CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

When it comes to the end of a car lease, you have a few different options for what you can do. To make the best choice possible, it’s important to understand a few factors that go into the different lease-end options you have at your disposal.

Deciding what to do at the end of a car lease depends mostly on how you feel about the car. Of course, your financial situation and inclinations also come into play. We’re about to explore each of the options available to you as your lease ends.

Looking for help with leasing a car at the best price? Let our team of expert Car Coaches take the hassle out of car buying and leasing. Here’s how we can help.

When you return your leased car, it will be thoroughly inspected, this is called the “lease-end inspection,” and it’s important to understand that you may be charged fees for excessive wear and tear to the vehicle. When you take your vehicle to the dealership they’ll be looking for:

Before you head for the dealership, you should ensure you have everything that came with the car to avoid additional fees. This means you’ll want to bring both sets of keys, make sure the spare tire is in the trunk, have the original floor mats in the vehicle, etc, etc.

If you plan to simply return the vehicle, you should also be prepared to pay the lease disposition fee, which is often around $400 (although the exact amount is on your lease contract). This fee is to cover the costs of reselling your leased car, and if you plan to return your vehicle (and not lease another vehicle from the same manufacturer) you cannot get out of paying this fee. If you went over your mileage allotment expect to get a bill sent to you, and if you’re terminating your lease before it’s over, expect even more fees (as well as the reality that you’ll still need to make your remaining lease payments).

Let’s say you want to return your car and then get a new lease. That is of course also an option, and one the dealership will be excited to help with. It’s likely that the dealership has contacted you in the months leading up to your lease-end to try and get you into a new lease already, and so by the time you show up to return your vehicle you may have already put together your new lease deal.

When you return a vehicle and then lease another from the same manufacturer they will waive the lease disposition fee. The vehicle you are returning will still need to go through a lease-end inspection, and you’ll face fees if you don’t have the second set of keys, or went over the allotted mileage.

You may be able to roll any lease equity over into a new lease as well. Lease equity is the positive equity created when your car is worth more than the residual value stated in your lease terms. Lease equity typically only occurs when you have severely under-driven the mileage stated on your lease, or when you simply get lucky because of an increased demand for your specific car.

For example, let’s say you lease a Honda Accord, and the stated residual value at the end of the term is $15,000. You lease it and barely drive it during the 36 month lease. You head to the dealership to return your current lease and move into a new Accord. When you arrive the dealership lets you know that the vehicle’s “book value” (how much they’re willing to buy it for) is $16,000. Rather than return the vehicle, you work with the dealer to buy it, trade it in, and roll over the equity ($1,000) into the new lease.

When leasing a car, many people decide to move into a new lease with the same dealership. While reasonable, you should shop around before jumping into another lease. Like we always preach, you should negotiate the largest dealer discount from MSRP before committing to a car deal.

If you’ve enjoyed your leased car you always have the option of buying it outright at the end of your lease. You know exactly how much you’re going to pay for the car (the residual value set when you signed the lease contract), and you know everything about the vehicle (since you’ve been driving it for the past few years).

The residual price is in your leasing contract and was determined based on their estimation of what your car would be worth at the end of the lease. Comparing the residual value against the current market value is often the deciding factor for people considering buying their leased car.

For example, John leases a Toyota Prius, and at the time the contracts are drawn up, the manufacturer calculates that the Prius will be worth 58% (residual values are always represented as percentages) of its original MSRP. That means John can buy his Prius outright, at the end of the lease for $17,000 (remember, this is a hypothetical). Because of market conditions, and the fact that John only put 18,000 miles on the Prius, he knows the vehicle is worth $20,000 if he sold it to a private party, or $18,500 if he sold it to the dealer. These figures mean John should almost certainly buy the car since it’s $1,500 cheaper than the market rate.

However, if John’s lease comes to an end and the book value on his Prius is actually $15,000, John would be paying an extra $2,000 over his Prius’ market value if he bought it outright at the end of the lease. In this case John would be better off turning in the leased Prius and buying one elsewhere for $15,000.

One of the most challenging decisions people face when considering what to do at the end of a car lease is often the same decision that originally led them to their lease: should you lease it or buy it?

There are pros and cons to both options. Objectively considering both will ultimately help you decide what to do at the end of a car lease.

People decide to buy cars at the end of their leases all the time. There are many good reasons why. However, there are also a few notable drawbacks.

Pro:

Cons:

Buying a car usually makes more financial sense than leasing a car. One benefit of purchasing the vehicle that you’ve been leasing is that you know exactly how it’s been driven and maintained, as compared to buying a used car off the lot.

Our Car Coaches are ready to help you determine which option is best for you. Our community saves thousands of dollars every day. Check out these uplifting success stories!

In case you missed it: Check out this 100% FREE car buying negotiation cheat sheet.

Some people are serial car leasers. They’d never want to commit to owning the same car for longer than a lease. Let’s take a look at some reasons why.

Pro:

Cons:

You may notice that these pros and cons lists are quite similar to the lists you might make before you first got into a lease. That’s because deciding what to do at the end of a car lease is similar to deciding to start a lease in the first place: lease a new car or buy the one you’ve been driving.

Deciding between the three lease end options detailed above can often be tricky. It typically comes down to how you feel about the car. If you love the way it drives and you want to keep driving it, buying it is usually the best option, even if the numbers say you should turn it in. Conversely, if you dislike driving it and you’ve been counting down the days, it’s probably best to turn it in and walk away.

Now you know what to do at the end of a car lease, but you still have homework to do. You need to determine the car’s current market value and compare it against the residual price. The difference between these numbers will help you decide what to do at the end of a car lease.

