CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

You’ve heard us say it before, and you’ll hear us say it again; December is the best month to buy a new or used vehicle. End of year sales promotions are typically the most aggressive of the year, dealerships are determined to hit their month-end, quarter-end, and year-end volume-based sales objectives, and manufacturer’s budget their largest share of dollars to go towards December marketing activities. December is the best month to buy a car, truck, or SUV, but that doesn’t necessarily mean every “deal” on a dealers lot is a good one.

This year we commissioned our first ever CarEdge research project, the 2020 Negotiability Report. With our data partner MarketCheck, we analyzed nearly 2 million vehicle listing pages to determine which vehicles dealers should be desperate to sell in the ten largest cities, and Detroit (because if it has to do with automotive, then you have to include Detroit, it’s a rule).

The results were interesting. It’s incredibly clear that there is an oversupply of some vehicles in certain areas, while there is a lack of supply in others. Take for example in the Chicago, IL region. We found that half of the most negotiable new cars in Chicago are Audi’s. Could that have something to do with the fact that there are 7 Audi dealerships in the city, and maybe that is causing a bit of an oversupply? Sure. What does that mean for you if you’re in that area? Go get yourself a great deal on an Audi!

The methodology for this research project was simple. Just like we have a Negotiability Score in the CarEdge app, we calculated the same score across all vehicles in each of the eleven regions to determine what their score is. We then ranked the top ten for new and used in each region. If you’re unfamiliar with the Negotiability Score, it is a 0 to 100 score we assign to any vehicle identification number (VIN), and it is calculated by analyzing a vehicle’s “time on lot” (how long it has been listed for sale by a dealership), and the local area’s market days supply (an industry metric to determine how “in demand” a vehicle is).

To access the full report, please click here: https://caredge.com/negotiability-report-december-2020/

For links to each specific region, refer here:

New York: https://caredge.com/negotiability-report-december-2020/#Most_Negotiable_Vehicles_in_New_York

Los Angeles: https://caredge.com/negotiability-report-december-2020/#Most_Negotiable_Vehicles_in_Los_Angeles

Chicago: https://caredge.com/negotiability-report-december-2020/#Most_Negotiable_Vehicles_in_Chicago

Houston: https://caredge.com/negotiability-report-december-2020/#Most_Negotiable_Vehicles_in_Houston

Washington, DC: https://caredge.com/negotiability-report-december-2020/#Most_Negotiable_Vehicles_in_Washington_DC

Miami: https://caredge.com/negotiability-report-december-2020/#Most_Negotiable_Vehicles_in_Miami

Philadelphia: https://caredge.com/negotiability-report-december-2020/#Most_Negotiable_Vehicles_in_Philadelphia

Atlanta: https://caredge.com/negotiability-report-december-2020/#Most_Negotiable_Vehicles_in_Atlanta

Phoenix: https://caredge.com/negotiability-report-december-2020/#Most_Negotiable_Vehicles_in_Phoenix

Detroit: https://caredge.com/negotiability-report-december-2020/#Most_Negotiable_Vehicles_in_Detroit

Having bad credit, or no credit, and wanting to buy a car is not impossible. Depending on the rest of your financial situation, you can absolutely learn how to buy a car with no credit.

We’ll be focusing on the no credit or bad credit aspects of car buying in this article. For more comprehensive advice on car buying, please look over our in-depth case study that covers the general concepts involved in buying a car.

Are you ready to learn how to buy a car with no credit, or with bad credit? Let’s get started by really nailing down the definition of these terms.

No credit means you have no credit history. You have no credit profile because you’ve never established any sort of credit history. As far as the banks and lenders are concerned, you don’t exist.

Yet, here you are, trying to buy a car. You definitely exist. What do you do?

You’ll need to save up and put a ton of cash down. You’ll also need to have all your paperwork in order, along with having plenty of quality references. Keep reading – we’re about to cover all of this in detail.

Whereas no credit means you simply don’t have a credit history, bad credit means you do have a credit history, and it’s not good.

Bad credit, which is officially known as subprime, is a credit score that’s between 500 and 600. If you’re below 500, that’s considered super subprime and would also fit within the ‘bad credit’ label.

Having bad credit indicates to any potential lenders that you have not handled past loan obligations well. You might have taken out an auto loan and failed to make payments, or you took out a few credit cards and let them go into collections.

Either way, now you’re in a situation where it’s hard for finance managers at dealerships to convince lenders to approve you for a loan.

If your credit score is over 500, you might be able to find a lender who will loan 90% of the value of the car. That leaves you to cover 10%. If your score is below 500, they might cover 75% of the car, leaving you with 25%.

This means that you should start saving because you’re going to be expected to put more money down than someone with a higher credit score.

It’s worth noting that you should avoid visiting multiple dealerships to get approved by a lender. Doing so can harm your credit score by stacking up hard inquiries. In theory, when shopping for a similar item (a car) over 30 days, it counts as one credit inquiry. However, it’s truly unclear how the credit bureaus interpret multiple inquiries for subprime candidates.. Avoid multiple dealerships if at all possible and work with one or two.

Be realistic about the cars you are looking at. A bad credit score will decrease your buying power substantially, even if you are putting a good amount of cash down. Consider buying a certified pre-owned vehicle to get the most value out of your buying power.

Lastly, be ready to have a higher APR than what’s being advertised. For people with a subprime credit score, the average rate for a new car is 12.15%, and for a used car it’s 16.78%.

If you’re looking into how to buy a car with no credit, your first plan of action is to save up as much cash as possible. The more cash you’re able to put down, the better.

