It’s also possible that the leasing company financed the vehicle that they bought from the dealer. In that case, the financial institution would possess the title until the leasing company pays it off.

At CarEdge, we’re always working on something new to help demystify car buying, car selling, and ownership. If you’re considering a new car lease, estimate your monthly payment in seconds with our latest free tool: our car lease calculator.

No, but If you want to lower your monthly payment, consider making a down payment on your lease. In a car lease, the down payment is called a capitalized cost reduction, or cap cost reduction. These up front payments are optional, but they can help make leasing more affordable by lowering the monthly payments. The payment is lower because the cap cost reduction has lowered the cost of the vehicle to the lender.

Any advertised lease payment typically requires a specified amount of cash down. For example, an advertised lease monthly payment may include $3000 cash down plus the first payment, acquisition fee, tax, title, registration and dealer fees.

Remember as a rule of thumb, for every $1000 in cap cost reduction on a 36 month lease your monthly payment will be reduced about $27.

Shoppers with bad credit may be required to make a security deposit, which is returned once the car is returned at the end of the lease.

I put zero down on my leases and when I say zero, I mean not even a penny. Cash down on a lease just reduces the cost of the vehicle to the lease company and if the vehicle were ever declared a total loss, that money that you had put down is lost forever. A lease down payment is not covered by your auto insurance. They only cover the value of the vehicle, not the value of the cash that you put down.

Whatever money you are thinking about putting down, deposit it into a separate investment account and draw from it monthly when you are making your lease payments. This way your money is still making money each month until you need to draw from it.

Yes, your lease’s monthly payment includes interest, this is the money factor.

You can’t shop around for a better interest rate when it comes to a lease without shopping for a different car altogether. You won’t see an interest rate on your contract when leasing a car, but you can request this information from the dealer or leasing company. The total amount of interest paid on a car lease depends on the length of the lease term and even the type of vehicle. If you lease a model that is likely to depreciate faster, the leasing company is more likely to charge higher interest to ensure that loss in value (the residual) is accounted for.

One way to lower your interest rate (Money Factor) on a lease is by placing Multiple Security Deposits if the lender provides the option. Each MSDS equals one monthly payment and will reduce your MF by a percentage point determined by the lender. There is a limit on how many MSDS you can apply, but the savings can be significant in some cases.

Yes, in most cases customers can pay for a lease up front. Paying for an entire lease at the time of signing is called a one-pay, or single-pay lease. Some lenders will discount interest costs if you pay for the whole lease up front. Make sure to find out if there is any benefit to you before you commit to paying for a car lease up front.

Risk Mitigation

Convenience:

Flexibility:

Financial:

The car isn’t yours.

Few vehicles will lease well.

Fees and costs.

Still debating whether to lease or buy? We’ve got you covered. Check out our CarEdge guide to leasing versus buying in 2022.

Yes, an EV lease is a great way to give electric vehicles a try. Some lease companies pass along the EV tax credit to the consumer by lowering the capitalized cost by the EV credit amount.

Leasing an electric car may be a great option to consider since battery technology improves every year. When your lease is up, you’ll be stepping into a whole new world of next-generation EVs.

See the best EV deals right now in your area

Negotiate what you can

The cap cost and money factor are negotiable. You should always try to negotiate the money factor as close to the buy rate as you can get!

Shop around for deals, be flexible

Deciding what to do at the end of a car lease depends mostly on how you feel about the car. Of course, your financial situation and inclinations also come into play.

These are your options at the end of a car lease:

Which option is a good fit for you? If you love the vehicle and can afford to finance or buy it outright, you can keep a vehicle with a good service history at a set price (from the residual on your lease contract).

If you no longer need a vehicle, leasing allows you to simply return the car and keys at the end of the lease term. Remember, leasing is just like a long-term rental.

Stuck on what to do when your lease ends? Check out our guide, “What to Do At the End of a Car Lease.”

Join the CarEdge Community for expert advice and a place to connect

Join the CarEdge Community to connect with auto industry experts and fellow consumers and car enthusiasts. See the best deals, latest news, and car buying shenanigans to steer clear of. Best of all, a sense of community awaits. We’d love to connect with you!

One of the most common questions we get asked at CarEdge is, “What’s better right now, buying vs. leasing a car?” In 2022, with car prices going crazy, this question has become even more important to answer. In this article we’ll answer a few of the most common questions when it comes to buying vs. leasing a car. You’ll learn things like:

Let’s dive in.

