CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

Every month, analysts and journalists report on the “average new car price in America.” It sounds useful, but to the average American car buyer, it rarely is.

That number includes every new vehicle sold, from a heavily discounted Mitsubishi Mirage to a $200,000 Porsche 911. Low-volume luxury models and niche vehicles skew that average in ways that have nothing to do with the cars most Americans are actually buying. When the average new car price goes up, is it because your next car costs more, or because a handful of wealthy buyers picked up more exotics last month? You can’t tell.

At CarEdge, we think car buyers deserve a more accurate measure of car price trends. So we built one.

Each month, we track the average transaction prices and inventory levels of the 20 best-selling vehicles in America. These are the trucks, SUVs, and cars that mainstream car buyers are actually shopping for: the Ford F-150, the Toyota RAV4, the Honda CR-V, and the like. These are vehicles that move in massive volumes and reflect the market the way most Americans experience it.

By focusing on the Popular 20, we filter out the noise and outliers. What remains is a clear, honest signal of where new car prices and inventory are actually heading for mainstream buyers.

We track two things for each model every month.

Average Transaction Price is what cars are actually selling for, not the MSRP.

Market Day Supply (MDS) is how many days of inventory dealers have on hand at the current sales pace. This is the single best indicator of where prices are heading. Low supply means dealer leverage. High supply means shopper leverage. Learn more about this market metric here.

We’ll update this data every month. Over time, we hope this becomes a useful tool, providing a ground-level view of the market that journalists, analysts, and car shoppers can actually rely on.

