CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

It’s a new year, yet the car market is presenting drivers with the same classic dilemma: should you buy new or used in 2026? This year, several factors are reshaping the debate, including depreciation trends, interest rates, and price shifts in both new and used car markets. Making the right choice requires a close look at your financial situation and ownership goals. We spoke to CarEdge Co-Founder and auto industry veteran Ray Shefska about how car buyers can make smart, financially-sound decisions in 2026’s market.

Here are some key considerations to help you determine whether buying new, buying used, or leasing makes the most sense for you.

New cars are known for their steep depreciation, and in 2026, depreciation rates have returned to pre-pandemic levels. That means a new car can lose 20-30% of its value within the first two to three years of ownership. If you’re buying an EV or PHEV, depreciation can be even higher.

However, buying new has its advantages, too. Manufacturer incentives are sweetening the deal for buyers with attractive lease offers, low APR financing, and cash incentives that simply aren’t available for used car buyers.

Here’s a look at the pros and cons of buying a new car in 2026.

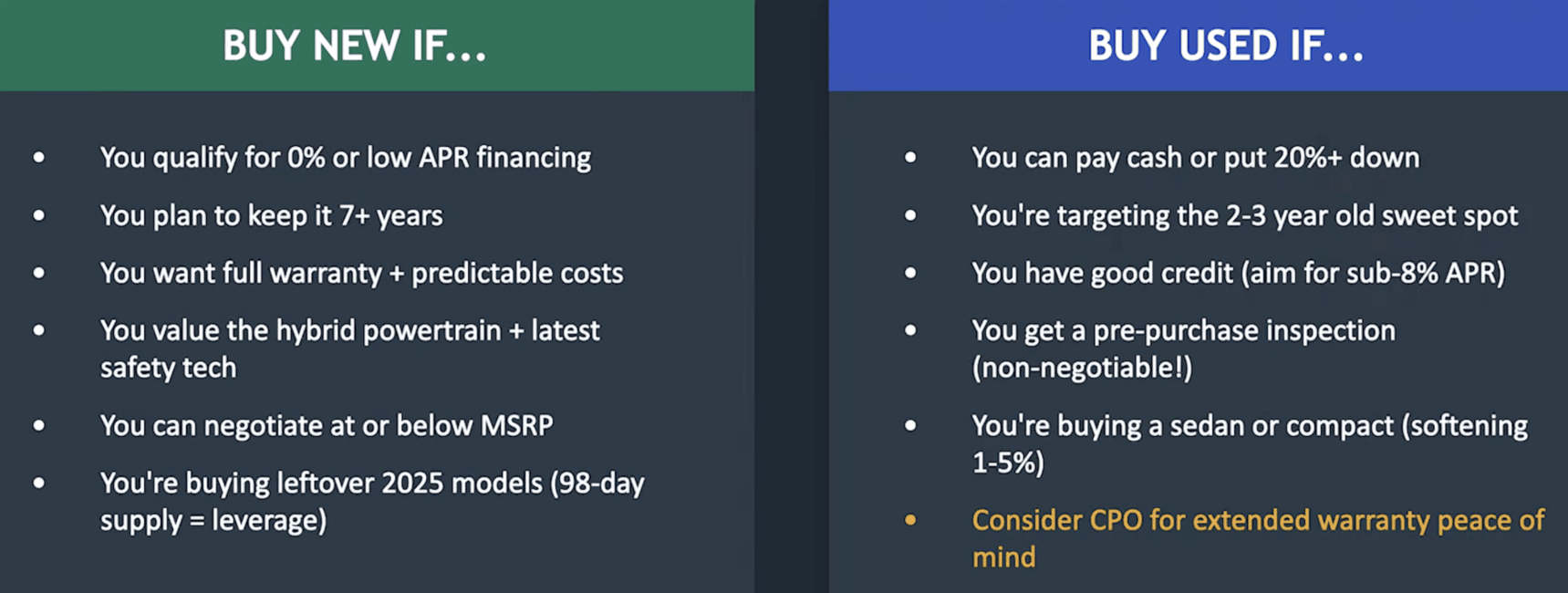

Why Buy New in 2026?

