CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

“We’ve got another buyer coming in an hour.”

“There’s someone else who’s very interested in this car.”

“I need to know if you’re serious because we have other offers.”

Sound familiar? If you’ve spent any time negotiating at a car dealership, you’ve probably heard some version of this classic pressure tactic. CarEdge Co-Founder Ray Shefska, with decades of dealership experience, calls this exactly what it is: manufactured urgency designed to make you panic and pay more.

Here’s how to handle it, and why this tactic rarely means what they want you to think it means.

This pressure play works on basic human psychology: fear of missing out. Nobody wants to lose something they’ve already invested time in, and salespeople know that once you’ve test-driven a car and started imagining yourself in it, you’re emotionally attached.

The dealership’s goal is simple: create artificial urgency to:

In Ray’s experience, this tactic comes out most often when negotiations stall or when you say you need to think about it.

Here’s what Ray wants you to know: In most cases, there is no other buyer.

“When there genuinely is another interested party, the dealership doesn’t need to tell you about it. They’ll just sell it to that person. The fact that they’re spending energy trying to convince you to buy suggests they don’t have a better offer waiting.”

Even when there is another buyer, consider these realities:

Dealerships talk to dozens of people every day. Maybe someone did express interest in that car—but “interest” doesn’t mean they’re qualified, approved for financing, or actually ready to purchase. Most of these “interested buyers” never materialize into actual sales.

A truly in-demand vehicle—especially in 2026’s market where inventory has normalized—doesn’t sit on the lot long enough for this conversation to happen. Hot cars sell within days, often at or above asking price, without negotiation drama.

Unless you’re buying something truly rare (a limited-edition model, a specific classic car, etc.), there are similar vehicles available at other dealerships. The salesperson wants you to forget this fact.

It’s always best to shop the cars that are most negotiable, as determined by local market data. Here’s how we find them.

When a salesperson says another buyer is coming, Ray recommends this simple response:

“I understand. If they buy it before we reach an agreement, I’ll find another one.”

That’s it. Don’t argue. Don’t panic. Don’t try to compete with this phantom buyer. Just acknowledge what they said and demonstrate that you’re not going to be pressured.

Here’s why this response is so effective:

It Calls Their Bluff Without Confrontation

You’re not accusing them of lying, but you’re making it clear their pressure tactic isn’t working. You’re showing confidence in your position and your ability to walk away.

It Reminds Them You Have Other Options

Salespeople sometimes forget that they need the sale too. Your response subtly reminds them that if they lose you over this pressure play, they’ve lost a real buyer chasing a maybe-buyer.

It Keeps You in Control

By remaining calm and non-reactive, you maintain negotiating power. Panic is expensive. Composure saves you money.

It Often Leads to Backtracking

In Ray’s experience, this response frequently results in the salesperson suddenly having more flexibility: “Well, let me talk to my manager and see what we can do for you…”

Funny how that “urgent” other buyer becomes less urgent when you’re willing to walk.

Know the market value of the car you want using resources like:

When you know what the car is actually worth, pressure tactics become background noise.

Walk in with your own financing already secured. This eliminates one pressure point (“We need to see if you qualify”) and often gets you a better rate than dealer financing. Review this guide to financing like a pro before you shop.

Contact 3-5 dealers for the same make and model. Get quotes in writing (email is perfect). This gives you real leverage and makes the “another buyer” tactic meaningless—you literally have other options ready.

Use our Dealership Ratings Based on Real Prices to find the most transparent car dealers near you.

The single most powerful negotiating tool is genuine willingness to leave. If you’re not prepared to walk out, you’ve already lost leverage. Remember: there are other cars, other dealers, other days.

Let’s say you use Ray’s response, walk away, and the dealership actually sells the car to someone else. Now what?

Here’s the truth: You probably dodged a bullet.

If they were willing to let you walk over a reasonable negotiation, one of two things happened:

1. They really did have a buyer willing to pay more—which means you would have overpaid to compete

2. They made a strategic mistake—they gambled on pressure and lost a real sale

Either way, you did the right thing. In today’s market, you will find another vehicle. You might even find a better deal at a dealership that doesn’t play these games.

Understanding the current market helps you evaluate these tactics:

Bottom line: The “another buyer” tactic is less credible in 2026 than it was during the shortage years. Dealers have cars to sell, and competition among dealerships is healthy.

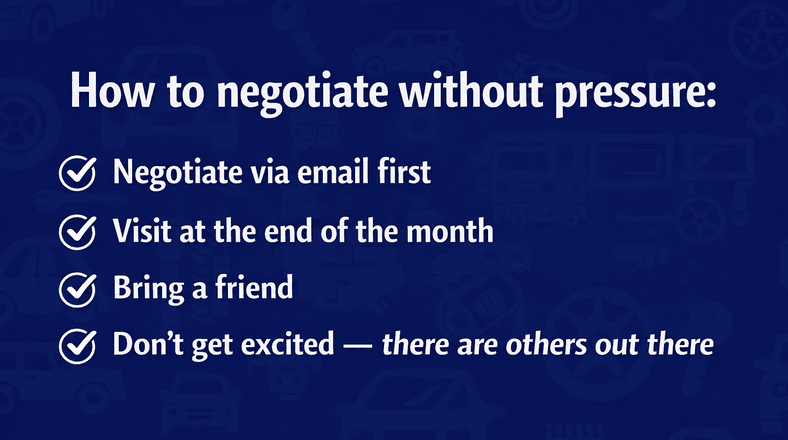

One of the best ways to avoid pressure tactics entirely is to conduct initial negotiations via email. Get quotes from multiple dealers in writing before you ever set foot in a showroom. This eliminates the time pressure and lets you think clearly.