| January 2026 | February 2026 | Percent Change | |

|---|---|---|---|

| Ford F-150 | $61,109 | $61,217 | 0.18% |

| Chevrolet Silverado 1500 | $53,286 | $52,911 | -0.70% |

| Toyota RAV4 | $37,379 | $37,432 | 0.14% |

| Honda CR-V | $38,667 | $38,709 | 0.11% |

| Ram 1500 | $59,331 | $60,056 | 1.22% |

| GMC Sierra 1500 | $62,583 | $62,347 | -0.38% |

| Toyota Camry | $35,209 | $35,202 | -0.02% |

| Toyota Tacoma | $46,103 | $46,088 | -0.03% |

| Toyota Corolla | $25,666 | $25,710 | 0.17% |

| Honda Civic | $29,210 | $29,277 | 0.23% |

| Hyundai Tucson | $35,321 | $35,444 | 0.35% |

| Ford Explorer | $50,078 | $49,953 | -0.25% |

| Nissan Rogue | $33,191 | $32,764 | -1.29% |

| Jeep Grand Cherokee | $45,370 | $45,348 | -0.05% |

| Chevrolet Trax | $25,565 | $25,652 | 0.34% |

| Subaru Crosstrek | $32,690 | $32,896 | 0.63% |

| Kia Sportage | $35,508 | $35,492 | -0.05% |

| Subaru Forester | $39,344 | $39,466 | 0.31% |

| Jeep Wrangler | $53,454 | $53,477 | 0.04% |

| Subaru Outback | $40,225 | $40,876 | 1.62% |

| Top 20 Average Selling Price | $41,964 | $42,016 | 0.12% |

| January 2026 | February 2026 | Percent Change | |

|---|---|---|---|

| Ford F-150 | 81 | 129 | 59% |

| Chevrolet Silverado 1500 | 65 | 92 | 42% |

| Toyota RAV4 | 22 | 37 | 68% |

| Honda CR-V | 53 | 67 | 26% |

| Ram 1500 | 149 | 163 | 9% |

| GMC Sierra 1500 | 78 | 115 | 47% |

| Toyota Camry | 33 | 45 | 36% |

| Toyota Tacoma | 58 | 58 | 0% |

| Toyota Corolla | 37 | 44 | 19% |

| Honda Civic | 57 | 67 | 18% |

| Hyundai Tucson | 95 | 132 | 39% |

| Ford Explorer | 117 | 141 | 21% |

| Nissan Rogue | 101 | 93 | -8% |

| Jeep Grand Cherokee | 133 | 156 | 17% |

| Chevrolet Trax | 88 | 109 | 24% |

| Subaru Crosstrek | 73 | 90 | 23% |

| Kia Sportage | 100 | 121 | 21% |

| Subaru Forester | 103 | 77 | -25% |

| Jeep Wrangler 4-Door | 151 | 180 | 19% |

| Subaru Outback | 74 | 117 | 58% |

| Top 20 Average MDS | 83 | 102 | 22% |

Of the 20 models we track, 18 saw market day supply increase from January to February. Inventory is building across the mainstream market, and that matters enormously for buyers. More supply means more negotiating leverage, less pressure to pay over sticker, and more time to make a smart decision.

The biggest jumps came from some of the market’s highest-volume trucks and SUVs. The Ford F-150 saw its MDS leap from 81 to 129 days, a 59% increase in a single month. The Subaru Outback surged from 74 to 117 days, and both the GMC Sierra 1500 and Hyundai Tucson climbed 37 days each. These are significant moves.

Sometimes, a sudden jump in supply reflects a recent delivery of vehicles from the factory. That is likely the case with the Outback and F-150. To find vehicles sitting on dealership lots the longest, use tools like CarEdge Pro to gain market insights. These are always the most-negotiable new cars.

On the other end of the spectrum, the Toyota RAV4 remains the tightest vehicle in our index at just 37 days supply, up from 22 in January but still firmly in seller’s-market territory. The Toyota Tacoma held perfectly flat at 58 days. The Subaru Forester was the only model to see a meaningful inventory decline, dropping from 103 to 77 days. Subaru is likely selling down 2025 Forester inventory as new 2026 shipments are imminent.

Despite the inventory surge, transaction prices barely moved for most models. The Popular 20 average transaction price in January was $41,979. In February it was $41,994, essentially flat.

That stability is worth noting. Rising inventory doesn’t immediately push prices down — the market doesn’t move that fast. Prices tend to lag inventory by weeks or months. If the supply trend continues into March and beyond, downward pressure should follow, particularly in the truck segment where inventory is growing fastest.

The Ram 1500 was the most notable outlier on the upside, rising $725 to $60,056 despite already carrying 163 days of supply, the second-highest in the index. That’s a disconnect worth watching. The Subaru Outback also climbed $651, coinciding with its inventory nearly doubling. Moving in the opposite direction, the Nissan Rogue fell $427 as its inventory slightly contracted.

The full-size truck segment — F-150, Silverado, Ram, and Sierra — dominates our index both by volume and by price. Their average transaction prices sit well above $60,000, a level that would have seemed extraordinary just a few years ago. At the same time, three of the four now sit at 90-plus days of supply, with the Ram above 160. These are buyers’ market conditions by any historical standard. Shoppers cross-shopping full-size trucks have real leverage right now and should use it.

Pay close attention to the MDS figure for the vehicle you’re considering. Anything above 90 days is a buyer’s market in 2026. With these models, you have room to negotiate. Trucks and large SUVs have higher inventory in general, and are the most negotiable. Thousands of 2025 models remain unsold, and these present the greatest opportunities for saving.

Anything below 45 days means the dealer has the upper hand. Negotiating discounts will be tough for these cars. Right now, the RAV4, Camry, and Corolla are all in high demand and short supply.

If you’re watching the broader market, the February inventory surge is the leading indicator to follow. If inventory (as measured by MDS) continues climbing into the spring, expect transaction prices to soften, especially for slower-selling trucks and three-row SUVs.

Methodology: Average transaction prices reflect what buyers paid at the dealership, aggregated across all trim levels and configurations for each model. Market Day Supply is calculated by dividing current dealer inventory by the average daily sales rate. Data covers the United States. The 20 models included reflect the best-selling vehicles in America by volume as reported in Car and Driver, with direct-to-consumer models from Tesla omitted.