Drawbacks of Buying New:

If you’re considering a new car but worry about depreciation, leasing may be a better option for you in 2026. It allows you to enjoy the benefits of driving new without the financial impact of resale value losses. Otherwise, buying used is the better option for many drivers. More on that below.

Interest rates are a defining factor in the new versus used car debate. While borrowing costs remain high in 2026, automakers are making it easier to finance new cars by offering low APR financing. Used car loans, on the other hand, often come with higher interest rates from banks and credit unions. It’s important to keep in mind that low-APR financing is reserved for what the industry calls ‘well-qualified buyers‘.

Why New Cars Win on Interest Rates:

In 2026, the average used car loan rate is about 12% APR, while new car loan rates average 7% APR. Used car loans typically come with interest rates about 5% higher than those for new vehicles. Over a five-year loan term, this can significantly increase the total cost of financing a used car. If monthly payments are a concern, financing a new car with low APR may actually make more financial sense.

👉 However, NEVER negotiate monthly payments – always negotiate the Out-the-Door Price to avoid add-ons and ripoffs.

See Every 0% APR Offer This Month

The days of guessing what to pay for a new car are over. In 2026, buyers have access to tools that provide insight into dealer pricing, invoice costs, and manufacturer incentives.

How to Save Big When Buying New:

These tools make it easier than ever to negotiate confidently and secure the best deal on a new car in 2025.

After years of record-breaking price hikes, used car prices are finally starting to decline. However, they remain elevated compared to historical norms, and deals can still be hard to come by without the right negotiating tools.

Why Consider Buying Used in 2026?

Challenges of Buying Used:

Despite these challenges, buying used is still the go-to option for many drivers who prioritize affordability and don’t mind sacrificing the latest features.

For many car buyers, a 3-5 year-old used car strikes the perfect balance between affordability, reliability, and long-term value. This “sweet spot” in the used car market offers significant benefits that make it a smart choice for budget-conscious drivers who don’t want to sacrifice quality or performance.

Here’s why a 3-5 year-old used car could be the ideal option for you:

New cars typically lose 30-40% of their value within the first three years, making depreciation one of the biggest hidden costs of buying new.

Compared to buying new, 3-5 year-old used cars are significantly more affordable. The average used car price in 2026 is $26,000, nearly 50% lower than today’s average new car price of $50,000.

A car that’s 3-5 years old still comes equipped with many of the features found in today’s new models, such as advanced safety systems and driver assistance.

A 3-5 year-old car is typically well within its prime and often covered by a portion of the manufacturer’s original powertrain warranty. If coverage is about to run out, get an Extended Warranty quote for peace of mind.

While interest rates for used car loans are higher than those for new cars, lenders generally offer better rates for late-model used cars compared to older vehicles. This makes financing a 3-5 year-old car more manageable and less risky.

By choosing a 3-5 year-old used car, you get the best of both worlds: modern features at a lower price, and the ability to avoid the financial pitfalls of buying new. It’s a smart compromise for 2026 car buyers looking for value and reliability. To ensure you’re making a wise investment, always research market trends, request vehicle history reports, and schedule a pre-purchase inspection before buying any used car.

In 2026, the decision between buying new or used depends largely on your financial situation and long-term ownership goals.

When to Buy New:

When to Buy Used:

No matter which option you choose, doing your homework is key. Research market trends, compare deals, and always negotiate to get the best price possible.

Navigating today’s car market doesn’t have to be stressful. With tools like the Research Hub, Free Dealer Invoice Pricing, and CarEdge Pro, you’ll have all the information you need to negotiate like a pro. Whether you’re shopping for new or used cars, we’ve got the resources to help you save thousands.

Ready for an expert to negotiate on your behalf? CarEdge Concierge is your perfect fit!

Start your car buying journey with confidence at CarEdge, where transparency meets savings.

The car buying game has fundamentally changed. In 2026, the smartest shoppers walk into dealerships with the same information dealers once kept behind closed doors—and it’s completely free. This shift in power dynamics is forcing a new kind of negotiation, one where informed buyers set the terms instead of reacting to sales tactics.

Let’s break down exactly how educated car shoppers are winning deals in 2026, using real negotiation strategies that work.