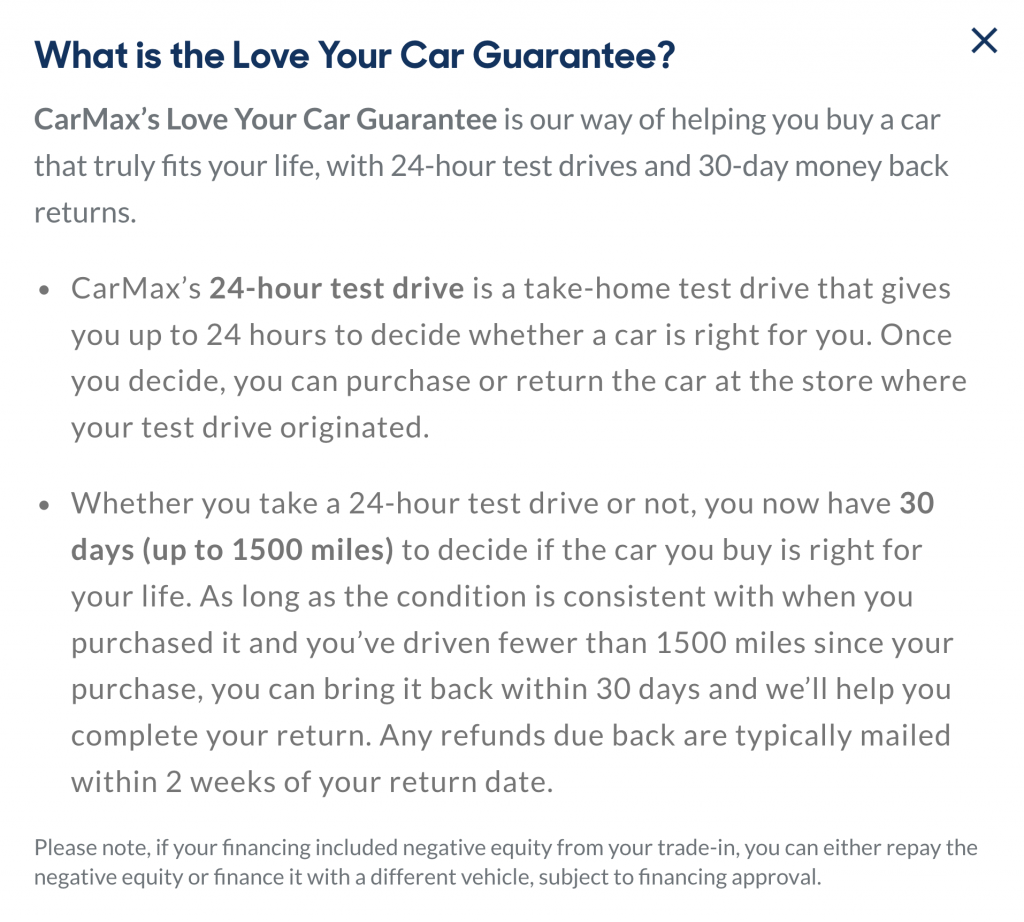

CarMax just announced a new program that is the first of its kind: The CarMax Love Your Car Guarantee. We scoured the Internet for every piece of information we could find on this new guarantee to put this post together for you.

In this CarMax Love Your Car Guarantee review, we’re going to break down exactly what’s in the program. Next, we’ll take it a bit further and compare this new program to their competitors. Lastly, we’ll discuss how you can negotiate with CarMax to get the best price for your car.

Get in…let’s go!

CarMax is the country’s largest retailer of used cars. They changed the game by being one of the first companies to introduce a “no haggle” experience when buying and selling used cars.

Now, the CarMax Love Your Car Guarantee program is set to bring about another change in the world of used cars. This recently announced program has two distinct features that consumers are going to love:

Both of these features are game-changers. Nobody else is offering anything close to these right now. It make buying a car from CarMax more tempting than ever before (someone at CarMax did their consumer research well).

The 24-hour test drive allows prospective car buyers to take a vehicle home, see if it fits into their garage, see how their child’s car seat fits, and get a general feel for the car before deciding if it’s right for them.

The 30-day money-back guarantee, offered as long as the car has 1,500 miles or less driven, provides peace of mind for weary car buyers. If you notice something that you didn’t catch during the 24-hour test drive or you simply change your mind, you can return it within 30 days to the same CarMax location. As far as this CarMax Love Your Car Guarantee review is concerned, this is revolutionary.

CarMax has had a money-back guarantee for years, but it’s only been for a period of seven days. Increasing the number to 30 days is a confidence inspiring move. It shows that they believe you’ll love the car you choose, and even if you don’t it’s not the end of the world.

These features come together to create an entirely different used car buying experience. We’re excited to see how the rest of the used car companies react to the CarMax Love Your Car Guarantee. We’re looking at you Carvana, Vroom, and Shift.

This CarMax Love Your Car Guarantee review wouldn’t be complete without comparing the program to their competitors.

Some automakers, including Cadillac and Buick, have 24-hour test drives available for their new vehicles. However, nobody else in the used car world is offering a 24-hour test drive. CarMax stands alone in letting customers take the vehicle home and try it on for size.

However, CarMax isn’t the only one in town offering a money-back guarantee. Here’s a snapshot of key competitor’s offerings:

As you can see, seven days has been the standard for years. As these app-based used car companies have popped up, they’ve mimicked CarMax’s offering. Now, CarMax has pulled ahead substantially.

We’re excited to see how these newer competitors react to the new CarMax Love Your Car Guarantee program. Will they copy it? Or maybe even surpass it? Only time will tell.

CarMax and all of their competitors promise a “no haggle” car buying process. While this might seem like a relaxing way to buy a vehicle, it can often work against you. We’ve previously talked in-depth about how you can still negotiate with “negotiation-free” car dealers, but it’s worth covering the main points in this CarMax Love Your Car Guarantee review.

There are three things that you can still negotiate with every “no haggle” used car dealer:

The dealership might approve you for a lower interest rate than what they actually offer you, and then pocket the difference if you agree. Negotiate with them to lower your interest rate; they don’t want to lose a car sale over the interest rate.

Did you know that you don’t have to buy an extended warranty when you purchase your car? This is also true for GAP insurance, tire and wheel protection, and anything else they offer you. You can buy them all from a third-party down the road and potentially save money. It might be better to decline their offers and just shop around later, but if you want to buy these extras from the dealership, make sure that you negotiate. The cost of all of these warranties is inflated to provide the dealership with a profit.

If you’re trading a vehicle in, negotiate how much they’ll give you for it. CarMax and other used car giants are always in need of fresh inventory…they want your car. They’d rather buy a car from you than a dealer auction where they don’t really know what they’re going to get. Let them know how much you can get from a private party and use that to drive up your trade-in value.

Keep these three areas in mind if you decide to do business with any of these used car giants that promise a “no haggle” process. You should never simply accept a number they give you…negotiate!

While we’re excited about the new CarMax Love Your Car Guarantee program, you should do your due diligence and read through the fine print for both the 24-hour test drive and the 30-day money-back guarantee. CarMax has not made sample contracts or agreements available online for their new program.

If everything is as good as it seems, this new CarMax program could shake up the world of used cars. We wouldn’t be surprised if Carvana and other competitors start coming out with new policies to try to keep up.

You just negotiated and agreed to a car deal. Congratulations! Now isn’t the time to put down your guard … As one sales process ends, another is about to begin.

You see, the F&I (finance and insurance) office is where the real money is made in a car dealership. It’s where an F&I manager will offer you all sorts of additional products to go along with your new vehicle. In today’s modern F&I office there are dozens of products you can buy, and to convince you to buy them, savvy F&I managers use what is called menu selling.

What exactly is F&I menu selling? How should you handle it? And what should you know before you step foot in an F&I office?

Don’t worry, we’ve got you covered. CarEdge is dedicated to arming you with all of the information that you need to get the best deal possible (both on the front-end, and on the back-end of your car deal).

Let’s break down exactly what an F&I menu is, discuss why it’s in use, and teach you how to handle it. The next time you walk into the car dealership, you’ll be ready.