If you’re looking at a $10,000 car and you have $3,000 down, the finance manager has a great argument with the lender about why they should approve someone with no or bad credit: you don’t want to lose $3,000.

Conversely, if you have $300, the argument falls flat.

People who investigate how to buy a car with no credit often end up going to “buy here, pay here” car lots. Be warned, those types of places will require even more cash down than most dealerships. Essentially, the cash down amount that they require will cover their investment in the car. That way, if you stop paying the loan, at least they got out what they paid for the car.

Sidenote: If you’re going to work with a “buy here, pay here” lot, make sure they report your loan to credit bureaus.

Before you even visit the dealership, get all your paperwork in order. Anyone wanting to know how to buy a car with no credit should know that you’re going to have to prove that you have a job and stable personal finances. You should prepare:

All of this paperwork forms a well-rounded image of who you are, financially speaking. It helps lenders approve your request, even if you have no or bad credit.

Another way to go is to look for financing options outside of the dealership.

Joining a credit union is the best thing you can do if you’re looking at how to buy a car with no credit and want to look outside of the dealership for options. That’s because credit unions look at members with a more favorable eye than other lenders. You might be able to secure an auto loan with more favorable interest rates than if you went to the dealer, too.

Credit unions are easy to join. There are all types of credit unions, look for one in your area, and join up.

You’ve now learned that if you’re looking at how to buy a car with no credit, or bad credit, you still have options. Your lack of a credit profile, or your bad credit profile, doesn’t prevent you from owning a vehicle.

Save up for a large down payment, bring all your paperwork, and be ready to have a higher APR than advertised. You’ll be able to drive away from the lot happy.

Updated 9/29/21

Knowing how to sell your car for the most money possible has never been more important. In 2021 we’ve seen used car prices appreciate nearly 30%, which means the car (or truck, or SUV) in your driveway is worth way more than when you originally bought it. What a time to be alive!

If you decide that it’s time to sell your car, there are a few things we recommend you do to make the most money possible. Right now, with new car inventory at all-time lows, car dealers, consumers, and everyone in between will be interested in your used car for sale. To maximize your profits we have a few suggestions.

Let’s explore how you can sell your car and address some common questions, like “Should I get my car detailed before I sell it?” “Should I sell private party or to a dealer?” And, “How much is my car really worth?” Let’s dive in.

National online used car dealers like Carvana, Vroom, CarMax, and Shift have been growing in recent years. These companies are publicly traded and focused heavily on growth. Because of this, digital retailers are always purchasing more vehicles in order to continuously expand their inventory.

To sell your car for the highest price possible we recommend you start by getting free online quotes from these four major players. Their business models rely on them having vehicles to sell, and because of that they have made it very simple to sell them your car online. Getting a quote from Carvana takes less than five minutes and only requires your VIN and the current odometer reading.

Carvana, Vroom, CarMax, and Shift vary their prices by geographic region. We recommend you get quotes from each company to see who is offering the highest price right now. Each company wants a different “mix” of inventory and one of them will want your car the most.

Click here to get a Carvana quote: https://www.carvana.com/sell-my-car

Click here to get a Vroom quote: https://www.vroom.com/sell

Click here to get a CarMax quote: https://www.carmax.com/sell-my-car

Click here to get a Shift quote: https://shift.com/sell-my-car

From our experience, we’ve seen that Carvana and Vroom will typically pay the highest price for newer used vehicles. CarMax typically pays the most for older used vehicles. Shift occasionally tops them all.

Bear in mind that Vroom has recently been admonished by the Better Business Bureau, so if the quote you get from Carvana is within a few hundred dollars of your price from Vroom, you may simply want to go to Carvana.

Car dealers are notoroius for “lowballing” your trade-in. Well, in today’s market you are the one in control, and we recommend you give your local dealers a chance to buy your car from you.

Car dealerships are rapidly running out of inventory, and with Carvana, Vroom, Shift, and CarMax spending a lot of money to buy cars directly from consumers, local car dealers know they need to pony up some serious cash to do the same.

We recommend that you contact all of your local dealerships and share with them the quotes you received from the online digital used car dealers. To sell your car for the most money possible, you need leverage, and with online cash quotes, you have that.

If a dealership is willing to beat the price quote you have, that’s great! Your next concern is likely “will they change the price when I come in and they inspect the vehicle?” To mitigate issues there, watch this video on how car dealers appraise cars, and make them aware of any issues in advance.

We have heard a few horror stories from the online used car dealers that they revise their prices lower once they have inspected a vehicle, so the best thing you can do with them, or with your local dealer is to pre-empt that by telling them about any damage or issues.

After going through the prior two steps, if you are willing to invest more time in the process you’ll likely be able to sell your car for the most money possible to a private buyer. Unlike selling to a dealership, selling to a private party takes a bit more work, however an interested private buyer will likely pay even more than the dealership, because they know that if they don’t buy it from you, they’ll have to buy it at a marked up price from the dealership.

Thankfully, the work you did in the steps before (getting quotes from dealerships) will inform your asking price. We recommend you take the highest offer you received from one of the car dealers and add 10% on top of it. That is a fair listing price for a private party sale.

Why 10%? It’s simple:

Advertising a vehicle for sale right now has never been easier. There is A LOT of fraud on peer to peer websites, however. We recommend listing your vehicle on the classic websites: Facebook Marketplace and Craigslist.

In this market you will likely be receiving many inquires immediately.

If you’re selling your car to a private buyer we recommend you clean and detail it. If you are selling to a dealership there is no need to get the vehicle detailed, however it is a good idea to get the vehicle looking clean and like it has been well maintained.

