CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

The Ford F-150, America’s best-selling truck, could be facing significant price hikes in 2025 due to increased tariffs on aluminum and steel. The Trump administration has implemented a 25% tariff on all aluminum and steel imports, creating cost pressures for automakers that rely heavily on these materials. Here’s how Ford’s production lines will be impacted, and how consumers may end up paying more for the F-150 in 2025.

On March 13, a 25% tariff on all aluminum and steel imports went into effect. This follows the 2018 tariffs imposed by President Trump, which included a 25% tariff on steel and a 10% tariff on aluminum imports. This time, the impact on vehicle prices could be greater.

Automakers have grown more reliant on aluminum in recent years, particularly for trucks like the F-150 and Super Duty models, which use extensive aluminum in their bodies, hoods, and beds. According to Barclays research reported in the Wall Street Journal, these tariffs could add an average of $400 in material costs per vehicle—a cost that will likely be passed on to consumers.

Ford has been working with suppliers to stockpile aluminum as trade uncertainties linger. However, a Ford spokesperson acknowledged that shifting to U.S.-sourced aluminum would take years. While Ford sources 90% of its steel domestically, most high-quality automotive aluminum originates from Canada.

Sales of Ford’s F-Series trucks have declined slightly over the past five years, dropping from 896,526 units sold in 2019 to 834,641 in 2024. At the same time, base prices have surged by 30%, while prices for the popular Lariat trim have jumped by 55%. Whether F-150 buyers will tolerate additional price increases remains uncertain.

Ford is one of the automakers with the highest car price inflation in recent years. Other truck-focused OEMS, like Stellantis and General Motors, have also raised prices more than competitors.

Adding to the complexity, inventory levels are unusually high, with 145 days of market supply nationwide for the F-150 in March 2025. This oversupply could act as a deterrent to further price hikes—at least for now. However, if production costs continue rising due to tariffs, automakers may still decide to pass some of these costs onto buyers.

Aluminum-intensive vehicles like the F-150 and Super Duty pickups are at particular risk of cost inflation. The auto industry has increased aluminum usage by 30% over the past decade, primarily to improve fuel efficiency and reduce weight. However, U.S. aluminum production has declined, making imports more essential than ever.

The last time similar tariffs were imposed in 2018, Ford and General Motors both reported billion-dollar losses due to rising material costs. Spot prices for steel hit a decade-high before demand collapsed, leading to steel industry cutbacks. Automakers are concerned about a repeat scenario, where higher prices could hurt sales and profitability.

The best strategy for F-150 shoppers in 2025 is to identify aging inventory. These trucks will always be the most negotiable, as dealership floorplanning costs add up in today’s high-interest rate environment. Online tools make it easier than ever to find the most negotiable new and used vehicles for sale. With negotiation know-how, truck buyers can walk away with thousands of dollars in savings.

Drivers who are tired of haggling and dealership visits can even have a pro negotiate your deal. There’s no excuse for overpaying for a truck in 2025!

Auto industry leaders have voiced concerns over the lack of domestic aluminum supply, noting that Canada supplies 75% of the U.S.’s primary aluminum. Alcoa, the world’s 8th-largest aluminum exporter, has pushed for Canadian exemptions, arguing that domestic production cannot meet demand.

Jean-Marc Germain, CEO of aluminum roller Constellium, told the Wall Street Journal that he supports long-term tariffs. However, he warns that imposing a 50% levy on Canada would only drive more imports from other countries.

With these tariffs in place, Ford and other automakers will have to adjust their pricing strategies in 2025 and beyond. F-150 buyers should brace for higher costs in the near future if tariffs continue.

Also: Here’s every car and truck built in Canada, Mexico, and China for sale in the U.S.

Looking to score a great deal on a new car in 2025? Some models will be tougher to negotiate than others. High demand, limited production, and niche appeal make these vehicles nearly impossible to get below MSRP. Our CarEdge Concierges, who negotiate deals every day for our top-rated car buying service, have identified these as the hardest cars to negotiate this year. If you’re shopping for one of these, expect stiff competition and minimal discounts. Let’s take a look at the toughest cars to negotiate this year.

Tough to find trims: Core, Circuit Edition, MORIZO Edition

Why it’s tough to negotiate: The GR Corolla is a specialty entry-level sports car with few direct competitors. Demand is high, and Toyota isn’t flooding the market with them.

Tough to find trims: Manual transmission versions

Why it’s tough to negotiate: With only 211 units available on dealer lots in March 2025, this performance coupe remains in limited supply. Manual Supras are toughest to negotiate right now.

Tough to find trims: All trims

Why it’s tough to negotiate: Toyota’s revived off-roader has just 9,000 units available and a mere 64 days of market supply—making it one of the hardest vehicles to find at a discount.

Tough to find trims: TRD Pro

Why it’s tough to negotiate: While the base Tundra is more available, the off-road-ready TRD Pro model remains a top choice, keeping prices high.

Tough to find trims: SE, XSE

Why it’s tough to negotiate: The RAV4 Prime is one of the best-selling plug-in hybrids, making it hard to find at a discount. Some buyers even put down deposits before the cars arrive.

Tough to find trims: Platinum, Limited

Why it’s tough to negotiate: As a rare three-row hybrid SUV without minivan styling, the Highlander Hybrid has just 1.5 months of supply, far below industry averages.

Tough to find trims: All trims

Why it’s tough to negotiate: The RX is already Lexus’ best-seller. With the hybrid powertrain, it gets even more attention thanks to impressive fuel economy.

Tough to find trims: F Sport, Premium

Why it’s tough to negotiate: Entry-level luxury combined with hybrid efficiency makes this a sought-after model with little room for price negotiations.

Tough to find trims: All trims

Why it’s tough to negotiate: The GX is essentially a luxury Land Cruiser, making it highly desirable. Expect to pay well over the $65,200 starting price.

Tough to find trims: All trims

Why it’s tough to negotiate: As the best value in the Defender lineup, this model has high demand and little incentive for dealers to discount it.

Tough to find trims: Autobiography

Why it’s tough to negotiate: The Autobiography trim is the most sought-after Range Rover spec, ensuring demand stays high.

Tough to find trims: Autobiography, First Edition

Why it’s tough to negotiate: Popular trims mean buyers have little leverage in negotiations.

Tough to find trims: V

Why it’s tough to negotiate: Starting at $162,000, this high-performance Escalade is a low-volume model, meaning dealers have no problem selling them at MSRP or higher.

Why it’s tough to negotiate: The Raptor is a specialty off-road truck with a loyal following. Out of 134,000 new F-150s available, only 3,390 are Raptors, making them a rare find at a discount.

If you’re set on buying one of these high-demand models, here are a few strategies to improve your chances:

Before committing, use CarEdge’s free tools to compare total ownership costs, including maintenance, insurance, and depreciation.

Tired of the car buying hassle? No problem – we’re happy to do the negotiating for you. Learn more about CarEdge’s Car Buying Service.