Use these free email templates to get started on the right foot.

Dealerships have monthly quotas. Shopping in the last few days of the month often means salespeople are more motivated to make deals happen—on your terms, not theirs.

A second person helps in two ways: they provide emotional support when pressure tactics emerge, and they give you a built-in reason to pause (“I need to discuss this with my friend”). It’s harder to pressure two people than one.

The more you gush about loving the car, the more leverage the dealership has. Stay neutral and businesslike. You can get excited after you’ve agreed on a fair price.

“Another buyer is coming” is designed to create panic. Your job is to remain calm, remember that you have options, and refuse to be rushed into a decision that costs you thousands of dollars.

Use Ray’s simple response: “I understand. If they buy it before we reach an agreement, I’ll find another one.”

Then stick to your research, your budget, and your willingness to walk away. More often than not, that “other buyer” will mysteriously disappear, and suddenly the dealer will be very interested in working with you on your terms.

And if they do sell it to someone else? You’ll find another car—probably at a better price, at a dealership that doesn’t play games.

Remember: The dealership needs to sell cars. You just need to buy one car. That’s leverage. Use it.

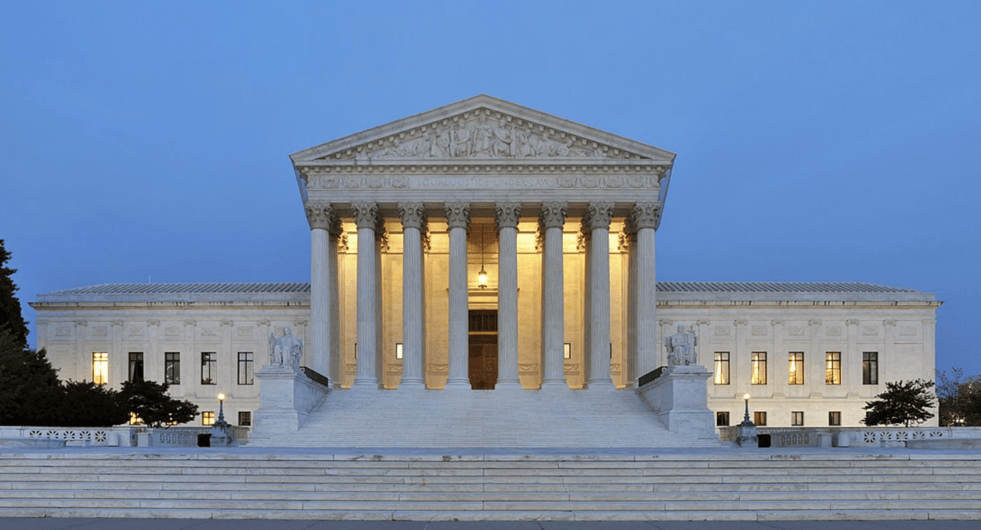

On Friday, February 20, 2026, the U.S. Supreme Court ruled that President Trump exceeded his authority when imposing sweeping global tariffs under the International Emergency Economic Powers Act (IEEPA). The 6-3 ruling puts an end to tariffs imposed under the IEEPA, but it leaves other tariff options on the table for the administration.

That decision immediately reshapes U.S. trade policy, and it has real consequences for automakers, dealerships, and car buyers. It’s important to note that this remains a developing situation, and President Trump has already committed to imposing a new 10% global tariff in coming days.

To understand what happens next, we first need to look at what the tariff environment actually looked like just before the ruling.

Before the Supreme Court decision, vehicle imports into the United States were operating under meaningfully elevated effective tariff rates. Across all imported vehicles, the blended effective tariff rate averaged approximately 15.3%. That reflects the real-world duties being paid at the border after negotiations and adjustments, not just the original headline tariff proposals.

Rates varied by country:

In practice, most North American-built vehicles retained duty-free status, preserving a major supply chain advantage for USMCA-compliant production.

It is important to clarify that these figures represent effective rates, not just headline announcements. Although initial tariff proposals were often higher, negotiations had already reduced many of them to approximately 15% for key allies.

The Supreme Court ruling invalidated tariffs imposed under IEEPA authority. As a result, those specific duties are no longer legally in force unless re-established under a different statutory mechanism. Some have estimated that more than half of the existing tariffs imposed by the U.S. were issued under the IEEPA.

Other trade authorities — such as Section 301 or Section 232 — could be used in the near future to bring back tariffs. At a press announcement on Friday, President Trump said that he will be launching a new 10% tariff using a different legal backing that the overturned IEEPA tariffs. While the Court removed the existing tariff structure, it did not permanently eliminate the possibility of future tariffs on auto imports.