Next update: March 27, 2026

About CarEdge

Founded in 2019 by father-and-son team Ray and Zach Shefska, CarEdge is a leading platform dedicated to empowering car shoppers with free expert advice, in-depth market insights, and AI-powered tools to navigate every step of the car-buying journey. From researching vehicles to negotiating deals, CarEdge helps consumers save money, time, and hassle. With trusted resources like the CarEdge Research Center, Vehicle Rankings and Reviews, and hundreds of guides on YouTube, CarEdge is redefining transparency and fairness in the automotive industry.

Follow us on YouTube, TikTok, X, Facebook, and Instagram for actionable car-buying tips and market insights.

The workers who buy trucks can no longer afford them. Here’s what the data shows.

The full-size pickup truck has always been more than just a vehicle. For electricians, contractors, factory workers, and drivers, it’s a professional tool — and often the biggest purchase they’ll make outside of a home. For decades, a mid-tier truck was attainable on a blue collar income. That’s no longer the case.

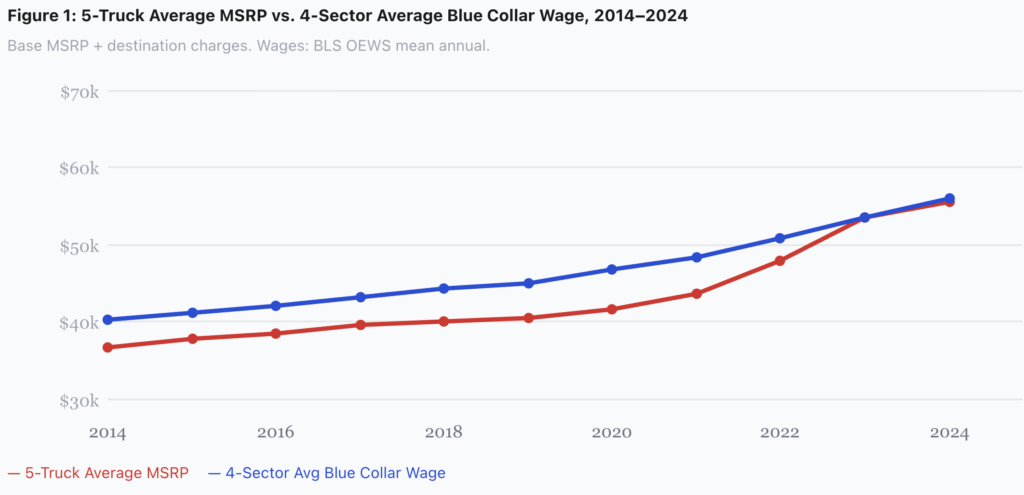

A new CarEdge analysis of truck pricing and the most recent U.S. wage data finds that between 2014 and 2024, the average mid-tier full-size truck climbed 53.1% in price — while the average blue collar wage grew just 38.7%. Truck prices are rising nearly 40% faster than the paychecks of the workers most likely to buy them.

Read the full CarEdge Truck Price Inflation Report →

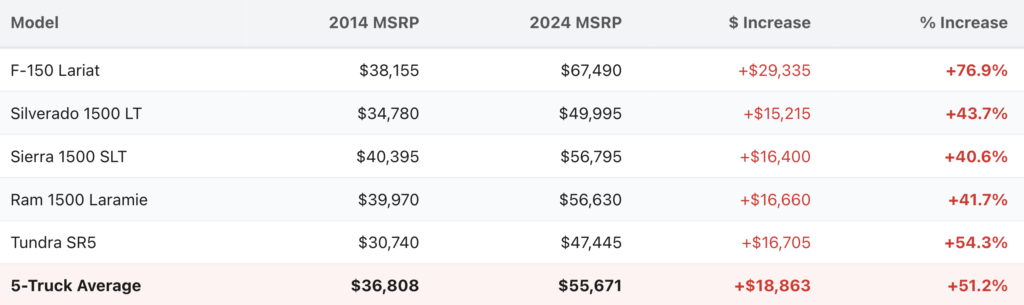

In 2014, the five trucks in our study averaged $36,808. By 2024, that average had reached $55,671 — an increase of nearly $19,000 in ten years. To put that in perspective: the entire base price of the most affordable truck in the study in 2014 is now less than the price increase on the most expensive model alone.

