CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

As a result of ongoing new vehicle production shortages, used cars, trucks, and SUVs are in high demand. This means that “rougher” and “edgier” used vehicles are making their way to dealership lots for sale to the public. One way to protect yourself from unknowingly purchasing a clunker is to look at a Carfax or AutoCheck vehicle history report.

Today we’re going to share a few stories from the CarEdge Community about AutoCheck and Carfax, and provide our recommendations for how you can protect yourself if you are buying a used car.

Let’s dive in.

Let’s start with the basics … How do these two companies work? AutoCheck and Carfax both operate in the same way; they source data from different places and compile that information into reports that are easy for a consumer to understand. With this in mind, it’s clear how the two companies compete. Who can get more (and better) data about a vehicle? That’s the challenge.

Become a FREE CarEdge MemberCarfax and AutoCheck both boast impressive lists of data partners on their websites. For example, Carfax says they have 112,000 data sources, while AutoCheck was developed by Experian and has access to all of their resources and relationships. Both companies provide compelling credentials as to why they are superior to the other. That being said, they both face the same issue: if data is not reported to them from one of their data partners, it will never show up on a report.

This brings us to the most important question of them all … Which is more reliable? Carfax or AutoCheck? We’ll answer this question by providing a few anecdotes from our experiences, as well as what we’ve heard from CarEdge Community members who have shared their stories with us in the community forum or via Live Chat with our Auto Advocates.

Sadly, this happens more frequently than we’d like. Take for example the case of Chris, a gentleman in Alaska who purchased a 2019 Ford Fusion from a local independent dealership.

Chris went to the dealership, took the Fusion for a test drive, reviewed the AutoCheck report that the dealer provided, and purchased his car. A few days later he took it to the local Ford dealership because a light came on in the dash. Within an hour, Chris had a sinking feeling in his stomach when a technician came to him and explained that his vehicle had been in a severe accident. Chris, unbeknownst to him, had bought a clunker.

How could that happen? The AutoCheck had been clean. In case it wasn’t obvious, this is why we always recommend getting a pre-purchase inspection completed on any used vehicle (even certified pre-owned). That being said, what was scary about Chris’ experience is that Carfax had different data than AutoCheck—they did report damage to the vehicle (but not an accident).

Let’s look at the two reports, and some photos of the vehicle before it was repaired.

As you can see on the AutoCheck report, the Fusion comes back “clean” and with an average AutoCheck score. Let’s look at the Carfax report.

As you can see on the Carfax report there are no accidents reported either, however there is a report of damage to the vehicle.

Right there on the Carfax report it says clearly “get the vehicle inspected before you buy.” Carfax knew about the damage, and AutoCheck didn’t. Chris obviously didn’t get the vehicle inspected, and he trusted the dealer who sold him the vehicle because they provided a “clean” AutoCheck.

Become a FREE CarEdge MemberDoes this mean AutoCheck is inferior to Carfax? We’ll let you be the judge …

We heard a similar story from a CarEdge Community member named Kristen.

Kristen had a nearly identical experience to Chris. She bought a vehicle (and even got the extended warranty), only to find out a few weeks later that it had previously been in not only one, but two accidents!

Does AutoCheck not collect as much information as Carfax? Based on some of our communities experiences, it appears that way.

I know we sound like a broken record, but getting a pre-purchase inspection is one of the best things you can do to protect yourself when buying a used vehicle. A pre-purchase inspection isn’t bullet-proof, but it certainly increases the likelihood of you avoiding a fate like Chris or Kristen.

Another trick you can use to get more information about a vehicle is to ask your insurance company to check the VIN in their systems. Insurance companies have databases similar to Carfax and AutoCheck that they can access on your behalf. Once you’ve found a vehicle you’re interested in, call your insurance company and ask them what info they have on the VIN. If it comes back clean on their end, then get the pre-purchase inspection.

In nearly every state, when you purchase a used vehicle you are purchasing it “as-is.” This means that no matter what condition the vehicle is, you are purchasing it as such. This doesn’t mean a dealership can sell you any clunker (vehicles have to pass state safety inspections to be sold), however it does mean that once they’ve sold you something it is entirely yours to deal with. The contract you signed stated it is being sold to you “as-is” and that the dealer cannot be held liable for the condition of the vehicle.