Some of the best SUVs, electric vehicles, and full-size trucks are available with steep discounts in March. Automakers are ramping up discounts to combat sluggish sales, with cash incentives reaching as high as $10,000 off MSRP. We’ve rounded up the 10 best cash discounts available this month, with savings that could make a serious dent in your out-the-door price. Keep in mind that most of these offers expire at the end of March, so if you see something you like, act fast.

Don’t shop without your personal buyer’s guide (100% Free)

March Savings: Up to 20% off MSRP

Offer valid through: 3/31/2025

Jeep Gladiator Base MSRP: $53,590

Estimated Price with Savings: $43,000

If you’ve been eyeing a Jeep Gladiator, now is the time to buy. Jeep is slashing 20% off MSRP for the 2024 Gladiator Rubicon 4×4. The reason is simple: 2024 inventory is lasting deep into 2025, and it’s time to clear out last year’s Jeeps before summer arrives.

Compare Jeep Gladiator depreciation, cost of ownership, and more

March Savings: $10,000 Customer Cash

Offer valid through: 4/30/2025

Kia EV6 Base MSRP: $42,600

Estimated Price with Savings: $32,600

Kia is offering a massive $10,000 cash discount on its much-loved EV6 crossover. The 2025 EV6 is almost here, and will arrive with a minor facelift. However, this model refresh presents a big opportunity for savings. If you’re looking for an electric vehicle with 300 miles of range, fast-charging (10-80% in as little as 20 minutes), and a futuristic interior, the 2024 Kia EV6 is one of the best deals available.

See Kia EV6 listings in your city

March Savings: $10,000 off MSRP

Offer valid through: 4/30/2025

Kia EV9 Base MSRP: $54,900

Estimated Price with Savings: $44,900

Kia isn’t stopping at the EV6—its three-row EV9 is also getting a $10,000 customer cash discount. This all-electric SUV offers spacious seating, cutting-edge tech, and up to 304 miles of range. The only 3-row SUVs on the market today are the Tesla Model X, Rivian R1S, Volkswagen ID.Buzz, and the Kia EV9. Among these, the EV9 charges the fastest AND has the lowest price tag.

See discounted Kia EV9 listings in your city

March Savings: Up to $10,000 on the 2024 Hornet R/T eAWD

Offer valid through: 3/31/2025

Dodge Hornet Base MSRP: $41,400

Estimated Price with Savings: $31,400

The Dodge Hornet has been struggling to sell, and Stellantis is now offering a variety of stacked incentives to move inventory. With up to $10,000 in potential savings, including lease loyalty bonuses, it’s a great time to grab this performance-focused compact SUV. A plug-in hybrid powertrain comes standard with the Hornet R/T.

Compare Dodge Hornet listings in your city

March Savings: Up to $7,000 off MSRP, or $10,500 in lease incentives

Offer valid through: 3/31/2025

Jeep Wrangler 4xe Base MSRP: $50,695

Estimated Price with Savings: $43,695

Wrangler fans take note: Jeep is offering $7,000 in cash savings on the 2025 Wrangler Sahara 4xe. If leasing is your preference, you can qualify for up to $10,500 in lease bonus cash. The Wrangler 4xe is a rare blend of off-road ability and electrification, and these incentives make it more affordable than ever.

Compare Jeep Wrangler depreciation, cost of ownership, and more

March Savings: $9,000 off MSRP

Offer valid through: 3/31/2025

Jeep Grand Cherokee Base MSRP: $36,495

Estimated Price with Savings: $27,495

Jeep is pushing hard to sell its remaining 2024 Grand Cherokees with a $9,000 cash bonus for current FCA lessees. This is a great opportunity to drive home a legendary midsize SUV with a refined interior and modern tech, now with a huge discount.

Compare Jeep Grand Cherokee depreciation, cost of ownership, and more

March Savings: Up to $7,850

Offer valid through: 3/31/2025

GMC Sierra 1500 w/ TurboMax Base MSRP: $44,895

Estimated Price with Savings: $37,045

GMC is offering up to $7,850 in total savings on the 2025 Sierra 1500, including a $6,500 purchase allowance and an engine credit. With truck prices remaining high, this March discount helps offset the cost of a well-equipped full-size pickup.

Compare GMC Sierra 1500 depreciation, cost of ownership, and more

March Savings: $7,500 off MSRP

Offer valid through: 3/31/2025

Nissan Ariya Base MSRP: $39,590

Estimated Price with Savings: $32,090

Nissan is compensating for the Ariya’s lack of a federal EV tax credit with a $7,500 customer cash incentive. It may not be the fastest-charging electric crossover in 2025, but with this cash discount, it’s an attractive bargain, especially for city driving.

See Nissan Ariya listings in your city

March Savings: $7,500 off MSRP

Offer valid through: 3/31/2025

Chrysler Pacifica PHEV Base Price: $51,055

Estimated Price with Savings: $43,555

Minivan buyers can take advantage of a $7,500 customer cash offer on the plug-in hybrid Pacifica, with additional tax incentives available. This is a great chance to drive home a fuel-efficient, family-friendly hybrid minivan at a major discount.

Compare Chrysler Pacifica depreciation, cost of ownership, and more

March Savings: $6,500 off MSRP

Offer valid through: 3/31/2025

Ram 1500 Lone Star Crew Cab Base Price: $45,230

Estimated Price with Savings: $38,730

Ram’s $6,500 cash allowance on the 2025 1500 Lone Star Crew Cab 4×2 includes multiple stackable incentives. In March 2025, Ram buyers can take advantage of National Retail Consumer Cash ($4,000), National Bonus Cash ($1,500), National Truck Month Bonus Cash ($1,000). This is the best deal on a 2025 model year truck right now.

Compare Ram 1500 depreciation, cost of ownership, and more

March is turning out to be a great time to save big on a new car or truck. The hefty cash discounts this month aren’t just random generosity from automakers. A few key factors are driving these deep price cuts:

At CarEdge, we help you make the most of these discounts. Before you buy, check out our real-time market insights, depreciation forecasts, and cost-of-ownership analysis to ensure you’re getting the best deal possible. Plus, we can connect you with local inventory and expert guidance to help you negotiate even more savings.

These March deals won’t last forever, so if you see a car you like, act fast and let CarEdge help you buy smart!

Spring car buying season is here, and many shoppers are heading to dealerships with their tax refunds in hand, ready to make a down payment on a used car. According to a recent survey by Talker Research, Americans expect to receive an average refund of $1,700 this year. With the average price of a used car sitting at $25,128 in March 2025, a solid down payment can help offset high borrowing costs.

However, used car shoppers are facing an unpleasant reality: the highest used car loan rates in over 40 years. Rising interest rates are making monthly payments significantly more expensive in 2025, tightening budgets for many buyers. Before financing a used car this spring, it’s crucial to understand how today’s high APRs will impact your loan – and what steps you can take to minimize costs. Here’s what to expect and how to protect your wallet.