By 2023, something happened that had never happened before: the average truck price hit 1.00x the average annual blue collar wage. For the first time on record, buying a new truck meant spending an entire year’s gross salary.

Occupational wage statistics for 2025 are expected to be released by the Bureau of Labor Statistics in the summer of 2026. CarEdge will run the numbers again with the latest figures when we have the update.

Not all blue collar workers are in the same position. Construction and extraction workers — among the higher earners in the group at $63,920 annually — now need about 10.5 months of gross pay to afford the average truck, up from 9.5 months in 2014.

Production and transportation workers have it worse. Earning between $48,000 and $50,000 a year, these workers now need more than 13 months of gross income to cover the average truck price — and that’s before taxes, rent, or any other expense.

The pandemic accelerated an affordability crisis that was already underway. Between 2021 and 2023, the five-truck average surged nearly $10,000 in just two years as semiconductor shortages collapsed inventory and manufacturers prioritized their most profitable high-trim models. Prices spiked — and never came back down.

But the pandemic wasn’t the whole story. Automakers had been quietly walking away from the blue collar buyer for years. The number of new vehicle models priced under $25,000 dropped from 36 in 2017 to just 10 five years later. Entry-level truck trims became nearly impossible to find on dealer lots by design.

Then came the EV losses. Ford expects to continue losing billions on EVs for years to come. GM took roughly $6 billion in EV-related write-downs. Those losses were largely offset by charging more for the gas-powered trucks that actually sell. The workers who buy F-150s effectively subsidized a failed industry bet.

New-car prices in 2024 were still 29% higher than in 2019, and CarEdge projects trucks and SUVs will rise another 3–5% in 2026 — before any tariff impact on imported components. Relief isn’t coming soon. But there are ways to fight back.

Shop leftover 2025 models. Ford and Ram are heading into 2026 with tens of thousands of unsold 2025 trucks on dealer lots. That’s leverage. Dealers are motivated to move aging inventory, and buyers who target outgoing model-year trucks can often negotiate well below MSRP — sometimes thousands under sticker. The longer those trucks sit, the more room there is to negotiate.

Know the dealer’s cost before you walk in. CarEdge’s free dealer invoice tool shows you what the dealer actually paid for the truck — not what they’re asking for it. That number is your anchor. Any negotiation should start there, not at MSRP.

Have AI negotiate aging inventory for you. CarEdge Pro gives you access to target discount recommendations, market pricing data, and a step-by-step negotiation guide so you know exactly what to say — and what to push back on — at every stage of the deal.

Consider the used and CPO market. Certified pre-owned trucks from the last two to three years still offer strong capability at a meaningfully lower price point. With new truck prices near historic highs, a lightly used model can represent significant savings without sacrificing much in terms of condition or features.

Look at mid-size alternatives. For buyers whose work doesn’t require a full-size bed or towing capacity, mid-size trucks offer real utility at a significantly lower price point — and are usually easier to negotiate on.

Explore the full CarEdge Truck Price Inflation Report, including all data and methodology →

CarEdge analyzed base MSRP data for five best-selling full-size trucks cross-referenced against Bureau of Labor Statistics wage data for four blue collar occupational sectors, covering 2014–2024. Full methodology available at caredge.com/truck-price-inflation-2026.

For the first time, car shoppers can compare dealers by transparency — not just star ratings.

Car reviews have been around for decades. Dealer reviews have been around for years. But until now, no one has rated car dealerships based on what actually matters most to buyers: what they charge, and how transparent they are to deal with.

CarEdge is launching the Dealer Transparency Index — the first car dealership rating system built entirely on verified, real-world pricing data. No anonymous opinions. No self-reported surveys. Just actual out-the-door quotes, collected by CarEdge’s AI-powered car buying agents, and shared for every consumer to see.