It is important that you understand the “as-is” concept, because your recourse post-purchase if something does go wrong is limited. If you’re like Chris or Kristen you have a few options to remediate the situation, however none are ideal. It is critically important that you understand you are purchasing the vehicle “as-is” and that you should be measured and pragmatic before signing the contract.

Currently, there is a global shortage of new cars, trucks, and SUVs. Manufacturers like Ford, GM, and many others have been struggling for months to supply their dealerships with enough new inventory to keep up with demand.

Market days supply, a metric that sales managers and industry executives track religiously, is at historic lows. Dealerships typically carry a 60 to 90 days supply of inventory. This means that if a dealership did not receive another vehicle, they would have enough inventory to meet demand for 60 to 90 days. To paint a picture of how dire the situation is, Subaru currently has an 8 day supply of inventory. 8 days.

Get market days supply data for your area for FREE. Run a Market Price Report NOW!

Why is there a lack of supply? Because of an ongoing semiconductor shortage that has plagued the automotive industry for all of 2021, and likely into 2022.

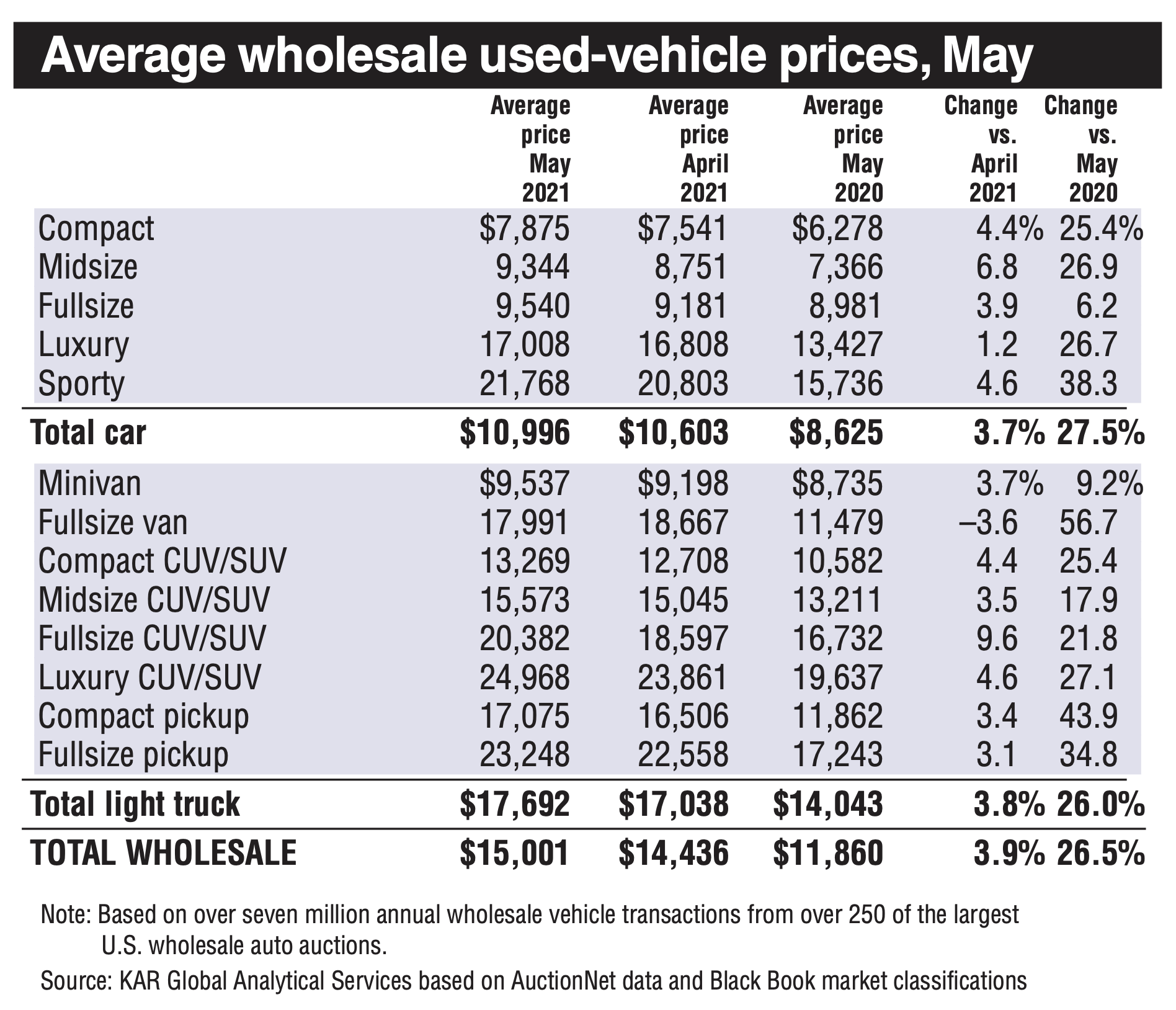

The “chip shortage” as many are referring to it, and the subsequent new vehicle shortage have had ripple effects across the entire automotive industry. With fewer new vehicles available for sale, used car prices have skyrocketed. Used vehicles are worth 25% more right now than they were at this exact same time last year. Considering a car is a depreciating asset, that’s not supposed to happen.

It’s fair to say that we’re currently experiencing a seller’s market of unprecedented magnitude. That being said, many people find themselves in a position where they need to buy a vehicle. In that case, there are a few things to be aware of in advance of signing on the dotted line of your buyer’s order.

As we’ve learned from CarEdge Community members who work in dealerships and financial institutions, lenders are still financing vehicle purchases, even as loan to value ratios are severely out of whack. What impact will consumers face once the bubble bursts? Let’s unpack exactly that.

Become a FREE CarEdge MemberWhen you buy a car it depreciates. The exception to this rule has been 2021, however we expect that once new vehicle production returns to normal, all vehicles will depreciate as per usual.

Before the chip shortage, a car buyer could expect their new vehicle to depreciate about 20% in their first year of ownership. For many owners who financed their purchase, this meant that they likely owed more on their loan than what the vehicle’s market value is after one year.