This remains an evolving situation, and the auto industry is certainly following developments closely.

Removing a roughly 15% effective tariff from imported vehicles changes the cost equation meaningfully.

When a vehicle carried a 15% duty at the port of entry, that cost had to be absorbed somewhere. In many cases, it was passed through to consumers in the form of higher MSRPs. In other cases, automakers absorbed reduced incentive spending to offset it. This meant fewer low-APR incentives and cheap lease deals for consumers.

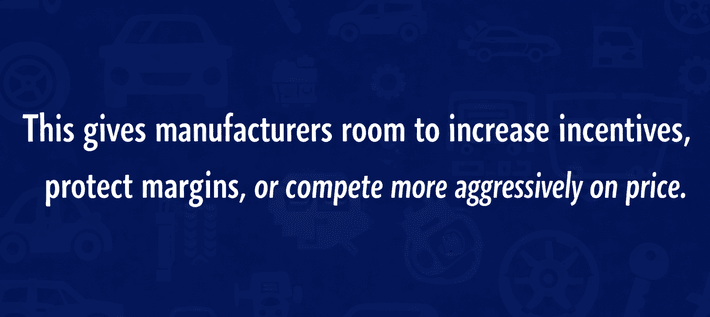

With that layer removed, automakers gain flexibility.

While vehicle prices are not going to fall 15% overnight, eliminating tariff pressure reduces upward pricing momentum. For now, the ruling gives manufacturers room to increase incentives, protect margins, or compete more aggressively on price.

This is welcome news as the industry is expecting sales to stagnate through 2026. With more competitive pricing and incentives now on the table, automakers will have new options to compete for your business.

Parts costs could also ease. Even vehicles assembled in the United States often rely on globally sourced components. If imported parts were previously facing 10–15% duties, removing those costs lowers production expenses and improves manufacturing economics. In a market where affordability remains strained in 2026, even incremental cost relief can matter.

Even the cars and trucks made in America could benefit from the Supreme Court ruling.

Competitive dynamics may also shift. Prior to the ruling, Japanese, Korean, and European vehicles were competing under approximately 15% tariff pressure, while Chinese imports faced even steeper effective burdens. With tariffs invalidated, those imported vehicles regain structural cost competitiveness. That increases pricing pressure on domestic manufacturers and could lead to stronger cross-brand competition. This typically benefits consumers.

There is also the potential for financial adjustments. Companies that paid tariffs may seek refunds, which could improve short-term profitability and potentially support future incentive programs. However, refund processes are often complex and could take time to resolve.

Before the February 20 Supreme Court ruling on President Trump’s global tariff strategy, most major vehicle-exporting countries were operating under an effective tariff environment of roughly 15%. China faced much higher blended rates, and USMCA-compliant vehicles from Canada and Mexico remained duty-free.

With those tariffs now overturned under IEEPA authority, imported vehicles and parts regain cost relief. Production inputs become less expensive, competitive pressure increases, and one of the largest recent cost drivers in the auto market has been removed.

If new car prices come down (even modestly), used car prices could also decline. That would be a win for all car shoppers in 2026. Those looking to sell or trade-in could see their trade-in values drop, however.

Vehicle prices are not going to collapse overnight. But structurally, this ruling removes a major upward force on pricing. For car buyers navigating a still-expensive market in 2026, that represents a meaningful shift — and potentially the first real affordability tailwind the industry has seen in quite some time.

After 43 years on both sides of the dealership desk, CarEdge co-founder Ray Shefska has seen every negotiation tactic in the book. And here’s something most car buyers don’t realize: the questions a salesperson asks in the first five minutes can cost you thousands of dollars before you even start negotiating.

These aren’t just innocent conversation starters. They’re carefully designed information-gathering tools that shift negotiating power away from you and directly into the dealer’s hands. In 2026, with dealership profit margins under pressure and inventory levels normalizing, these tactics are more aggressive than ever.

Let’s break down the five questions you should never answer directly—and exactly what to say instead.

Why This Question Is Dangerous

This seems like friendly small talk, but it’s actually the opening move in a complex strategy. When you tell them what you drive, you’re revealing:

In 2026, with trade-in values fluctuating more than ever due to the stabilizing used car market, this information is particularly valuable to dealers. Check out our guide to trading-in, and stick to your plan!

The Right Response

Instead of answering directly, say:

“I’m here to learn about this vehicle first. Let’s focus on what you have available.”

Or if they push:

“I might have a trade, I might not—depends on the numbers we agree on for this car first.”

Ray’s Pro Tip

“Never let them appraise your trade-in before you’ve negotiated the purchase price of the new vehicle. These are two separate transactions, and combining them only benefits the dealer. Get the best price on the new car first, then introduce the trade-in as a separate negotiation.“

Why This Is the Most Expensive Question

This is the single biggest trap in car buying, and it’s become even more prevalent in 2026 as dealers lean heavily into payment-focused selling. Here’s what happens when you give them a monthly payment target:

In 2026, the average new car loan has stretched to 68 months with the average payment hitting $739. Don’t become another statistic.