The first question most dealerships ask is: “What’s your monthly payment goal?” It sounds helpful, but it’s actually a negotiation tactic designed to shift your focus away from the vehicle’s actual price.

When you anchor a negotiation around monthly payments, dealers gain enormous flexibility to adjust loan terms, interest rates, and hidden fees while keeping your payment within your stated range. You might hit your $500/month target, but you could be paying thousands more over the life of the loan than necessary.

Smart buyers in 2026 shut this down immediately. Instead of discussing payments, they focus on one number:

This approach forces transparency and keeps the negotiation focused on value rather than affordability theater.

Here’s what changed everything: pricing intelligence that was once dealer-exclusive is now available to anyone with an internet connection. Tools like CarEdge provide:

In our example negotiation, the buyer came prepared with specific numbers: MSRP of $63,435, invoice of $59,311, and the knowledge that the F-150 had been on the lot for 84 days. This intel completely reframes the conversation.

When a vehicle has been sitting for nearly three months, the dealer is carrying floor plan costs and wants to move it. An informed buyer can leverage this without being aggressive—simply acknowledging the reality shifts negotiating power.

The key is having this data before you contact the dealer. Once you’re in the negotiation, having specific numbers on hand signals that you’re serious and informed.

Modern car buying starts with research, not test drives. Here’s the smart sequence:

Step 1: Do Your Homework

Step 2: Make Initial Contact

Step 3: Frame the Negotiation

Step 4: Negotiate with Data

Salespeople are trained to steer you toward payment discussions. Here’s how to redirect:

Dealer: “What monthly payment are you looking for?”

You: “I’m not focused on the monthly payment right now. I want to make sure we agree on a fair selling price first. Once we settle on the out-the-door number, we can structure financing however makes sense.”

This response is firm but not adversarial. It signals experience without creating tension.

Every day a vehicle sits on a dealer lot costs money. Most dealerships pay floor plan interest to finance their inventory—typically $20-50 per day per vehicle depending on its value.

An F-150 that’s been sitting for 84 days has cost the dealer roughly $1,680-$4,200 in carrying costs alone. That’s before accounting for lost opportunity (that lot space could hold faster-moving inventory) and depreciation risk.

This context doesn’t mean you strong-arm the dealer, but it does mean they’re motivated to move aged inventory. A reasonable offer on a vehicle with high days-on-lot is likely to get serious consideration, especially if you’re a qualified buyer ready to close quickly.

When negotiating a car deal, it’s helpful to know exactly how much profit for the dealership is built into each sale. No matter what the salesperson tells you, you do have plenty of room to negotiate savings! Here’s a quick breakdown of the pricing hierarchy:

Your goal is to negotiate a selling price between invoice and MSRP, closer to invoice especially on aged inventory, then verify the out-the-door price includes only legitimate fees.

In the example negotiation, the buyer:

This approach immediately shifts the dynamic. The salesperson recognizes they’re dealing with someone who’s done research, which tends to accelerate the negotiation process and reduce back-and-forth games.

Buying a car in 2026 isn’t about being the toughest negotiator or playing games—it’s about being informed. When you walk in with invoice pricing, inventory age, and market data, you’re negotiating from a position of knowledge rather than reacting to sales tactics.

The dealers who adapt to this new reality focus on service, transparency, and efficiency. The ones who don’t quickly find themselves losing deals to competitors who respect informed buyers.

Your goal isn’t to squeeze every last dollar out of a dealer. It’s to pay a fair price based on actual market conditions and vehicle cost structure. With the right information and approach, that’s exactly what you’ll accomplish.

The power shift in car buying is real, and it’s permanent. Smart shoppers in 2026 are leveraging it to save thousands while making the process faster and less stressful for everyone involved.

The 2026 Hyundai Venue has officially claimed the title of the cheapest new car you can buy in America, with a base MSRP of $20,550. With the Nissan Versa and Mitsubishi Mirage both gone from the U.S. market, the Venue stands alone at the bottom of the price ladder.

That’s a remarkable feat in a market where the average new car now costs close to $50,000. But here’s the thing: cheap isn’t the same as good value. And when you dig into the numbers, the Venue’s low sticker price starts to look less like a deal and more like a trap.