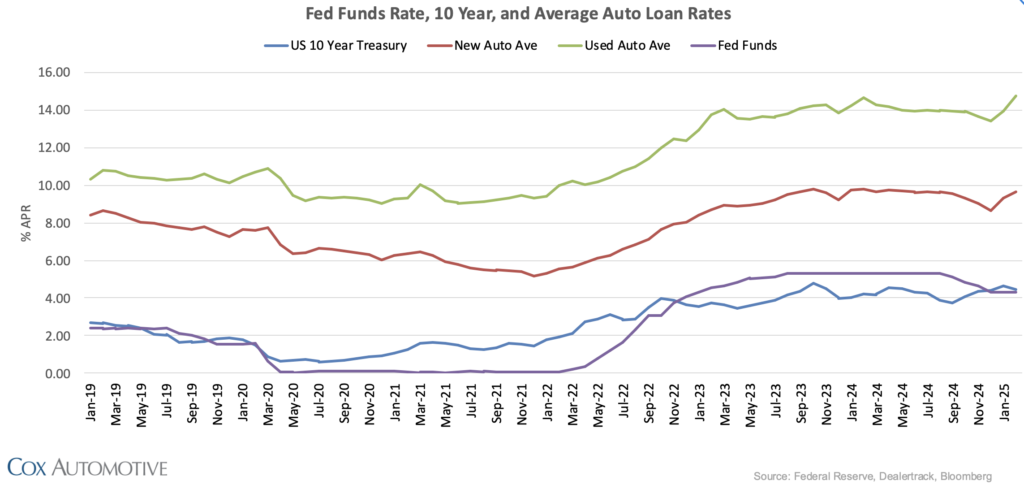

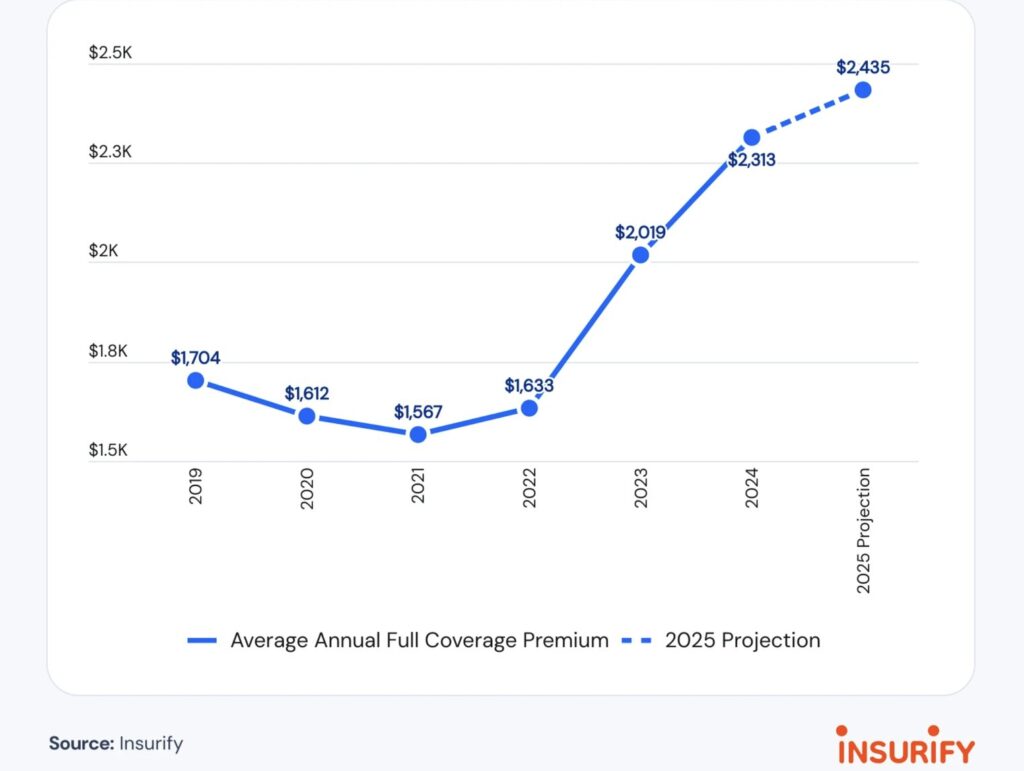

Over the past year, used car prices have fluctuated but have generally trended lower. While this is good news for buyers, the cost of financing remains a major hurdle. Used car loan rates have surged to levels not seen since the early 1980s.

After a brief dip in December, interest rates jumped sharply in January and February. According to Cox Automotive, the average used car loan rate in March 2025 is now 14.73% APR. For comparison, new car rates sit at 9.69% APR on average.

For buyers with lower credit scores, the situation is even worse. Many subprime borrowers are being offered rates close to 20% APR – adding thousands of dollars in interest over the life of a loan.

It’s hard to fathom just how much high interest rates can quickly add up, adding thousands of dollars to the total cost of owning a car. Consider the following real-world example: A $25,000 used car loan financed for 72 months at a 15% APR interest rate will accumulate $13,000 in total loan interest over 72 months. For buyers with bad credit, a 20% APR loan rate would push the interest paid above $18,000 for the same loan amount. Buying a car at all starts to lose its appeal with rates at these levels.

Several factors are keeping borrowing costs elevated in 2025:

While the overall rate environment isn’t favorable, car buyers can take steps to secure the best financing possible. Here’s how:

Check Your Credit Score Before Shopping: Your credit score plays a major role in determining your interest rate. Scores above 700 typically secure the best rates, while subprime borrowers (below 600) face the steepest costs. Your debt-to-income ratio is also a key consideration.

Get Pre-Approved by a Credit Union or Local Bank: Credit unions often offer lower rates than dealership financing. Getting pre-approved also gives you negotiating power when discussing financing options with dealers.

Make a Larger Down Payment: The more cash you put down, the less you have to borrow – reducing your interest charges over time. With tax refunds arriving, consider using that money to increase your down payment.

Choose a Shorter Loan Term: A 36- or 48-month loan will come with a lower interest rate than a 72- or 84-month loan. While monthly payments will be higher, you’ll save money on interest in the long run.

Avoid Add-Ons That Increase Loan Costs: Extended warranties, service contracts, and dealer add-ons can be financed into your loan, but this increases the total amount borrowed – and the interest you’ll pay.

👉 Before you commit to a used car with a high APR, drivers with good credit should check out the Best New Car Financing Incentives This Month. For well-qualified buyers, there are plenty of low-APR and even zero percent APR deals out there!

Take our free car buyer’s guide with you to save more and buy with confidence.

With used car loan rates at historic highs, some drivers may be better off repairing their current vehicle rather than financing a new one.

If your car is paid off or close to being paid off, investing in repairs can be far cheaper than taking on a high-interest loan. Consider getting a repair estimate before deciding whether to trade in or keep your car.

Always consider the total cost of ownership before buying any car. Use these free cost of ownership tools to see the numbers – you might be shocked at what you find!

👉 The Best Used Cars Under $10,000

Used car prices are coming down slowly, but financing costs remain a major challenge in 2025. With average used car loan rates nearing 15% APR for the first time in 40 years, shoppers need to be strategic about where they finance and how much they borrow.