After you’ve negotiated your car deal, you’ll meet the F&I Manager. Sometimes you’ll meet the F&I Manager when you’re still completing your car deal with your salesperson, but nine times out of ten, you’ll meet them once you step foot in their office. You’ll exchange some pleasantries as you acclimate, then they’ll pull out the menu. That’s right, a menu. It will have four or five columns, each with different types of coverage and protection. At the bottom of each column is a display price for your projected monthly payment.

The menu can either be physical (like a menu you would see at a dinner), or digital (typically pulled up on either an iPad, or a giant screen on the F&I Managers desk).

The finance manager will go over each column, discussing the different levels of coverage available in each program, and give you the total monthly price for each package. Note that it’s the monthly price, but more on that later.

You’ll then be asked which level of protection is right for you. Nowhere on the menu is there an option to have no coverage; you’ll have to ask for that on your own.

This entire concept is known as menu selling. It’s a simplistic way to get you to buy an extended warranty, tire and wheel protection, dent and ding coverage, etc, etc. The entire concept is based on the notion that if you give people a list of options, they’ll feel compelled to pick at least one of them, and when you frame it as “this protection only increases your monthly payment by $15 per month,” it becomes increasingly difficult (as a customer) to say “no.”

Don’t fall for it. It’s fine if you want added coverage for your new car, but don’t let this psychological trick be the reason you purchase. F&I menu selling isn’t an unethical car dealer practice, but it’s certainly a tactic you’ll run into. Simply be prepared.

And, as always we do offer transparent pricing for CarEdge members on vehicle service contracts, so if you are interested in buying an “extended warranty” get a “cost plus” quote from us to price shop with. More on that here: https://caredge.com/extended-warranty/

Way back in the day it wasn’t uncommon for F&I products (like extended warranties) to get “slipped in” to a customer’s car deal, even if they weren’t disclosed. Those days are fortunately long gone (thanks to several lawsuits), and nowadays “disclosure” is a primary concern for the F&I Manager.

All F&I products need to be presented to every customer, and the customer must specifically decline the coverage being offered. If the customer declines, they’ll have to sign something that says they declined. This policy prevents finance managers from selling you something you don’t even know about, but at the same time, it opens up entirely new sales opportunities.

For a while, F&I Managers would simply tell you about the different levels of protection. Then, some revolutionaries came up with the idea of “The Menu”. It caught on like wildfire, and it’s now standard practice in car dealerships around the country. Our favorite implementation of the “menu” is the docuPAD, a giant tablet that sits on a F&I Managers desk. It looks a little silly, doesn’t it?

What do you do when you’re greeted with the F&I menu?

The first thing that any reputable F&I Manager will go over is your base payment, without any added coverage. They’ll also show you the APR and the term length of your loan (if you’re financing). You need to initial next to all three to indicate that you received those specific terms.

If you would like to decline all options, make that clear. Say that you’re ready to sign the disclosure and that you will not be buying any further coverage. Be firm and confident. Be prepared to walk out on the entire deal if they push you on trying to buy coverage that you don’t want. This is especially important if the F&I Manager says anything along the lines of “You know we can lower your interest rate by a point if you buy the extended warranty …” Not only is this illegal, it’s a sign that this is a dealership you shouldn’t do business with!

Of course, you might actually want some of the options on the menu, and this is where it gets tricky. You’ll need to understand the full price of the products, not just their impact on your monthly payment.

The way that they convey the price is in terms of how it will impact your monthly payment. They’ll say that you’re going to pay nothing today, it’s all bundled into the payment, and it’ll only increase by X amount. Those are all sales tactics.

Here’s what you do: ask for the total cost of the product you’re interested in. Don’t accept the standard “it’s only $15 per month” answer. You need a full dollar amount. Most F&I Managers won’t have an issue providing you the total figure, it may simply take some poking and prodding. Once you get the price, know that you can cross shop at other dealerships, online companies, and even here at CarEdge. Whatever you do, don’t fall prey to the idea that you can’t negotiate on F&I products. Just like your car deal, the products in the F&I office are negotiable.

F&I menu selling prays on payment buyers. A payment buyer is a term for anyone who buys their car based on their monthly payment. There’s nothing wrong with this, and it’s a perfectly reasonable way to think about car buying.

However, the issue with F&I menu selling is that it takes advantage of payment buyers by squeezing options into the monthly payment, then downplaying their cost.

The best way to protect yourself against F&I menu selling is to focus on the out-the-door (OTD) price. The OTD price is the total figure that includes everything you’ll be paying for, including extended warranties and other options. It’s really the best way to know how much you’re actually paying for a car. You will have negotiated the OTD price with your salesperson, and now you’ll do it again with the F&I Manager.

Conceptualizing your car buying experience as a single number, instead of a series of monthly payments, helps you understand the impact of menu selling. Sure, $15 per month seems reasonable. Stretched over a long enough term, that can be $2,000 added to the price of your car.

Here’s a general rule of thumb: if there’s a tax applied to it, you can negotiate it. Everything else cannot be negotiated. Guess what’s taxed? Every option on the menu, and every other service the F&I office presents you with.

If you do want something that’s being offered, get them to go lower on price. Finance Managers have a complex commission structures, but in the simplest terms, most are rewarded for moving a volume of products, even if they aren’t the most profitable. This means the F&I Manager is motivated to move their products so that they get paid more.

You can use this to your advantage by asking for a discount. Say that the payment option on the menu is too much, but you’re interested in the coverage. Be clear that you don’t want to extend your payment term, but you want a lower monthly payment.

You might be surprised by how flexible finance managers can be. The key is to use the same trick for declining coverage overall, projecting confidence and staying firm.

F&I menu selling is so prevalent that we can almost guarantee you’ll be seeing it the next time you buy a car. Ever since its creation, it’s been a massive profit generator for car dealerships. By packaging everything into options and just tacking it onto your monthly payment, more and more car buyers are susceptible to saying “yes,” when in reality they aren’t 100% sure what they’ve bought.

Menu selling isn’t “good or bad,” it’s simply a function of buying a car. Our hope is that when you experience it you’ll be more informed and confident as a result of taking the time to read this page.

Misdirection is the secret to every magic trick ever created. It’s also the secret to the smoothest tricks performed by car salespeople. One classic old-school dealer close is called the 4-square close. It’s a specific type of close that’s been used for decades and is still employed by salespeople in car dealerships around the country.

Here at CarEdge, our mission is to provide you with the quality education and information that you need to secure a reliable car at a fair price. Today, we’re going to dissect this old-school dealer close and show you how to make it work in your favor.

Let CarEdge help you buy your next car! It’s like Honey, but for buying cars, trucks, and SUVs. Sign Up For Free

If you prefer to watch instead of read, simply click on the video above.

Imagine you’re at the dealership to buy a new car, and the car salesperson comes back from the sales manager’s office to the cubicle she left you in. She’s holding a folded piece of paper and has a smile on her face. She says something about how the sales manager must be in a good mood, and she unfolds the paper as if it holds the secret to happiness.

