CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

From trucks to SUVs to performance cars, Chevrolet’s passenger lineup is broad. While this versatility gives shoppers options, five models stand out with higher average resale values.

After highlighting which new Chevrolets lose the least value after five years, we’ll take a closer look at buyer reassurances that enhance each model’s appeal, including, but not limited to, insurance, maintenance, and interest.

Discover the Chevrolets with the strongest resale retention below.

The 2026 Chevrolet Silverado 3500HD has the lowest 5-year depreciation rate of any Chevrolet model at 22% of value lost over five years. This assumes an average of 13,500 miles annually. With a selling price of $59,504, this one-ton, heavy-duty pickup maintains 94.17% residual value after a year, which is strong considering that new cars typically lose 10% to 11% of their value immediately upon driving off the dealership lot.

Key factors influencing the Silverado 3500HD’s high market demand include its exceptional towing (up to 36,000 lbs for 2026), complemented by robust Duramax diesel performance with 470 horsepower and 975 lb-ft of torque.

Since drivers often choose the 3500HD for its work and personal capability, durability is of the utmost importance. The Chevrolet Silverado 3500HD delivers this durability through design choices like high-strength steel construction, along with a fully boxed ladder frame that resists twisting forces and optimizes towing strength. Silverado 3500HD durability further protects your investment by lowering maintenance costs to 8% ($4,803) after five years.

Given the 2026 Chevrolet Silverado 3500HD’s depreciation rate, it’s no surprise that the 2026 Silverado 2500HD ranks second on our list by losing 29% of its value on average after five years, assuming a selling price of $58,013.

The Silverado 2500HD shares the 3500HD’s fully boxed ladder frame and reinforced steel, which solidify durability, and its three-quarter-ton size is better for those who can skip the 3500HD’s extreme max capacity and bulk. However, the 2500HD still delivers plenty of capability in work and personal use with 22,420-lb max towing, and you can select the 3500HD’s 6.6L Duramax turbo-diesel V8 to match its 470 horsepower and 975 lb-ft of torque.

While the 2026 Silverado 2500HD has higher five-year depreciation, it offers slightly lower average insurance, fuel, and interest costs.

If you’re interested in the fast-growing subcompact SUV segment, the 2026 Chevrolet Trax is worth considering, thanks to its competitive 34% depreciation rate after five years.

Since its 2015 model-year debut, the Trax has built a following thanks to its strong value proposition. For 2026, the Trax starts at $21,700. Competing entry models within its segment, such as the Kia Seltos and Nissan Kicks, have higher base prices at $23,790 and $22,430, respectively.

Drivers looking for a subcompact SUV still want to make the most of their vehicle’s class size, and the 2026 Trax delivers in this area following the 2024 model’s redesign, adding 11 inches in length and 2 inches in width. Chevrolet markets the Trax as compact, but most sources still list it as subcompact due to its dimensions.

A true Chevrolet compact like the 2026 Equinox has a higher five-year average depreciation rate of 40%, but you’ll want to consider that, unlike the Equinox, the 2026 Trax doesn’t offer all-wheel drive (AWD) as an option.

The subcompact 2026 Chevrolet TrailBlazer similarly benefits from its segment’s high demand with a 37% average five-year depreciation rate. Like the Trax, the 2026 Trailblazer’s starting price remains accessible at $23,300.

However, the Trailblazer distinguishes itself with available AWD, a more powerful available engine, and improved light off-road capability. The Trailblazer and Trax both contain a standard 1.2L turbo engine producing 137 horsepower and 162 lb-ft of torque, but the Trailblazer offers an optional 1.3L turbo with 155 horsepower and 174 lb-ft of torque. This added power, complemented by available AWD, is a valuable asset in the subcompact economy class where performance is often lacking.

The Trailblazer is also better equipped for off-roading beyond optional AWD with the ACTIV trim’s functional skid plates and all-terrain tires. In contrast, the Trax offers all-terrain tires, but its optional skid plates are purely decorative.

If a midsize pickup’s right for your driving needs, the 2026 Chevrolet Colorado’s 5-year depreciation rate of 39% makes this truck worthy of your consideration, especially if you’re an urban contractor or outdoor enthusiast.

While our list’s leader, the 2026 Silverado 3500HD, has a starting price of $45,900, which is $13,500 more than the 2026 Colorado, it’s worth noting that the Colorado competes with this full-size pickup in more ways than one. Fuel costs are naturally much lower ($10,500 over five years compared to $19,250), and its interest/maintenance costs are 3% and 2% lower than average.

You’ll want to prioritize the Colorado over the Silverado 2500HD or 3500HD if your driving values place greater emphasis on fuel efficiency, city and parking maneuverability, and moderate towing needs, along with a lower starting cost.