If you’re planning to buy a used car this spring, use tools like CarEdge’s Free Car Buying Guide to compare financing options and find the most negotiable deals. Knowledge is your best tool to fight back against high borrowing costs. Don’t head to the dealership without a plan!

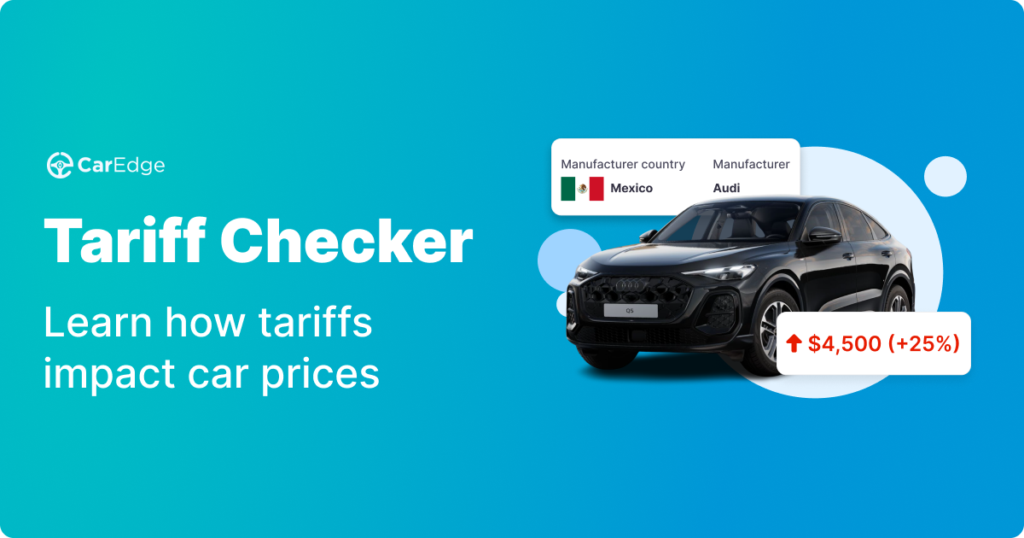

If you’re in the market for a new car or truck, possible price hikes should be on your radar. In 2025, 25% automotive tariffs are officially here. In a shift from previous tariffs, the new auto tariffs apply to all vehicles imported into the United States. However, cars imported from Mexico, Canada, and China are likely to be most impacted due to the complexity of North American supply chains. Here’s what car buyers should know as spring car buying season gets underway.

Several of the most popular new cars and trucks sold in the U.S. are manufactured or partly assembled in Canada, Mexico, and China. However, the impacts of tariffs on the U.S. auto industry are much more wide reaching than it may seem on the surface. This is due to closely intertwined automotive supply chains spanning the three North American manufacturing hubs.

A new report from S&P Global Mobility forecasts that lost production due to tariffs could reach 20,000 units per day that are not built. This would equate to one third of North American vehicle production being lost due to tariffs.

It remains unclear how quickly consumers will begin to see higher sticker prices and lower incentives. What we do know is which new cars and trucks are most severely impacted. Here’s a look at some of the models now facing higher costs due to the tariffs, including average selling prices and market supply data as of spring 2025.

The following new cars, SUVs, and trucks are manufactured in Mexico, and sold in the United States. Note that many other models contain parts that are manufactured in Mexico and imported into the U.S. for final assembly.

| Make | Model | Country of Origin | Average Selling Price | Days of Supply | Total For Sale | 45-Day Sales Total |

|---|---|---|---|---|---|---|

| Audi | Q5 | Mexico | $58,462 | 74 | 7,765 | 4,697 |

| BMW | 3 Series | Mexico | $55,598 | 121 | 5,067 | 1,890 |

| BMW | 2 Series Coupe | Mexico | $49,663 | 186 | 4,106 | 996 |

| Chevrolet | Silverado 1500 | U.S. and Mexico | $54,508 | 129 | 84,463 | 29,359 |

| Chevrolet | Equinox EV | Mexico | $42,944 | 101 | 8,327 | 3,699 |

| Chevrolet | Blazer EV | Mexico | $49,635 | 195 | 11,215 | 2,584 |

| Ford | Bronco Sport | Mexico | $33,689 | 175 | 43,625 | 11,198 |

| Ford | Maverick | Mexico | $34,541 | 142 | 34,977 | 11,097 |

| Ford | Mustang Mach-E | Mexico | $48,137 | 89 | 10,161 | 5,109 |

| GMC | Sierra 1500 | U.S. and Mexico | $62,381 | 108 | 48,095 | 20,013 |

| Honda | Prologue | Mexico | $54,310 | 179 | 11,775 | 2,953 |

| Kia | K4 | U.S. and Mexico | $25,267 | 75 | 19,274 | 11,507 |

| Nissan | Sentra | Mexico | $23,813 | 155 | 31,396 | 9,099 |

| Nissan | Kicks | Mexico | $25,756 | 120 | 25,519 | 9,535 |

| Ram | Ram 1500 | U.S. and Mexico | $58,431 | 133 | 51,508 | 17,400 |

| Ram | Ram 2500 | Mexico | $65,058 | 106 | 20,085 | 8,526 |

| Ram | Ram 3500 | Mexico | $71,664 | 124 | 11,388 | 4,145 |

| Toyota | Tacoma | Mexico | $46,796 | 54 | 55,021 | 45,724 |

| Volkswagen | Jetta | Mexico | $26,157 | 90 | 9,216 | 4,616 |

| Volkswagen | Tiguan | Mexico | $32,995 | 68 | 11,491 | 7,615 |

| Volkswagen | Taos | Mexico | $29,145 | 152 | 14,497 | 4,305 |

All prices and market data are as of March 3, 2025, reflecting the state of the car market before tariffs officially began.

In 2025, 20 models of new cars, SUVs and trucks are manufactured in Mexico for export to the United States. The automakers likely to be hardest hit by President Trump’s tariffs are Nissan, Volkswagen, Ford, and General Motors. Due to Volkswagen’s smaller model lineup, the German automaker will feel an outsized impact with three popular models being produced in Mexico.

Buyer’s looking for one of the more affordable new cars on sale today will be impacted by tariffs. Three popular models among budget buyers are all produced in Mexico: the Nissan Kicks, Nissan Sentra, and the new Kia K4. Finding a new car under $25,000 will become even more difficult in 2025 due to tariffs.

In 2023, the United States imported 141,847 motor vehicles and parts from Canada, a record high. These new cars are manufactured at facilities located in Ontario, with a large portion exported to the United States. As of the most recent data, the U.S. was the largest market for Canadian automotive exports, making up 62% of total auto exports. Here are all of the cars and trucks manufactured in Canada for export to the U.S. in 2025:

| Make | Model | Country of Origin | Average Selling Price | Days of Supply | Total For Sale | 45-Day Sales Total |

|---|---|---|---|---|---|---|

| Chrysler | Pacifica | Canada | $47,483 | 125 | 7,717 | 2,783 |

| Chrysler | Voyager | Canada | $41,815 | 178 | 1,218 | 308 |

| Dodge | Charger | Canada | $54,189 | 239 | 7,298 | 1,372 |

| Honda | CR-V | U.S. and Canada | $37,967 | 66 | 56,300 | 38,135 |

| Honda | Civic | U.S. and Canada | $28,783 | 59 | 21,550 | 16,553 |

| Lincoln | Nautilus | China and Canada | $61,047 | 219 | 16,457 | 3,375 |

Stellantis and Honda will be hardest hit by tariffs on Canada in 2025. The Civic and CR-V are top-sellers for Honda. As models known for their affordability and overall value, it will be interesting to see if Honda Motor American Honda Motor, the North American branch of Honda Motor Company, decides to pass import tariffs on to car buyers in the form of MSRP hikes or severe reductions in incentives.