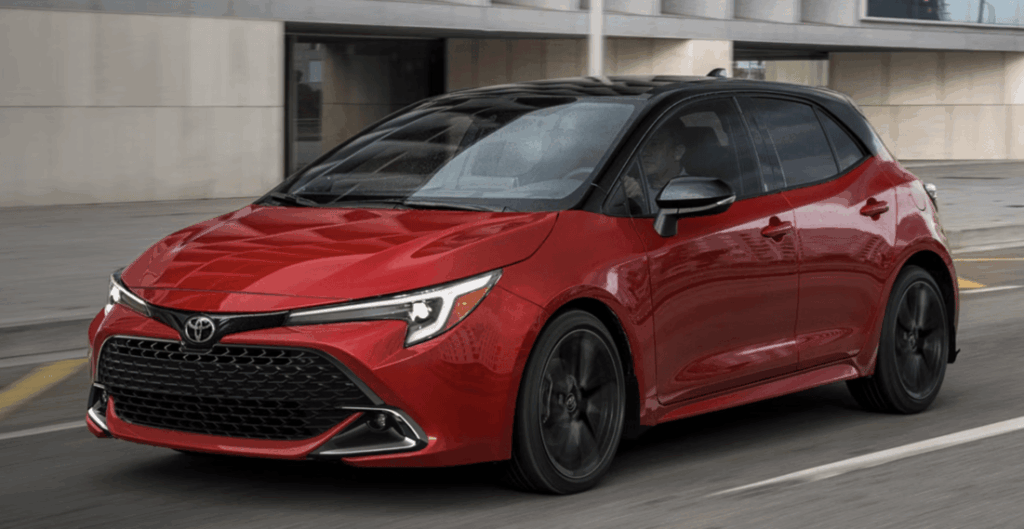

Spend roughly $4,000 more, and you can drive home in a 2026 Toyota Corolla Hatchback — a car that beats the Venue in nearly every category. Here’s why that extra investment is worth it.

Yes, the 2026 Hyundai Venue starts at $20,550. But that number doesn’t tell the whole story.

Once you add the mandatory destination fee, the base price is $22,150. Want heated front seats and wireless phone charging in your Venue? The SEL trim will run you $24,200.

The Toyota Corolla sedan starts at $24,120 with destination fees included. For an apples-to-apples comparison, we’ll be comparing the 2026 Toyota Corolla Hatchback to the Venue. The popular Corolla Hatchback SE starts at $26,560.

So the real-world price difference between base models is about $4,410. Over a five-year loan, that’s roughly $75 to $90 more per month depending on your interest rate. For most buyers, that’s a manageable gap.

And as we’ll soon show, you get a lot in return.

Here’s the part that tends to surprise people: the cheaper car actually costs more to own in the long run.

CarEdge’s 5-year total cost of ownership tells the story clearly:

That’s nearly $1,900 in savings with the Corolla over five years, despite its higher sticker price. The primary drivers? Depreciation and maintenance.

The Hyundai Venue is projected to lose 36% of its value over five years. The Corolla Hatchback? Just 23%. That 13-point difference means the Corolla holds significantly more resale value — money that stays in your pocket when it’s time to sell or trade in.

All things considered, CarEdge rates the two cars accordingly: the Corolla Hatchback earns an A+ value rating, while the Hyundai Venue gets a B. Neither is bad, but the Corolla Hatchback is the clear winner.

Reliability is one of the biggest factors in total cost of ownership, and it’s one of the clearest wins for the Corolla.

Consumer Reports rates the 2026 Corolla Hatchback 73 out of 100 for reliability. The Venue scores just 55 out of 100. That 18-point gap is significant — it reflects a meaningful difference in how often you’re likely to deal with unexpected repairs and maintenance headaches over time.

The overall Consumer Reports scores tell a similar story:

On safety, the gap is even sharper. NHTSA awarded the 2026 Corolla Hatchback a perfect 5 out of 5 stars. The Venue earned 4 out of 5 stars. For buyers who prioritize keeping themselves and their passengers safe, that difference matters.