The Right Response

Say this instead:

“I don’t shop by monthly payment. What’s your best out-the-door price on this vehicle?”

We’ve been saying it for years: The out-the-door price is the only price you should be negotiating. Use this free calculator to see how it works.

If they persist:

“I have my own financing arranged. I’m only discussing the vehicle price today.”

Ray’s Real-World Example

“I’ve watched salespeople take a customer who said “I can afford $500 per month” and show them vehicles they could have bought for $400 per month with a shorter loan term. That extra $100 over 72 months? That’s $7,200 in unnecessary spending, plus thousands more in interest.“

Why Dealers Ask This Early

This question serves multiple purposes for the dealer:

In 2026, dealer financing kickbacks have actually increased as manufacturers push captive financing programs. The dealer might make $1,500-$3,000 just on your loan—incentive to push you away from your credit union’s better rate.

The Right Response

Keep your cards close:

“I haven’t decided yet. What’s your best price on the vehicle?”

Or more firmly:

“That depends on the deal we work out. Let’s talk about the car first.”

The Strategic Play

Even if you’re paying cash, Ray recommends acting like you’ll finance initially. “Get their best price, then “change your mind” and pay cash. Why? Because dealers often give better prices when they think they’ll profit on financing. Yes, it’s a game—but they taught us how to play it.“

The Pressure Behind This Classic Line

This question appears helpful on the surface, but it’s actually a closing technique designed to:

In 2026, with inventory levels much healthier than the shortage years of 2021-2023, there’s absolutely no reason to be in a rush unless you’ve done your homework and know you’re getting a fair deal.

The Right Response

Shut down the pressure:

“I’m not making a decision today. I’m gathering information and comparing options.”

Or:

“I need to see your best offer first, then I’ll take time to consider it.”

Ray’s Perspective

“When I was selling, this question was explicitly designed to create urgency and get a commitment. Here’s the truth: that “special price” they can offer you today? It’ll be there tomorrow. And next week. The best deals come from patient buyers who don’t fall for artificial deadlines.“

Why This Seems Harmless But Isn’t

This feels like the salesperson is being helpful and understanding your needs, but they’re actually:

In 2026’s market, feature-loaded vehicles carry significantly higher profit margins. That’s why automakers and dealers alike love to sell big trucks and SUVs. That panoramic sunroof and premium audio system? They cost the dealer far less than they’ll charge you.

The Right Response

Stay focused on the vehicle in front of you:

“I’m interested in this specific model we’re looking at. Let’s discuss this one.”

Or:

“I’ve done my research on what I need. What’s your best price on this configuration?”

The Upsell Trap

Ray says to watch out for this trap, and always stick to your budget. “Once you start describing your “dream car,” the salesperson will conveniently discover they have something “even better” that matches your description—at a much higher price point. Stick to your researched vehicle choice and don’t get emotionally sidetracked.“

After spending decades on both sides of the desk, here’s the approach that consistently gets CarEdge readers the best deals:

Step 1: Do Your Homework Before You Arrive

Step 2: Control the Initial Conversation

Step 3: Negotiate One Thing at a Time

Step 4: Be Willing to Walk Away

Dealers in 2026 are increasingly adding “market mandatory accessories” to vehicles before they hit the lot—things like paint protection, nitrogen-filled tires, or wheel locks. These typically cost the dealer $100-$300 but get marked up to $1,500-$3,000.

How to handle it: Negotiate these items down or off entirely. They’re not mandatory—they’re dealer profit centers.

After the backlash against ADM (Additional Dealer Markup) during the shortage years of 2021-2023, some dealers now call these markups “market adjustments” or “market price corrections.” It’s the same thing with a friendlier name.

How to handle it: Any price above MSRP requires justification. You should never pay over MSRP for the vast majority of models in 2026. Most models can be successfully negotiated to 5-10% below MSRP, or even more for leftover 2025 models.

More dealers are using online tools that ask you to input your trade-in info, desired payment, and financing preference before you ever visit. These are the same five questions in digital form.

How to handle it: Use online tools to research and identify vehicles, but don’t provide specific trade-in or financing information until you’re ready to negotiate in person.

A CarEdge reader emailed us last month about her experience buying a 2026 Honda CR-V. She watched our content on YouTube and implemented these exact strategies:

Total savings: $4,800 by simply controlling the information flow and negotiating strategically.

In 2026, the dealers who succeed are those who understand that informed buyers do their homework. The five questions we covered today are designed to extract information from you before you’ve extracted fair pricing from them.

Your goal walking into a dealership should be simple: keep your cards close, deflect these information-gathering questions, and focus relentlessly on one number—the out-the-door price of the specific vehicle you want.

Remember Ray’s golden rule from 43 years in the business: “The person with the most information and the least urgency wins the negotiation.”

Don’t answer these five questions directly. Don’t rush into a deal. Don’t let emotion override research. And for the love of everything, don’t focus on monthly payments.

Do your homework, control the conversation, and negotiate one item at a time. That’s how you drive off the lot with a fair deal—and how you avoid leaving thousands of dollars on the table.

