CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

Car buyers, take note: Year-end sales are still months away, but that doesn’t mean you can’t score a good deal right now. We found 10 of the best cash discounts that expire at the end of the month. Some deals slash more than a quarter off MSRP.

Below, we’ve rounded up the 10 biggest cash discounts right now. All MSRPs include destination fees, and incentives may vary slightly by region. Every one of these deals expires on September 30, 2025, so act fast.

The Hornet hasn’t been the sales hit Dodge expected, but that’s translating into one of the deepest discounts in recent memory for a compact SUV. You can drive home the plug-in hybrid version of the Hornet with 27% off MSRP right now.

See offer details, or view Hornet listings near you.

Hyundai is sweetening the deal on the redesigned Kona Electric. Importantly, this $7,500 incentive is a manufacturer cash offer, not the federal EV tax credit. The Kona Electric doesn’t qualify for federal incentives, which expire at the end of this month.

See offer details, or view Kona Electric listings near you.

Genesis is cutting prices on its GV60 luxury EV as sales remain slow. Buyers can also choose an alternative 0% financing option. The GV60 is not eligible for federal EV incentives, but state incentives may apply.

See offer details, or view GV60 listings near you.

Luxury three-row SUVs rarely see this kind of discount, but considering parent company Nissan’s slowing sales and vanishing market share, perhaps it’s not such a surprise. September brings a hefty $8,000 off the Infiniti QX60.

See offer details, or view QX60 listings near you.

Ram’s pricing pressure continues. With 15% off MSRP, Big Horn models are suddenly priced far more competitively in the full-size truck segment. Don’t expect deals like this on the F-150 or Silverado.

See offer details, or view Ram truck listings near you.

The Sierra 1500 Elevation trim is carrying big incentives this September. Zero-percent financing aside, this is about as good as it gets for Sierra 1500 deals.

See offer details, or view GMC Sierra listings near you.

Plug-in hybrids like the Jeep Grand Cherokee 4xe are heavily incentivized right now, with nearly $8,000 in cash savings. Why is Jeep’s 4xe series the subject of clearance pricing? Reliability concerns give shoppers pause. See Grand Cherokee total cost of ownership data here.

See offer details, or view Jeep listings near you.

The Encore GX is Buick’s affordable small crossover, and $3,000 off makes this entry-level SUV a great deal. These days, it’s easy to forget that Buick was once known as a luxury brand.

See offer details, or view Buick listings near you.

Nissan is offering a $3,500 cash discount on the Frontier as the automaker struggles to improve U.S. sales numbers. As Toyota, Honda, Hyundai, and Kia have gained fans, Nissan has lost a lot of ground. Car buyers can use that to your advantage.

See offer details, or view Nissan listings near you.

2025 Jeep Gladiator Rubicon 4×4 – 10% Off MSRP

Grab your rubber ducks! Jeep is out to conquer the off-road world with $5,500 off MSRP for the 2025 Gladiator Rubicon. With competition from the Ford Bronco and Toyota Land Cruiser, Jeep is fighting for market share like never before.

See offer details, or view Jeep listings near you.

September’s cash deals won’t last forever, but luckily year-end sales are just around the corner. If you’re not a fan for any of these offers, chances are you won’t have to wait long to find something you like.

As CarEdge’s Ray Shefska puts it:

“If you don’t see the deal you’re looking for this month, don’t worry — chances are you’ll find it during December’s year-end sales push. Automakers and dealers always get aggressive to clear out inventory before the calendar flips. But if you’re shopping for an EV, now is the time to buy. Federal tax credits expire at the end of September, and waiting could mean leaving thousands on the table.”

Want to know where the real car deals are? Use CarEdge Pro to see behind the scenes of your local market and CarEdge Concierge if you’d like a professional to negotiate your deal for you.

Car prices have been climbing for years, and overall, that’s a trend that continues for 2026. But here’s the twist: a handful of 2026 models are actually cheaper than last year’s. And we’re not just talking about EVs. From crossovers to trucks, these seven models buck the trend with real price cuts. (All prices include mandatory destination charges, which unfortunately are still on the rise.)