The Venue is powered by a 121-hp four-cylinder engine. It’s adequate for city driving, but Car and Driver testing showed it takes 8.5 seconds to reach 60 mph, and reviewers consistently note a near-complete lack of passing power on the highway. The CVT doesn’t help matters.

The Corolla Hatchback packs a 2.0-liter four-cylinder making 169 horsepower — a full 48 more than the Venue. It reaches 60 mph in 8.3 seconds, edging out the Venue despite moving a larger, better-equipped car.

Fuel economy is another win for the Corolla. The EPA rates it at 32 mpg city and 41 mpg highway, compared to the Venue’s 29 mpg city and 33 mpg highway. The Corolla’s 8 mpg highway advantage can add up to real savings at the pump, especially for drivers who commute longer distances

This is one area where the Hyundai Venue has a genuine edge. Hyundai’s warranty coverage is among the best in the industry:

Hyundai Venue:

Toyota Corolla Hatchback:

Hyundai’s 10-year/100,000-mile powertrain warranty is legitimately impressive and provides real peace of mind. If warranty coverage is your top priority, the Venue deserves credit here.

That said, it’s worth asking why Hyundai offers such an extensive warranty. In part, it’s because the Venue’s reliability scores aren’t as strong as Toyota’s. The Corolla Hatchback scores 18 points higher on Consumer Reports’ reliability scale. Toyota rarely shows up in recall notices, but we can’t say the same for Hyundai.

The 2026 Hyundai Venue isn’t a bad option for drivers with tight budgets who need new-car warranty coverage above all else. We’re not here to dismiss it.

But if you can stretch your budget by roughly $4,400 at the base level, the 2026 Toyota Corolla Hatchback is the smarter buy in almost every dimension: lower 5-year cost of ownership, better resale value, superior reliability, a perfect NHTSA safety rating, more horsepower, and much better fuel economy.

The cheapest price tag at the dealership isn’t always the cheapest car to own. Sometimes, spending a little more upfront is exactly how you save money in the long run.

![10 Cars with the Lowest Cost of Ownership [2026 Data]](https://caredge.com/wp-content/uploads/2026/02/2026-Toyota-Corolla-Hatchback-1080x569.png)

New car prices are still high in 2026. Insurance isn’t getting cheaper. And repair costs aren’t trending down either.

So if you’re buying this year, you can’t just look at the sticker price, you have to look at the total cost of ownership.

Using CarEdge 5-year cost of ownership projections — which factor in depreciation, insurance, maintenance, fuel, and financing — we’ve gathered the 10 cars with the lowest total cost of ownership in 2026.

Predicted 5-Year Total Cost of Ownership: $30,541

Starting MSRP with Destination Fees: $26,560

Predicted 5-Year Depreciation: 20% of value lost

The Toyota Corolla Hatchback has the lowest total cost of ownership in 2026. The Corolla Hatchback checks every box for the ideal commuter car. It’s fuel efficient, extremely reliable, and affordable. With just 20% depreciation projected over five years, it holds value exceptionally well, and that’s what drives it to the very top of this ranking.

See Toyota Corolla Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $32,435

Starting MSRP with Destination Fees: $22,150

Predicted 5-Year Depreciation: 26% of value lost

With the Mitsubishi Mirage discontinued, the Venue now wears the crown as the cheapest new car in America in 2026.

Low MSRP plus manageable depreciation equals one of the lowest ownership costs on the market. It’s not fast, but it’s affordable — and for many buyers, that’s what matters.

See Hyundai Venue Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $32,541

Starting MSRP with Destination Fees: $25,890

Predicted 5-Year Depreciation: 24% of value lost

Few vehicles have the long-term reputation of the Civic. Reliability drives resale value, and resale value drives total ownership cost.

It costs slightly more upfront than some competitors, but its durability keeps long-term costs impressively low.

See Honda Civic Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $32,759

Starting MSRP with Destination Fees: $27,790

Predicted 5-Year Depreciation: 26% of value lost

Now offered only as a hatchback, the Impreza has quietly evolved into a refined compact with standard all-wheel drive.

Prices have climbed significantly — up roughly $8,000 since 2021 — but strong resale values help keep ownership costs competitive.