Before your next dealership visit:

1. Print out or screenshot these five questions and responses

2. Research fair market value for your target vehicle

3. Get pre-approved for financing from 2-3 sources

4. If trading in, get appraisals from online buyers like CarMax and Carvana

5. Role-play deflecting these questions with a friend or family member

6. Commit to walking away if you don’t get a fair deal

The 2026 car market is vastly different from the shortage years, and dealers know they need to work harder for your business. Use that to your advantage by being the informed, prepared buyer who knows exactly which questions to deflect—and how to deflect them.

Happy car shopping, and remember: the best deal is the one where you control the conversation from start to finish.

If you’ve walked into a Toyota dealership recently and asked about a RAV4, you probably felt your stomach drop. The markups on America’s best-selling SUV are, frankly, insane right now — and dealers are counting on you not knowing any better.

But here’s the thing: you don’t have to pay those inflated prices. CarEdge’s Ray Shefska has spent decades on the dealership side of the desk, and his son and co-founder Zach tracks the pricing data obsessively. Together, we’re pulling back the curtain on exactly what dealers pay for a RAV4, what they’re charging you, and what you should actually agree to spend.

Let’s break it all down.

The Toyota RAV4 has been the best-selling crossover in America for years running, and 2026 is no different. Demand remains sky-high for a few key reasons:

When demand outstrips supply, dealers add “market adjustments” — a polite way of saying they’re tacking on pure profit above MSRP. And right now, those adjustments on certain RAV4 trims are reaching $3,000 to $7,000 or more.

Before you can negotiate effectively, you need to understand the numbers. Here’s the reality that dealers don’t want you to see — the gap between invoice price (what the dealer pays Toyota) and MSRP (the sticker price).

| RAV4 Trim | Invoice Price (Est.) | Base MSRP | Built-In Dealer Margin |

|---|---|---|---|

| LE | $28,800 | $31,090 | $2,290 |

| XLE | $30,200 | $32,590 | $2,390 |

| XLE Premium | $32,500 | $35,090 | $2,590 |

| Adventure | $34,000 | $36,690 | $2,690 |

| TRD Off-Road | $35,200 | $38,090 | $2,890 |

| Limited | $36,800 | $39,790 | $2,990 |

Note: Invoice prices are estimates based on available dealer cost data. Actual invoice may vary slightly by region and installed options.

That built-in margin of $2,000–$3,000 is already profit for the dealer — before any markup. On top of that, Toyota offers dealers holdback (typically around 2% of MSRP) and potential volume bonuses. So when a dealer tells you they’re “barely making anything” at MSRP, that’s simply not the full picture.

The gas-only RAV4 markups are bad. The hybrid markups are worse. And the RAV4 Prime? That’s where things go completely off the rails.

| Model | MSRP Range | Typical Market Markup (2026) |

|---|---|---|

| RAV4 Hybrid | $33,090 - $41,290 | $2,000 - $5,000 over MSRP |

| RAV4 Prime SE | $44,090 | $3,000 - $7,000 over MSRP |

| RAV4 Prime XSE | $49,590 | $5,000 - $10,000+ over MSRP |

We’ve seen real listings showing RAV4 Prime XSE models with $8,000 to $10,000 “market adjustments” slapped right on the window sticker. That’s a $50,000 compact SUV pushed to nearly $60,000 before taxes and fees.

As Ray puts it: “Just because they CAN charge it doesn’t mean you should pay it. There’s always another dealer.”

Wondering how you can put this knowledge to use saving you money in 2026? Here are the numbers you should walk into the dealership armed with.

For the standard (non-hybrid) RAV4, inventory has improved enough that you should not be paying over MSRP. Period. In fact, depending on your market and willingness to be patient, here’s what to target:

If a dealer won’t budge off a markup on a gas RAV4, walk away. There are plenty of them on lots right now.

Hybrid inventory has improved compared to 2023–2024, but it’s still tighter than the gas model. Your targets:

The Prime is the toughest nut to crack because Toyota allocates so few to each dealer. But that doesn’t mean you should light money on fire:

Knowing the right price is half the battle. Here’s how to actually get it.

Email or message the internet sales departments of at least 5–8 Toyota dealers within a 100-mile radius. Ask for their out-the-door price on the specific trim and color you want. This creates competition and immediately reveals who’s marking up and who’s not.

At CarEdge.com, you can check what others are actually paying for a RAV4 in your area. Real transaction data beats guesswork every time.

Markup culture varies wildly by region. Dealers in the Southeast and parts of the Midwest tend to be more competitive on Toyota pricing than coastal metros. A 3-hour drive could save you $3,000–$5,000 on a RAV4 Prime.

These are the best states for car buying, but keep in mind that you’ll always pay sales taxes to whichever state you reside in.

This is the sneaky markup. Dealers will add nitrogen-filled tires, door edge guards, all-weather mats, and paint protection — items that cost them $200 total — and charge you $1,500–$2,500 as a “dealer accessory package.” This is a markup by another name.

Ask specifically: “What dealer-installed accessories are included, and can they be removed from the price?” If the answer is no, that’s a red flag.

Check out our guide to dealer add-ons and fake fees.