CarEdge contacts dealerships on behalf of real car shoppers and collects itemized out-the-door quotes — the full price including doc fees, add-ons, and any dealer markup above the listed price. Every quote is then scored across four categories:

The result is a transparency score from 0 to 100, with letter grades from A to F. Dealers with five or more verified quotes are ranked publicly at caredge.com/dealer-ratings.

Anyone who has bought a car knows the feeling: you walk in expecting one price and walk out paying another. Dealer fees, paint protection packages, nitrogen-filled tires, and documentation charges can add thousands of dollars to a purchase — often without clear explanation.

Until now, there’s been no reliable way for shoppers to know which dealers play it straight and which ones play games. Yelp and Google reviews tell you whether the coffee in the waiting room was good. CarEdge’s Dealer Transparency Index tells you whether the dealer charged you $1,200 for a paint sealant you didn’t want.

The data makes clear that pricing behavior varies enormously. The highest-rated dealers score a perfect 100/100. The lowest score under 30. That gap represents real money — often thousands of dollars — out of consumers’ pockets.

The index is live now, with dealers earning grades from A to F based on their verified pricing behavior. The spread between the best and worst dealers is striking — top-rated dealers score a perfect 100/100, while the lowest-rated fall below 30. That gap represents real money out of consumers’ pockets, often thousands of dollars per transaction.

The ratings are continuously updated as new quotes come in.

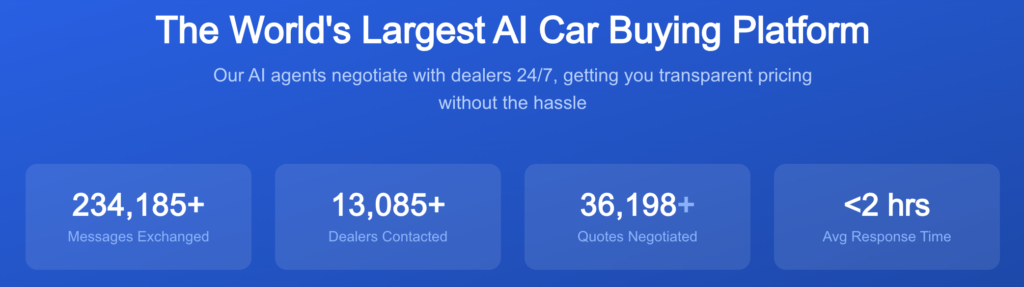

The Dealer Transparency Index is powered by CarEdge’s AI negotiation platform, which exchanges messages with dealers 24/7 on behalf of consumers. The platform has contacted thousands of dealers and negotiated quotes across the country, with an average dealer response time of under two hours.

“Consumers deserve to know what dealers actually charge — not what they claim to charge,” said Zach Shefska, co-founder of CarEdge. “We built this because the information exists. It just needed to be organized, scored, and made public.”

Car shoppers can search and compare dealer transparency scores at caredge.com/dealer-ratings. Dealers are searchable by name, location, and grade.

CarEdge was founded in 2019 by Ray and Zach Shefska to bring transparency and fairness to car buying. CarEdge always serves consumers — never dealers or automakers.

Dealer grades referenced are based on CarEdge’s Transparency Index and reflect pricing data derived from actual out-the-door quotes generated through consumer inquiries on the CarEdge platform or by CarEdge acting on behalf of the consumers it represents. Scores may be based on limited sample sizes and are subject to change as additional data is collected.

If you own a Ford or Lincoln truck or SUV from the last few years, there’s a decent chance you’re caught up in one of the largest vehicle recalls in recent memory. In February 2026, Ford filed paperwork with the National Highway Traffic Safety Administration (NHTSA) covering 4,380,609 vehicles over a software flaw that can kill your trailer’s brakes and lights while you’re towing.

Here’s what the recall is about, which Ford models are impacted, and how the latest Ford recall is a sign of a much larger problem for the automaker.