If you’re selling a vehicle to a private buyer do not be surprised if they ask to see a CarFax report and to get a pre-purchase inspection.

When considering how to sell your car, be prepared to accommodate a PPI and have a vehicle history ready for potential purchasers to review.

Great, so you know how much your car is worth and you’re ready to sell it. You likely now wondering, “So what exactly do I need to sell my car?”

The following items will be useful in making your sales experience as smooth as possible:

If you’re selling to a dealership your experience will be pretty simple … Arrive, sign off on a variety of paperwork that allows the dealership to handle motor vehicle paperwork on your behalf, get your check, and leave.

If you’re selling to a private party it will look a little different.

Here are a few pointers:

Are there really “Black Friday car deals?” Each year it seems the Black Friday tradition has started earlier and earlier, with retailers having Black Friday promotions a week before Thanksgiving even happens. What happens this year amidst the global pandemic is anyone’s best guess.

That being said, automakers have tried for years to drum up sales during any holiday, and Black Friday is no exception. You don’t have to look too far to find automaker’s promoting their incentives and offers this holiday season.

This begs the question though, should you take one of these Black Friday car deals, or are you better off waiting until the end of the year to make your car purchase? 2020 is an atypical year for many reasons, and with new and used car prices swinging dramatically over the past few months, it is hard to say when prices will be best for car buyers.

When it comes to negotiating the best car deal possible, there are two major factors to consider; what manufacturer incentives are, and how likely the dealer is to negotiate on their inventory. If you’re thinking about getting a Black Friday car deal, then you need to understand how both are influenced at this time of year.

Within the automotive industry it is well known that end of year sales promotions are typically the strongest of the year. Why? Because most manufacturers are publicly traded companies, and they have to report their earnings quarterly to their shareholders. Even though a lot of manufacturers run on a “fiscal calendar” instead of the traditional calendar year, there is still a lot of weight put into “end of year” numbers, and inevitably thousands upon thousands of corporate employee bonuses are dependent on hitting certain targets.

As we’ve talked about in other guides here on the CarEdge website, automotive manufacturers are not afraid of a little fraud to hit their annual goals.

*cough cough* BMW *cough cough*

That being said, this isn’t the preferred path to hit sales figures, and believe it or not, automakers prefer to steeply discount their vehicles to sell them to consumers before they fake the fact that they were sold! Novel concept, eh?

Foureyes, a dealership sales enablement software company, has great insight into manufacturer specific discounting. If you visit this page (https://lps.foureyes.io/auto-pricing-trends) you’ll see original equipment manufacturer (OEM) specific discount percentages broken down by model year.

Our recommendation is that you look at this data daily as you’re actively navigating the car buying process. You may not qualify for all of the manufacturer’s incentives, however you can at least time your purchase to align with when they are most aggressive. For most OEMs that will be the end of the year, not Black Friday. The notion that there are Black Friday car deals is really more of a marketing gimmick than actuality.

When are car dealers most likely to negotiate a fair car deal? Black friday, or at the end of the year? The answer to this question is highly variable, and every dealership will be different, but as a rule of thumb, most car dealers will be more likely to negotiate with you on price at the end of the calendar year.

Read our complete guide on how to buy a car: How to Buy a Car: A Case Study

As we’ve talked about in other full-length guides, car dealerships don’t make the bulk of their money from selling cars; they make it from factory incentives when they hit volume goals. There is no time where manufacturer incentives mean more than at the end of the year. Dealership’s can have hundreds of thousands of dollars on the line come December 31st, and a few more car deals could push them over the edge to secure those bonuses.

That being said, dealerships have monthly incentives from their manufacturers as well, and those incentives certainly are in place during the month of November. That’s why it’s impossible to say for certain that every dealer will be more likely to negotiate on price in December vs. November—it depends on where they are in each month relative to their volume based incentives.

Want to make car buying easy? Let us do the hard stuff! It’s like Honey, but for buying cars, trucks, and SUVs. Sign Up For Free

With all that in mind, it is important to remember that the basics of negotiating a car deal do not change. If you’re looking to get the best price possible, you’ll want to focus your efforts on vehicles that have been sitting on dealer’s lots for a long time. Just remember that you can always use our Negotiability Score as a guide for which vehicles dealers are more and less likely to negotiate on.

The Market Price Report is 100% free, so please use that as you begin to navigate the car buying process.

This section of our Black Friday car deals guide is solely focused on manufacturer incentives. Like we discussed above, dealer discounts are going to be dependent on each individual dealership’s interest in negotiating with you. Again, that is primarily driven by how close they are to their monthly volume sales goal, and how long a specific vehicle has been on their lot.

When it comes to consumer incentives being offered by manufacturers, our friends at Find The Best Car Price have done a great job aggregating all of the different incentives in one place.

Many manufacturers, such as Kia, Mazda, Toyota, and more are still offering zero percent financing options. We strongly recommend that you consider these manufacturer financing incentives (if you qualify).

Aside from finance incentives, the manufacturer cash incentives are steep for some vehicles, but nothing too spectacular. If you’re in the market for a Nissan Leaf there are cash incentives up to $6,000. 2020 GMC Sierra 1500 has a $6,000 cash incentive as well, and if you’re in the market for a 2020 Chevy Bolt EV, there are $8,500 in cash incentives on the table.

We recently wrote about a CarEdge community member named Clark, who purchased his Jeep Wrangler a few weeks ago. Clark’s story is a great example of navigating the car buying process in 2020, and especially amidst the ongoing Coronavirus pandemic.