How so? Consider this scenario.

If you bought a $40,000 car and it depreciates 20%, it’s worth $32,000 after one year. Even though the vehicle selling price was $40,000, you likely financed more than $40,000. This is because the selling price of a vehicle isn’t the actual, or total price you pay. The total price is what we refer to as the out the door (OTD) price. The OTD price includes all fees, taxes, and accessories. When you finance a vehicle you finance the OTD price, PLUS any ancillary products you purchase in the finance office (unless you purchase them in full upfront).

Now the OTD price before you go to the dealership. Use the FREE OTD Calculator NOW!

That means your loan amount will be more than the $40,000 selling price (unless of course you plan to pay taxes and fees in cash, or make a substantial down payment). Every state and locale has different tax codes (we calculate those for you in our free OTD Price Calculator!), and dealer fees vary from state to state (we’re looking at you Florida), but a general rule of thumb is that your OTD price will be 10% higher than the selling price of the vehicle.

That $40,000 purchase is actually a $44,000 purchase, and unless you’re putting some serious cash down, you can quickly see how you’ll be in a negative equity position the moment you drive off the dealership’s lot. Your loan is for $44,000 (with zero down), and the value of the vehicle you are purchasing (new) is $40,000. You’re already in a $4,000 negative equity position.

What we described above is a typical negative equity situation consumers would face last year (pre-pandemic). Our concern is what will inevitably happen to consumers in 12, 24, or 36 months from now. Their negative equity position will be magnitudes greater than the example we just shared.

New vehicles are frequently selling for thousands of dollars over MSRP. Consumers are buying and financing thousands of dollars of “additional dealer markup” simply because of the supply shortage. In 2021, on a new Kia Telluride with $8,000 in additional dealer markup, you may have financed $54,000 on a $40,000 MSRP vehicle. That’s a serious negative equity position!

That being said, many lenders are not approving loans without significant cash down payments. Lenders need to abide by loan to value ratios that make sense based on your credit score and history. However, from everyone we’ve met with, lenders are still lending, and somehow consumers are manufacturing a large enough down payment to justify getting a loan approved.