Knowing which Chevrolets offer the best resale values is only the start of how CarEdge helps you maximize your automotive investment. Our free tools help you learn what you should pay for a given model in your area, receive essential research and ratings, and gain access to shopping cheat sheets covering topics like negotiation tactics, price verification steps, and more.

If you’d prefer to have one of our expert car buyers handle your transaction from start to finish, you can get started using our Concierge Service with a free consultation.

The car buying game has fundamentally changed. In 2026, the smartest shoppers walk into dealerships with the same information dealers once kept behind closed doors—and it’s completely free. This shift in power dynamics is forcing a new kind of negotiation, one where informed buyers set the terms instead of reacting to sales tactics.

Let’s break down exactly how educated car shoppers are winning deals in 2026, using real negotiation strategies that work.

The first question most dealerships ask is: “What’s your monthly payment goal?” It sounds helpful, but it’s actually a negotiation tactic designed to shift your focus away from the vehicle’s actual price.

When you anchor a negotiation around monthly payments, dealers gain enormous flexibility to adjust loan terms, interest rates, and hidden fees while keeping your payment within your stated range. You might hit your $500/month target, but you could be paying thousands more over the life of the loan than necessary.

Smart buyers in 2026 shut this down immediately. Instead of discussing payments, they focus on one number:

This approach forces transparency and keeps the negotiation focused on value rather than affordability theater.

Here’s what changed everything: pricing intelligence that was once dealer-exclusive is now available to anyone with an internet connection. Tools like CarEdge provide:

In our example negotiation, the buyer came prepared with specific numbers: MSRP of $63,435, invoice of $59,311, and the knowledge that the F-150 had been on the lot for 84 days. This intel completely reframes the conversation.

When a vehicle has been sitting for nearly three months, the dealer is carrying floor plan costs and wants to move it. An informed buyer can leverage this without being aggressive—simply acknowledging the reality shifts negotiating power.

The key is having this data before you contact the dealer. Once you’re in the negotiation, having specific numbers on hand signals that you’re serious and informed.

Modern car buying starts with research, not test drives. Here’s the smart sequence:

Step 1: Do Your Homework

Step 2: Make Initial Contact

Step 3: Frame the Negotiation

Step 4: Negotiate with Data

Salespeople are trained to steer you toward payment discussions. Here’s how to redirect:

Dealer: “What monthly payment are you looking for?”

You: “I’m not focused on the monthly payment right now. I want to make sure we agree on a fair selling price first. Once we settle on the out-the-door number, we can structure financing however makes sense.”

This response is firm but not adversarial. It signals experience without creating tension.

Every day a vehicle sits on a dealer lot costs money. Most dealerships pay floor plan interest to finance their inventory—typically $20-50 per day per vehicle depending on its value.

An F-150 that’s been sitting for 84 days has cost the dealer roughly $1,680-$4,200 in carrying costs alone. That’s before accounting for lost opportunity (that lot space could hold faster-moving inventory) and depreciation risk.

This context doesn’t mean you strong-arm the dealer, but it does mean they’re motivated to move aged inventory. A reasonable offer on a vehicle with high days-on-lot is likely to get serious consideration, especially if you’re a qualified buyer ready to close quickly.

When negotiating a car deal, it’s helpful to know exactly how much profit for the dealership is built into each sale. No matter what the salesperson tells you, you do have plenty of room to negotiate savings! Here’s a quick breakdown of the pricing hierarchy:

Your goal is to negotiate a selling price between invoice and MSRP, closer to invoice especially on aged inventory, then verify the out-the-door price includes only legitimate fees.

In the example negotiation, the buyer:

This approach immediately shifts the dynamic. The salesperson recognizes they’re dealing with someone who’s done research, which tends to accelerate the negotiation process and reduce back-and-forth games.

Buying a car in 2026 isn’t about being the toughest negotiator or playing games—it’s about being informed. When you walk in with invoice pricing, inventory age, and market data, you’re negotiating from a position of knowledge rather than reacting to sales tactics.

The dealers who adapt to this new reality focus on service, transparency, and efficiency. The ones who don’t quickly find themselves losing deals to competitors who respect informed buyers.

Your goal isn’t to squeeze every last dollar out of a dealer. It’s to pay a fair price based on actual market conditions and vehicle cost structure. With the right information and approach, that’s exactly what you’ll accomplish.

The power shift in car buying is real, and it’s permanent. Smart shoppers in 2026 are leveraging it to save thousands while making the process faster and less stressful for everyone involved.

The 2026 Hyundai Venue has officially claimed the title of the cheapest new car you can buy in America, with a base MSRP of $20,550. With the Nissan Versa and Mitsubishi Mirage both gone from the U.S. market, the Venue stands alone at the bottom of the price ladder.