The defect lives inside the Integrated Trailer Module (ITRM), a software-driven component that manages communication between your truck and whatever you’re towing. When the vehicle wakes up from sleep mode — essentially every time you start it — there’s a chance the ITRM loses its connection to the rest of the truck’s computer system.

Ford and NHTSA describe it as a “race condition” bug, meaning the software is sensitive to the timing and sequence of events during startup. Most of the time it works fine. But when it doesn’t, the consequences can be serious: your trailer’s stop lamps go out, its turn signals stop working, and on trucks equipped with the high-series ITRM, the trailer’s electric brakes can fail entirely.

Think about what that means in practice. You’re on the highway pulling a 10,000-pound boat or a loaded work trailer. The driver behind you has no warning you’re slowing down. You apply the brakes, but only your truck is stopping — the trailer isn’t. That’s a crash waiting to happen.

Ford says it’s aware of 405 warranty claims potentially connected to the defect, along with two formal complaints filed directly with the NHTSA. The company has not identified any crashes or injuries tied to the issue.

Your dashboard will usually tip you off before things get dangerous. If you see a “Trailer Brake Module Fault” message pop up on your instrument cluster — possibly accompanied by a fast-flashing turn signal indicator or a “Blind Spot Assist System fault” warning — that’s the ITRM telling you it lost communication. Stop towing if you see either of these messages and get the software update as soon as possible.

The recall (NHTSA ID: 26V104000; Ford’s internal number: 26C10) covers the following vehicles:

The F-150 and Super Duty alone account for more than 3.4 million of the 4.38 million affected vehicles. These are America’s most popular trucks, which is part of why this recall is so significant.

Ford estimates that only about 1% of the affected vehicles actually have the defect — roughly 44,000 trucks and SUVs. But with numbers this large, even 1% is a lot of vehicles on the road.

The good news is that this is a software problem, and software problems tend to have clean fixes. Ford plans to push an updated ITRM software patch that eliminates the race condition bug entirely. Better still, most owners won’t need to make a dealer appointment.

Here’s the timeline:

Starting March 17, 2026: Ford will begin mailing recall notices to affected owners. On that same date, you’ll be able to search your VIN on the NHTSA website (nhtsa.gov/recalls) or Ford’s recall page to confirm whether your vehicle is included.

March 17–23, 2026: Owners can also take their vehicle to any Ford or Lincoln dealer at no charge to have the software update applied. No appointment necessary — walk-ins are welcome for recall repairs.

May 2026: Ford plans to begin rolling out the fix as an over-the-air (OTA) update for vehicles that support it. If your truck can receive OTA updates, you may not have to do anything at all beyond accepting the update when it arrives.

Either way — dealer visit or OTA — the repair is completely free.

If you don’t want to wait for a letter in the mail, you can check today. Go to nhtsa.gov/recalls and enter your 17-digit VIN to see if your vehicle is impacted by any open recalls. Your VIN is printed on a sticker inside the driver’s door jamb, on your registration, or on the lower left corner of your windshield.

Ford’s own recall lookup is available at ford.com/support/recalls.

Note that Ford expects all affected VINs to be searchable in the NHTSA system starting March 17. If you check today and your VIN doesn’t surface any results for this specific recall, give it until mid-March before concluding you’re in the clear.

It would be easy to treat this as an isolated incident, but it’s hard to ignore the context. In 2025, Ford issued 153 recalls covering more than 12.9 million vehicles — the most recalls any automaker has issued in a single calendar year, by a wide margin. The previous record was 77, set by General Motors in 2014. Second place in 2025 wasn’t even close: Chrysler finished with 53.

2026 hasn’t started much better. Before this trailer module recall even dropped, Ford had already issued eight recalls in the first 50 days of the year. That’s enough to put Ford ahead of every other automaker before February is out.