Depending on who you talk to, leasing is either the best thing since sliced bread, or a foolish financial mistake. Many people misunderstand what leasing is; it’s simply a contract between you and a third party company that allows you to rent an asset for a set period of time with pre-negotiated terms and conditions. It’s nothing more and nothing lease less.

When you lease a vehicle there are four important factors that make up your monthly payment:

Let’s break each of these down.

When you lease a vehicle you do not purchase it, instead you are renting it. Instead of negotiating an out-the-door price (which is the price of the vehicle plus all taxes and fees), you negotiate the capitalized cost (also referred to as the “cap cost”) of the lease. The cap cost is the amount that is being financed with a lease. This will include:

👉 Be sure to read this guide on which fees are legit and which you should fight back against.

The cap cost plays a major role in your monthly lease payment. As a rule of thumb, for every $1,000 in additional cap cost, that will roughly translate to $20 a month in payment on a 36 month lease. So if the salesperson won’t budge on their $2,000 paint and fabric protection package, that will end up costing you about $40 a month for three years. Ouch. With a lease you always negotiate the cap cost.

The residual value is the pre-set value that the leasing company says a vehicle will be worth at the end of the lease term. Residual values are represented as percentages of a vehicle’s MSRP, not the negotiated capitalized cost.

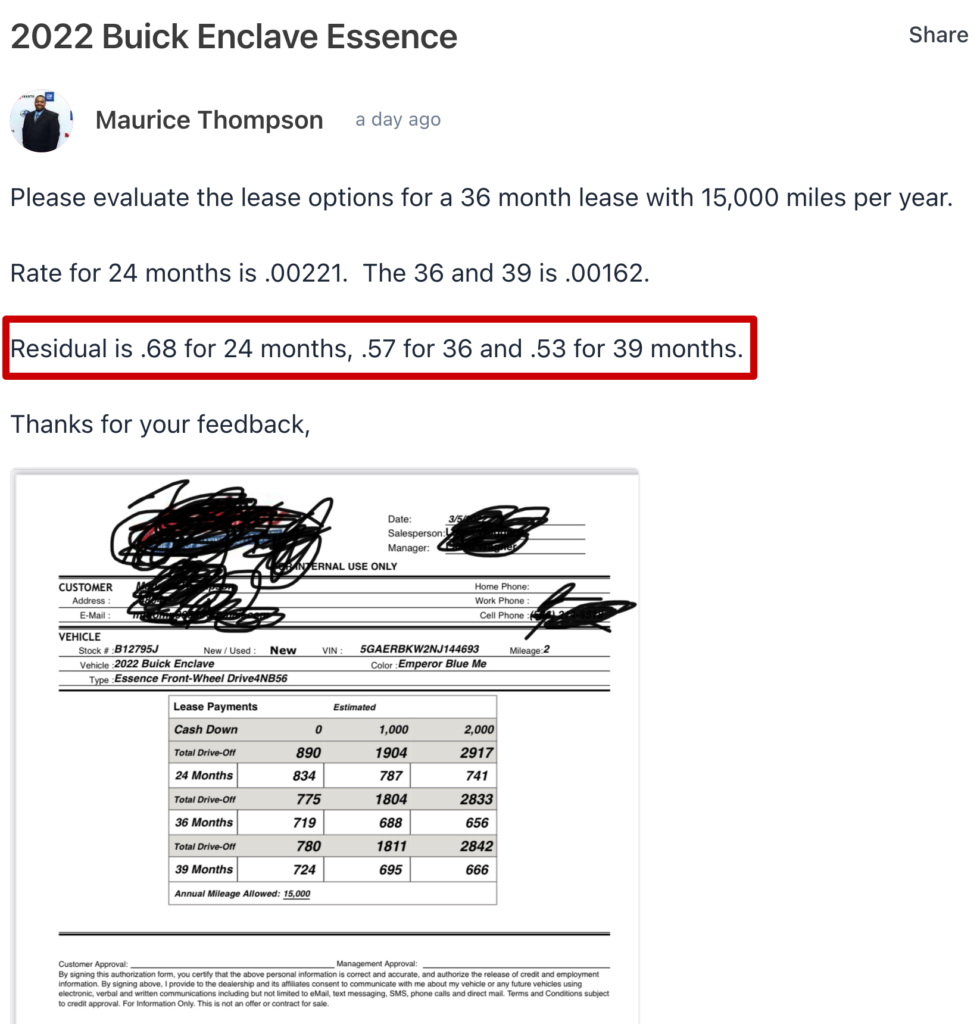

For example, in this car deal you can see that the dealer provided Maurice with three different residual values for three different lease term lengths.