Yes, your focus may be on getting the best Black Friday car deals, however it’s important to be like Clark, and understand big-picture trends in the automotive industry before you step foot in a dealership (or more likely email them).

Because of the Coronavirus pandemic, used car inventory has been in short supply. If you tune in to our weekly show on YouTube, you know that used car prices have been sky high (but are finally coming back down), and that new car manufacturing was nearly eliminated earlier this year, leading to supply constraints at dealerships right now.

All that being said, know that “knowledge is power,” and that being knowledgeable about the market conditions (especially in 2020 when things are as crazy as they have been), can save you thousands of dollars when you eventually do go to buy your car.

Trust me, I know buying a car isn’t easy. Believe it or not, neither is selling a car. After doing it for 43 years, I can assure you that being on either side of a car deal isn’t the most pleasant experience either. This is in large part because of information asymmetry, meaning that the dealer has more information than the car buyer, and the car buyer has most likely been taken advantage of in the past by one dealer or another.

By now you know what our objective here at CarEdge is: we exist to support car buyers as they navigate the process. Today I wanted to share with you my best guess as to how much dealers make on new cars broken down by brand. These are estimates, and not facts. During my 43 year career I worked for a lot of OEMs (original equipment manufacturers, or brands), but not all of them. I don’t know every brands profit margins, but I do have a good sense of what they are for most.

Want to make car buying easy? Let us do the hard stuff! It’s like Honey, but for buying cars, trucks, and SUVs. Sign Up For Free

Keep in mind that profit margins are different by model and not just make. What do I mean? I mean that a Mercedes-Benz C300 is going to have less profit built into it’s MSRP than a G550. That being said, on average, my best guess is that Mercedes-Benz’ have eight percent profit built into the MSRP price. I hope that makes sense.

If you work for one of these manufacturer’s, or at a dealership and you have insight into how much profit is built into the MSRP price for each brand, please leave a comment below and we will update the table to reflect that. This is a “living” document, and should be used as a guide for your car buying process, not as fact. The only way to truly know how much a dealer is making when they sell a new car is to ask them. More on that can be found here.

If you haven’t already, be sure to use our FREE Market Price Report which contains a suggested offer price to help you begin negotiations with any dealer on any car.

Without further ado, let’s dive in!

Here’s about how much profit dealers make on new car sales:

| OEM | profit built into MSRP |

|---|---|

| Acura | 8.00% |

| Alfa Romeo | 8.00% |

| Audi | 8.00% |

| BMW | 8.00% |

| Bentley | 12.00% |

| Buick | 8.00% |

| Cadillac | 8.00% |

| Chevrolet | 8.00% |

| Chrysler | 7.00% |

| Dodge | 7.00% |

| Fiat | 5.00% |

| Ford | 8.00% |

| GMC | 8.00% |

| Genesis | 8.00% |

| Honda | 6.00% |

| Hyundai | 5.00% |

| Infiniti | 8.00% |

| Jaguar | 8.00% |

| Jeep | 6.00% |

| Kia | 5.00% |

| Land Rover | 8.00% |

| Lexus | 8.00% |

| Lincoln | 8.00% |

| Lotus | 7.00% |

| Maserati | 10.00% |

| Mazda | 6.00% |

| Mercedes-Benz | 8.00% |

| Mini | 6.00% |

| Mitsubishi | 5.00% |

| Nissan | 6.00% |

| Porsche | 8.00% |

| Ram | 8.00% |

| Subaru | 6.00% |

| Toyota | 6.00% |

| Volkswagen | 6.00% |

| Volvo | 8.00% |

Today Zach interviews Joel Milne, CEO of RepairSmith. Zach and Joel discuss the automotive repair industry, how RepairSmith helps their customers, and more. Listen to all Auto Insider podcast episodes here: https://caredge.com/topics/podcast/

Joel is a serial technology entrepreneur, with a love for building consumer-facing products. Joel previously co/founded four venture-backed technology startups and brings a lifetime of experience building and operating technology companies to RepairSmith.

Joel is a serial technology entrepreneur, with a love for building consumer-facing products. Joel previously co/founded four venture-backed technology startups and brings a lifetime of experience building and operating technology companies to RepairSmith.

As a technical founder, Joel has served as CEO, COO, and CTO for his previous companies, having raised over $100M in venture financing and scaled multiple businesses nationally.

Joel began programming at age 10, started college at 16, and founded his first technology company upon graduating at 21. He holds a bachelor’s degree in engineering from Queen’s University and an MBA with distinction from Harvard Business School.

Joel is a member of the Forbes Business Council and named Executive Hero of the Year for Effective Leadership During COVID-19 by the Consumer World Awards. He is also an angel investor, advisor to numerous startups and active in the Southern California startup community. Joel has been featured on Forbes, Fox Los Angeles, ABC Los Angeles, CBS Los Angeles, KIIS-FM, and more. Joel is passionate about the NBA champion Raptors and super convenient car repair.

“How to buy a car 101” should be a mandatory course taught in high schools throughout the United States. It’s incredible that modern day car buying is as aggravating, infuriating, and convoluted as it is, but that doesn’t mean every car shopper shouldn’t know the basics of how to buy a car.

Everyday we receive hundreds of emails from CarEdge members. Many of the emails are success stories about how we’ve helped with our Market Price Report, Deal School e-course, and guides. It puts a huge smile on our face to know that we are helping thousands of people navigate the car buying process more effectively and efficiently.

Just the other day we received an email from a gentleman named Clark. Clark bought a used 2017 Jeep Wrangler with 17,635 miles, and he shared his entire purchase process with us (step-by-step) from start to finish. Clark knows how to buy a car, and we thought we’d take his experience, which he documented and shared with us, as a case study that you can follow when you go to buy your next car.