What makes all of this particularly hard to square is that Ford handed out company-wide bonuses just weeks ago — tied specifically to quality improvements. According to Reuters, CEO Jim Farley told employees in a February town hall that bonuses would be set at 130%, citing meaningful gains in “initial quality,” a metric that measures how often owners bring vehicles in for repairs within the first 90 days of ownership. Farley reportedly described current initial quality as the best it’s been in a decade.

Ford and Farley aren’t wrong that initial quality and recall counts measure different things. A recall can be triggered by a defect that only appears years into ownership, or — as Ford has argued — by a more aggressive internal strategy to find and fix issues before regulators force the issue.

Ford also paid a $165 million NHTSA fine in 2024 for being too slow to recall vehicles with defective rearview cameras, which likely explains some of the heightened urgency to act quickly now.

But from where a car buyer sits, the optics are tough. A record-breaking recall year followed by bonuses for quality, followed by one of the largest single recalls in recent memory — all before March — is a lot to process. Both things can be true simultaneously: initial quality may genuinely be improving while older software and hardware issues continue to surface in the field. The question for buyers is which metric they weight more heavily when deciding whether to pull the trigger on a new F-150 or pick up a used Super Duty.

If you regularly tow with your truck, the most practical step is to pay attention to those dashboard warnings. A “Trailer Brake Module Fault” message is your signal to stop towing and get the update applied. If your truck is sitting in the driveway and not connected to a trailer, the defect poses no safety risk — the problem only becomes dangerous when you’re actually towing something.

If you’re shopping for a used F-150, Maverick, Super Duty, Ranger, Expedition, or Navigator right now, don’t let this recall alone steer you away from an otherwise solid truck. An open recall is a known, fixable problem. What you want to confirm is that the recall has already been repaired before you purchase. Ask the dealer to confirm recall status before you sign, or check the VIN yourself.

Have a Ford or Lincoln truck caught in this recall? Check your VIN at nhtsa.gov/recalls, and reach out to CarEdge if you have questions about how open recalls affect your negotiating position.

The car-buying game has fundamentally changed. According to a Cox Automotive study from January 2026, 66% of buyers now cross-shop new AND used vehicles. That’s up from 57% one year ago. Even more striking: 29% of new car buyers are actively comparing leasing versus buying before they sign anything. Both numbers are all-time highs, and they represent a massive shift in how consumers approach the market.

Dealers? They absolutely hate it. And for good reason: when you cross-shop, you hold all the leverage.

A few years ago, the playbook was simple. You walked into a dealership knowing whether you wanted new or used, and salespeople could steer you toward whatever had the best margin. But three major forces have flipped the script:

1. Inventory normalization: New car supply has recovered from pandemic lows, while used prices have cooled from their 2021-2022 peaks. The gap between new and used isn’t as predictable anymore.

2. Rate volatility: Interest rates have swung wildly. A lightly used car with a 6% rate might cost more per month than a new model with manufacturer financing at 2.9%.

3. Information access: Tools like CarEdge, ChatGPT, and even TikTok have made it trivial to compare a 2024 CPO model against a brand-new 2026 with incentives—all before you ever talk to a salesperson.

The result? Buyers are making smarter, more flexible decisions. And dealers are losing control of the narrative.

Let’s break down what this means in practice. If you walk into a Honda dealership looking at a new Accord, there’s a two-in-three chance you’ve also priced out:

This isn’t indecision, it’s responsible car shopping. Buyers are treating the car market like any other major purchase: they’re comparison shopping.

Why does this frustrate dealers? Because it kills the anchor. Salespeople rely on anchoring your expectations to a single category. If you’re “a new car buyer,” they can upsell trim levels and warranties. If you’re “a used car buyer,” they can push certification fees and extended coverage. But when you’re both, they can’t box you in.

This one’s even more telling. Nearly three in ten buyers who do choose new are also running lease vs. finance calculations. That’s a massive behavioral shift.

Why? Because the math has gotten weird. In 2026, you might find:

Smart buyers are asking: “Do I even want to own this, or should I just lock in a low payment and reassess in three years?” Dealers hate this because leases require transparent residual calculations, and they can’t bury profit in interest rate markup as easily.