Right now, at this very moment, the new Kia Telluride you just bought brand new might actually be worth MORE now that it’s a used vehicle (what a crazy time we are living in), however that is exactly the “bubble” we are talking about. Everyone knows that the Kia Telluride you just bought with $8,000 in additional dealer markup isn’t actually worth more used than it was new. That’s the craziness of our current supply/demand imbalance.

Become a FREE CarEdge MemberSo what happens in 24 months when that Kia Telluride price has normalized and it has deprecated the way we all expect it to? The owner who financed that purchase is going to be looking at a sobering reality, their Telluride will be worth considerably less than what they owe on their current loan. If they want to move into a different vehicle they’ll have a tough pill to swallow.

The same reality is playing out in the used car market. With used vehicle prices highly inflated, consumers are financing purchases on used cars and trucks that aren’t worth as much as they appear to be right now. The negative equity position they’ll be in will be staggering. The first impact of the “bubble bursting” will be the reality that millions of Americans will owe thousands of dollars more on their auto loans than what their vehicle is actually worth. This will have some interesting effects on vehicle sales in the near future.

Understanding GAP Insurance right now is very important! Read our FREE guide to GAP Insurance.

By now you are likely familiar with massive “online” car dealers like Carvana, Vroom, and Shift. Each of these companies has gone public over the past few years, and with valuations north of $50B, each has a lot of money to invest in growing their business.

What’s interesting about their business model (and Carmax’s too) is that they make most of their money not selling cars, but on selling loans, and ancillary products (extended warranties) tied to the purchase of a vehicle. To sell a loan or an extended warranty, you have to sell a car. Selling a car is actually really expensive. You have to find a vehicle to buy, recondition it so that it’s “showroom” ready, and then market it for sale.

Even with all that overhead, there is enough money in loans and extended warranties (and occasionally in the actual sale of the vehicle) that they make money (or at least make enough money to justify raising more capital from investors).

As used car prices have skyrocketed, we’ve seen an intensified bidding war amongst the deep pocketed publicly traded used car dealers. We’ve documented for months how Carvana, Carmax, Vroom, and Shift are paying incredibly high prices for used vehicles. Remember, if they don’t have inventory, they can’t make money, and if they can’t make money, their investors won’t be happy. It’s a vicious cycle.

What happens when the bubble bursts and used vehicle prices fall? Each of these dealers will be looking at their portfolio of hundreds of thousands of VERY expensive cars they paid for that are NOT worth what they paid for them. Depending on how quickly prices fall, each of these companies could be looking at hundreds of millions of dollars in inventory that is worth less than what they paid for it.

In a “post bubble burst” world we’ll be looking at quarterly reports from each of these companies that discuss how they’ll need to offload inventory at a loss to free up cash to be able to purchase new inventory at a lower price. This practice is called cost averaging, and it’s inevitable it will happen. The companies that don’t handle this well will certainly suffer, and as consumers we may be able to benefit from some sort of “fire sale” if/when it happens.

The third impact we see when the bubble bursts, is that there will likely be fewer in-market auto buyers. Like we discussed above, with expected negative equity positions to be very large, there will likely be a substantial number of buyers who take themselves out of the market when they realize that they owe thousands (if not tens of thousands) more on their current vehicle than what it is worth. We expect that many people will decide it makes more sense to hold onto their existing vehicle than “roll the negative equity” into a new loan and try to purchase another vehicle in 12, 24, or 36 months.

If you need to buy a car in this market, there are a few things you can do to protect yourself.

Become educated about the market situation. Reading this article will help you, and we also suggest you watch a few of our recent YouTube videos to get up to speed.

Be aware of your local market conditions. Although the supply shortage is global in scope, be sure to understand your local market conditions by running a Market Price Report.

Get support negotiating with the dealer/seller. Post your OTD worksheet to the CarEdge Community Forum, or live chat with our Auto Advocates On Demand. No matter what, get a second set of eyes to review your deal before you sign the dotted line.

Get pre-approved for financing instead of relying on the dealer!

Be patient! We’ve heard from dozens of community members that they’re still able to get fair deals right now. It takes patience and persistence. You’ve got this.