Continue to check back each week as we monitor the real-time impact of tariffs on car prices for these affected models.

Just a handful of new cars are produced in China for export to the United States. The following models will be subject to the 10% tariff on imports from China:

Polestar, no longer under Volvo’s umbrella, is going to be hit the hardest from the tariffs on Chinese imports. Sales of Polestar’s electric vehicles have already been falling in North America due to competitors with faster charging, more driving range, and lower price tags. If tariffs continue for months on end, it’s not clear if Polestar will see 2025’s challenges as reason enough to exist the North American market entirely to focus on more favorable tides in Europe and Asia.

If you’re shopping for a new car, here’s what you need to know:

These tariffs are already reshaping the auto market, and will cost both consumers and automakers money. Whether automakers shift production to the U.S. in response remains to be seen, but for now, buyers should be prepared for rising costs in the form of rising MSRPs and a reduction in incentives, like zero percent financing.

If you have been considering shopping around for a better insurance rate, now is the time. Tariffs are likely to drive premiums even higher in 2025 as car parts are subjected to the levy. Compare quotes today to lock in your rate before the coming hikes.

CarEdge will continue tracking these developments and providing insights on how they affect car prices, financing, and buying strategies. Stay informed, and check out our free car buying tools to help you navigate the challenges ahead for car buyers in 2025.

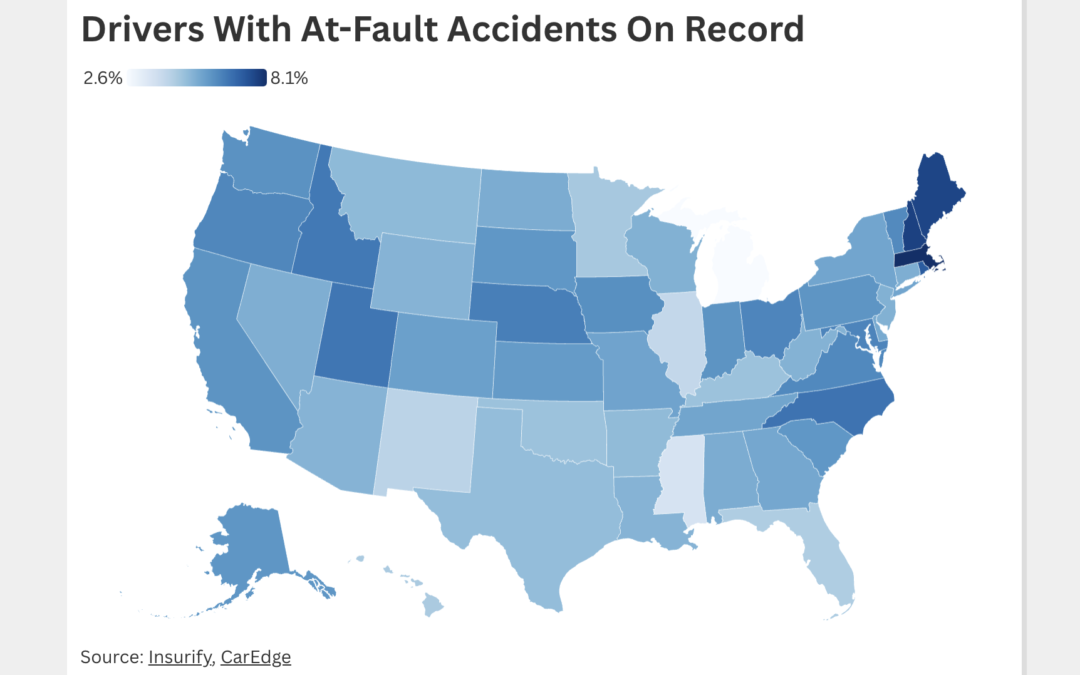

Auto insurance rates are climbing in 2025, and while that’s no surprise to most drivers, what might shock some is which states have the highest accident rates. Car accidents are a major factor driving insurance premiums higher, but they aren’t the only culprit. Rising car prices, increased repair costs, and even tariffs map push rates higher this year.

Using Insurify’s latest insurance data, we’ve identified the states with the most at-fault accidents in 2025 — and the states where drivers are least likely to be involved in a crash.

Insurify, a digital insurance marketplace licensed in all 50 states, connects drivers with quotes from over 100 providers. Thanks to this expansive data set, Insurify is able to track national trends, offering a unique look at which states have the highest accident rates.

Nationally, 5.3% of drivers have an at-fault accident on their record. But in some states, that number is significantly higher.

New England stands out as the region with the most accident-prone drivers. Massachusetts takes the top spot, with 8.1% of drivers having an at-fault accident on their record. New Hampshire follows closely behind at 7.7%, while Maine rounds out the top three at 7.6%. Rhode Island also ranks in the top five, with 7.1% of drivers reporting accidents.

North Carolina is the only non-New England state in the top five, with 6.6% of drivers having an at-fault accident on record.

Here’s a look at the 10 states with the highest accident rates in 2025:

| State | Drivers with At-Fault Accidents |

|---|---|

| Massachusetts | 8.05% |

| New Hampshire | 7.67% |

| Maine | 7.59% |

| Rhode Island | 7.12% |

| North Carolina | 6.61% |

| Utah | 6.56% |

| Idaho | 6.49% |

| Nebraska | 6.36% |

| Maryland | 6.26% |

| Ohio | 6.23% |

Source: Insurify data

On the other end of the spectrum, some states report far fewer accidents. Whether due to lower population density, better infrastructure, or safer driving habits, these states see fewer crashes than the national average.

Michigan has the lowest rate of at-fault accidents in the country, with just 2.6% of drivers having one on their record. Mississippi follows at 3.6%, while Illinois and New Mexico also rank among the least accident-prone states.

Interestingly, Florida, often criticized for aggressive driving, high insurance costs, and outrageous dealership fees, is also among the states with lower accident rates, at just 4.5%. This suggests that while Florida has unique insurance challenges, at-fault accidents aren’t the primary issue.

Here’s how all 50 states and the District of Columbia rank in terms of drivers with at-fault accidents on their record, as of 2025:

The visualization above was produced by CarEdge using Insurify data.

Having an at-fault accident on your record can significantly increase your car insurance premiums. On average, drivers who cause an accident see their rates rise by $800 or more per year, depending on the severity of the crash and their insurance provider. These rate hikes typically last three to five years before gradually returning to normal—assuming no additional accidents occur.