To protect Clark’s privacy we’ve removed his personally identifiable information from any screenshots. Keep in mind that every resource or tool we recommend in this case study is 100% free.

Without further ado, let’s dive in.

One of the things Clark did that we highly recommend all car buyers do, is he researched trends in the automotive industry before contacting any dealers. Of course you want to get a great deal when you buy your next car, but what if the supply of vehicles is incredibly short right now, and no matter how impressive your negotiating skills are, car dealers simply won’t budge? What if the inverse is true, what if you know that the industry currently has a surplus of inventory, and that dealers are desperate for you to come in and buy a car.

In which scenario do you think you’ll get a better car deal?

Don’t be intimidated by the idea that you’ll need to scour the web looking for industry insights into inventory levels … We have you covered.

Want to make car buying easy? Let us do the hard stuff! It’s like Honey, but for buying cars, trucks, and SUVs. Sign Up For Free

Many research organizations exist that provide weekly and monthly updates on auto industry trends. Unfortunately these resources are only marketed towards industry professionals (which makes sense). That doesn’t mean you can’t access the same information.

Each week we publish a “Market Update” on the CarEdge YouTube channel. These 10-15 minute videos walk you through the high-level trends occurring in the auto industry this week. We pull our data from a few sources:

Our recommendation would be you either watch our weekly Market Update, or you refer to the three resources linked above. Either way, you’ll have a great sense for where the retail automotive market stands week in and week out.

Clark did this, and it was the perfect first step in his car buying process.

Once you have an understanding of the current market conditions, we recommend you zero in on market conditions for the specific vehicle (year, make, model, and trim) that you’re considering buying in your geographic area.

Our free Market Price Report is a great resource to do this, and that’s what Clark used.

You will use the Market Price Report in a two-pronged approach. First, to help you understand market conditions for the specific vehicle you’re interested in, and second to help you negotiate the best out-the-door price possible.

When we analyzed the overall market conditions (in the step above), we learned about inventory levels for the automotive industry as a whole. Now, with the Market Price Report, we’ll look at inventory levels for the specific vehicle we’re interested in for our geographic region.

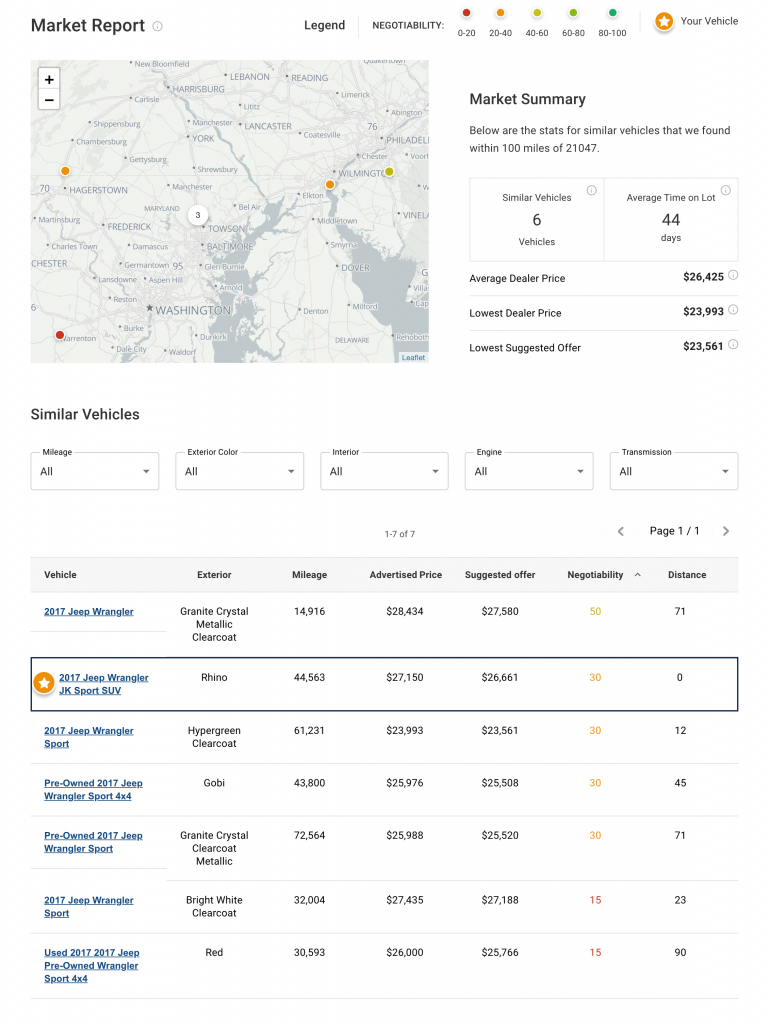

Let’s break down this screenshot. And again, for clarity’s sake, you can generate up to 100 of these reports for FREE here.

You can see there are 6 similar Jeep Wranglers in my area. The average amount of time they have been on dealer’s lots is 44 days. Either using the map, or the table, I can see there is another Wrangler within 100 miles of my location that has a higher Negotiability Score. The Negotiability Score is a calculation that takes into account days on lot and market conditions.

As a car buyer, I can now see that there aren’t that many Jeep Wranglers in my area, so negotiating a once in a lifetime car deal may not be realistic. That’s okay, this is why we analyze the Market Price Report, to set realistic expectations.

This is exactly what Clark did. From his email to me, Clark said, “I ran 24 different Jeeps through your tool. I narrowed it down to 7 that I liked. I chose to start with the one I bought because I felt like I had the most negotiating power.”