When it comes to buying a car, there are definitely no “magic words” that will convince a salesperson to give you an amazing deal, but there are a few phrases that can give you leverage in negotiations. Ready to learn how to negotiate with a car salesman? Great! Let’s get moving.

Car buyers with a vehicle to trade should get familiar saying “I’d like to discuss my trade-in later.” When selling and buying a car at the same time it is best to treat them as two separate transactions. A salesperson will always want to “work their magic” on the numbers and make it look like you’re getting a better deal than it is when you negotiate the trade-in and the new vehicle purchase price at once.

So keep it simple with one of the most vital car buyer negotiation phrases. Every time that the salesperson brings up your trade-in while you’re talking about the new car, remind them that you’d “like to discuss my trade-in later.”

Chances are that you may even need to come up with a few versions of this phrase, since the salesperson is likely to bring up the value of your trade-in more than once.

Learn how to get the most from your trade-in. Check out our guide of trading in your car and using it to your advantage.

The vehicle purchase process is terribly confusing. Here at CarEdge we strive to teach our members about all of the numbers involved in a car deal before they even contact a dealership so that they can stay in control of the process. One of the most vital (and obvious, albeit challenging!) numbers you should know, is the value of the car that you want to buy.

Unlike buying a refrigerator, a sofa, or literally any other item, buying a car entails hours of gamesmanship over what the “price” of the vehicle actually is. Be prepared to say “I know what the car is worth” to a salesperson, and feel confident that you actually do.

By the time you go to the dealership or begin email negotiations, you will have used the Market Price Report to know exactly how much you should be paying for your car. If you’re looking to buy a used vehicle, you will have run it through CarEdge’s Black Book vehicle valuation tool to get the same pricing information the dealer has, immediately leveling the playing field. The purpose of this phrase is to let the salesperson know that you’ve done your research and you know what you’re talking about.

I’ve said it before, and you’ll hear me say it again … You don’t want to act too eager when you are buying a car. “I like this vehicle, but I don’t love it,” is one of the important phrases you can say to a car salesman to keep control of the conversation. Your salesperson should know that you like the car and that you might buy it, but you’re not so in love with it that you’re going to pay more than it’s worth.

Don’t say this phrase and expect any response. Just say it during your test drive to show that you still need to be convinced that the value is right. It’s one of our car buyer negotiation phrases that’s somewhat subtle, yet important. It’s all about keeping your cards close to your chest.

As an added bonus, this phrase can be a good reminder to yourself that you should walk away if you don’t get a good deal. It’s easy to get caught up in the emotions of buying a car, but by repeating this phrase, you can stay in control of the negotiations.

Buying a car in 2021 is not easy! Check out our guide step-by-step guide here.

Are you buying a new vehicle, or are you factory ordering a car? Great, ask to see the invoice price. Having the dealer’s invoice will give you much more information that you can use during your negotiations. In fact, this is one of the most important phrases you should say to a car salesman. When you know the dealer’s invoice price, you’ll be able to propose a fair deal with a fair amount of markup.

More on how to get the dealer to give you their invoice here: https://caredge.com/guides/dealer-invoice/

There’s nothing that a salesperson wants to hear less than this phrase. They want to sell you a car today, not tomorrow. Most salespeople know that if you leave the lot, you might not return. They would prefer to keep you there, make you happy, and sell you a car. However, if you aren’t reaching the right numbers in your agreement, it might be time to leave.

You deserve to be treated properly and to get a fair deal on your vehicle. That’s why this is our top suggestion for buyer negotiation phrases: It gives you a chance to stand up for yourself and retain control of the negotiations.

Do you want to learn more about how to negotiate with a car salesman like a pro? We created our step-by-step car buying guide to coach you through the phases of buying a vehicle like a pro. Check it out here!

Updated September 22, 2021

One of the oldest pieces of wisdom that people have passed around about buying a car is that it’s always better to buy a used car. In fact, nearly 70% of Americans say they would consider buying a used car, according to Cision. Is this age-old wisdom always true when it comes to used vs. new cars? What about in a strange year like 2021?

Today, we’re going to take a look at several factors that influence the new vs. used car buying decision, including factors that are unique to 2021.

When we compare used vs. new car values, we’re comparing equivalent vehicles that vary primarily based on model year. We all know that a 10 year old car will cost less than a brand-new car, so we need to compare equivalents (the same make, model, and trim) to honestly address the question, “Should I buy a new or used car?”

We all know that 2020 and 2021 have presented the world with unique problems. One of these problems is a semiconductor shortage. Semiconductors, also referred to as integrated circuits, ICs, and “chips,” are used in nearly every electronic device, which means there is a generally constant (and increasing) demand for them.

When the pandemic hit in 2020, semiconductor manufacturers had to shut down and then re-open with new safety restrictions. Doing so hurt productivity, along with the productivity of the entire supply chain.

Since it takes so much time to produce a semiconductor, it has been a slow struggle to catch up to the demand that multiple industries are placing on chipmakers.

You may be interested in this deep dive on How We Ran out of Cars in the US.

The second issue is related to other inputs that are required to manufacture vehicles.

Earlier in 2021 there was a severe winter storm that hit Texas and knocked their power grid offline. This storm resulted in oil refineries halting production, including the production of byproducts. One of these byproducts is used in foam seats in cars. Because of this, many automakers were struggling to secure foam so that they can continue to produce new cars.

There was also a rubber shortage that effected automakers.

More recently, we’ve seen automaker struggle securing other raw materials, such as resins and steel.

All of these factors have made 2021 a unique year in which to purchase a car. Keep these factors in mind as we proceed to examine which is better value; new or used cars.

Let’s begin with the most important attribute: Value. What is the current value of the car that you’d like to buy? You must understand the current value to decide whether to buy new or used.

We recommend using our Market Price Report to help determine the value of the car that you’re after. Our report will compare actual sales prices from various dealerships in your area to determine what a fair price might be for the car.

Run a Market Price Report for the target car that you have in mind. The price that we suggest as a fair price isn’t the entire story. To understand the full price that you can expect to pay, you’ll need to click through to the website of the dealership selling the car. Read through their listing and look for any manufacturer or dealership incentives.

You may discover that there is a $3,500 rebate on your car or some sort of dealer incentive for financing that will impact the purchase price. There may even be credits or rebates that apply to certain people, such as first responders and members of the military.

Deduct the dealer incentives from the price that we’re telling you is fair and you’ll have a great idea about the current value of the car.

You’re not done yet! To truly compare apples to apples for a used vs. new car, run another Market Price Report for a used car variant of the same make and model. For example, if your new car was a 2021 Honda Accord, you might run a new report for a 2019 Honda Accord.

Do the same thing and click through to the dealership website. Notice how there are no added discounts, incentives, or credits? Used cars generally do not have any added discounts.

Also use the Valuation Report in the app to get a sense of what a dealer would charge for the used car. Check out our guide to the Black Book value, which is used by many dealers.

Now, you have an excellent idea about the true value of both new and used cars for the make and model you’re interested in. Even though you can now answer the question about which one is a better value, there’s much more to consider before you make your purchase.

The price that someone is asking for a car is hardly ever going to be the actual price that someone else pays, something that’s true for both new and used cars. As such, to truly answer the question at hand, you need to consider how much you can negotiate with the seller.

When you run a Market Price Report, you’ll see a negotiability score towards the top. This score is calculated based on how long the car has been on the lot as compared to the average in the region. If a car has been on the lot for 70 days and the average in the area is 20 days, you’ll likely have some great luck negotiating for that car.

As such, when you’re comparing new vs. used car values, you need to keep in mind how much you can potentially negotiate off of the vehicle. There’s always plenty of room to negotiate with a new car, but the attitude with used cars is often “the price is the price.” Keep this in mind as you determine whether to buy a new or used car.

Negotiating doesn’t just happen when you’re haggling down the MSRP, it also happens when you’re seeking financing. Speaking in generalities, you’ll receive better financing offers when you’re buying a new car, along with having more room to negotiate on those offers. Used cars are usually a bit more cut and dry.

What difference does a warranty make in the used vs. new car battle? Your new car is going to come with some type of warranty to protect you from manufacturer’s defects. It may even have another warranty for powertrain components. Additionally, the car will be in factory-perfect condition, so you won’t need to worry about a pre-purchase inspection.

On the other hand, a used car is going to have whatever may be left on the warranty from when the car was initially bought. In many situations, that means there will be no warranty or that you only have a year or two left. Plus, you’ll absolutely need a pre-purchased inspection to make sure that you have a solid understanding of its condition.

Should you buy new or used? How important is the warranty to you? If it’s vital, then new cars are the way to go.

You should do the leg work to determine whether a new or used car is better in your exact situation. Our tools will do most of the hard work for you, but you still need to use them to determine whether a new car is better than a used car for the make and model you’re investigating.

When it comes to 2021, our conclusion is that buying a new car is generally the way to go, due to the material shortages that are impacting the industry. These shortages have raised the prices for used cars, which are more in demand, although this may change as the year goes on. While you may not have as much room to negotiate with a new car, you’ll still find more value with a new car than with a used car that has a temporarily inflated price.

Anyone looking to buy a car, whether it’s used or new, will benefit from using our Market Price Report. You can run three searches for free, which allows you to compare cars and make your ultimate decision. Head on over to the Market Price Report and run one today!

Most people don’t look forward to buying a car. While the act of owning a new car is enjoyable enough that some people can power through it, it’s just not worth it to everyone. That’s where car brokers come in.

Car brokers can help you to navigate the automotive world on a personal level to help you buy your dream car. They can even help you to find a rare or specific vehicle.

Today, we’re going to examine what a car broker is, when you should use one, and how you can find a quality one.

What is a car broker? A car broker, also known as a car buying service, is basically a professional car buyer. The goal of a car broker is to level the playing field between you and the car dealership.

An auto broker is familiar with car dealership’s sales tactics, strategies for negotiating, and profit margins. They know how and where to save money throughout the entire process. They won’t fall for some of the numbers manipulations or specific strategies that might work on other customers. Instead, they’ll see these tactics coming and have a rebuttal already prepared.

Some auto brokers work for themselves or a small company, while others are part of a concierge service at a bank or credit union. An auto broker will often work for dealers and customers, helping to connect the two.

There are two ways that car brokers make their money: As a flat rate or as a percentage. An auto broker might charge everyone a flat rate, ranging from $200-$1,000. Other brokers opt to charge a percentage of the money that they saved you on your purchase. Expect to pay a retainer of approximately $100 once you decide to use an auto broker.

Car brokers can help to negotiate deals for new and used cars with dealerships.

Now that we’ve answered the question “what is a car broker,” we need to discuss the reasons that you should use one. People typically decide to use a car buying service to save time and money. Car brokers know exactly how to navigate the sales process to find any opportunities to save you money. You also won’t have to waste your time negotiating and spending hours at a dealership.

Other car buying services might be used when you’re looking for a rare or vintage car. Specialists hunt down these cars and buy them for their clients. This is a much more high-end service than the kind offered by the average car broker.

Using a car broker is similar to using a real estate agent. They help you to minimize mistakes and maximize your savings. For those looking to skip the whole car buying process altogether, this is a great way to go.

There are several things that you need to do when you want to hire a car buying service. You should begin by asking about options available through your favorite warehouse club store or the credit union that you bank with. Many types of brokers that offer car buying services may even have their fees included with your memberships.

If you don’t have a free option, it’s time to head online and look for a well-reviewed auto broker. Some attributes to look for are:

You will need to make sure that the auto broker is licensed to sell cars in your state and that they are able to abide by any other regulations that may apply to your specific transaction. Research any potential auto brokers on review-based sites to see how other customers have felt about working with them.

Want to get a better deal by yourself? Join CarEdge to get access to a suite of tools and information to help you get the best deal buying a car.

Deciding to work with an auto broker might well be worth your time. If you don’t care to learn the ins and outs of car buying in order to score a great deal, auto brokers are an excellent alternative. Keep in mind the requirements that we’ve outlined above and do plenty of research before deciding which one to work with.

Of course, if you want to learn how to negotiate and handle the work yourself, we’ve got a deal school that’s designed just for you.