Toyota’s allocation system doesn’t work exactly like Ford or Chevy’s factory ordering, but many dealers will take a priority order or put you on an allocation list at MSRP. If you can wait 6–12 weeks, this is one of the best ways to get a fair price on a Hybrid or Prime.

Just make sure to get your out-the-door price in writing with the dealership when you place the order. You don’t want to play any games when your car finally arrives.

End-of-month, end-of-quarter, and late in the model year (September–November) are when dealers are most motivated to move units and hit manufacturer bonus targets. That $2,000 markup in March might become an MSRP deal in October.

These are the best times to buy a car.

Before you walk into any dealership, write down your maximum price. If the deal doesn’t hit that number, leave. Every single time. The most powerful negotiation tool you have is your willingness to walk away — and dealers can sense it.

As Ray always says: “The dealer needs to sell you a car more than you need to buy one today.”

If RAV4 markups are making your blood pressure spike, it’s worth considering whether a competitor might give you better value right now.

The point isn’t that these vehicles are better than the RAV4 — it’s that paying $5,000+ over MSRP for any vehicle is rarely a smart financial move when comparable options exist at fair prices.

Let’s do the math that dealers hope you won’t do.

Say you pay a $5,000 markup on a RAV4 Hybrid XLE Premium. Here’s what that actually costs you:

And here’s the kicker: that $5,000 markup does not increase your vehicle’s resale value. When you go to sell or trade in, the car is worth the same whether you paid MSRP or $5,000 over. You’re just eating that loss.

The market is always changing, and the data gives us clues about what might be on the horizon for RAV4 shoppers:

The Toyota RAV4 is a fantastic vehicle — there’s a reason it sells in huge numbers year after year. But a good car at a bad price is still a bad deal.

Here’s your takeaway: On a gas RAV4, you should be paying MSRP or less. On a Hybrid, target MSRP. On a Prime, don’t exceed $2,000–$3,000 over MSRP, and expand your search radius before accepting more. Never pay for mandatory dealer-added accessories you didn’t request, get multiple quotes, and always be willing to walk away.

The dealers marking up RAV4s by $5,000+ are banking on two things: your impatience and your lack of information. Now you have the information. Don’t let impatience be the thing that costs you thousands.

For personalized deal analysis and real-time pricing data, check out the tools at CarEdge.com — we’re here to make sure you never overpay.

Have a RAV4 deal you want us to evaluate? Share it in the CarEdge Community forum for others to chime in.