See Subaru Impreza Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $32,875

Starting MSRP with Destination Fees: $23,845

Predicted 5-Year Depreciation: 26% of value lost

The 2026 Sentra is all-new, with updated styling inside and out. The Sentra has been in the U.S. market for 44 years, and as other sedans get the axe, this one is here to see another year.

The Sentra undercuts the Civic on price but trails slightly in power and reliability. Still, it lands squarely among the most affordable cars to own this year.

See Nissan Sentra Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $33,333

Starting MSRP with Destination Fees: $23,535

Predicted 5-Year Depreciation: 31% of value lost

The K4 replaced the Forte in 2025 as Kia’s entry-level model.

Depreciation is a bit higher than others on this list, but its low starting price keeps overall ownership costs firmly in budget territory.

See Kia K4 Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $33,735

Starting MSRP with Destination Fees: $18,585

Predicted 5-Year Depreciation: 24% of value lost

Production ended in December 2025, but roughly 11,000 units remain on dealer lots in early 2026.

If you can find one, it’s one of the absolute cheapest ways to get into a new car this year.

See Nissan Versa Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $34,297

Starting MSRP with Destination Fees: $30,295

Predicted 5-Year Depreciation: 37% of value lost

The Camry is one of the more expensive cars on this list, but it’s also one of the most reliable. The extremely low maintenance costs are why the Camry remains in the top 10.

See Toyota Camry Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $34,616

Starting MSRP with Destination Fees: $24,120

Predicted 5-Year Depreciation: 26% of value lost

Not interested in the hatchback? The Corolla sedan remains one of the safest financial bets in the compact segment.

It’s slightly cheaper upfront than the hatchback, and still exceptionally affordable to own.

See Toyota Corolla Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $34,718

Starting MSRP with Destination Fees: $27,950

Predicted 5-Year Depreciation: 27% of value lost

To be frank, the HR-V is the CR-V’s less popular sibling. Looks and sales volume aside, it’s still a great, reliable crossover. And it’s one of the few reliable crossovers that can be had for under $30,000.

See Honda HR-V Cost of Ownership Data

If you’re looking for the most affordable cars to own in 2026, the pattern is clear:

It’s easy to focus on MSRP when shopping for a new car, but the sticker price only tells part of the story. Insurance, maintenance, and depreciation can quietly add thousands to your total cost over time, even for a new car. Every model on this list proves that affordable ownership is still possible in 2025, but only if you make a smart purchase.

Whether you’re shopping new or used, don’t just ask what a car costs today—ask what it’ll cost you tomorrow. For deeper insights, explore cost of ownership and depreciation data for every model at CarEdge Research.

If you’ve been watching the car market, you know something’s broken. But here’s what most people don’t realize: car repossessions in 2026 are tracking at levels we haven’t seen since the 2008 financial crisis. For owners at risk of losing their vehicle, this is a statistic that hits close to home. And if you’re a used car buyer, this could be a little-known opportunity to snag a deal.

CarEdge co-founder Ray Shefska here has spent decades in dealerships, and he’s seeing something alarming on the lots right now. Let me break down exactly what’s happening, what dealers aren’t telling you about these repo cars flooding the market, and how you can navigate this situation whether you’re buying or currently at risk of losing your vehicle.

Let’s start with the numbers. According to recent data from Cox Automotive, auto loan delinquencies (60+ days past due) have climbed to 4.8% in early 2026—the highest rate since 2010. Here’s why:

1. Pandemic-Era Loans Coming Due

Remember 2021-2022 when everyone bought cars at inflated prices with six or seven month loans? Those buyers are now 3-4 years into loans, and many are deeply underwater. Their $45,000 electric vehicle or luxury crossover is worth $25,000, but they still owe $38,000. Many are looking for a way out of negative equity, but few are finding an easy solution.

2. Payment Shock Is Real

The average new car payment in 2026 is $748/month. Used cars? $563/month. That’s not a car payment—that’s a second mortgage. When you combine that with inflation in groceries, rent, and insurance, something has to give.

3. Subprime Lending Came Roaring Back

From 2021-2024, lenders loosened standards dramatically. People with 580 credit scores were getting approved at 18-22% APR. Now those loans are imploding. Subprime auto loan delinquencies are above 6.5%. As banks and automaker captive financing companies lose money on more loans, it become tougher for all borrowers to secure a good rate.