And that is exactly what the Market Price Report is intended for; to help you focus your attention on the best option in your area!

I told you, “How to buy a car 101” really should be a course they teach in all high schools across America!!

After reviewing local market conditions with the Market Price Report, you’ll want to turn your attention towards focusing in on a vehicle or two to negotiate with the car dealer. How do you choose which one to focus on? We recommend you use our Negotiability Score as an indicator for which you should focus on (the higher the score, the better). That’s what Clark did.

Clark knew the days on lot for the specific vehicle, the market conditions in his geographic area, and was ready to contact the dealer to negotiate the out-the-door price. He did something that we highly recommend as well, which is to get a copy of the CarFax before going too deep into the sales process.

We also recommend (although Clark did not do this) getting a pre-purchase inspection on any used vehicle you purchase. It’s a relatively small investment that gives you the peace of mind to know that the car you’re buying isn’t a clunker.

Once those two steps are complete you can then contact the dealer to negotiate the out-the-door price of the vehicle. From Clark, “Long story short After talking about the black book numbers and COVID situation I made an offer of $28,000 + TTL. They came back with an offer of $28,164 + $300 dollar fee for a total of $28,464. Just at what your Dad suggested. (see offer sheet attached)”

Most car salespeople are trained to ask you how you plan to pay for your purchase, cash, finance, or lease. Our advice is to say you’re open to financing through the dealership if their rates are competitive (unless of course you don’t plan to do that).

That being said, you should absolutely secure pre-approved financing from your local bank or credit union before going to the car dealership. That’s exactly what Clark did, “I was pre-approved through my credit union at 3.19% (60Mo) …”

Then Clark did what we recommend all car buyers do; he gave the dealer a chance to beat his pre-approved rate:

“I gave them (the dealer) a chance to beat that which they did at 3.05% (60Mo).”

That is a textbook example of how to negotiate with a car dealership. That is how to buy a car 101!

Today Ray and Zach do a deep dive into extended warranties. Many people are unaware that extended warranties on cars are typically not extended warranties. What do I mean? They’re actually vehicle service contracts. What’s the difference? Tune in to find out!

Access the Market Price Report now for FREE: https://app.CarEdgemember.com/

A Vehicle Service Contract (VSC) is an automotive protection plan that covers the cost of certain repairs and breakdowns in exchange for an upfront or monthly fee. Unlike auto insurance, which covers damage from accidents, a VSC helps pay for mechanical failures and unexpected repairs, giving car owners peace of mind.

While individual drivers often purchase a VSC for their own vehicle, fleet operators also use these contracts to protect multiple vehicles under their management. The terms of a VSC outline which repairs are covered and under what conditions, helping consumers avoid costly out-of-pocket expenses when unexpected breakdowns occur.

Understanding the difference between a Vehicle Service Contract and auto insurance is key. Insurance primarily covers accident-related damage, while a VSC steps in when a vehicle experiences a mechanical failure unrelated to a collision. For many drivers, having both types of coverage provides the best financial protection against unforeseen car expenses.

That being said, it is of the utmost importance that you understand what vehicle service contracts are (and what they are not), so that you can make an informed decision. Without further ado, let’s dive in.

Believe it or not, there is actually no such thing as an “extended warranty” for a car, truck, or SUV that comes from a third party (not the manufacturer or the dealer). Let’s take a closer look at this common misconception.

The term “extended warranty” is used colloquially by third party companies, but technically it does not exist. A warranty is something that comes with the purchase or lease of the vehicle. It can be given by the manufacturer (most typically) or the dealer, but it is an incident of the sale. Warranties are express (the vehicle conforms to a written statement like this vehicle has a new transmission) or implied (warranty of merchantability or fitness for a particular purpose such as if the dealer knows the customer will use it for commuting).

If a customer pays for extended coverage, that is a vehicle service contract. Under the Magnuson Moss Act, if a dealer sells a vehicle service contract to the customer within 90 days of sale, the dealer cannot disclaim implied warranties. Nevertheless, the term “extended warranty” is sometimes used incorrectly to refer to a vehicle service contract.

Of course, vehicles can (and do) have warranties. Those warranties most commonly come from manufacturers. For example, Kia offers a 10-year/100,000 mile limited powertrain warranty on new vehicles. If you’re then being sold an “extended powertrain warranty,” look at the fine print to confirm it is coming from either the dealer or the manufacturer.

If it is a third party, know that they are not selling you an extended powertrain warranty, they are selling you an extended service contract that covers the vehicle’s powertrain. There is a difference between the two. You’ll know it’s a third party if the name on the contract isn’t the dealership’s or the manufacturer’s company name.

Typically, when we talk about coverage, we talk about two things: stated coverage and exclusionary coverage. Stated coverage refers to a policy where the covered items are explicitly listed in the contract. If it is not stated as “included” then it is not covered. Exclusionary coverage is broader, and therefore offers better protection for the consumer. If a part is not specifically listed as excluded, then the contract provider has to pay the claim for the part. This type of coverage is the best because it protects your vehicle in all but a small selection of circumstances.

Now that we know the difference between a vehicle service contract and an extended warranty, the question is, are vehicle service contracts worth it? To answer this question we need to talk about VSC coverage for new and used vehicles.

Are vehicle service contracts worth it for new vehicles? In summary, it depends on your risk tolerance.

Any vehicle service contract you are offered is inclusive of manufacturer warranties. What does this mean? This means that a vehicle service contract does not replace, nor extend a manufacturer’s existing warranty on a vehicle.