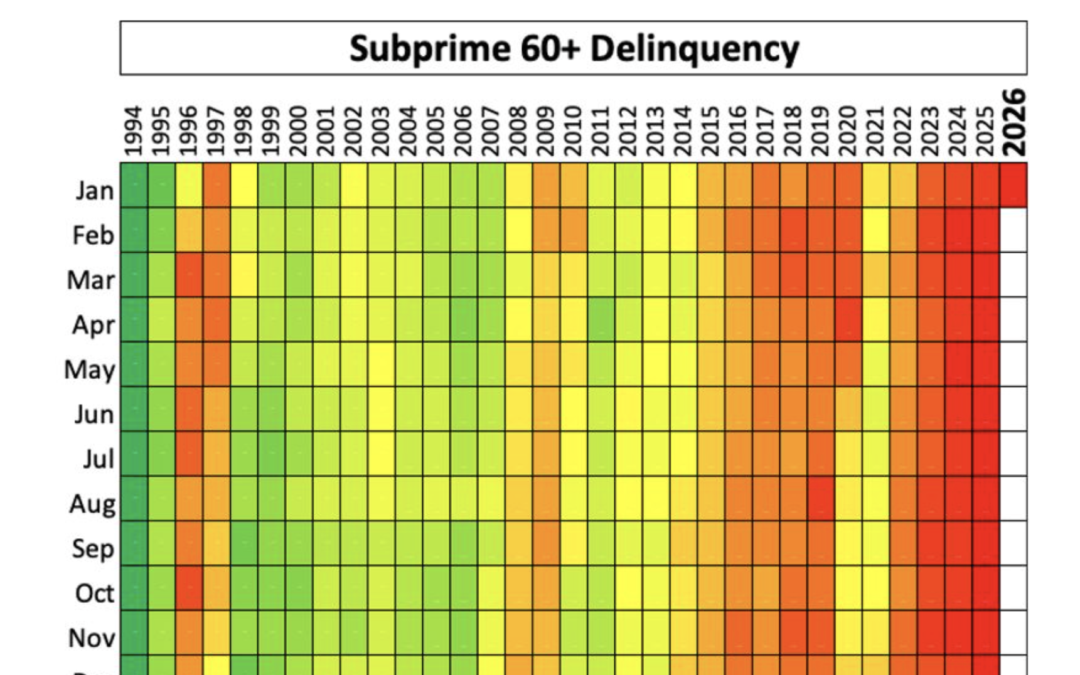

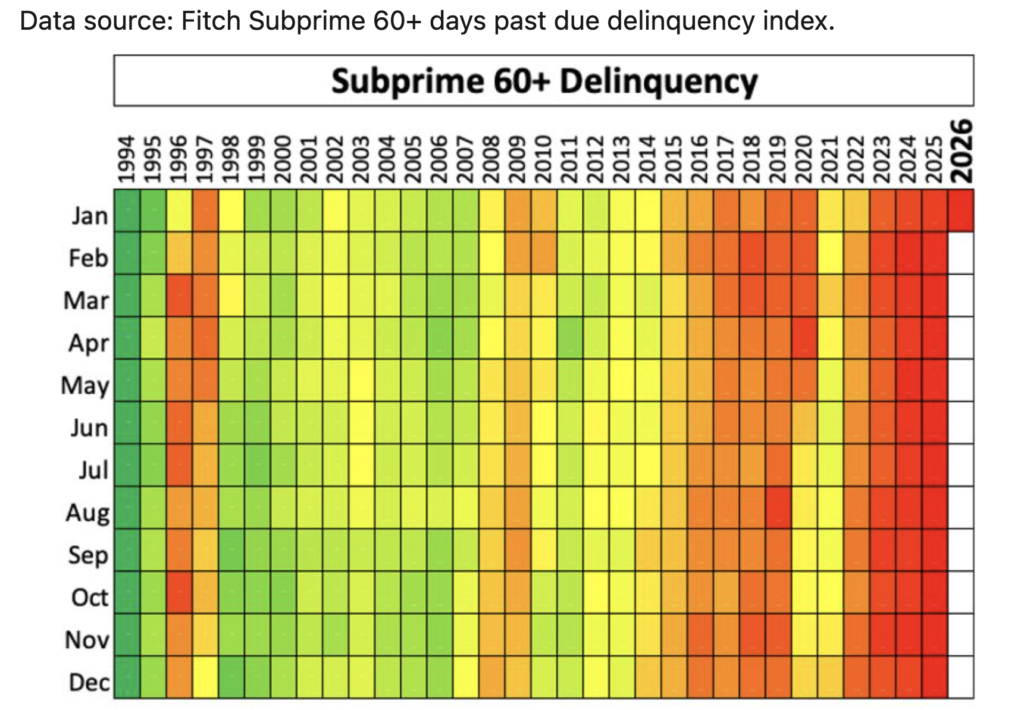

The numbers are in, and they’re alarming. Subprime auto loan delinquencies have reached their highest level in 32 years — a record stretching all the way back to January 1994. According to data published by Fitch and analyzed by industry expert Bill Ploog, the January 2026 figures mark a 385-month record high for 60-plus-day past-due delinquencies among subprime borrowers.

So what does this mean for everyday car buyers, the auto industry, and the future of car prices? Let’s break it down.

A delinquency heat map shared by Ploog covering 385 months of data paints a stark picture. Green represents the lowest delinquency rates for a given month across multiple years, red represents the highest, and yellow marks the midpoint.

For subprime borrowers — those with lower credit scores — the chart has been deep red for nearly four consecutive years, from 2023 through early 2026. That means the percentage of subprime auto loan holders who are 60 or more days behind on their payments is at the worst levels seen in over three decades.

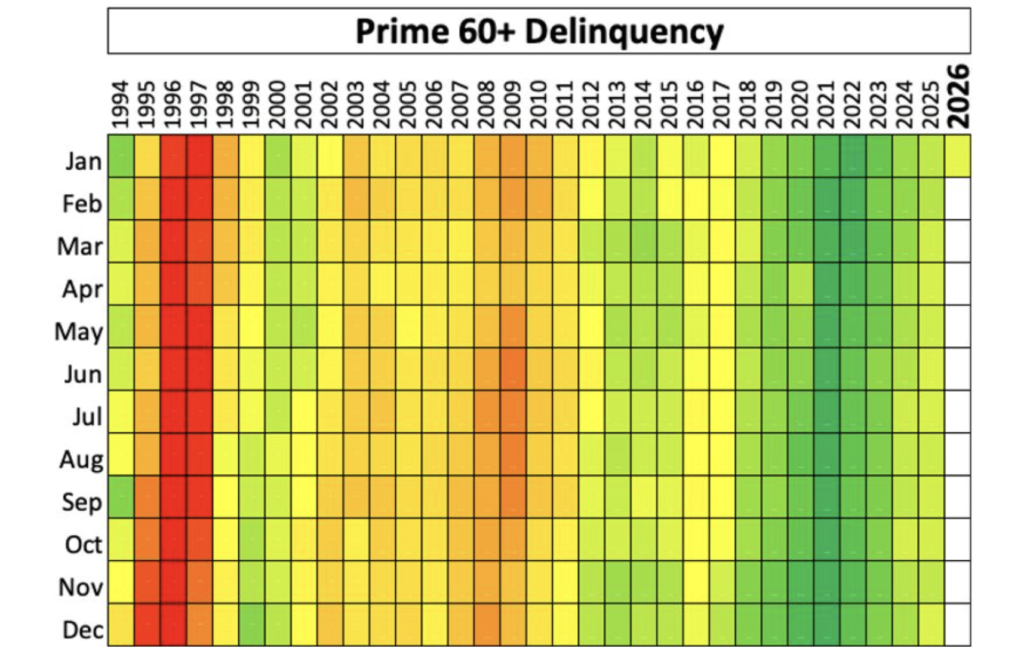

Meanwhile, prime borrowers — those with good credit — are doing just fine. Their delinquency rates remain healthy and stable. The crisis is concentrated squarely among those who can least afford it.