What she shows you are four squares drawn on the paper. You’re about to experience the 4-square — a tried-and-true old school dealer close. Above the four squares you’ll see your name, the vehicle you’re interested in purchasing, and its MSRP. Below are four squares that are the foundation of this close. Those squares are:

She’ll break down each square, saying they’re giving you a great sale by reducing the MSRP. She’ll move on to the trade-in square and say you’re getting a great deal there, too. Then she goes over to the cash down, and say you “only” have to pay that amount. Finally, she then goes over to the payment ranges, there’s typically three of them, and she’ll tell you what they are.

After that, she closes: “Which payment range works best for you?” That’s the conclusion of this old school dealer close. She’s hoping that you simply pick a payment range and you proceed to the next step in the car buying process.

However, you’re probably not going to be happy with every number she presents to you (at least you shouldn’t be!) You’re going to go through the squares, one by one, and say you want better figures (a lower selling price, more for your trade, etc). She might discount the car a little more or up the trade-in value, but the two squares that she really manipulates are the cash down amount and payment ranges. She’ll say something like “it’s just math” as she changes numbers around to suit your requests.

The car salesperson might decrease what you put down, then increase your payment amount, then stretch the payment term. As you negotiate, she’ll keep moving numbers around (probably after multiple trips to the “manager’s office” to get approval) until you are satisfied with your payment amount, the term, and the money down. When that happens, she has successfully closed, and you move on to the next phase.

This entire process is misdirection. The car salesperson is focusing on cash down and payment terms while neglecting the other two boxes, trade-in value and sale price.

It’s a smooth old school dealer close. Unaware buyers fall for it time and time again, which is why it’s still in use. We’d love to see this old school dealer close fade away into obscurity, but that will take a well-educated public.

What can you do to counter this close? Can you avoid it altogether, or perhaps even put it to work for you?

Most car buyers are only interested in how much they are going to pay every month and how much they are going to have to put down. It makes sense since those are the numbers that have a direct impact on their bank account. You hear us talk about it all the time, we shouldn’t be payment shoppers, but naturally, most of us are. It’s okay, you simply need to be informed when you make your buying decisions.

However, focusing on those numbers writes a blank check for dealerships, as they can massage these two numbers to boost their profits. It’s why they use the 4-square close to keep you focused on money down and the payment amount.

Here’s what you do instead: you keep changing the focus to the other two boxes. You keep saying you want more off of MSRP, and you want more for your trade-in. Stand firm in your choice and say that you know they can do better.

Or, we can even take it further.

Take the pen from the car salesperson and add a new box, and label it OTD. That stands for out-the-door, and that’s the real figure you focus on. How much is that car going to cost you, total, to drive off the lot?

You want a grand total that factors in every expense (taxes, title, tags, fees, etc.) and is the absolute final number. You tell them they can keep reducing the sale price and boosting the trade-in value until you both agree on an OTD amount. These will be tough negotiations, but you’ll need to remain firm to secure the OTD price you’re after.

Once you have an agreeable OTD amount, then you can talk about the other boxes. You can discuss how much you need to put down and your monthly payment amount.

It’s vital to understand that these figures are secondary. Many people who focus solely on their monthly payments don’t even know how much the car ends up costing them. You don’t want to be in that situation; you want to walk away knowing you got a fair deal.

You should also make it clear that you want a specific monthly payment, and you only want to put a certain amount of money down. Don’t let them still manipulate these numbers, because they’ll try. Once you’ve agreed on an OTD price, you make sure they match what you want to put down and the payment terms you’re after, especially when you get back into the F&I office.

We’ll be honest; it will be difficult to enact the above plan. Car salespeople are trained to keep the focus on the two squares that make them money. Shifting focus back to the sale price and the trade-in value will be a challenge. Getting them to agree on an OTD amount will be even more difficult. You’ll have to employ every negotiation tactic in your toolbelt, but it’ll be worth it. You’ll avoid getting taken advantage of at the dealership, and like we always say, you can (and should) treat your trade-in as a separate transaction, that way you can focus on getting a fair OTD instead of getting confused between the sale of your vehicle and the purchase of a new one.

Something you must remember is that you are always in control when buying a car. If the salesperson and sales manager won’t work with you on an OTD amount, or you don’t like what they offer you, walk away. You can say something like, “these figures don’t work for me,” and excuse yourself. Anything other than a firm and confident “no” will open the door for overcoming more objections. That’s what they’re trained to do, and you can bet they’ll do it.

If they keep pushing, make it clear that the numbers aren’t what you have in mind, so you’re going to leave and find another dealership. You should always have the mindset that you have nothing to lose by walking away. This is why we always say the best time to buy a car is when you don’t need to, since it allows you the comfort of knowing you can walk away.

You might discover that the dealership is actually more willing to work with you if you’re about to leave. Or they won’t, and you’ll leave and move on to the next dealership. Either way, you need to stand up for yourself and don’t let dealers take advantage of you with this classic old-school dealer close.

Over the years I’ve heard (or used) every old-school dealer close in the book. “Closes” range from the salesperson putting “soft” pressure on you while acting as your “friend” to more advanced tactics like the 4 square. There is a certain art to it (as there is in all sales), but it’s not the type of art most people like (especially not when they’re at a car dealership).

Our job at CarEdge is to help you be a more informed and educated car buyer. Today we’ll cover one of the more common “close” tactics called the 3 “m” close. Although it is a bit old-school a lot of dealerships still employ it, and unfortunately new people to the industry are learning it.

The 3 “m” close attempts to overcome the common objections that someone might have when they’re close to signing the dotted line, but aren’t quite ready. Today, I’ll walk you through exactly what’s going on with this close, how to spot it, and what to do about it. As always, if you don’t feel like reading, simply click play on the video above.

Let CarEdge help you buy your next car! It’s like Honey, but for buying cars, trucks, and SUVs. Sign Up For Free

You need to be ready to walk into the dealership with confidence, and my hope is this article will help. Let’s dive in.

The three “M” close comes into play when a salesperson hears a customer’s first objection, which is often “I need to think about it.” At that point, salespeople are trained to go into a maneuver like the 3 “M” close. You’ll hear something like, “Do we have the right machine picked out for you?”

When you hear this (or some variant of it), recognize what the salesperson is doing, they’re beginning to get into the 3 “M” close, and you just heard the first “M”; is it a problem with the “machine.” You could bet money that the following two M’s are next. This is a dealer favorite old-school close.

The goal of this M is simply to get to you to say that you like the car that’s been picked out and that it’s the right car for you. After all, if you like the car, then there’s some other issue that needs to be addressed. That’s the essence of this old-school dealer close: break down the three common barriers and seal the deal.

If you say it’s not the right car, then they’ll start showing you other vehicle options. If it’s an issue with the machine, your salesperson will act fast to find another vehicle on their lot that meets your needs, wants, and desires.