That’s a remarkable feat in a market where the average new car now costs close to $50,000. But here’s the thing: cheap isn’t the same as good value. And when you dig into the numbers, the Venue’s low sticker price starts to look less like a deal and more like a trap.

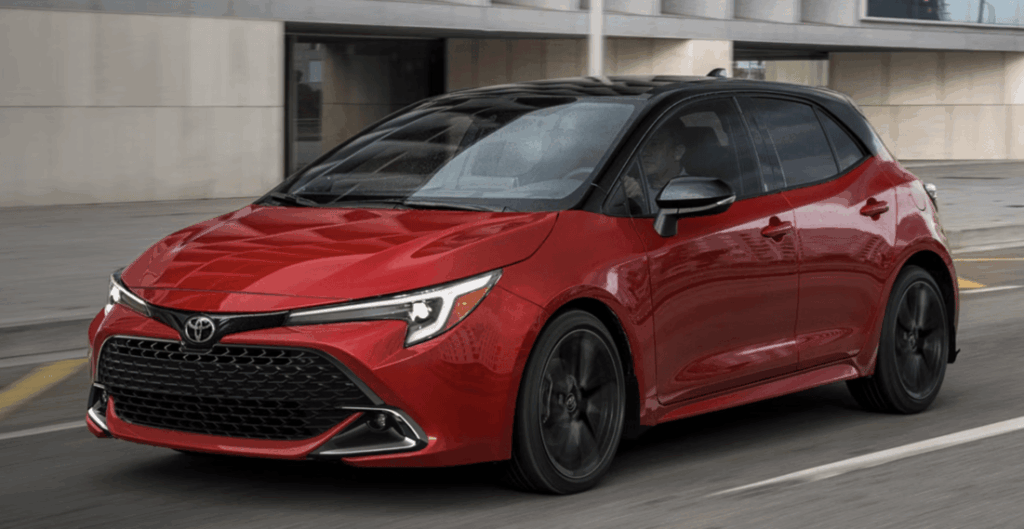

Spend roughly $4,000 more, and you can drive home in a 2026 Toyota Corolla Hatchback — a car that beats the Venue in nearly every category. Here’s why that extra investment is worth it.

Yes, the 2026 Hyundai Venue starts at $20,550. But that number doesn’t tell the whole story.

Once you add the mandatory destination fee, the base price is $22,150. Want heated front seats and wireless phone charging in your Venue? The SEL trim will run you $24,200.

The Toyota Corolla sedan starts at $24,120 with destination fees included. For an apples-to-apples comparison, we’ll be comparing the 2026 Toyota Corolla Hatchback to the Venue. The popular Corolla Hatchback SE starts at $26,560.

So the real-world price difference between base models is about $4,410. Over a five-year loan, that’s roughly $75 to $90 more per month depending on your interest rate. For most buyers, that’s a manageable gap.

And as we’ll soon show, you get a lot in return.

Here’s the part that tends to surprise people: the cheaper car actually costs more to own in the long run.

CarEdge’s 5-year total cost of ownership tells the story clearly:

That’s nearly $1,900 in savings with the Corolla over five years, despite its higher sticker price. The primary drivers? Depreciation and maintenance.

The Hyundai Venue is projected to lose 36% of its value over five years. The Corolla Hatchback? Just 23%. That 13-point difference means the Corolla holds significantly more resale value — money that stays in your pocket when it’s time to sell or trade in.

All things considered, CarEdge rates the two cars accordingly: the Corolla Hatchback earns an A+ value rating, while the Hyundai Venue gets a B. Neither is bad, but the Corolla Hatchback is the clear winner.

Reliability is one of the biggest factors in total cost of ownership, and it’s one of the clearest wins for the Corolla.

Consumer Reports rates the 2026 Corolla Hatchback 73 out of 100 for reliability. The Venue scores just 55 out of 100. That 18-point gap is significant — it reflects a meaningful difference in how often you’re likely to deal with unexpected repairs and maintenance headaches over time.

The overall Consumer Reports scores tell a similar story:

On safety, the gap is even sharper. NHTSA awarded the 2026 Corolla Hatchback a perfect 5 out of 5 stars. The Venue earned 4 out of 5 stars. For buyers who prioritize keeping themselves and their passengers safe, that difference matters.

The Venue is powered by a 121-hp four-cylinder engine. It’s adequate for city driving, but Car and Driver testing showed it takes 8.5 seconds to reach 60 mph, and reviewers consistently note a near-complete lack of passing power on the highway. The CVT doesn’t help matters.

The Corolla Hatchback packs a 2.0-liter four-cylinder making 169 horsepower — a full 48 more than the Venue. It reaches 60 mph in 8.3 seconds, edging out the Venue despite moving a larger, better-equipped car.