2026 Base Price (MSRP + destination): $47,490

For 2025, Stellantis is out to turn around falling sales. Core to their strategy is adjusting pricing to lure in buyers. For 2026, the Dodge Durango R/T Plus is a whole lot more affordable. The Plus version of the popular Durango R/T gains premium features like leather-trimmed heated/ventilated seats, power sunroof, and adaptive safety tech.

👉 Learn more about the Dodge Durango

2026 Base Price (MSRP + destination): $52,395

Cadillac trimmed the Optiq’s price by nearly $2,000 for 2026 with the addition of a new entry-level Luxury rear-wheel-drive trim. Without federal incentives, it remains to be seen how sales will trend. At least this luxury electric crossover now has a more accessible starting point.

👉 Learn more about the Cadillac Optiq

2026 Base Price (MSRP + destination): $54,895

Chevy lowered the price of the Silverado EV’s Work Truck trims, bringing the starting price down to $54,895. Buyers can choose from three WT trims with ranges spanning 293 to 493 miles. Even at the top, the ‘26 Silverado EV is more affordable. Chevy swapped out the $97,895 RST Max Range for a new $88,695 Trailboss Max Range.

👉 Learn more about the Chevrolet Silverado EV

2026 Base Price (MSRP + destination): $36,995

After skipping 2024 and 2025, Jeep revived the Cherokee for 2026 with an all-new design, larger dimensions, and a standard hybrid powertrain. Despite improvements, the base price is $2,295 cheaper than the 2023 Cherokee that ended production.

👉 Learn more about the Jeep Cherokee

2026 Base Price (MSRP + destination): $47,355

The Wrangler lineup remains mostly unchanged for 2026, but the Rubicon trim received a rare price cut of more than $1,500. While other Wrangler trims have seen hikes, off-road fans who want the Rubicon will be saving money. Who to thank? Jeep’s slowing sales, unfortunately.

👉 Learn more about the Jeep Wrangler

2026 Base Price (MSRP + destination): $61,395 (Light Long Range)

The base EV9 still starts at $56,395, unchanged from 2025, but several trims in the lineup are cheaper in 2026. The popular GT-Line dropped by $2,000 to $73,395, while the Land is $1,000 less at $67,395. Buyers focused on higher trims will benefit the most.

2026 Base Price (MSRP + destination): $25,135

For 2026, Kia introduced a new entry-level front-wheel-drive LX trim, bringing the Seltos’ starting price down by nearly $1,000. That makes the Seltos one of the cheapest crossovers you can buy new in 2026.

👉 Learn more about the Kia Seltos

It’s rare to see new models get cheaper, but any price cut is worth noting. The truth is, the only way we’ll see more of them is if buyers push back against rising MSRPs. The best way to send that message? Skip the models with price hikes whenever you can. Vote with your wallet!

Shoppers looking to maximize savings should check local car market conditions, shop the deals, and be ready to negotiate. And most of all, NEVER shop monthly payments, and ALWAYS shop the out-the-door price!

Learn how CarEdge can make car buying (and leasing) easier than ever before.