A decent salesperson will set up this M by saying something like, “Nobody wants to do business with someone that they don’t like, so am I the problem?”

It’s human nature not to want to hurt someone else’s feelings, so it’s almost a guarantee that you’ll say something along the lines of “No, of course you’re not the problem.” People usually want to avoid conflict, so it’s highly unlikely you’re going to say you don’t like your salesperson, even if you can’t stand them.

The car salesperson might even rope in other people that you’ve met from the dealership and say that everyone here would do anything to make sure you got in the right car. Everything said at this step is meant to set themselves up as your best friend who’s just trying to help you get into the right car.

Once they verify that they aren’t the problem, they’ll move on to what probably is the actual problem: the money.

The final M is typically where the actual objection is taking place. You might like the car, you might like the salesperson, but if the numbers don’t add up, you’ll have an objection to signing your vehicle purchase agreement.

At this stage, everyone is on the same page, and the salesperson knows that the money is the issue. Don’t be surprised when they still ask if it is, it’s all part of how they were trained. Once you confirm that the money is the problem, they’ll break down how it’s a good deal or possibly waive some fee that should’ve already been waived.

One tactic that we saw when this topic was brought up on our YouTube channel was pushing to let the customer take the car on an “extended test drive.” This is a bit of a gray area, but can be legitimate. Some dealerships do actually let you bring the car back if you don’t like it after a few days, but you absolutely need to have it in writing. If you don’t get it in writing, then you’re just buying the car. Of course, if you get in a car accident during your extended test drive, you’re the one on the hook, so at the end of the day, I’m not a big fan or proponent of taking a dealer up on this offer.

Another option is that they switch to another closing tactic that’s more specific to the money issue. The purpose of this old-school dealer close is to have you admit where the problem is so that they apply more pressure in that specific place. If it were a game of chess, the 3 “M” close is getting you to move your pawns out of the way so they can strike where it matters.

Whatever their next step is, you can be sure it’ll involve overcoming your objection about the price. They might pull up vAuto and show you that they’ve got the best price around. They might also break down the financial figures one more time to show that the financing agreement being offered is incredible.

Either way, you don’t want to buy that car. So, what can you do against this close?

One of the things customers say that leads into the 3 “M” close is the classic, “I need to think about it.” Dealers hear that countless times in their careers and the 3 “M” close is used to overcome this objection. Car salespeople are well aware that “I need to think about it” is often an attempt to get out of the dealership, and salespeople are wired to think “How can I close this deal now?”

Unfortunately, your attempt to leave is their attempt to close you. Their job is to help convince you to sign the paperwork today, not tomorrow, not next week, not in a month. That’s where the 3 “M” close comes in. In theory, every objection is dismantled, and you’ll drive away in your new car.

Here’s what you do. Memorize this line because it’s your way to avoid the entire close: “I’m not ready to make that decision.” Short, simple, and conveys all the information they need.

It’s a similar concept to “I need to think about it,” but it leaves less room for pushy sales tactics. If the car salesperson keeps pushing, repeat it. You can always get up and walk away. It’s better to face a temporary awkward situation than sign up for a car payment that’s just a bit too high, and trust me, it won’t be the first time in that salesperson’s career they’ve heard “no!”

Your absolute best weapon against this close is saying “no” at any point. You’re always free to say “no” and walk out of the dealership. Every car salesperson has heard no before, and they’ll hear it again. Don’t be afraid to make them hear it one more time if you’re not ready to sign the dotted line.

We firmly believe that arming you with information is the best way to prepare for the sales tactics that car dealerships employ. Not every dealership is going to roll out this old-school dealer close, but many will. Now that you’re ready for it, you should also be ready to say “no” and walk out.

It’s no surprise that working in the auto industry since the 70’s has yielded dozens of crazy stories. Zach asked me to gather together some of my craziest dealership stories in one place. You’ll hear some good ones, some bad ones, and they’re all a sneak peek into the life of working at a dealership.

Without further ado, let’s dive in.

Back in the late ’70s, we had a customer come to the Nissan dealership and go through the motions of buying a new car. When it came time to do a test drive, we took a photocopy of his ID, and he and the salesperson headed out. During the drive, the customer asked to make a stop at a 7/11 to pick something up.

It turns out what he wanted to “pick up” was all the cash out of the 7/11 cash registers. He planned to use our car as the getaway car for his robbery. The salesperson was an unwitting accomplice (don’t worry, the salesperson wasn’t charged), and the robber was arrested.

Back at the dealership, when the test drive had dragged on for longer than normal, we called the cops, and they were able to track down the robber and his unsuspecting accomplice. This is one of the many reasons why we take photocopies of driver’s licenses before test drives. In my 43 years of being in the car business, this experience might hold the top spot as one of the craziest dealership experiences I’ve ever had.

Much like the story above, I remember when I worked as a sales manager at singlepoint Pontiac dealership (yes those existed at one time), and a customer was going through the motions of looking to purchase a car. When it came time to test drive the car, he and the female sales associate disappeared. After being gone for 7 or 8 hours, there was cause for concern.

Let CarEdge help you buy your next car! It’s like Honey, but for buying cars, trucks, and SUVs. Sign Up For Free

Again, back at the dealership we called the cops (you’d be surprised how many 911 calls I had to make during the early days of my career), and fortunately the prospective customer (and kidnapper) came back with the car and our sales associate. When he arrived, the police were waiting, and he was charged with kidnapping. Thankfully, having a photocopy of the driver’s license helped the police bring a quick resolution to the kidnapping.

At our old Mini dealership, we carefully picked all of our test drive routes based on showing off how well the Minis handled. Many people buy Minis because of how fun they are to drive, so our job as a sales team was to expose prospective customers to that experience anytime they got behind the wheel. I was a sales manager at the dealership back in the early 2010’s, and I still remember the day I had to rush from my office to a backroad only a mile from the dealership to once again call 911.

A customer out on a test drive drove right into a tree. The car rolled and was totaled, and both the customer and the salesperson were rushed to the hospital. Fortunately, everyone survived, and miraculously the salesperson only missed a few days of work.

I remember the salesperson telling me that their last words right before the accident were, “You might wanna slow down here.” If only the customer had listened. I always hated it when prospective customers drove too aggressively on test drives. I didn’t like having my life put in jeopardy. This experience was a good example of why you need to be careful when test driving a new car.

Two mistakes were made in this next story: the salesperson said “yes,” and they didn’t take a photocopy of the customer’s ID.

This story took place at a Jaguar dealership, which is a car brand known for high-value cars. A customer came in one day and wanted to test drive a vehicle. He brought in a high-value vehicle to trade in. He said he wanted to take it home to show his wife, and he wanted to go alone.

This part is where our mistake happened. The salesperson agreed to it without even taking a copy of their license.

We never saw the customer again. It turns out the trade in vehicle was also stolen, and the Jaguar that was test-driven to “show his wife” was the next stolen vehicle.