If it gets any worse, the entire auto lending system will be under threat.

4. The Trade-In Trap

Industry veteran Ray Shefska sees it all the time: “People come in already $8,000 upside down on their current loan, roll that negative equity into a new $50,000 purchase, and suddenly they’re financing $58,000 at 9% interest. When life happens—job loss, medical bills, divorce—that payment becomes impossible.“

Repossession isn’t just losing your car. For many, having a car repossessed is a financial chain reaction that can follow you for years. Understanding the sequence of events and the full scope of the damage is the first step to avoiding it, or dealing with it if you’re already there.

The Repossession Timeline:

The Financial Damage:

If you know repossession is inevitable, you don’t have to wait for the tow truck to show up in the middle of the night. Voluntary repossession—where you call your lender and arrange to drop the car off yourself—puts you in control of the timing and lets you clear out your belongings on your own terms.

The financial damage is nearly the same either way. Voluntary repo still hits your credit report just like an involuntary one, and you’re still on the hook for any deficiency balance if the car sells at auction for less than you owe. The one practical upside is that you may avoid the repo agent fee ($400–800), which slightly reduces what you’ll owe in the end.

Think of it less as a financial solution and more as a way to manage a bad situation with a little more dignity. If you’ve exhausted your other options—negotiating with the lender, refinancing, or selling the car yourself—voluntary surrender at least lets you exit on your own terms rather than waking up to an empty driveway.

Car dealers have good reasons for not advertising repossessed cars. Many shoppers would be turned off by this revelation. Few drivers want their “new” car to remind them of the financial hardships others have endured. So, how can you find out if a car was repossessed? Let’s get into it.

Ray’s seen thousands of repos come through dealerships, and here’s how they get there:

Route 1: Wholesale Auction (Most Common)

“When a bank repos a car, they want it gone fast,” Ray explains. “It goes to Manheim, ADESA, or another wholesale auction. Dealers bid on these, usually getting them for $3,000-7,000 below clean retail because repos often have issues like missed maintenance, interior damage, sometimes even mechanical sabotage from angry former owners.”

Route 2: Direct Sales to Franchise Dealers

Captive finance arms (Ford Credit, GM Financial, Toyota Financial) often send repos directly to their franchise dealers. “A Ford repo might come straight to a Ford dealership’s used lot,” Ray notes. “These are usually in better shape because they were newer when repossessed.”

Route 3: Buy-Here-Pay-Here Lots

Higher-mileage repos with issues often end up at BHPH dealers who do in-house financing. These lots target the same subprime buyers who lost their cars to repo, creating a dangerous cycle.

Here’s what dealers won’t voluntarily disclose:

1. They’re Not Required to Tell You It’s a Repo

Unlike flood damage or salvage titles, repossession history doesn’t show up on a Carfax or vehicle title. A dealer can legally sell you a former repo without disclosure.

2. Repo Cars Often Have Hidden Issues

“I’ve seen repos come in with 15,000 miles past due for an oil change, bald tires, and check engine lights,” Ray says. “The previous owner knew it was getting taken back—they stopped maintaining it months ago.”

3. The “Auction Fresh” Red Flag

On a Carfax, look for “sold at auction” within the last 30-60 days, especially if there’s only one previous owner. That’s often a repo that got wholesaled.

4. Dealers Mark Them Up Anyway

Just because a dealer bought it cheap at auction doesn’t mean you get a deal. They’ll still mark it up to market rate or higher. Your job is to negotiate knowing they have less money in it.

Research red flags

Check the Carfax or AutoCheck report. A Repossession may show:

At the Dealership, keep an eye out for these signs:

Questions to ask the salesperson

1. “Where did you acquire this vehicle?” (If it came from an auction, that’s normal. Inquire further by asking if it was a bank return. In dealership lingo, repos are often called “bank returns”)

2. “Can you show me the last service records?” (Gaps of 12+ months are a warning sign)

3. “Has this vehicle had a pre-purchase inspection by your service department?” (Many repos don’t get proper reconditioning)

4. “What’s your best out-the-door price?” (Repos have more negotiating room since dealers bought them cheap)

The opportunity is real, but be careful. Here’s Ray’s advice: “The repo surge means there’s legitimate opportunity for educated buyers. Banks are motivated, dealers have inventory they want to move, and you can get a good car for the right price—but you MUST do your homework.”