But even drivers with clean records aren’t immune to rising premiums. Insurance companies set rates based on the overall risk in a given area. If a state or city experiences high accident rates, insurers adjust their pricing accordingly to offset increased claim payouts. That means even if you’ve never been in an accident, living in a high-risk state could mean paying more for coverage.

If your rates have gone up, it may be time to compare insurance quotes and explore ways to lower your premium. Shopping around, maintaining a clean driving record, and improving your credit score can all help keep costs down in 2025. Stay safe out there!

![Reviewed: 5 Best Instant Cash Offer Sites to Sell Your Car [2025]](https://caredge.com/wp-content/uploads/2023/11/Image-1080x675.png)

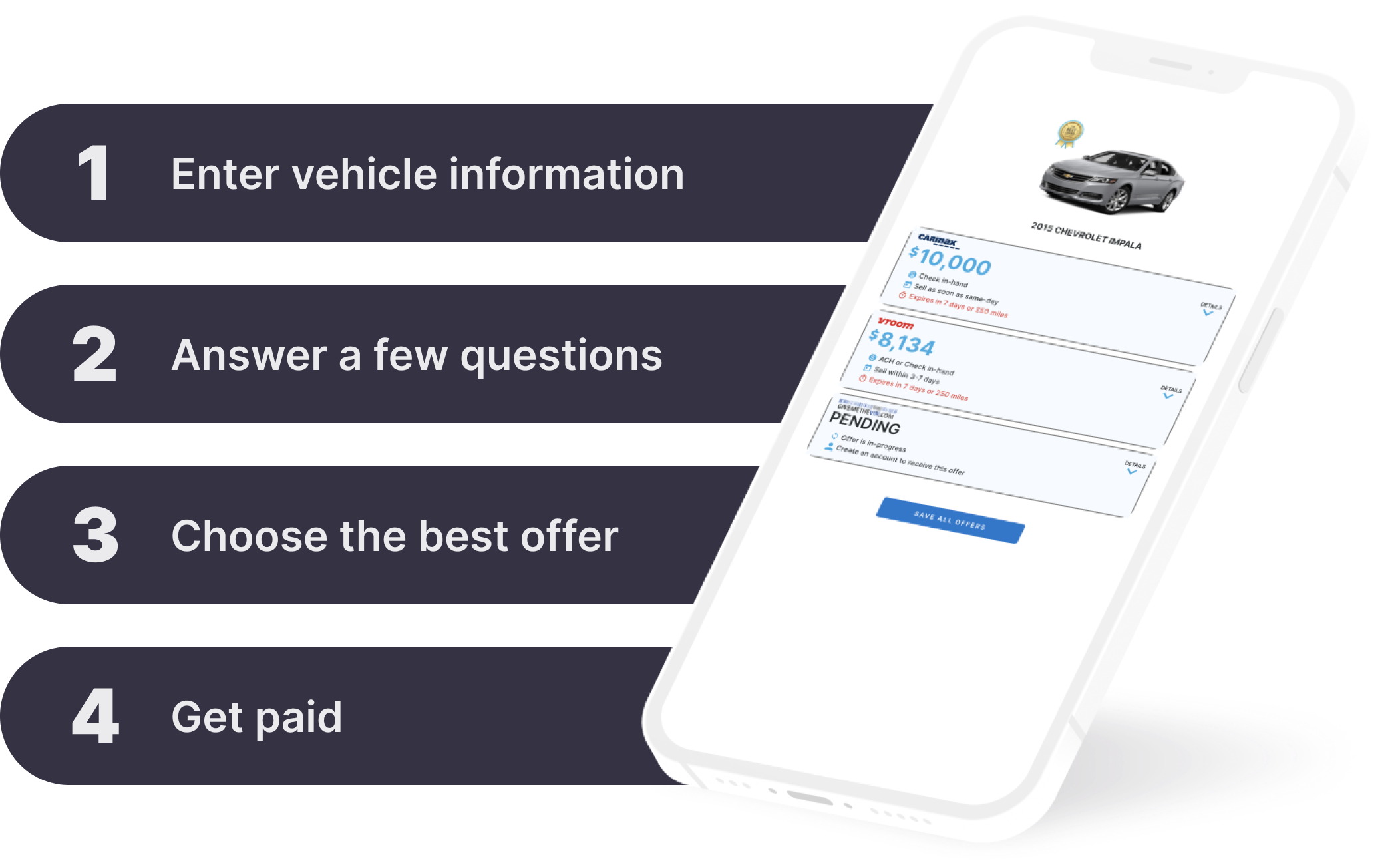

If you’re looking to sell your car quickly and hassle-free, getting an instant cash offer for a car can be one of the easiest ways to do it. Instead of haggling with private buyers or trading in for a low-ball offer, these online platforms provide an upfront price based on your vehicle’s details. But which services are worth considering? We’ve reviewed five of the best options to help you get the most for your car in 2025.

Summary: CarEdge provides a transparent process for selling your car by offering market-based pricing insights and connecting you with vetted buyers. With a data-driven approach, CarEdge ensures you get a competitive instant cash offer while giving you the tools to make an informed decision.

CarEdge’s instant cash offer is sourced from three trusted partners: Peddle, givemethevin.com, and webuyanycar.com.

Pro:

Cons:

The Verdict: CarEdge is a great choice for sellers who want a transparent, data-driven approach to getting the best instant cash offer for their car.

Summary: CarMax is a well-known brand that offers a straightforward process for selling your vehicle. By entering your car’s details online, you’ll receive an instant cash offer that you can redeem at any of the 253 CarMax locations nationwide. The offer is valid for seven days, giving you time to compare deals.

Pro:

Cons:

The Verdict: CarMax is a great option for those who prefer an established company and don’t mind visiting a physical location to complete the sale. However, it can come with the unpleasant dealership experience that most drivers prefer to avoid.

Summary: Carvana provides a completely online selling experience. You enter your car’s details, receive an offer, and if you accept, Carvana will pick up your vehicle and issue payment, with no need to visit a dealership. Note that Carvana’s instant cash offers are known to fluctuate from day to day.

Pro:

Cons:

The Verdict: Carvana is a good option for sellers who want a fully digital, contact-free process. However, sellers should be aware that offers can fluctuate wildly day to day, depending on market conditions. Compare quotes from other instant cash buyers before you commit.

Summary: Kelley Blue Book (KBB) provides a tool that generates an instant cash offer based on your car’s details and market value. This offer can be redeemed at participating dealerships after an inspection.

Pro:

Cons:

The Verdict: KBB Instant Cash Offer is a great option for those who prefer to sell their car through a well-known website with multiple dealership options. It’s not recommended for sellers who prefer to stay away from the dealership experience.

Summary: EchoPark provides an instant cash offer online, valid for seven days or 500 miles. If you sell your car to EchoPark within 48 hours of receiving the offer, they’ll add an extra $250 to your payment. However, you must bring your car to an EchoPark location to finalize the deal.

Pro:

Cons:

The Verdict: EchoPark is a strong option for sellers who live near one of its locations and want to maximize their offer with the $250 bonus incentive.

The best option depends on your priorities. If you want the best offer without dealership hassles, CarEdge is a great option. With CarEdge’s car value tracking tool, you can see your car’s value change in real time. This makes it easier to decide when to sell. If you prefer a traditional dealership experience, CarMax or KBB Instant Cash Offer could work better. For those near an EchoPark location, the extra $250 incentive makes it a great pick.

Ultimately, all sellers should compare offers from each of these online car buyers to see where the best deal is. Instant cash offers for cars can vary widely from one buyer to the next.

Walking into a dealership can feel like stepping onto a high-pressure battlefield of negotiations. Salespeople are trained to close the deal quickly, and some will say almost anything to get you to sign on the dotted line. While many sales professionals are honest, there are common tactics designed to rush your decision or make a deal seem better than it really is.

If you’re buying a car in 2025, knowing these five common car salesperson lies can help you negotiate smarter and avoid getting taken for a ride. Don’t forget your custom Car Buying Guide to get the best deal, no matter what you’re in the market for!

This classic tactic creates a false sense of urgency, making you feel like you’ll lose out on a great deal if you don’t act fast. It’s meant to pressure you into making an impulsive decision before you have time to shop around or think things through.

Reality Check: While manufacturer promotions and incentives do expire, dealerships set their own pricing. If a dealer is truly motivated to sell, they’ll likely offer the same deal—or something very close to it—tomorrow, next week, or even next month. If you feel rushed, walk away and take your time.

Salespeople use this line to make you feel like you’re getting an unbelievable bargain. The idea is to make you hesitate to negotiate further, thinking that they’ve already cut the price as low as possible.

Reality Check: Dealerships rarely lose money on a car sale. Between manufacturer rebates, holdbacks, incentives, and extended warranties, dealers have plenty of ways to make up for any so-called ‘loss.’ They wouldn’t stay in business if they were truly selling at a loss, so don’t let this claim stop you from pushing for a better deal.

👉 Use these Car Buying Cheat Sheets to beat the dealer, EVERY time

This tactic plays on ‘fear of missing out’ and is meant to make you feel pressured to buy before someone else does.

Reality Check: Sure, popular models do sell quickly, but unless you’re after an extremely limited or in-demand car, there’s usually another one available. A salesperson may or may not have other interested buyers, but it’s almost always an attempt to rush your decision. If you’re unsure, leave the lot and check the dealership’s online inventory later—chances are, the car will still be there.

This is a classic numbers game. By making you believe you’re getting an above-market offer on your trade-in, the dealer can justify charging more for the new car—or distract you from negotiating on financing terms.

Reality Check: Trade-in values are based on wholesale market prices, not what the dealer “paid.” Often, if a dealer offers a high trade-in value, they make up for it by adding hidden fees, increasing the price of the new car, or adjusting loan terms. Before heading to the dealership, research your trade-in’s true market value using tools like CarEdge Pro so you know what your car is really worth.

👉 Trade-In Tactics For Success (Free Guide)

Salespeople want to minimize concerns about a used car’s reliability. Saying a vehicle has no issues or a clean history can ease doubts and make you more likely to buy without further investigation.

Reality Check: Even if a car has no reported accidents on a Carfax or AutoCheck report, that doesn’t mean it’s problem-free. Hidden damage, flood history, or undisclosed mechanical issues could still exist.

Always get a third-party mechanical inspection (also known as a Pre-Purchase Inspection) before purchasing any used car. It’s a small price to pay to avoid thousands of dollars in unexpected repairs down the road.

👉 Stay on top of your car buying to-do list with this complete checklist!

Car dealerships use pressure tactics to speed up the sale, but with the right preparation, you stay in control. Here’s how to safeguard your purchase and maximize your savings:

Do Your Research – Know the fair market price of the car you’re considering. Use tools like CarEdge behind-the-scenes Pro to check real-time pricing and historical trends.

Take Your Time – If it’s meant to be, it’ll still be there tomorrow. Never feel pressured to buy on the spot. This is especially true of used car purchases.

Negotiate Based on the “Out-the-Door” Price – Dealers add fees, taxes, and extra costs. Always ask for a detailed breakdown of all charges. Use this free Out-the-Door Price Calculator to know what to expect.

Verify Everything – Don’t take a salesperson’s word for it. Get a vehicle history report, read the fine print, and get a pre-purchase inspection for any used car.

Be Ready to Walk Away – The best negotiating tool? Your willingness to leave. If a deal doesn’t feel right, walk away and find a dealership that respects your time and budget.

CarEdge car buying experts are ready to help you save time, a LOT of stress, AND money. Get started today with your FREE Car Buyer’s Guide!

Spring car buying season is almost here, and for shoppers looking to score a deal, March could bring some great opportunities to save. As inventory levels continue to climb for certain automakers, discounts, low APR financing, and lease specials are becoming more generous.

If you’re in the market for a new car, it’s crucial to know which brands are struggling with excess inventory—because that’s where you’ll find the biggest savings. Based on current market data, these five car brands are most likely to offer the best deals in March 2025.

Jeep has been pushing 0% APR financing offers throughout February, and with inventory nearly three times higher than the industry average, these deals aren’t going anywhere anytime soon.

Here’s why we expect Jeep to advertise big incentives in March 2025:

Jeep’s push to move upmarket hasn’t gone according to plan, leaving dealers struggling to sell premium models like the Grand Wagoneer. The result? Deep discounts and aggressive lease deals. If you’re looking for an SUV in March, expect continued 0% APR offers and lease specials across Jeep’s lineup.

Get FREE Pro & Find the BEST Jeep Deals Near You

Nissan’s future in the U.S. is looking more uncertain by the day. Despite offering multiple zero percent financing deals in February, inventory is still piling up.

Nissan’s current inventory situation hints at big discounts to come in March:

Never-ending incentives might be hurting Nissan’s bottom line, but for car buyers, it’s great news. If you’re shopping for a Nissan in March, expect big discounts, low-interest financing, and lease deals to continue as dealers work to offload aging inventory.

Get Your FREE Guide to Buying a Nissan – And Saving More

Hyundai has been steadily building up inventory over the past few months, and now it’s sitting at its highest level in years.

Here’s why we think Hyundai will be one of the automakers with the best deals in March 2025:

In February, Hyundai was offering 2.99% APR for 72 months across most of its lineup. March could bring a return to 0% financing, especially for models like the Santa Fe, Tucson and Elantra. Hyundai is known for aggressive incentives when inventory gets too high, making March a prime time to negotiate a great deal.

Get Your Guide to Hyundai Deals in Seconds!

Ram trucks are sitting unsold, and dealers are desperate to clear them out. This is largely due to declining sales, high prices, and rising competition in the full-size truck segment.

Here’s a look at the current inventory situation:

Part of the problem is that Ram trucks have become increasingly expensive. While the average selling price of a new Ram is just below $60,000, a large portion of their inventory consists of high-end models priced over $80,000. In today’s economic climate, that’s a tough sell—especially with high interest rates making financing more expensive.