When a borrower falls 60 or more days behind on their auto loan payment, banks begin seriously considering repossession. The vehicle gets seized, sent to auction, and sold — often for far less than what’s owed on the loan. It’s a lose-lose scenario: the borrower loses their car and likely takes a devastating hit to their credit, while the lender absorbs a loss.

This isn’t just a rearview mirror metric. Because the data reflects accounts that are already 60-plus days past due, it’s showing us the consequences of lending decisions made months or even years ago. The decisions that got us here were baked in long before the numbers showed up on the chart.

Several converging factors have created what many are calling bubble territory in auto lending:

As Ray Shefska, a 43-year auto industry veteran and co-host of CarEdge Live, put it: “What more clearly do you need to see that suggests there’s a bubble going on?“

Industry voices are increasingly sounding the alarm on ultra-long auto loans. Brian Binstock, a well-known figure in automotive retail, recently posted that 84-month car loans are “a death trap for customers” — and bad for dealers too.

We’ve been warning against 84-month loans for years.

Here’s the logic: when a dealership puts a customer into a 7-year loan, that customer is effectively removed from the market for the better part of a decade. They can’t trade in, they can’t upgrade, and they’re stuck underwater on a depreciating asset.

“Dealers become enamored with short-term profit gains and don’t look at the long-term ramifications,” Ray explained. “When you put people into 84-month and 96-month auto loans, you are essentially taking them out of the market. Two or three years from now, the same dealers are going to be wondering how to get their customers back. You don’t. You can’t.”

This dynamic is compounded by the decline of leasing. During COVID and the chip shortage, manufacturers pulled back on subsidized lease programs. Leasing, which once represented 32–33% of all vehicle sales, dropped to roughly 17–18%. Leasing had the built-in benefit of cycling customers back into the market every three years. Without it, the industry has leaned harder on long-term financing — with devastating consequences.

The subprime auto loan crisis also raises serious questions about the investors buying asset-backed securities (ABS) tied to these loans. Companies like Carvana, whose loan portfolios skew heavily subprime, package and sell these loans to investors on Wall Street.

“Why would you look at these stats, look at that chart, and say ‘Yeah, let’s buy that stuff’?” Zach Shefska asked during the show. “What could possibly go wrong? We are at a 32-year high, and yet it doesn’t set off alarm bells on Wall Street.“

The parallels to the 2008 housing crisis are hard to ignore. Back then, lenders were approving mortgages for anyone who could “fog a mirror.” Today, the same dynamic is playing out in auto lending. If you can prove you have a pulse and a minimal income, there’s likely a lender willing to approve you — often at predatory interest rates and on terms designed to maximize lender and dealer profit at the borrower’s expense.

Here’s where it gets interesting for anyone shopping for a vehicle. If subprime delinquencies continue to climb and more borrowers are effectively locked out of the market — whether through repossession, negative equity, or simply being trapped in a long-term loan — demand for vehicles should eventually decline.

Basic economics says that when demand drops and supply holds steady, prices come down. That could mean more affordable cars in the future — but it’s a long road to get there.

There’s also a manufacturing angle. If automakers recognize that a growing share of buyers are locked into 6-, 7-, or 8-year loans, they may reduce production to avoid flooding dealerships with inventory that has no buyers. That could temper the price relief somewhat.

As Ray noted: “You take these people out of the market, there’s less demand. When you take out demand and keep supply the same, prices should go down. That should be what happens.“

But he also cautioned that financial engineering — creative lending programs designed to squeeze more buyers into the market — could delay or prevent that correction from ever fully materializing.

The auto loan crisis doesn’t exist in isolation. Consumer debt across the board is at record highs. Credit card balances continue to climb month after month, and most cardholders make only minimum payments — a strategy that can take 30 years to pay off a balance.

“We as a society have created this cycle, and we need to break the cycle,” Ray said. “We need to say it’s okay if you don’t have the latest and the greatest. Just have something that works and works well.“

The data tells a story of a system that incentivizes short-term consumption over long-term financial health. Lenders profit from high-interest, long-term loans. Dealers profit from moving units today. Finance managers profit from maximizing their pay plans. And borrowers — especially subprime borrowers — bear the consequences.

The 32-year record in subprime auto loan delinquencies is more than a statistic — it’s a warning signal for the entire auto industry and for consumers alike. The combination of extended loan terms, loose lending standards, record negative equity, and declining borrower creditworthiness has created conditions that many industry experts are calling unsustainable.

Whether this leads to a meaningful correction in car prices, a wave of dealership struggles, or a fundamental rethinking of how auto lending works in America remains to be seen. But one thing is clear: the current trajectory isn’t working for the people it’s supposed to serve. Being informed, making disciplined financial decisions, and living within your means isn’t just good advice — in today’s auto market, it’s essential.