With that in mind, why then would you buy a VSC, if the manufacturer warranty is already in place? There are two reasons:

Let’s unpack both of these two reasons why you should consider getting a VSC on a new car.

First, it’s important to understand that many administrators offer perks with their service contracts to make them more appealing to new car owners. For example, trip interruption coverage, rental car reimbursement, and 24/7 roadside assistance are all included in CarEdge’s vehicle service contract. These are perks that are typically not included in a manufacturer’s warranty.

Generally, new car vehicle service contracts are much more affordable. Unfortunately, for consumers, most dealers add incredible mark up to these products, so you’d be hard pressed to consider them “cheap” when you’re sitting in the finance and insurance office at the dealership, but CarEdge is proud to offer the best Vehicle Service Contract pricing.

At the end of the day, if you’re able to negotiate a fair price on a VSC for a new car, it can most certainly be worth it. Purchasing coverage for your new car is entirely up to you and your risk tolerance. And, as always, read the contract before you sign!

Similar to new cars, service contracts for used vehicles are priced according to how much risk the plan administrator is taking on. That being said, service contracts for used vehicles are the same “value” as they would be for a new vehicle.

It is important to understand that if the used vehicle you are purchasing has existing manufacturer warranties in place (for example the vehicle you are buying has 25,000 miles on it, and the manufacturer warranty cover up to 36,000 miles), then the vehicle service contract is inclusive of that existing warranty (just like what we discussed above with regards to new cars). For clarity, this means that the service contract does not extend the manufacturer’s warranty, instead it exists in conjunction with the manufacturer’s warranty.

It is very important that you read the contract carefully before purchasing a vehicle service contract. In the contract you will see what repairs the administrator excludes. The last thing you want to do is sign up for a service contract, only to go to the repair shop one day and have to foot the bill because what broke wasn’t covered.

When deciding whether a VSC is worth it, consider your risk tolerance, vehicle reliability, and budget for unexpected repairs. For new cars, an affordable service contract can be a smart way to add extra perks like roadside assistance, trip reimbursement, and rental car reimbursement. For used cars, a VSC can provide financial protection against costly repairs, but it’s essential to read the contract carefully to understand what’s covered.

At CarEdge, we believe in transparency — no inflated dealership markups, just fair pricing for coverage that can give you peace of mind. Get your vehicle service contract quote in minutes, and rest assured with CarEdge!

As if buying a car wasn’t hard enough, purchasing add-ons like an extended warranty can be even more frustrating and irritating for car shoppers. For starters, what if I told you that the phrase “extended warranty”, is frequently used in an intentionally misleading way to profit off car buyers? We are talking about the car business, so maybe it’s easier to believe because of that, but the truth is, nine times out of ten, when someone is talking to you about an extended warranty they’re using the entirely wrong phrase.

Why then do you see commercials for extended warranties, get letters telling you that you should purchase an extended warranty, or receive phone calls telling you that your car is out of warranty and that you should buy an extended warranty RIGHT NOW? Because capitalism, that’s why.

Selling extended warranties is a lucrative business, even if in most cases it is a made up word that doesn’t actually exist. Many companies have found great success in the tactics described above (essentially fear marketing), and for better or worse, the term “extended warranty” isn’t going away anytime soon.

All that being said, we strongly suggest that you read or guide to vehicle service contracts. Most extended warranties are actually just vehicle service contracts. More on that below.

If you’re dead set on learning about extended warranties, then have no fear. We’ve taken most of our guide on vehicle service contracts and adapted it for this page. The reality is, more car buyers search for “extended warranty” than they do for “vehicle service contract” so it’s important we cover both topics (even though in most cases they are the same thing).

Without further ado, let’s dive in.

So what actually is an extended warranty on a car? First you need to understand that a warranty is something that comes with the purchase or lease of a vehicle. It can be given by the manufacturer (most typically) or the car dealer, but it is an incident of the sale. Third parties cannot issue warranties for goods they did not produce or sell directly.

An extended warranty on a car, truck, or SUV that is sold by a third party is actually a vehicle service contract. An extended warranty sold by a seller (dealer), or manufacturer is an extended warranty.

The Magnuson–Moss Warranty Act of 1975 was enacted to fix problems as a result of sellers using disclaimers on warranties in an unfair or misleading manner. The unfortunate reality is that sellers are still using the term warranty in a misleading way.

Here’s a great example of this in practice. Go to PenFed Credit Union and you’ll see they sell “extended warranties”.

The moment you click on one of the sample contracts you quickly realize it is for a vehicle service contract.

What’s the difference between the two? Quite a bit!

Warranties are express (the vehicle conforms to a written statement like this vehicle has a new transmission) or implied (warranty of merchantability or fitness for a particular purpose such as if the dealer knows the customer will use it for commuting).

Want to make car buying easy? Let us do the hard stuff! It’s like Honey, but for buying cars, trucks, and SUVs. Sign Up For Free

If a customer pays for extended coverage, that is a vehicle service contract. Under Magnuson Moss, if a dealer sells a vehicle service contract to the customer within 90 days of sale, the dealer cannot disclaim implied warranties. In approximately 38 states, a dealer can otherwise disclaim express and implied warranties. It does so on the Used Car Buyers Guide and in the RISC or lease agreement.

All that being said, the term “extended warranty” is frequently used incorrectly to refer to a vehicle service contract. Extended warranties on vehicles can only be administered from the manufacturer or the dealer. For example, CarMax offers a 90 day or 4,000 mile limited warranty, and then prolonged vehicle service contracts through their third party administrators.