Since there was no photocopy, there was nothing to give to the cops once the salesperson (and sales manager) realized what had happened.

Fortunately that experience didn’t happen to me, but the lesson was still learned: always get a copy of the ID every time.

This one didn’t happen at one of our dealerships, but it was a nearby dealership. There was a Mercedes-Benz dealership directly across from us when I worked at Acura North Scottsdale in Scottsdale, Arizona. All of the dealerships in the complex shared the same (or at least similar) test drive routes.

I still remember the day we saw a big smoke cloud on the not-too-distant horizon. It turns out; one of the driver’s test driving a new Mercedes-Benz AMG vehicle didn’t quite realize that the road had a sharp left coming up and kept driving straight directly into a storm drainage ditch. The car was totaled, but fortunately, nobody was injured.

How about a change of pace? Let’s talk about a positive experience from our time in the auto industry.

Back at the Mini dealership, we had an arrangement with a minor league baseball team (the York Revolution in York, PA) to showcase our cars. For about four years, we would caravan 50 or 60 Minis up to the stadium from Maryland every year. I negotiated with the Revolution that our caravan would drive around the field, and as a group we would enter from center field and drive around the warning track.

The crowd loved it, the sales staff loved it, the customers loved it.

It was one of the things we did that brought our staff and our customers together. It helped show them that we were people just like them, not con artists out to raid their bank accounts.

One thing that we loved about this experience was seeing people from all walks of life come together over one mutual interest: their love of their Mini.

Let’s finish up our craziest dealership stories with a few short positive stories.

Every year during Christmas at our Acura dealership, we would set up tables and all the necessary supplies to wrap gifts. We would invite sales staff, customers, and everyone’s families to come wrap presents for Toys for Tots. It was an excellent experience for us all, and it felt good to give back to the community.

When we were in Phoenix, we had regular BBQs for our customers. In reality, it ended up being for all the salespeople and their customers in the entire auto complex. We enjoyed providing a full spread of meats and sides for our fellow salespeople.

My last story is one of my favorites. One time, our dealership was selected as one of the top 30 best places to work in Phoenix. As they counted down and gave out awards to 30 small businesses around the Phoenix metro area, we wondered why they hadn’t gotten to us yet. As it turns out, they were saving us for last. We secured the number one spot as the best small business to work at in Phoenix, and the day of the announcement I was the one at the event representing Acura of North Scottsdale. I still remember getting up on stage to accept our award and not having a clue what to say. I was dumbfounded and proud at the same time!

Working in the auto industry for four decades has yielded plenty of stories. Much like any career, there are some excellent stories, some bad stories, and plenty that fell in between. I’m grateful for my time in the industry, especially now that I am able to help thousands of people from the other side of the desk.

If you’re buying a car, you’re probably wondering if you could shave a few dollars off of your monthly payment by removing GAP coverage from your bill of sale. Before you do, it’s very important to determine if you need the protection that GAP insurance offers. Luckily, this is pretty straightforward, at least compared to many other facets of car buying.

We’ll answer all these questions and more in today’s post. We’ll be taking a deep dive into GAP insurance to explain the ins and outs of this unique type of coverage.

GAP is an acronym that stands for Guaranteed Asset protection. GAP insurance is a type of insurance designed to provide car buyers with financial protection if you total your car, and owe more than it is worth. More specifically, GAP insurance makes up the difference between what the insurance company will pay you, and what you owe on your auto loan.

GAP insurance covers the difference between what your car is worth, and what your insurance company will pay if it is totaled. How does it work?

What GAP covers is best explained with a classic example. Let’s say you bought a brand-new Honda Civic for $20,000. You financed it and bought GAP insurance. The second you drive off the lot, you’re in a major accident that totals your car. Your insurance company pays you $15,000 for the totaled vehicle, but what about the remaining $5,000 that you owe? That’s where GAP insurance comes in. GAP insurance will cover the $5,000, plus it should (depending on your policy) cover any deductibles involved.

If you didn’t have GAP insurance, you’d be on the hook for the remaining $5,000. You’d still have to be making monthly payments for a vehicle that you don’t even have anymore.

GAP coverage is available for both used and new cars. Finance managers will try to sell it on all eligible vehicles. Fortunately, some lenders will directly state if a vehicle is eligible for GAP coverage. This prevents GAP from being sold when it’s absolutely not needed.

You should buy GAP insurance when you don’t have a lot of equity in the vehicle when you drive it off the lot. This situation happens when your trade-in wasn’t worth that much, or you simply didn’t put that much money down. So, if you’re wondering should I buy GAP insurance, you need to look at how much equity you’ve already put into the car.

A general rule of thumb is that you should have GAP coverage if you put less than $5,000 down on the car. Keep this in mind when you’re at the dealership, asking yourself, “should I buy GAP insurance?”

Of course, the above rule is not appropriate in every situation. If you buy a car for $60,000, this rule won’t apply. Why? It’s because the second you drive it off the lot it’s worth 20% less. Your $60,000 car is now worth $48,000. You would need to put $15,000 or more down to avoid needing GAP insurance.

So should you buy GAP insurance? It ultimately comes down to how much you’re financing compared to how much you put down.

Most leases include GAP coverage by default, so you typically don’t need to purchase it separately. However, some brands—such as Toyota, Mazda, and a handful of others—do not include GAP in their leases. If you’re leasing a vehicle, always check the contract to confirm whether GAP is included. If a dealer tries to add GAP coverage to a lease where it’s already included, that would be unethical.

The exact cost of GAP insurance depends on where you buy it, the price of the car, and the amount of your down payment. Typically, at a dealership, an F&I Manager will take a policy that costs them $250 and try to sell it to you for $980. That’s why you should always negotiate your GAP insurance costs; they’re likely just trying to boost profits.

Try to get them down to a price that’s around $500 or lower, or better yet, get a quote from your local bank or auto insurance company. Those policies can run as little as $100 or $200 if purchased from your existing insurance company.

If you buy GAP insurance at the dealership, the cost is added onto the amount that you’re financing. This means that it will boost your monthly payment, but it won’t be by much. If you paid $500 for GAP coverage and spread it out over a five-year loan, you’re looking at an increase of $8.30 per month (recognize this is a sales tactic the F&I Manager will use on you). Of course, the specifics will vary based on what you end up paying for the coverage and the length of your loan.

Anyone wondering if they should buy gap insurance should keep in mind that it’s relatively cheap compared to what you could be on the hook for without it.

GAP coverage is useful, but it’s not needed for the duration of your loan. Once you’re around halfway through the loan, assuming you didn’t pay any extra against the principle, you should cancel the GAP insurance. If you did pay extra against the principle, you should cancel even earlier.

To cancel your coverage, all you need to do is call the dealership and ask for it to be canceled. The pro-rated amount of what’s left will come off the principle of your loan. This won’t reduce your monthly payment, but it will reduce your total payoff amount.

When you buy a new car with GAP insurance, set a reminder in your phone to tell you when it’s time to cancel. You might not remember as the years go by, but your phone definitely will.

Not everyone will need coverage, but many will.

If you’re still wondering if you need GAP insurance, take a look at all the numbers involved. It all depends on how much equity you have in the car when you drive off the lot. You’ll need to take a look at your down payment or trade-in value to determine if you need GAP insurance. In many situations, it’s well worth having. However, if you have enough equity in the car when you buy it, you don’t need it, and you can save a big chunk of money.

FREE help: Car Buying Cheat Sheet – Former Dealer Shares How to Negotiate Car Prices Confidently

Here at CarEdge, we get a lot of emails from car buyers like you looking for advice on how to get the best car deal possible. The question “should I pay cash for a car?” Comes into our inbox daily. If you’ve managed to save up enough cash to buy a car, kudos to you. Now, it’s time to be strategic about how you use it to get the best car deal possible.

Most people assume that telling a car dealer that you’re paying in cash is a negotiating tactic and will get you a better price. Here’s the truth: it doesn’t. Saying that you’re paying with cash kills your negotiating power.

If you’re wondering, “should I pay cash for a car?” The answer is complicated. Yes, pay the full amount as soon as possible. But don’t walk in with a briefcase of cash and slam it on the salesperson’s desk.

To understand how to answer this question, we need to begin by looking at how dealerships make their money.

Car dealerships make about a quarter of their profit off car sales, yet vehicle sales make up about half of their revenue. That’s because of the slim front-end margins on most car deals (especially for new cars, used cars are a bit of a different story.)

You’ve heard me say it before, and you’ll hear me say it again—selling cars is merely a means to sell other products like finance options, insurance products, service, and parts.

Car dealerships make most of their money in the service department, but when it comes to vehicle sales, dealerships make their money in the Finance and Insurance (F&I) office. The F&I office is referred to as the “back-end” of a car deal. The “front-end” is what you spend time negotiating with the salesperson. The irony is that dealers are incentivized to sell as many cars as possible (frequently at a loss) simply to make money on the back-end (and from manufacturer incentives).

If you’ve ever bought a car before, you’ve heard a salesperson ask you “do you plan to finance the vehicle?” This is because if they know you plan to finance (and especially if you intend to finance through the dealership) they know the dealership can make money on the back-end of the car deal. Every car dealership out there will ask you to fill out a credit application so they can secure financing options for you. When they do this, they bake profit into the numbers. This practice is a significant source of profit for a car dealership.

So, if you walk in and say you’re paying with cash, you’re telling the salesperson that you’re going to eliminate the dealership’s primary source of profit.

What do you do? You take out a loan.

Let’s say you have all this cash, and you want to buy your car at the best possible price. It should be as simple as buying a meal at a restaurant, right? Unfortunately, that’s not the case.

You’ll pay far more for your car if you ask to pay for it all upfront with cash. That’s because the dealership will not be willing to negotiate as much on the front-end of the car deal since you will not become a sales opportunity for the back-end of the deal (aka in the F&I office).

So what should you do? Take out a loan through the dealership and pay it off immediately (or refinance it). Doing this will get you a much lower price than paying with cash at the dealership.

Like we discuss in depth in Deal School, you want to negotiate the out the door price of the vehicle with the salesperson. By informing them of your interest in financing your purchase through the dealership, you’ll find that the salesperson will be more likely to negotiate on the front-end of the deal.

One rule of thumb is that if it’s taxable, it’s negotiable. If a fee is not taxed, you can’t negotiate it down or away. It’s important to know exactly what you can negotiate.

Here’s the essential part of the entire process: make sure the loan does not have a prepayment penalty. If it does, walk away or ask for a different lending option. Fortunately, most loans do not have a prepayment penalty. Typically only exclusive financing options from captive lenders (the manufacturer’s lending institution) have these clauses.

It’s advisable not to tell the dealer that you plan to pay off or refinance the loan immediately. Dealerships incur “chargebacks” when this happens, so let this strategy be our little secret, and not something you blurt out to the F&I manager.

When you’re in the F&I office, decide if you want any of the ancillary products like an extended warranty, and then go through with the rest of the paperwork with the F&I manager. Once you’re happy with all the numbers, pay your down payment, sign the paperwork, and drive away.

You’ve got a brand-new car and a brand-new loan. It typically takes a lender about a week to put a new loan on the books once they receive it from the dealership. Wait about two weeks, then call your lender and ask for the payoff amount. They’ll tell you exactly how much you have to pay to end your loan. Send them a check or wire transfer, and you’re done.

If you don’t have enough cash to pay off your loan immediately, look to refinance the existing loan. However, if you took advantage of a rare zero-APR financing incentive, don’t expect to find anything better out there.

Remember that credit checks within a 30 days period for an auto-loan are grouped into one “hit” on your credit, so you don’t have to be too concerned about getting your credit run once again to find refinance opportunities.

You may have done it by way of a loan, but this is the best way to use your cash to buy a car. If you skip the loan and pay for the car entirely in cash, you’ll end up paying far more than if you take out a loan and pay it off early.

Now that we’ve unveiled our master plan for how to use your cash most effectively to buy a car, we should take a step back and ask if it’s a good idea in the first place.

If you’re asking “should I pay cash for a car,” we’re assuming you have a hefty savings account and financial portfolio. However, if paying cash for a vehicle will drain your savings completely, it might make more sense to finance the loan and put a large amount down for your down payment.

It’s also worth shopping around for different financing offers. No matter what, we always recommend having a pre-approval from an outside financial institution before you go to the dealership so that you have leverage when you are in the F&I office. In some cases, captive lenders offer special financing offers (like 0% APR) that no outside lender can beat. In those cases, financing through the dealership is the only logical option.

Since you now know paying for a car with cash won’t get you a better deal, you might want to reconsider the entire idea. Is this the best use of your cash? If you still think it is, make sure you take out a loan and immediately pay it off instead.

It’s vital that you don’t tell the salesperson, sales manager, or F&I manager that you’re going to pay off the loan immediately. They really don’t want to incur the chargeback.

Instead, go through the motions of taking out a loan and simply pay it off a week later. With this strategy you’ll get the best car deal possible.

Infiniti is a brand known for quality and luxury, so how does their certified pre-owned program stack up to the rest? If you’re interested in buying an Infiniti certified pre-owned vehicle, you need to know the ins and outs of their program.

We are about to dive into the Infiniti certified pre-owned program and discuss their complicated warranty, inspection process, and go over their perks.

TLDR; The warranty policy is needlessly complicated. There’s also no additional powertrain warranty on top of the standard warranty, although the powertrain is covered within this warranty. Ultimately, we like this program, but it has some severe drawbacks that we didn’t expect from Infiniti.