In February, Ram is offering 4.9% APR for 72 months, and up to $6,500 in cash allowance. The best truck deals in March are likely to be even better.

See the Best Truck Deals in YOUR ZIP Code

Ford is another automaker with rising inventory in 2025. When supply exceeds demand, incentives make a comeback. That’s exactly what we expect to see in March.

Ford’s Current Inventory Situation:

Ford has been aggressively discounting its EVs, but so far, gas-powered models haven’t seen the same incentives. If inventory continues to rise, expect bigger cash discounts and better financing offers in March.

Compare truck deals in your area (Free Tool)

March 2025 is shaping up to be a great time to buy a new car—but only if you know where to look. Jeep, Nissan, Hyundai, Ram, and Ford are all carrying excess inventory, and dealers will be under pressure to move cars fast. Use tools like CarEdge Pro to find the oldest inventory, and all of the best opportunities for negotiating serious savings.

For car buyers, that means:

– Lower interest rates on financing deals

– Hefty cash discounts on slow-selling models

– More negotiability as dealers work to clear out old stock

🚗 Before you buy, make sure you’re getting the best deal possible. Use CarEdge’s Free Car Buyer’s Guide to compare deals, understand pricing trends, and negotiate like a pro!

Selling cars isn’t a walk in the park in 2025. High interest rates, rising production costs, and fierce competition all make turning a profit a challenge. And then there’s the looming threat of tariffs. These 5 car brands are facing mounting challenges in the U.S. market, creating an increasingly uncertain future. These companies are grappling with rising inventory levels alongside a shrinking customer base as the likes of Toyota, Tesla, and Subaru have gained fans and taken market share. Many have struggled to secure a strong foothold in America, while others are American icons that seem to be on their way out.

The following analysis delves into the factors driving these trends and the implications for each brand. These are the automakers at risk of leaving the U.S. market in the years to come.

Nissan appears to be hurtling toward financial disaster. A merger with Honda has officially fallen through, manufacturing facilities are running well below capacity, and Nissans are sitting on dealer lots for longer than ever before. It’s likely that Nissan’s corporate leadership is considering all options right now. Just this past week, news broke that Honda would reconsider reviving takeover talks if Nissan’s CEO steps down. In November 2024, Nissan CEO Makoto Uchida said that the automaker needed to undertake serious restructuring to get out of what he called an “extremely tough situation.” It’s not yet clear how this will play out for what was once a top-selling automaker.

A look at the numbers puts Nissan’s predicament in focus. In the United States, Nissan is set up for 8.5% market share in terms of dealer footprint and manufacturing capability. Yet, U.S. market share remains low, hovering around 4.5%. There’s a huge mismatch here that can’t continue forever.

The likes of Toyota, Hyundai, Kia, and Subaru have taken market share from Nissan in the U.S. market. Sales haven’t exactly plummeted, but years of declines are starting to add up.

Here’s a look at how Nissan’s U.S. sales have fared compared to it’s immediate competitors over the last decade:

Although U.S. sales have steadily fallen, they’re still selling over 900,000 cars annually. However, Nissan’s corporate leadership has made it crystal clear that the company’s immediate threat is its balance sheet. Last year, an anonymous Nissan official told the Financial Times that the automaker has “12 to 14 months to survive.” A dire situation, indeed.

BMW owns the brand, and could pull the plug if sales continue to wane. Sales have tanked in recent years. It’s clear that Mini lost their niche in the American auto market as their vehicles grew in size. Mini’s best year was back in 2012, with 76,354 U.S. sales. How’s the bigger new model selling? Not well. There’s 188 days of supply for the new Countryman heading into spring car buying season.

Alfa Romeo once had a bright future in North America. Following the brand’s arrival in 2016, sales climbed quickly, and peaked at nearly 24,000 units sold in 2018. However, it’s been steadily downhill ever since. In 2024, Alfa Romeo sold just 8,865 cars in the U.S. The Quadrifoglio versions of the Giulia and Stelvio have officially been canceled, leaving an even narrower lineup for American car buyers.

With recent leadership shakeups at Stellantis, it’s more likely than ever that some brands are on the way out. Alfa Romeo is at the top of that unfortunate list.

Be sure to check out just how far several Stellantis brands have fallen in the interactive graph below.

In 2025, Chrysler is exclusively a seller of minivans. Since the sunset of the Chrysler 300 sedan, the Pacifica and resurrected Voyager are all that’s left. Sales have fallen by 50% over the past decade. With Chrysler’s Airflow EV officially dead, it’s not clear if there’s a future at all for Chrysler.

The good news is that Mitsubishi’s U.S. sales were up in 2025, led higher by sales of the Mirage, the most affordable new car in America. The bad news is that Mirage has officially been cancelled, just as drivers are increasingly desperate for cheap new cars.

Mitsubishi has fallen far behind its Japanese rivals. Back in 2000, Mitsubishi wasn’t too far behind the likes of Toyota, Honda, and Nissan. In 2025, there are only 300 Mitsubishi dealers in the United States, a fraction of the competition’s footprint. It’s not clear if the success of the Outlander will be enough to keep the brand stateside in the long term.

Over the course of the past decade, sales of Jeep, Chrysler, Dodge, and Ram models have fallen sharply. Jeep and Ram remain mainstays in the U.S., but other brands under the Stellantis umbrella have a less certain future. Here’a a look at how sales of Stellantis’ brands have contracted over the last ten years. As you’ll notice, Fiat, Maserati, Chrysler, and Alfa Romeo are just a fraction of today’s market:

Make no mistake: Stellantis is in deep trouble. In the U.S. market, Stellantis (and FCA US) sales are down 42% from 2015 to 2024, tumbling from 2,243,907 vehicles sold in 2015, to just 1,303,570 sold in 2024. New leadership is looking to trim the fat, of which there is plenty in the U.S. market. Alfa Romeo and Chrysler are high on the list, but Fiat and Maserati are the clear runner ups.

Jaguar is essentially taking a year off in 2025, which is without a doubt a bad sign. With electrification progressing slower than anticipated, and sales of ICE models on the decline, it’s not clear if Jaguar will have a future in North America beyond 2025. Jaguar sold just 13,210 cars in America in 2024. That’s not enough to remain relevant in the decade to come.

The writing is on the wall for these struggling automakers. Whether it’s declining sales, bloated inventories, or corporate shakeups, these brands are facing serious uncertainty in the U.S. market. For car buyers, this presents both risks and opportunities.

Deals on the Horizon – As automakers like Nissan, Chrysler, and Mitsubishi fight to stay relevant, expect steeper discounts, better incentives, and negotiable prices on their remaining inventory.

Resale Value Concerns – If a brand exits the market, resale values can plummet due to concerns over service, parts availability, and long-term support.

🔎 Do Your Research – Before buying, check for reliability ratings, resale projections, and market trends to avoid getting stuck with a depreciating asset.

Want to see the latest deals on cars from struggling brands? Check local listings now.

💡 Get expert car-buying guidance. Use your Free Car Buyer’s Guide to compare market data, incentives, and resale value forecasts. Or, let our Concierge team negotiate the best deal for you!