If you are purchasing a vehicle from your local dealer and they offer an extended warranty, it is up to you to do your due diligence and check who the administrator is of that warranty. Is it the dealer (unlikely)? If so, then it’s an extended warranty. Is it a third party administrator (likely), then it’s a vehicle service contract.

Why is it important that you understand the difference between an extended warranty and a vehicle service contract? Because some unscrupulous people will try and sell you an extended warranty that leads you to believe your existing warranty is “extended” thanks to the warranty you just purchased. This is not the case! Extended warranties administered through a third party (aka a vehicle service contract) do not extend your current warranty (crazy right?). Instead, they are inclusive of existing warranties on a vehicle. This means it will run in parallel with the manufacturer warranty and does not “extend” the warranty of the vehicle. It is critically important that you confirm who is actually administering the “warranty” to know if it is actually extending your coverage, or if it’s simply a vehicle service contract.

Maybe congress should pass another law that makes it illegal for companies to call themselves “Route 66 Warranty” when they really sell vehicle service contracts, but that can be for another blog post!

Okay, now that we understand what an extended warranty for a car is (and isn’t), the question is “should I buy one?” There are a few factors that go into answering this question. The TLDR is; you have to assess your risk tolerance and decide for yourself if an extended warranty is a good value or not.

One of the first things you need to understand about extended warranties for cars is that they are priced dynamically. Similar to other insurance products (think auto insurance for example), extended warranty pricing is different based on each and every vehicle identification number (VIN), and the current mileage of the car. That is to say that no two vehicles have the exact same price quote. An extended warranty on a Ford F-150 will be different then a BMW 3 series. Depending on the year, make, model, trim, and mileage, each extended warranty will be quoted from an administrator (like a Route 66 warranty, or even the manufacturer who is actually selling a legitimate extended warranty and not a vehicle service contract) with a different wholesale price.

Pricing for extended vehicle warranties is dynamic because the administrator is monetizing the risk associated with covering the costs of certain repairs to that vehicle. If you’re buying a brand new Toyota Camry that is covered by the manufacturer’s warranty, you can expect the wholesale price of a vehicle service contract to be very low. Toyota is an economy brand, and the parts needed to repair it are relatively inexpensive. Being new and under the manufacturer’s warranty means that the third party vehicle service contract most likely won’t end up with any claims against it.

Compare that to a used Mercedes-Benz E-Class sedan with 70,000 miles on it. The wholesale price for this VIN will be MUCH greater than the same extended warranty on the Camry. Why? Because the administrator is taking on a lot more financial risk. To make up for this, they sell the vehicle service contract at a much higher wholesale price.

At the end of the day, extended warranty companies are going to make their money. They know for each VIN in existence what the price is they need to offer to cover their risk and still make a profit.

What does that mean for you? It goes back to our TLDR. If you have a high risk tolerance, don’t bother with a vehicle service contract or an extended warranty. If you value the comfort of knowing things will be “covered” (although it is important to understand that there are a lot of exceptions in manufacturer, dealer, and third party contracts), then consider purchasing an extended warranty or vehicle service contract.

Now that we understand how an extended warranty for a car is priced on the wholesale side of things, we can begin to unpack what happens on the retail side. Traditionally third party extended warranties are sold to “agents,” who then turn around and sell the products to car dealerships.

If you’re keeping up at home, that means the administrator sells the extended warranty to the agent, then the agent sells the extended warranty to the dealer, and then the dealer sells the extended warranty to you, the car buyer. I don’t know about you, but that’s a lot of hands involved in one transaction.

How much does an extended warranty cost when you go to buy one? Well, that depends on how much mark up each person in the supply chain added on to the extended warranty before it gets to you. Agents need to make their money, so they’ll mark up the extended warranty 10 to 20% when they sell it to a dealer. Dealers need to make their money, and since they don’t make it by selling cars, they try and make up for that when they sell products like extended warranties. They typically mark up extended warranties 200 to 300%.

What does that mean for you? Well, an extended warranty that may have cost the agent $500 to buy wholesale will be offered to you for more than $2,000 at the dealership.

Now if you are actually buying an extended warranty from the manufacturer, and not a vehicle service contract disguised as an extended warranty, the pricing will certainly be similar. Remember, extended warranties can only be provided by the manufacturer or the dealer. Most dealerships do not offer their own warranties, and instead they rely on third party products (like vehicle service contracts that we’ve been discussing). However most manufacturers do offer some extended warranty plans.

For example, if you purchase a certified pre-owned vehicle it will typically come with an extended warranty. This actually is an extended warranty because it is coming from the manufacturer. You may also have the opportunity to purchase an extended warranty directly from the manufacturer, again that is a real extended warranty. The cost for these warranties is different for each and every manufacturer, and it is unknown what the markup is. However, just like with third party warranties, manufacturers price their extended warranties dynamically to make sure they are charging enough to make a profit.

Many third party companies claim to sell extended warranties. As we’ve discussed, they actually sell vehicle service contracts. Be weary of any company that markets themselves as a warranty provider when in reality they are selling vehicle service contracts. That being said, there are dozens of third party administrators you can purchase from.

Rather than give them publicity here on the CarEdge blog, we will simply refer you to this list: https://www.consumeraffairs.com/auto_warranty/

Yes! This is literally one of the only ways you can purchase an extended warranty. Manufacturers of goods are able to sell extended warranties on their products. You don’t even have to deal with the local car dealer to secure a manufacturer extended warranty. You can call the manufacturer directly and purchase a policy.

I don’t blame you! It’s fascinating how this part of the automotive industry works, isn’t it? Here are the resources I used to help gain a better understanding of how the extended warranty industry operates.