When you lease, you pay for the amount of depreciation that will occur over the course of the lease term. In Maurice’s case if he leased for 24 months the residual value is 68%, which means he will have paid for 32% of the vehicle’s depreciation from MSRP.

👉 Residual values are not negotiable and they are set by the leasing company. Dealer’s cannot modify residual values.

The money factor is the interest rate on a lease. Instead of paying an APR on a loan, you pay a money factor on the lease. Money factors are typically expressed in decimals which can be confusing. Don’t fret. Ask the salesperson for the money factor and then multiply it by 2400, that’s the interest rate you are paying on the lease.

Why do you pay interest on the lease? Because the leasing company is financing the purchase of the vehicle from the dealer. They then turn around and lease the vehicle they just bought to you. To make money they charge the dealer an interest rate (the money factor) to cover their cost of financing the purchase of the vehicle. That then gets passed on to you, the customer.

Money factors can and will be marked up. That means the leasing company may charge the dealer .00125 (3%) for the lease, and the dealer will turn around and tell you the money factor is actually .00175 (4.2%). That’s a sizable difference in rate, and represents a large profit center for dealers on a lease.

👉 You can and should negotiate the money factor on a lease.

Most states charge sales tax on each lease payment, some states do not. NY, NJ, MN, OH, GA for example charge sales tax upfront on the total amount of the lease payments. VA, MD, TX charge sales tax on the total selling price of the vehicle (the cap cost). In all other states, sales tax is simply factored into your monthly payment.

Sales tax is not negotiable.

Okay, so those are the mechanics of leasing, but that doesn’t answer the question, “What’s better right now, buying vs. leasing a car?” We’ll answer that below.

As we discussed above, there are four factors that impact how “good” a lease deal is. So far in 2022 we’ve seen two phenomena that make leasing less attractive than in prior years:

Since you can’t negotiate the residual value, there are some vehicles that are truly “unleasable” right now. Imagine leasing a Hyundai Kona EV for 36 months and paying for 50% of the vehicle’s depreciation. No thank you!

In most cases right now it is cheaper to buy instead of lease. That being said, there are still some advantages to leasing.

Proponents of leasing love to tout the benefits of not owning a car. When you lease there are three primary benefits:

Since a lease is simply a rental, you’ll have no negative equity at the end of the term. Plus, with a lease you are committed for 3 years and then you can switch into something new. And, if you do chose to buy your lease car you know the vehicle history and shouldn’t have any concerns.

These are benefits of leasing no matter how good or bad the lease deal was.

So what cars actually lease well right now in 2022? If you’re seriously weighing buying vs. leasing a car, you should consider these vehicle’s as lease options:

| Term | Year | Make | Model | MSRP | Average Payment (12,000 miles) |

| 36 | 2021 | BMW | i3 | $48,970.00 | $425.80 |

| 36 | 2022 | KIA | NIRO EV | $43,495.00 | $395.91 |

| 36 | 2022 | CHEVROLET | BOLT EV | $33,595.00 | $312.82 |

| 36 | 2022 | CHEVROLET | BOLT EUV | $36,245.00 | $341.01 |

| 36 | 2021 | CHEVROLET | BOLT EV | $38,567.00 | $367.63 |

| 36 | 2021 | HONDA | CIVIC TYPE R | $41,940.00 | $409.78 |

| 36 | 2022 | TOYOTA | TACOMA | $36,323.33 | $361.42 |

| 36 | 2022 | TOYOTA | TUNDRA 4WD | $51,455.00 | $524.43 |

| 36 | 2022 | HYUNDAI | KONA EV | $39,435.00 | $401.39 |

| 36 | 2022 | MITSUBISHI | OUTLANDER PHEV | $40,356.67 | $412.84 |

| 36 | 2021 | POLESTAR | POLESTAR 2 | $61,200.00 | $623.95 |

| 36 | 2022 | KIA | NIRO PLUG-IN HYBRID | $34,331.67 | $350.88 |

| 36 | 2022 | JEEP | WRANGLER UNLIMITED | $47,838.86 | $502.42 |

| 36 | 2021 | TOYOTA | TACOMA | $35,835.61 | $378.09 |

| 36 | 2022 | TOYOTA | TUNDRA 2WD | $48,478.57 | $527.23 |

Do you still have questions on buying vs. leasing a car? Get help from CarEdge’s team of car buying coaches. Click here to join CarEdge and get connected with a car lease expert who can help you navigate your deal. Here are some additional resources on car leases as well: