CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

CarEdge, the best place to buy, sell, and own a car with confidence, recently surveyed 408 U.S. drivers to better understand how consumers are navigating the car market in 2025. The survey, conducted from May 16 to May 19, comes at a pivotal time. Following the implementation of U.S. auto tariffs on April 3, car prices, interest rates, and inventory levels have all been in flux. With uncertainty growing, CarEdge sought to answer a critical question: how are real drivers adapting their car buying behavior?

Survey participants represent a broad cross-section of car shoppers and owners, from those who’ve recently purchased to those holding off for the foreseeable future. The full survey is available at CarEdge.com. Below, we break down the most important findings from this May 2025 snapshot.

The survey responses paint a picture of a divided car market, shaped by mixed economic signals and widespread caution. Among all respondents, 16% reported purchasing a car after the April 3 tariff announcement, while another 12% said they had bought a vehicle shortly before the tariffs went into effect. A much larger share (52%) said they are still actively shopping for a car, while 20% said they have not purchased a vehicle in the past six months and do not plan to buy one in 2025.

Tariffs have clearly impacted perceptions. Interestingly, among those who bought their car before April 3, 38% acknowledged they made the purchase early specifically to avoid the risk of higher prices. Among those who purchased after April 3, 16% said they believe they paid more due to the tariffs, with the vast majority of post-tariff buyers (84%) saying they believe they did not pay more.

Looking ahead, half of respondents are still planning to buy a car before the end of 2025. Of those future buyers, about a third plan to purchase new, another third are shopping used, and the remaining 30% are still undecided.

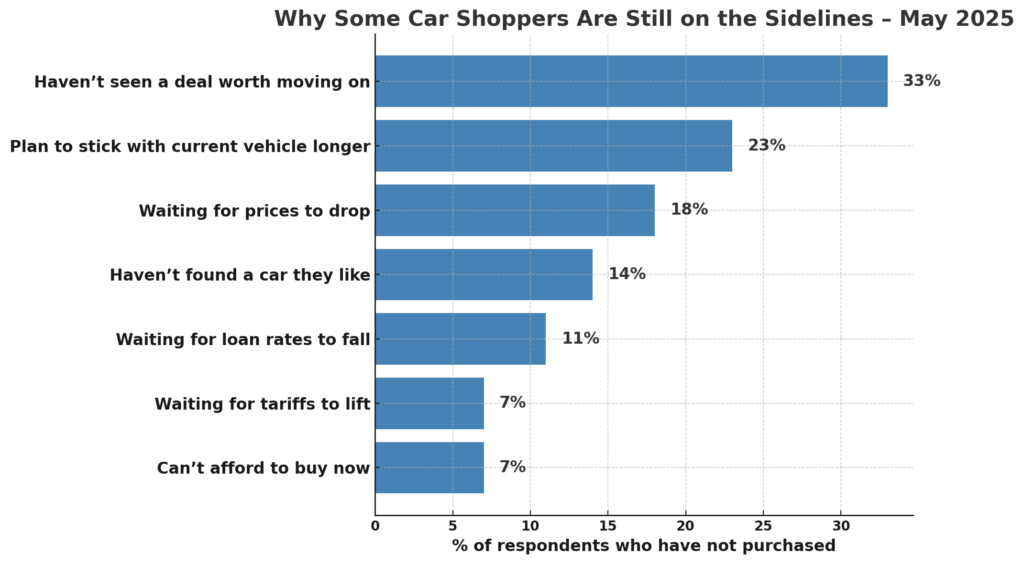

When it comes to what’s keeping people on the sidelines, affordability challenges and a lack of compelling deals top the list.

These are the barriers to buying (as a percent of all respondents who have not purchased):

With these top-line insights in mind, we next explore specific groups within the survey to uncover how recent and future car buyers are thinking about today’s market.

Survey respondents who purchased a car in the six months leading up to April 3 offer another layer of insight. Among these buyers, 61% purchased new and 39% purchased used.

What stands out most in this group is that more than a third (38%) said they intentionally bought their car early to avoid potential price hikes from tariffs. For the remaining 62%, tariffs didn’t factor into the timing of their purchase.

Income again played a role in how buyers approached the market. Among households earning $200K or more, just 22% said they made their purchase early in response to the looming tariffs. Nearly half (48%) of buyers earning between $100K and $199K did the same. In contrast, 39% of buyers earning under $100K said they bought early to avoid tariff-related price hikes.

This suggests that low- to middle-income consumers were more likely to act on policy changes and proactively adjust their buying timeline. Higher-income households, on the other hand, may not have been as concerned about the possible impact of tariffs on car prices this spring.

For respondents who bought a car after the April 3 tariff rollout, the data reveals a blend of resilience and skepticism. Among this group, 81% purchased a new vehicle, while 19% opted for a used one.

Despite the added costs associated with the new tariffs on imported vehicles, most post-April 3 buyers didn’t feel the sting. A strong majority—84%—said they don’t believe they paid more as a result of the tariffs. Still, 16% acknowledged they believe they did.

Among buyers who purchased after the April 3 tariff implementation, a different pattern emerged. Higher-income households were more likely to believe tariffs increased the price they paid. Specifically, 27% of households earning over $200,000 said they believed they paid more because of tariffs. In contrast, only 11% of households earning between $100,000 and $199,999 felt the same. Meanwhile, 17% of buyers with incomes under $100,000 said they believed tariffs had raised their purchase price.

These results suggest that while tariffs haven’t universally discouraged buyers, those with tighter budgets and those with a keen eye on policy changes are the most attuned to their potential impact.

Among those still planning to buy a car in 2025, the data reveals a thoughtful and strategic group of shoppers. Less than half (44%) of active shoppers expect to make their purchase within the next three months, while a majority (56%) plan to buy later this year.

When it comes to what they’re looking for, 54% say they’re in the market for a new car. About 19% are shopping for used vehicles, while just over a quarter are still unsure.

As for why these shoppers haven’t yet moved forward, deal quality remains the leading barrier. Respondents were asked to select all reasons why they have yet to purchase in 2025. 50% say they haven’t seen an offer worth acting on, while 30% are waiting for prices to come down. Another 21% say they haven’t found a car or truck they like. A smaller group is holding out for lower loan rates (18%), while tariffs were cited by just 11% of active shoppers.

One-fifth of active shoppers said that their decision to keep their current vehicle for longer was a factor in delaying their purchase.

Looking at the income distribution of active shoppers, the data continues to reflect a largely middle-income profile. The majority fall between $50K and $149K in household income, suggesting that many of these buyers are financially capable, but remain cautious in an uncertain economy.

Among drivers who have neither purchased a car in the past six months nor plan to buy one in 2025, a few clear themes emerge. This group is not driven by fear of rising costs or policy uncertainty, but rather by satisfaction with their current vehicle, and a lack of appealing options in today’s market.

The majority of these respondents (71%) say they’re sticking with their current vehicle longer, a sign that many Americans are adopting a “wait and see” approach to the market. Beyond that, 23% haven’t seen a deal worth moving on, while 9% say they haven’t found a car or truck they like. Price sensitivity remains a factor, with 20% waiting for prices to drop and 14% holding out for lower loan rates.

Concerns about tariffs are present, but not widespread. Among those on the sidelines right now, the reasons cited are roughly the same for all income segments. About one quarter say that they’re keeping their current vehicle for longer, while roughly 20% say they haven’t seen any deals worth acting on yet. The third most common reason for sitting out today’s car market is waiting for prices to come down. Only 7% cited tariffs as one of their reasons for not planning to buy a car in 2025.

The 2025 CarEdge Consumer Survey shows that the American car market remains fractured and cautious in the wake of economic headwinds and new policy shifts like auto tariffs. While some shoppers are moving forward with confidence, many are hesitant, skeptical, or simply waiting for conditions to improve.

The overarching takeaway? The car market in 2025 is no longer defined by pent-up pandemic demand or rapid inflation. Instead, it is being shaped by deal quality, interest rates, and policy awareness. For automakers, dealers, and car buyers alike, understanding these shifting motivations is key to navigating what’s shaping up to be one of the most complex car buying environments in recent history.

Founded in 2019 by father-and-son team Ray and Zach Shefska, CarEdge is a leading platform dedicated to empowering car shoppers with free expert advice, in-depth market insights, and tools to navigate every step of the car-buying journey. From researching vehicles to negotiating deals, CarEdge helps consumers save money, time, and hassle. Join the hundreds of thousands of happy consumers who have used CarEdge to buy their car with confidence. With trusted resources like the CarEdge Research Center, Vehicle Rankings and Reviews, and hundreds of guides on YouTube, CarEdge is redefining transparency and fairness in the automotive industry. Follow us on YouTube, TikTok, X, Facebook, and Instagram for actionable car-buying tips and market insights.

Subaru just became the latest automaker to raise vehicle prices, and it likely won’t be the last. As new tariffs and 2026 model-year pricing updates collide, car shoppers across the U.S. are noticing a troubling new trend: mid-year price hikes. But there’s still a window of opportunity: Subaru’s latest offers include low-APR financing and compelling lease deals.

If you’re planning to buy a new Subaru this summer, now may be your best chance to lock in a deal before the next round of price hikes hits.

Subaru of America is the latest automaker to hike vehicle prices as the cost of doing business rises. While many suspected tariffs were the cause, Subaru instead cited “current market conditions” and a need to “offset increased costs while maintaining a solid value proposition.”

According to a now-deleted dealer bulletin shared by Car and Driver, price increases range from $750 to $2,055, depending on the model and trim. As best as we can tell, these price hikes apply to all new Subaru models, meaning both 2025 and 2026 models. Here’s a breakdown of the new pricing changes:

These new sticker prices are already beginning to show up on dealer lots, and Subaru has confirmed that MSRP updates are rolling out immediately. However, it remains unclear how quickly they’ll affect prices for older inventory.

Subaru’s 2025 price hikes follow a familiar strategy. The best-selling Subaru models see the greatest price hikes, and those with sluggish sales are barely budging. For fans of the Ascent, Outback, and Forester, nearly $2,000 in price hikes will be an unwelcome sight.

Subaru’s latest price hike is part of a broader trend. Across the industry, automakers are dealing with a one-two punch: steep new tariffs on imported vehicles and parts, and 2026 model-year pricing creeping in. Add slow but steady inflationary pressures to the mix, and what you get is automakers like Subaru announcing mid-year price adjustments.

While Subaru avoided directly blaming tariffs, the timing aligns with similar hikes from other automakers. And with roughly 45% of Subaru’s U.S. sales coming from imported models, the brand is especially vulnerable.

Expect more automakers to quietly follow suit in the coming months. Volkswagen Group, Mazda, and Honda all import a large portion of their U.S. sales volume, and are likely to respond to the challenges. If you’re car shopping this summer, locking in pricing sooner could help you avoid the next wave of increases.

If you’re in the market for a new Subaru, now is the time to act. The brand is raising prices by up to $2,055, and the most popular models are already impacted. While older inventory may still reflect lower pricing, that window is closing fast.

The good news? Subaru is still offering 0% APR on select models, including some of its most in-demand vehicles.

Here’s a rundown of Subaru’s latest offers in late May 2025:

Subaru’s price increases are just the start of what’s shaping up to be a more expensive summer for car shoppers. With tariffs, MSRP hikes, and thinning incentives, it pays to act fast.

Whether you’re considering a Subaru or cross-shopping with competitors, the best deals won’t last long. Before you head to the dealership, make sure you’re prepared:

🔍 Check Dealer Invoice Pricing – Know what others are really paying before you negotiate.

🚗 Search Local Inventory – Compare prices near you and spot pre-hike listings.

Buy with confidence and save more with CarEdge on your side.

Tires aren’t cheap, but the right care and habits can help you squeeze more miles out of them safely. Whether you’re commuting daily or taking the occasional road trip, your tires are the foundation of your car’s performance and safety. Yet, far too many drivers replace tires sooner than they need to. And if you haven’t noticed, a set of 4 tires can cost well over $1,000 these days.

Here’s the good news: with just a little regular maintenance and a few smart habits, you can extend the life of your tires and your car. Let’s break it down.

Getting more life out of your tires means more money in your pocket, and a safer ride. It’s about consistency, not complexity. A few extra minutes each month checking pressure or rotating tires with your oil change can make a real difference.

Want to go the extra mile? Use the CarEdge Garage to stay on top of tire maintenance, track your car’s value daily, and never miss a service again. It’s free, and it’s the easiest way to make smarter decisions about your car.

In 2025, car buyers are tempted by employee pricing incentives, 0% APR offers, and huge cash discounts. But are you actually getting a good deal? While the ads shout “limited-time savings,” not every offer is as great as it looks. The truth is, some deals are just inflated MSRPs dressed up with a cash rebate.

So how can you tell what’s a smart buy, and what’s just dealership smoke and mirrors?

Start with this: the dealer invoice price. Here’s how to tell if you’re getting a good deal on a car this Memorial Day.

It’s easy to get swept up in the excitement of car sales. Dealerships know this, and that’s exactly why they flood the airwaves with “must-act-now” offers. But behind the scenes, there’s often a big gap between what they’re showing you and what they actually paid for the car.

That’s where many car buyers fall into the trap of overpaying.

It doesn’t help that Ford and Stellantis (Jeep, Ram, Dodge, and Chrysler, among others) are touting employee pricing specials, which are not as good as they seem.

The truth is, knowing what’s a good deal and what’s merely a mirage of a good deal is tougher than it should be in 2025.

The dealer invoice price is the amount a dealership pays the manufacturer for a vehicle. It’s lower than the MSRP (Manufacturer’s Suggested Retail Price) you see on the window sticker. But here’s the key: manufacturers often provide hidden incentives, kickbacks, or volume bonuses that drop the dealer’s real cost even further.

Knowing the invoice price puts you in control:

Even better? With the right leverage, you can often negotiate below the invoice price.

Instead of guessing what’s a good deal, we built a tool that shows you what dealers don’t want you to see. Just select the vehicle you’re considering, and we’ll give you:

✅ Dealer Invoice Price – Know what the dealer paid

✅ Target Discount Guidance – Understand what you should be paying

✅ Cost-to-Own Data – Factor in depreciation, fuel costs, and more

✅ Negotiation Tips – Learn what to say (and when to walk away)

✅ Inventory Pro – See which cars are likely negotiable

And the best part? It’s 100% free. No hidden fees, no catch. See for yourself →

To make the most of your car buying adventure (and your precious time), keep these tips in mind:

With car prices still hovering near record highs and inventory tightening in many areas, you can’t afford to go to the dealership unprepared. But with the right tools, you can make smart decisions, skip the stress, and walk away with a truly great deal. Your car deal starts with the facts, and CarEdge is here to give them to you.

It’s the end of the road for these familiar faces. As automakers shift priorities toward SUVs and electric vehicles, several long-running nameplates are quietly exiting stage left. Some have already ended production. Others are nearly sold out. Whether you’re a nostalgic fan or a bargain hunter, this summer is your last chance to drive home these cars before they’re gone for good.

Remaining inventory nationwide: 54

Production has ended for the Audi A4, as Audi shifts focus toward larger sedans and EVs. The A4 is effectively being replaced by the larger and sportier Audi A5 and S5 models. With Volkswagen Group’s uncertain EV strategy and financial struggles, streamlining the lineup played a role in the decision.

See the last A4 listings before they’re gone.

Remaining inventory nationwide: 3,600

As Cadillac pivots to electric vehicles like the Lyriq, Optiq, and Vistiq, models like the XT4 and XT6 are being discontinued. Production ceased in January 2025, so today’s inventory is all that’s left. At current selling rates (81 days of market supply), the last XT4 will be sold in August or September of this year.

See the last XT4 listings before they’re gone.

Remaining inventory nationwide: 2,061

Following 61 years as a classic American-made car, the last Malibu rolled off the assembly line in November 2024. In May, there were just 2,061 copies of the Malibu left for sale. With just 49 days of market supply, it’s likely that the last brand-new Malibu will find a home sometime in July. Perhaps a lucky museum will see the value and add one to their collection.

See the last Malibu listings before they’re gone.

Remaining inventory nationwide: 17

After 55 years and 1.1 million cars sold, the MINI Clubman ended production back in February 2024. In May 2025, 17 Clubmans remained unsold. Even as a critically endangered species, they’re slow to sell. If you want to claim one of the last Clubmans ever, you could probably get your hands on one over the next few months.

See the last Clubman listings before they’re gone.

Remaining inventory nationwide: 287

You’d be hard pressed to find many truck fans who will miss the Titan, but if you’re among this rare breed of Nissan aficionados, act fast as only 287 Nissan Titans remain unsold. At current selling rates, they’re on track to be extinct sometime in July.

See the last Legacy listings before they’re gone.

Remaining inventory nationwide: 4,615

Subaru has sold 1.3 million copies of the Subaru Legacy since launching the all-wheel drive sedan back in 1989. As the first Subaru model made in America, the Legacy has a special place in the hearts and minds of Subaru fans. Subaru previously announced that production of the Legacy would end sometime this spring. Although over 4,000 remain on dealership lots, it’s a relatively quick seller. At current selling rates, this Subaru sedan will be gone by late summer.

See the last Legacy listings before they’re gone.

Remaining inventory nationwide: 550

Volvo sales have been slowing over the past few years, and the S60 sedan has become a casualty of this trend. The S60 was built in South Carolina, which is now home to the 2025 Volvo EX90 SUV. Volvo will continue to build the S90 in China for other markets, but there are no plans to import them to the U.S. market.

See the last S60 listings before they’re gone.

A handful of other nameplates will also vanish after 2025, but remain widely available for now. The Nissan Versa is one such example. Want to see what else is going away by 2026? Check out our full list of cars being discontinued this year.

As always, be sure to shop smart with CarEdge’s free tools and local market insights. Looking to have an expert negotiate car prices on your behalf? We’ve got the perfect solution.

Happy summer car shopping!

Thinking about holding onto your car for the long haul? You’re not alone. In today’s car market of rising prices and rapid depreciation, many drivers are wondering whether it’s smarter to stick with the car they already own.

At CarEdge, we believe informed decisions save you thousands. Here’s what you need to know before deciding whether to keep your vehicle for longer, or start fresh with something new.

New cars lose 20–30% of their value in the first year alone. By keeping your car longer, you avoid taking that financial hit repeatedly. Plus, you won’t be shelling out for sales tax, registration fees, or dealership add-ons every few years. Insurance costs also tend to drop with older cars. This is especially if you drop comprehensive or collision coverage once the car’s value declines significantly as the miles add up.

Check out our free cost of ownership data

Most auto loans are paid off in 3–6 years. If you hold onto the car after that, you’ll enjoy years of driving without a monthly payment. Having a paid-off car means freeing up cash for other priorities, like savings or paying down debt.

You know your car. Its quirks, service history, how it drives in snow or rain—there’s no learning curve. That trust and comfort can go a long way in peace of mind, especially when you’ve maintained the car well.

Even the greenest EV has a carbon footprint from manufacturing. Holding onto your current car—even if it’s not electric—can be more environmentally friendly than replacing it with a new one every few years.

Buying a car can be a hassle. Keeping your current car means no time spent researching new models, test driving, negotiating prices, or dealing with trade-ins. It’s one less thing to worry about.

Even well-built cars eventually wear down. Between years 8 and 12, expect bigger-ticket repairs like suspension work, HVAC issues, or transmission problems. Costs can vary dramatically depending on the make and model, but reliability becomes less predictable.

See maintenance rankings by make and model

Newer vehicles often come with advanced safety features like automatic emergency braking, adaptive cruise control, blind spot monitoring, and more. Your old ride might not have these, which can make a big difference in both safety and comfort.

Seats wear out. Touchscreens lag. The cabin might feel outdated or less comfortable over time. Even if the engine runs strong, the driving experience may start to feel more like a chore.

After 10 years, most vehicles have very little resale value. This is especially true for cars with well over 100,000 miles on the odometer. In contrast, if you sell after 5 years, you might still recover 40–60% of the original price. If you plan to trade in later, timing matters.

We’ve got plenty of free depreciation tools to keep you informed.

If you own an EV, charger standards and technology may evolve. For instance, early Nissan LEAF owners are encountering challenges finding compatible charging these days. Even gasoline vehicles might also face limitations as fuel blends change or emissions standards tighten. An older car could eventually feel outdated or even unsupported.

Let’s say you buy a $35,000 car.

Over 10 years, buying two newer vehicles could cost $8,000 to $15,000 more than keeping one car the whole time, depending on the model, insurance, taxes, and maintenance needs.

If your car is still safe, reliable, and not draining your wallet in repairs, holding onto it a few more years is often the smartest financial choice. On the other hand, if maintenance costs or safety concerns are piling up, it may be time to move on.

Need help figuring out whether your current car is worth keeping?

👉 Check out the CarEdge Value Tracker, and know when it makes sense to sell.

Or, explore how long-term ownership compares to financing something newer with our full Cost to Own Rankings.

Subaru just became the latest automaker to announce price hikes—and it likely won’t be the last. As new tariffs and 2026 model-year pricing updates collide, car shoppers across the U.S. are seeing prices creep higher by the week. But there’s still a window of opportunity: Subaru’s Memorial Day deals include 0% APR offers and below-average financing on top models, and similar incentives from rivals like Tesla and Chevy are heating up too.

If you’re planning to buy a new car this summer, now may be your best chance to lock in a deal before the next round of price hikes hits.

Subaru of America is the latest automaker to raise vehicle prices as the cost of doing business rises—thanks in part to the recently imposed auto tariffs.

As first reported by Reuters, Subaru confirmed on May 19 that it’s increasing prices on several popular models, citing “current market conditions” and the need to “offset increased costs while maintaining a solid value proposition.” While the company avoided directly blaming tariffs, the timing lines up with widespread price adjustments across the industry as import taxes take a toll.

According to a dealer bulletin obtained by Reuters, the price increases will range from $750 to $2,055 depending on the model and trim. The Subaru Forester, which is already a top seller and widely imported, is among the most affected—prices will rise between $1,075 and $1,600. These new sticker prices are expected to hit dealership lots starting in June 2025.

Subaru imports roughly 45% of its U.S.-sold vehicles, according to S&P Global Mobility, making it particularly vulnerable to the 25% tariffs the U.S. now places on imported vehicles.

Subaru’s latest price hike is just the beginning. Across the industry, automakers are facing a one-two punch: steep new tariffs on imported vehicles and parts, combined with 2026 model-year price increases that are rolling out ahead of schedule.

While Subaru didn’t directly cite tariffs in its statement, the timing speaks volumes. The Trump administration’s 25% tariff on imported vehicles is already prompting automakers like Ford and Subaru to raise sticker prices to protect shrinking margins. And with almost half of Subaru’s U.S.-sold vehicles imported, the brand is especially exposed.

At the same time, many automakers are finalizing pricing for incoming 2026 models, which typically carry higher MSRPs. In many cases, even 2025 models still sitting on dealer lots are getting mid-cycle price bumps. That means car buyers in late spring and early summer are likely to see both tariffs and new model-year pricing converge, making it harder to find value on new vehicles.

Subaru may be the latest to raise prices—but they won’t be the last. As inventory updates in June and July, expect other automakers to quietly follow suit. If you’re planning to buy a new car this summer, shopping sooner rather than later could save you hundreds—or even thousands.

See the best Memorial Day sales, from 0% financing to huge cash offers.

If you’re in the market for a new Subaru, now is the time to act. Subaru is raising prices by as much as $2,055, and according to the automaker’s website, MSRP changes will roll out in June, and inbound inventory is likely to be impacted. While older inventory on dealer lots may not be affected, it remains unclear how quickly these price increases will be reflected in what shoppers actually pay once June arrives.

For now, Memorial Day deals are still live, including 0% APR offers on some of Subaru’s most popular models.

And while Subaru’s incentives are strong, some competitors are fighting hard for buyers this Memorial Day—especially as tariffs disrupt pricing across the board.

Here’s how Subaru’s best offers compare to the competition:

Still, Subaru’s 0% for 72 months on the 2025 Solterra and 2024 WRX stand out as some of the longest zero-interest terms available anywhere. With price hikes looming, now is the time to take advantage of Subaru’s May incentives.

Subaru’s price increases are just the start of what’s shaping up to be a more expensive summer for new car shoppers. With tariffs, MSRP updates, and tightening incentives, it pays to shop smart—and fast. Whether you’re considering a Subaru or cross-shopping with competitors, the best deals won’t last long.

Before you head to the dealership, get the facts with CarEdge:

Buy with confidence—and save more—with CarEdge on your side. Learn more about how we can help buyers of every budget.

![Every 0% APR Financing Offer This Memorial Day [2025]](https://caredge.com/wp-content/uploads/2025/05/zero-percent-financing-memorial-day-offers-1080x675.jpg)

Memorial Day weekend is still one of the biggest car shopping events of the year, but let’s be honest—2025’s deals aren’t what they used to be. Automakers are scaling back the big incentives we got used to in years past. However, for buyers with solid credit, there are still some great financing offers to take advantage of—specifically, zero percent APR deals.

As of this Memorial Day, there are 16 brands offering 0% APR financing on select models. Some are for 36 or 48 months, others stretch as long as 72 months. Below, we break down every zero percent APR deal available in May 2025, organized alphabetically by brand.

Learn how CarEdge can make car buying easy as can be with free and premium car buying help. Don’t go it alone in today’s market!

If you’re shopping for a new car this Memorial Day, zero percent financing deals are where the real savings are—especially with interest rates still as high as they are. These APR offers can save you thousands over the life of your loan, but keep in mind that most are limited to well-qualified buyers and specific models.

📍 Want to see what’s available near you?

Check local listings and financing deals with CarEdge to find your best options.

💬 Need help negotiating your financing terms?

Let CarEdge’s Car Buying Experts handle the heavy lifting. Learn more here →

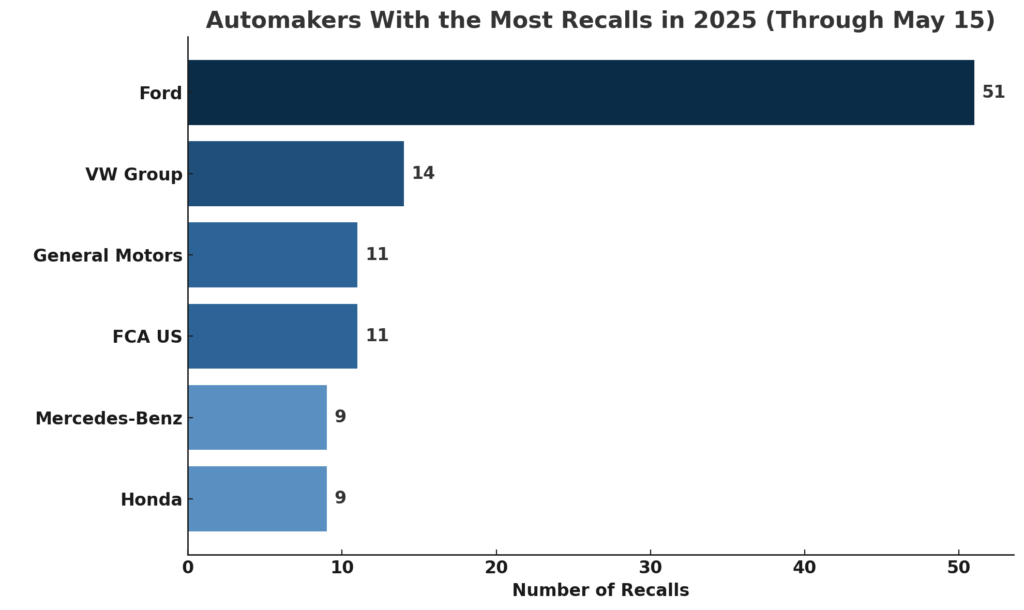

When it comes to vehicle recalls, 2025 is already shaping up to be a wild year. Some automakers are off to a rough start with multiple high-impact recalls, while others seem to be staying clear of trouble—for now. Let’s take a closer look at which automakers are facing the most scrutiny from regulators and what drivers need to know.

Last year, Stellantis unseated Ford as the automaker with the highest number of recalls, issuing 71 in total. In 2025, Ford Motor Company is once again leading the industry in total recalls, according to NHTSA reporting. As of May 15, Ford has issued 51 recalls, affecting over 1.8 million vehicles. That’s more than double the number of vehicles recalled by the next automaker on the list.

It’s been the year of the seatbelt recall for Ford. Models like the Explorer, Aviator, Expedition, and Navigator have all faced recalls for seatbelt-related issues that could compromise passenger safety.

Here are the Ford vehicles with the most recalls in 2025 (so far):

Check if your Ford vehicle is included in recalls.

With 14 recalls affecting 441,587 vehicles, Volkswagen Group isn’t having an easy 2025 either. Several major recalls have affected both Volkswagen and Audi models.

One of the strangest recalls this year? The all-electric Volkswagen ID.BUZZ was recalled because its third-row bench seat is too wide for the number of seatbelts provided. That’s…not something we see every day.

Top VW models with the most recalls:

Check if your Volkswagen vehicle is included in recalls.

General Motors has issued 11 recalls so far, affecting 773,033 vehicles. A massive recall of nearly 600,000 full-size trucks and SUVs equipped with the 6.2L V8 engine is the biggest driver of that number.

The reason? A defect in the connecting rod and crankshaft could lead to engine damage—or worse, complete failure.

GM models with the most recalls:

Check if your GM vehicle is included in recalls.

FCA US (now part of Stellantis) also lands on the list with 11 recalls, covering 140,197 vehicles. The most notable is the recall of 63,000 Jeep Cherokees that may lose drive power due to a faulty power transfer unit.

Models most affected by FCA recalls:

Check if your Jeep, Ram, Dodge, or other FCA vehicle is included in recalls.

So far in 2025, Mercedes-Benz has issued 9 recalls for just 37,563 vehicles. Some were fairly routine, like a recall for S-Class brake fluid leaks, but others were more concerning—like fire risks related to the high-voltage batteries in some electric models.

Vehicles impacted include:

Check if your Mercedes-Benz is included in recalls.

Honda has also logged 9 recalls this year, affecting 469,289 vehicles. The most significant issue? A software glitch in the fuel injection system that may cause engine stalling or a complete loss of power in newer Honda Pilot and Acura MDX models.

Honda models with the most recalls:

Check if your Honda is included in recalls.

Not every brand has had a tough year. A few automakers have managed to keep their recall numbers remarkably low so far in 2025.

Here are the major automakers with the fewest recalls through mid-May:

Keep in mind that some brands like Tesla may issue software-based recalls that don’t require a service visit. Still, fewer recalls generally signal stronger quality control—or fewer reported issues.

If you’re worried your vehicle might be affected by one of this year’s recalls, don’t wait. Check your VIN for free using the NHTSA Recall Lookup Tool.

And if you’re shopping for a vehicle and want to avoid future headaches, be sure to research recall history, reliability, and maintenance costs with CarEdge Research. Whether you’re buying used or new, making an informed choice starts with knowing the facts.