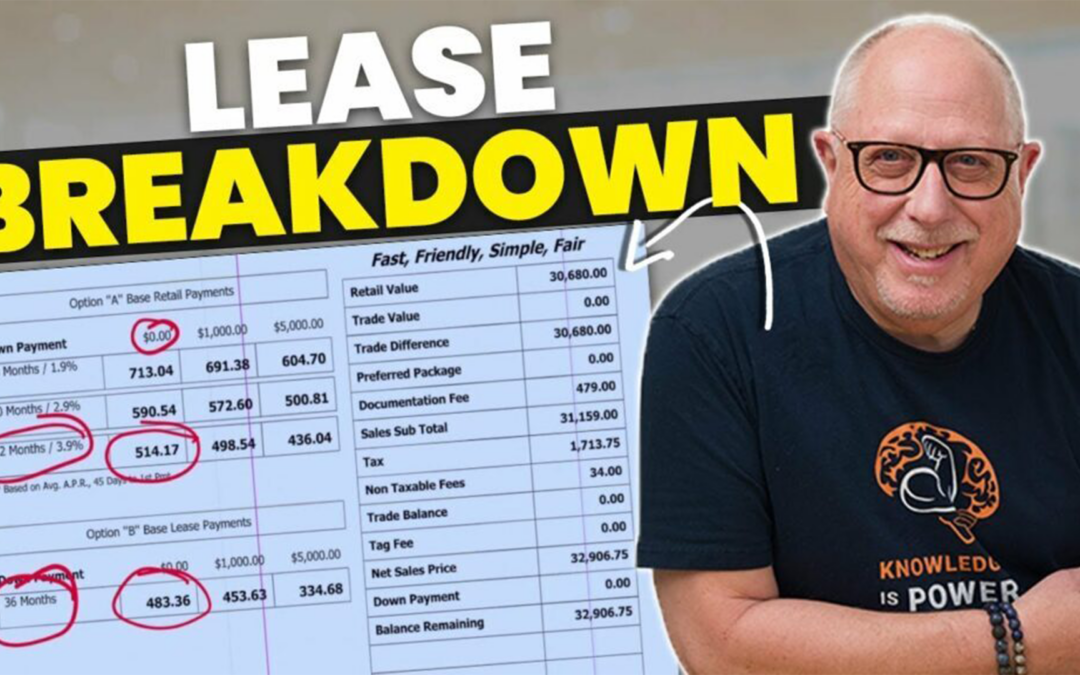

Whether you’re considering a lease for your next car or currently have a car on lease, you’re probably aware that a lease gives you no ownership. However, many dealerships processing end-of-lease returns neglect to mention an important detail. In some cases, when a lease is returned, the car has equity on it worth hundreds or even thousands. It’s called auto lease equity, and it’s money that should go in your pocket.

When you lease a car, you don’t get to drive it as much as you want. Rather, the lease is made out for a specific mileage level. Depending on the model and contract, you could be allowed anything from 30,000 miles to 60,000 miles in the three years that you keep the car. If you go over your mileage limit, you will be charged for overages when it’s time to return the car at the end of the 36-month lease period. This can be an expensive miscalculation on your part, so be careful to not exceed your mileage limit, unless you’re prepared to pay up at the end.

Should the opposite happen – if you manage to drive less than you’re allowed – you’ll have ended up paying more for the car than you’ve actually used. It’s this difference that makes up the equity that you have in your car. When the dealership sells the car on the used market, they are likely to get more than they originally hoped for, as they expected the car to have more mileage. They should give you a share of this windfall. Depending on the model and how many miles you’ve managed to save, you could have equity worth a substantial sum of money in the car.

If you’re wondering whether you have auto lease equity, the process is simple.

See, we told you it would be simple. It’s worth checking if you have lease equity, especially if you’re not too happy with your current ride.

Most dealerships don’t pay cash for the lease equity that your car brings them. Rather, they offer to give you credit that you can put towards your next lease, buying a new car, or even if you decide to buy the leased car outright. That’s always an option. Unfortunately, dealerships are often less than upfront about lease equity, and often fail to bring up the subject in the hope that their customers won’t know enough to ask.

See all of your lease-end options

Before you hand in the key at the end of your lease, it’s important that you look at the odometer and determine how many miles you’ve saved. If you’re under your lease mileage allowance, you should bring it up when it comes time to give back the car. Doing so could save you a lot of money in the form of a hefty discount on your next car.

Now for some free car leasing advice from CarEdge co-founder Ray Shefska! Subscribe to our YouTube channel for more tips and tricks for buyers and sellers.

If you’re shopping for a car in 2025, timing matters more than ever. Interest rates, expiring EV incentives, and dealership lots overflowing with new models have created a rare window for buyers to save big. But here’s the catch: not everyone should buy now.

For most car shoppers, the smartest move is to wait for year-end car sales in November and December. EV buyers are the exception, and we’ll explain why.

Mark your calendar. The first big wave of year-end deals will show up around Black Friday in late November. But the real flood of discounts lands in December, when automakers and dealers face the end-of-year crunch.

This is when manufacturers pile on cash rebates, 0% APR financing, and lease specials to hit sales targets and clear out inventory. Dealers are under pressure too, eager to move 2025 models off the lot before they officially become “last year’s cars.”

Now that we’ve covered when showtime will arrive, let’s get into who should wait for year-end specials, and who should just go ahead and buy now.

If you’re considering an electric vehicle, the clock is ticking. The federal EV tax credit expires on September 30, 2025. New IRS guidance confirms that buyers can still claim the credit as long as they have a binding written order with a deposit in place by that date—even if delivery happens later.

For the first time ever, electric vehicle inventory is lower than the overall new car market, at least by the Market Day Supply measure of demand. As buyers rush to snag their $7,500 point-of-sale discount or tax credit, several top electric models have fallen below 30 days of market supply. This makes EVs less negotiable for the time being, at least until inventory builds back up.

Ray Shefska, CarEdge co-founder, puts it plainly:

“EV shoppers should take advantage of the federal tax credits before they expire. Do it now, not later. It will be a while before EVs pile up on dealership lots again, so now is your best chance at savings.”

If you’re buying an EV, September is your deadline. After that, the credit vanishes, and you’ll be left paying more until inventory builds back up in 2026. Check out local EV listings with insider market data.

If you’re shopping for a gas-powered or hybrid vehicle, patience will pay off. Unlike EV buyers who need to act fast, the best move for everyone else is to wait until year-end sales in November and December.

That’s when automakers roll out their biggest discounts of the year to clear 2025 models off lots and make room for 2026 arrivals. Expect 0% APR financing, thousands in cash rebates, and aggressive lease specials once Black Friday kicks off the season.

Ray Shefska puts it this way:

“Manufacturers and dealers get more aggressive in December than at any other time of the year. That’s when you’ll see the deals worth waiting for.”

If you’re buying an ICE or hybrid model, hold off until year-end. You’ll likely save more by waiting just a few months than by rushing into a deal today.

If you’re hunting for the deepest discounts this November and December, look at leftover 2025 models. With 2026 vehicles already arriving, automakers don’t want unsold inventory sitting around. That’s where the best year-end car sales will be found.

As of September 2025, two-thirds of all new car inventory is from the 2025 model year. Open to something older for a greater discount? There are 90,000 2024 models that are still looking for buyers. Buyers should confidently negotiate at least 15% off MSRP for these cars and trucks that will soon reach their second birthday without a buyer.

Expect to see aggressive year-end car deals on:

Put simply: year-end sales are the last chance to score thousands off a 2025 model before automakers reset the board with higher 2026 prices.

If you’re thinking about waiting until next year, think twice. Automakers are already rolling out price hikes for 2026 models, and they’re not small. Subaru has announced increases across much of its lineup, Chevrolet is sneaking in higher MSRPs and padded destination fees, and other brands are following suit.

The truth is, MSRPs rarely fall, and 2026 will be no exception. Even if incentives improve later, higher sticker prices and fees mean many buyers will end up paying more. That’s why year-end 2025 car sales are your best shot at grabbing a 2025 model before the price resets upward.

Here’s another reason to wait: the Federal Reserve is expected to cut interest rates in late 2025, with meetings in September, October, and December. By November and December, auto financing could finally become more affordable.

Lower rates mean two things:

That’s why it pays to be prepared. Shoppers who know what fair pricing and rates look like will be better positioned when demand picks up.

Dealers love to talk about monthly payments, but don’t let that distract you from the total out-the-door cost. Always shop around before accepting a higher APR from the dealership, especially if you’re buying in-demand models like Toyota, Lexus, or Honda. Competitors like Mazda, Hyundai, and Kia commonly offer greater discounts and APR incentives.