To become an Infiniti certified pre-owned vehicle, the car must meet the following criteria:

The vehicle must undergo and pass the 167-point inspection. If a car doesn’t score 100% on the inspection, it will not become certified.

Only one warranty is offered by Infinity, and that is their Certified Pre-Owned Warranty. This warranty only covers mechanical breakdowns caused by parts not functioning as intended, which you could also call manufacturer defects. Their documentation explicitly states that the following are not covered:

All of these conditions are standard for a CPO warranty, and there’s nothing out of the ordinary.

The Infiniti Certified Pre-Owned warranty covers most components in your vehicle, including the powertrain. That’s why they don’t offer a separate powertrain warranty; they decided to cover both with the same warranty.

Get the information & insights dealers don’t want you to have! It’s like Honey, but for buying cars, trucks, and SUVs. Sign Up For Free

Infiniti does offer an extended protection warranty that can be purchased to enhance coverage and extend the warranty. This extended warranty adds coverage for 352 components, which you can view on their website.

It’s worth noting that their website does not make mention of any deductibles. They also don’t discuss the transferability of the warranty. Both of these pieces of information are vital when discussing a CPO warranty. Most automakers, such as Audi, explicitly state if there will be a deductible for covered repairs.

The Certified Pre-Owned Warranty has three different durations for the same warranty based on the age and mileage of the CPO vehicle that you’ve purchased:

Doesn’t that seem needlessly complicated? It’s almost as if they created this policy to confuse buyers. It looks like the best choice is option number 2, more than 15,000 miles but less than 48 months from being sold. With this warranty, you’ll have an additional four years of coverage with no mileage restrictions.

Ultimately, you’ll need to keep this complex coverage system in mind when making your purchase decision.

Every Infiniti must pass a 167-point inspection to be sold as an Infiniti certified pre-owned vehicle. Infiniti has made their complete checklist available on their website, but we’ll cover the main points below:

This inspection is precisely what we’d expect from Infiniti, a brand known for being luxurious and of the utmost quality. It seems like they do their best to ensure that every vehicle in their CPO program will last for decades.

Every automaker with a CPO program includes various perks to persuade people into buying from them. Infiniti has many perks in their CPO program as well:

These perks seem like the bare minimum for a brand like Infiniti. While these perks are more tempting than perks offered by some other automakers, Infiniti should certainly be doing more to entice people to buy one of their CPO vehicles.

We like Infiniti’s certified pre-owned program. However, we are not a fan of their complex warranty coverage policy based on mileage and the time since it was sold. It seems needlessly complicated. Plus, there’s no additional powertrain warranty, even though the powertrain is covered in the included warranty. Aside from these issues, the inspection appears to be thorough, which is arguably the most crucial part of a program. Still, make sure you have an independent mechanic perform a pre-purchase inspection to verify that you’re buying a quality vehicle.

To some, Porsche is the epitome of luxury and quality. While that’s an arguable perspective, we can’t deny that Porsches provide a certain level of luxury to their car owners. If you’re a Porsche fan, going for a certified pre-owned vehicle might be an ideal way to get into one. You won’t be paying nearly as much as you would be buying a brand-new Porsche.

However, you should carefully consider the Porsche certified pre-owned program. We’re about to take a look at their warranty, inspection process, and evaluate the perks the program offers.

TLDR; We are far from impressed by the Porsche CPO program. They need to add a powertrain warranty that lasts for at least seven years. They also need to provide more thorough inspections. While their expanded roadside assistance is nice, we think it’d be more beneficial to have a better warranty.

To become a Porsche certified pre-owned vehicle, the car must meet the following criteria:

We’re surprised that Porsche is certifying vehicles that are up to 13 years old. That’s almost double what most automakers will certify. We suppose that means they have confidence in their cars.

Porsche provides a limited warranty for all Porsche certified pre-owned vehicles that covers:

That’s pretty comprehensive. However, to be covered, the issue must stem from a manufacturer defect. If the problem stems from misuse, an accident, neglect, or normal wear and tear, the repairs will not be covered under the CPO warranty.

The complete lack of a powertrain warranty is alarming. While the powertrain is covered in their CPO warranty, we’d prefer to see a separate powertrain warranty that lasts longer than the CPO warranty. This is done by many other automakers, such as Acura.

That exclusion list is relatively standard for CPO warranties. This warranty is intended to protect you from the manufacturer’s defects and not cover you for every issue you have with your vehicle.

Porsche states explicitly that there is no deductible for warranty repairs, which we love to see. They also specify that specifically trained technicians will do all repairs, and they’ll only use genuine Porsche parts.

The warranty that comes with every Porsche certified pre-owned vehicle will last for two years and unlimited miles. This CPO warranty goes into effect when the new vehicle warranty expires or when the CPO vehicle is purchased if there is no existing new vehicle warranty.

The Porsche CPO warranty lasts for two years with unlimited mileage, but there is not a separate warranty for powertrain coverage that’s included in the two years. This is far below the industry standard for powertrain warranties, which is typically ten years.

Get the information & insights dealers don’t want you to have! It’s like Honey, but for buying cars, trucks, and SUVs. Sign Up For Free

Porsche does not explicitly state that the warranty is transferable, although other websites claim that it is transferable. This is something to clarify before buying a Porsche certified pre-owned vehicle since a transferable warranty will significantly increase your resale value.

Porsche has a modest 111-point inspection. The average for most CPO programs is around 150, so Porsche is well under the industry standard. You can view the complete CPO inspection checklist online, but we’ll cover the main points below:

We’re surprised to see such a light inspection for Porsche, a brand known for quality. Perhaps their inspection is more thorough than the number of inspection points leads us to believe? Or maybe they aren’t that invested in their certified pre-owned program? It seems like having more inspection points is a great way to ease a customer’s worries about buying a CPO vehicle.

Porsche provides 24-hour roadside assistance for two years after buying a Porsche certified pre-owned vehicle. Porsche provides more robust roadside assistance than most automakers. It includes:

Porsche also provides trip interruption benefits if your vehicle breaks down due to warrantied issues more than 100 miles from your home. This coverage includes reimbursement for meals, lodging, car rentals, and alternate transportation. They do not specify a dollar limitation with this coverage.

We’re surprised to see that these are the only perks offered by Porsche. Most manufacturers have an entire list of perks, while Porsche only offers two bonuses. One of the main perks we’d like to see them add is rental car coverage for warrantied issues. Having to cover your rental when the problem is due to a manufacturer’s defect does not sit well with us.

Overall, we’re not impressed by Porsche’s certified pre-owned program. The warranty is not nearly long enough. They should either extend it or create a separate warranty that covers the powertrain. Another concern is their inspection. They aren’t inspecting as many points as most other automakers. We recommend getting a pre-purchase inspection for any Porsche certified pre-owned vehicle.

If you’re set on getting a Porsche, going certified pre-owned is an excellent way to go. However, if you’re looking for a reliable CPO vehicle, there are other programs with a better offering.