Some banks sell repos directly to consumers through their websites:

Pros: Skip the dealer markup, often better condition disclosure

Cons: Sold as-is, limited negotiation, you handle all paperwork

Manheim and ADESA occasionally have public auction days. You can inspect vehicles beforehand and bid directly.

What to Bring:

If you play it smart, it’s possible to buy a repossessed car at auction for 20-25% below retail pricing.

If you’ve identified a likely repo at a dealership:

1. Get a Pre-Purchase Inspection: Non-negotiable. Pay $150-200 for an independent mechanic to inspect it thoroughly

2. Use Auction Data: Check recent auction results on sites like Manheim Market Report to see wholesale values

3. Negotiate Based on Condition: “I see this needs new tires ($800), brakes ($400), and hasn’t been serviced in a year. Here’s my offer based on these deferred costs.”

4. Get an Extended Warranty: If you’re buying a higher-mileage repo, negotiate for a dealer warranty or purchase a reputable third-party plan

If you’re not comfortable evaluating a repo, just wait for off-lease inventory. These are vehicles coming back from 2-3 year leases, typically well-maintained, and dealers are motivated to move them too. You get a known history without the repo risk. For many, it’s worth the patience and higher price tag for a known vehicle history.

The good news is that you have more options than you think. If you’re behind on payments and worried about repo, here’s Ray’s advice from someone who’s worked with hundreds of struggling buyers:

Don’t hide. Most lenders would rather work with you than repo your car. Call and ask about:

“The absolute worst thing you can do is ghost your lender,” Ray emphasizes. “Once they assign a repo agent, your options disappear.”

If you’re underwater but not too deep:

1. Get instant offers from Carvana, CarMax, and Vroom

2. Compare to private party value on Facebook Marketplace or Craigslist

3. If you can cover the difference between the offer and your payoff, sell immediately

4. If possible, use the proceeds to buy a $5,000-8,000 reliable used car that you own outright. If that’s not an option, start saving up.

If you can’t make payments and can’t sell, voluntary surrender is better than repossession:

“Voluntary surrender is better than hiding the car and playing games with the repo man,” Ray says. “It shows some responsibility and might make the lender more willing to negotiate on the deficiency.”

If you’re 30-60 days behind but your credit hasn’t tanked yet:

“I’ve helped people who were 60 days behind get into a different vehicle with a $200/month lower payment,” Ray notes. “It’s not ideal—you’re still buried—but it keeps you mobile and out of repo status.”

Used Car Prices Will Stabilize or Decline. Repo inventory flooding wholesale auctions puts downward pressure on used car prices. Good news if you’re buying, bad news if you’re trying to trade in.

Lending Will Tighten (Again). Expect stricter credit requirements, higher down payment demands, and shorter loan terms as lenders react to losses. The 84-month loan at 6.99% for 620 credit scores? That’s disappearing.

Subprime Buyers Will Struggle. If you have damaged credit and need a car, expect to pay 15-22% APR or resort to buy-here-pay-here dealers with even worse terms. Breaking this cycle requires saving for a cheap, reliable car you can own outright.

Opportunity for Cash Buyers. 2026-2027 could be the best time in years to buy a used car with cash or strong credit. Dealers need to move inventory, repos are plentiful, and negotiating leverage is shifting back to buyers.

If You’re Buying:

If You’re Struggling With Payments:

The bigger lesson according to Ray

“The repo crisis of 2026 is a direct result of over-leveraged buyers financing depreciating assets at high interest rates. If you take away one thing, let it be this: just because a bank will approve you for $60,000 doesn’t mean you should borrow it. Buy less car than you can afford, keep the loan term short, and always have an emergency fund. That’s how you avoid becoming a repo statistic, and having a car you no longer drive follow you for years.”

What’s your experience with the current auto loan market? Have you seen repos on dealer lots, or are you navigating a difficult payment situation yourself? Join the conversation at the CarEdge Community.