CarEdge can help you compare financing offers, negotiate discounts, and avoid dealer tricks. Whether you’re looking at year-end clearance sales or considering one of the last EV credits, the right strategy can save you thousands.

See how we can help make car buying easy and pain-free, no matter your budget.

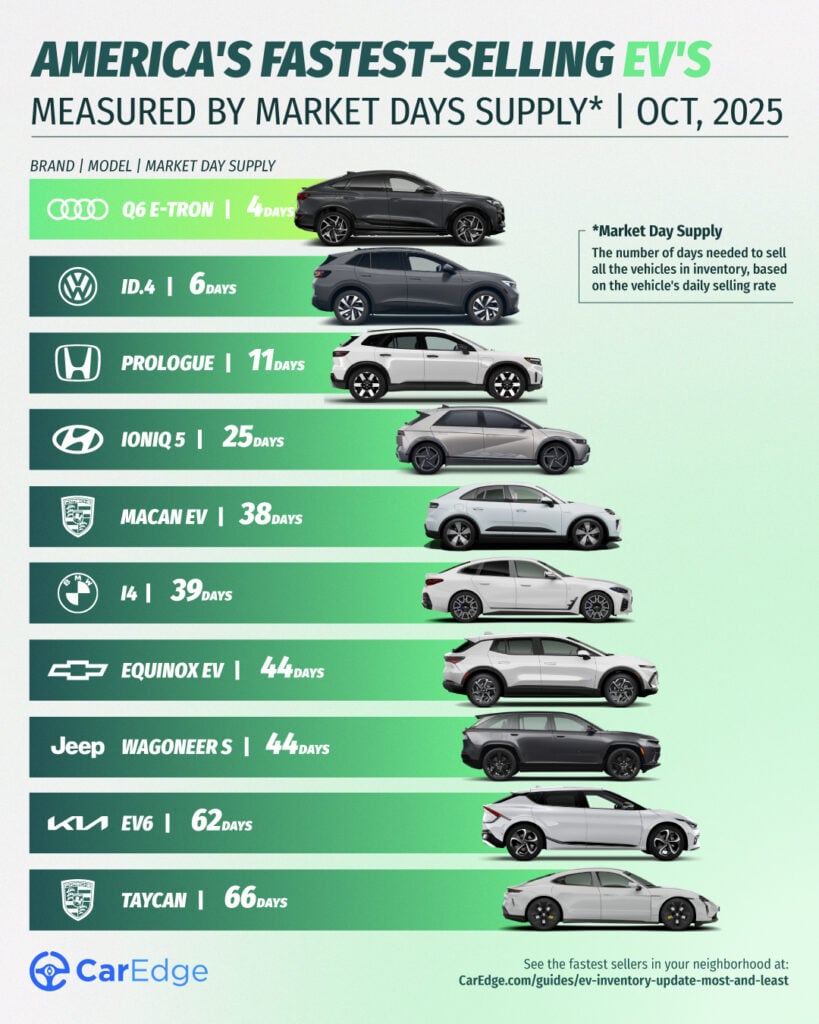

Last month, EVs were flying off dealer lots in the last days of the federal tax credit. Now, in October, the market is adapting to a new reality without incentives. Knowing which models are moving quickly, and which are stagnant, can give you the upper hand.

We analyzed October 2025 car market data to find the EVs with the lowest and highest market day supply (MDS). MDS measures how many days it would take to sell through current inventory at the current sales pace. Here are the standouts in today’s EV market.

These are the EVs with the lowest market day supply as of October 2025. That means they’re in high demand right now, and likely harder to negotiate on due to limited availability.

| Make | Model | Market Day Supply | Total For Sale | 45-Day Sales | Average Selling Price |

|---|---|---|---|---|---|

| Audi | Q6 e-tron | 4 | 371 | 4,644 | $67,518 |

| Volkswagen | ID.4 | 6 | 756 | 5,351 | $47,481 |

| Honda | Prologue | 11 | 1,974 | 8,514 | $54,017 |

| Hyundai | IONIQ 5 | 25 | 5,604 | 9,967 | $51,650 |

| Porsche | Macan EV | 38 | 856 | 1,152 | $87,805 |

| BMW | i4 | 39 | 1,639 | 1,889 | $66,479 |

| Chevrolet | Equinox EV | 44 | 9,215 | 9,911 | $40,041 |

| Jeep | Wagoneer S | 44 | 1,444 | 1,554 | $59,543 |

| Kia | EV6 | 62 | 3,156 | 2,277 | $49,353 |

| Porsche | Taycan | 66 | 1,094 | 742 | $141,455 |

Source: CarEdge Pro

For the first time ever, the Audi Q6 e-tron is the fastest-selling EV in America. The Volkswagen ID.4 is in second place as the September rush lifted sales rates. VW Group has three models in the top 10 right now, which is far from usual. The Macan EV has been a hot seller for Porsche.

Mercedes-Benz, Chevrolet, and Hyundai also have models in the top 10. The Chevy Equinox EV and Hyundai IONIQ 5 are the best-selling electric cars outside of Tesla right now, at least in terms of total sold.

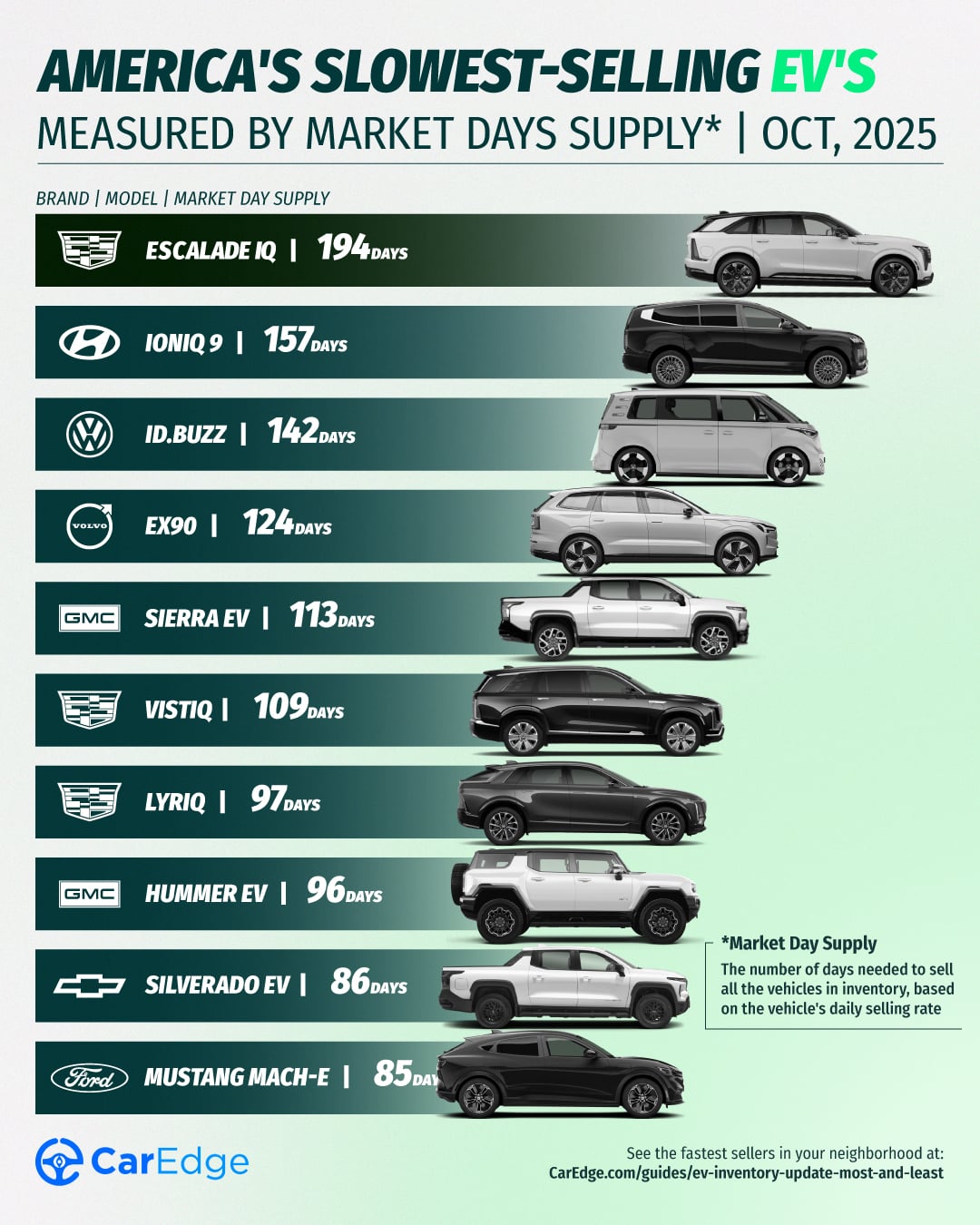

These EVs have the highest MDS, meaning they’re sitting unsold for far longer than average. Buyers may be able to score bigger discounts on these models — especially with CarEdge’s AI Negotiator doing the legwork for you.

| Make | Model | Market Day Supply | Total For Sale | 45-Day Sales | Average Selling Price |

|---|---|---|---|---|---|

| Cadillac | Escalade IQ | 194 | 3,639 | 844 | $142,724 |

| Hyundai | IONIQ 9 | 157 | 4,380 | 1,256 | $70,060 |

| Volkswagen | ID.BUZZ | 142 | 3,058 | 967 | $67,503 |

| Volvo | EX90 | 124 | 1,435 | 521 | $88,031 |

| Cadillac | Vistiq | 109 | 4,636 | 1,917 | $81,766 |

| Cadillac | Lyriq | 97 | 7,013 | 3,239 | $66,145 |

| GMC | Sierra EV | 113 | 3,914 | 1,555 | $87,106 |

| GMC | Hummer EV | 96 | 4,784 | 2,239 | $98,791 |

| Chevrolet | Silverado EV | 86 | 3,224 | 1,688 | $74,597 |

| Ford | Mustang Mach-E | 85 | 16,645 | 8,791 | $47,979 |

Source: CarEdge Pro

Cadillac’s Escalade IQ is the slowest-selling EV in America right now, with an eye-popping 194 days of supply. Luxury EVs dominate the slowest sellers, including the Volvo EX90 and Cadillac Vistiq.

Volkswagen’s ID.BUZZ has never been the hot seller that was once expected. Industry insiders suspect this is because of two things: high prices and slow charging compared to the competition.

The Ford Mustang Mach-E also finds itself here again, although sales have been picking up quickly. For buyers, these EVs are the most negotiable in October, but only if you know how to negotiate. Or, let AI negotiate for you.

If you’re chasing a deal, start your search with the slowest sellers. High inventory levels give you leverage, and dealers will be more motivated to talk price. Federal incentives are gone, so traditional car market dynamics will shape negotiability moving forward. Where supply far exceeds supply, you’ll always have more leverage.

Thinking about leasing? It’s worth considering. EVs tend to depreciate faster than gas-powered cars, and leasing can protect you from steep resale losses down the road. See depreciation forecasts for free with CarEdge’s Research Hub.

With CarEdge Concierge, our experts handle everything from finding available inventory to negotiating with dealers. Already know the exact EV you want? Use our first-ever AI Negotiator and let CarEdge AI negotiate with dealers anonymously on your behalf. It’s our most affordable car buying help ever!

You can also explore free tools like cost of ownership comparisons, car market updates, and our most popular free resource, downloadable negotiation cheat sheets. There’s no reason to shop unprepared in 2025.