Cross-shopping breaks the dealership playbook. Ray’s seen this firsthand over decades in dealerships. Here’s the traditional sales process:

1. Qualify the buyer: Are they trading in? What’s their budget? New or used?

2. Isolate the vehicle: Get them emotionally attached to one car.

3. Control the numbers: Structure the deal so monthly payment feels reasonable, even if the total cost is inflated.

Cross-shopping destroys step two. When a buyer says, “I’m also looking at a CPO model across town and a new one with 0% financing,” the salesperson can’t anchor you to their inventory. You’re signaling that you’ll walk if the math doesn’t work.

Dealers make money in a few key places:

When you cross-shop new and used, you’re implicitly comparing all three. A CPO car might have a lower sticker but a higher rate. A new car might have incentives that make financing cheaper. Suddenly, the dealer can’t hide profit in one bucket because you’re scrutinizing the whole package.

Ray’s advice? This is your power move. Don’t let them silo the conversation. If they’re pushing a used car, ask about new incentives. If they’re pushing new, ask about CPO inventory. Force them to compete against themselves.

Don’t walk in with your mind made up. Even if you think you want a new 2026 RAV4, spend 20 minutes researching:

Use tools like CarEdge Pro to pull real market data. When shopping new cars, always have the invoice price. You want to walk into the dealership knowing the range of good deals, not just one target.

Here’s a real example from a CarEdge member in early 2026:

The new car was $2/month more expensive. Guess which one the dealer wanted to sell? The used one—because they owned it outright and had more margin.

The buyer? She went with the new car. Better warranty, lower rate, and she leveraged the CPO quote to get an extra $500 off.

Even if you plan to own the car long-term, get a lease quote. Why?

Leasing has quickly become a popular option as rising MSRPs have put buying out of reach for many. For drivers who want something fresh and different every two or three years, leasing lets you avoid repeated depreciation hits.

Here’s the script:

“I’m comparing this 2026 Accord at $32,000 to a 2024 CPO at $28,500 and a leftover 2025 at another dealer for $30,000. I like your car, but I need you at $31,000 to make the numbers work.”

You’re not being rude—you’re being transparent. And transparency terrifies dealers because it means you’ve done your homework.

Ray’s tip: Don’t bluff. If you say you have another offer, you better actually have it. Dealers can smell BS, and it kills your credibility.

Buyers Have the Upper Hand

The 66% cross-shopping stat isn’t just a data point—it’s a power shift. For the first time in years, buyers are forcing dealers to compete on value, not just availability. Inventory is up, prices are negotiable again, and information asymmetry is shrinking.

But this won’t last forever. If demand spikes or rates drop sharply, dealers will regain leverage. The time to cross-shop is now.

Dealers Are Adapting (And You Should Too)

Smart dealers are already adjusting. They’re pricing CPO cars more competitively, offering transparent online quotes, and training salespeople to handle cross-shoppers without the hard sell. The dinosaurs who refuse to adapt? They’re losing deals left and right.

As a buyer, your job is to reward the good dealers and walk away from the bad ones. If a salesperson dismisses your cross-shopping research or pressures you to “decide today,” that’s a red flag. There are plenty of dealers who will work with you.

The fact that two-thirds of car buyers now cross-shop new and used isn’t a trend—it’s the new normal. And the 29% who compare leasing vs. buying? That’s a sign that buyers are getting smarter, not just more cautious.

Dealers hate it because it makes their jobs harder. But for you, it’s the best leverage you’ve had in years.

Here’s your action plan:

1. Cross-shop ruthlessly: New, used, CPO, leftover models—get quotes on all of it.

2. Compare leasing and buying: Even if you think you’ll buy, the lease quote reveals hidden value.

3. Negotiate with data: Walk in with real numbers from real competitors. No bluffing.

4. Don’t rush: The market is soft right now. Dealers need your business more than you need their car.

The power is in your hands. Use it. Learn how CarEdge can get you the best deal.