Fuel economy is another win for the Corolla. The EPA rates it at 32 mpg city and 41 mpg highway, compared to the Venue’s 29 mpg city and 33 mpg highway. The Corolla’s 8 mpg highway advantage can add up to real savings at the pump, especially for drivers who commute longer distances

This is one area where the Hyundai Venue has a genuine edge. Hyundai’s warranty coverage is among the best in the industry:

Hyundai Venue:

Toyota Corolla Hatchback:

Hyundai’s 10-year/100,000-mile powertrain warranty is legitimately impressive and provides real peace of mind. If warranty coverage is your top priority, the Venue deserves credit here.

That said, it’s worth asking why Hyundai offers such an extensive warranty. In part, it’s because the Venue’s reliability scores aren’t as strong as Toyota’s. The Corolla Hatchback scores 18 points higher on Consumer Reports’ reliability scale. Toyota rarely shows up in recall notices, but we can’t say the same for Hyundai.

The 2026 Hyundai Venue isn’t a bad option for drivers with tight budgets who need new-car warranty coverage above all else. We’re not here to dismiss it.

But if you can stretch your budget by roughly $4,400 at the base level, the 2026 Toyota Corolla Hatchback is the smarter buy in almost every dimension: lower 5-year cost of ownership, better resale value, superior reliability, a perfect NHTSA safety rating, more horsepower, and much better fuel economy.

The cheapest price tag at the dealership isn’t always the cheapest car to own. Sometimes, spending a little more upfront is exactly how you save money in the long run.

![10 Cars with the Lowest Cost of Ownership [2026 Data]](https://caredge.com/wp-content/uploads/2026/02/2026-Toyota-Corolla-Hatchback-1080x569.png)

New car prices are still high in 2026. Insurance isn’t getting cheaper. And repair costs aren’t trending down either.

So if you’re buying this year, you can’t just look at the sticker price, you have to look at the total cost of ownership.

Using CarEdge 5-year cost of ownership projections — which factor in depreciation, insurance, maintenance, fuel, and financing — we’ve gathered the 10 cars with the lowest total cost of ownership in 2026.

Predicted 5-Year Total Cost of Ownership: $30,541

Starting MSRP with Destination Fees: $26,560

Predicted 5-Year Depreciation: 20% of value lost

The Toyota Corolla Hatchback has the lowest total cost of ownership in 2026. The Corolla Hatchback checks every box for the ideal commuter car. It’s fuel efficient, extremely reliable, and affordable. With just 20% depreciation projected over five years, it holds value exceptionally well, and that’s what drives it to the very top of this ranking.

See Toyota Corolla Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $32,435

Starting MSRP with Destination Fees: $22,150

Predicted 5-Year Depreciation: 26% of value lost

With the Mitsubishi Mirage discontinued, the Venue now wears the crown as the cheapest new car in America in 2026.

Low MSRP plus manageable depreciation equals one of the lowest ownership costs on the market. It’s not fast, but it’s affordable — and for many buyers, that’s what matters.

See Hyundai Venue Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $32,541

Starting MSRP with Destination Fees: $25,890

Predicted 5-Year Depreciation: 24% of value lost

Few vehicles have the long-term reputation of the Civic. Reliability drives resale value, and resale value drives total ownership cost.

It costs slightly more upfront than some competitors, but its durability keeps long-term costs impressively low.

See Honda Civic Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $32,759

Starting MSRP with Destination Fees: $27,790

Predicted 5-Year Depreciation: 26% of value lost

Now offered only as a hatchback, the Impreza has quietly evolved into a refined compact with standard all-wheel drive.

Prices have climbed significantly — up roughly $8,000 since 2021 — but strong resale values help keep ownership costs competitive.

See Subaru Impreza Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $32,875

Starting MSRP with Destination Fees: $23,845

Predicted 5-Year Depreciation: 26% of value lost

The 2026 Sentra is all-new, with updated styling inside and out. The Sentra has been in the U.S. market for 44 years, and as other sedans get the axe, this one is here to see another year.

The Sentra undercuts the Civic on price but trails slightly in power and reliability. Still, it lands squarely among the most affordable cars to own this year.

See Nissan Sentra Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $33,333

Starting MSRP with Destination Fees: $23,535

Predicted 5-Year Depreciation: 31% of value lost

The K4 replaced the Forte in 2025 as Kia’s entry-level model.

Depreciation is a bit higher than others on this list, but its low starting price keeps overall ownership costs firmly in budget territory.

See Kia K4 Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $33,735

Starting MSRP with Destination Fees: $18,585

Predicted 5-Year Depreciation: 24% of value lost

Production ended in December 2025, but roughly 11,000 units remain on dealer lots in early 2026.

If you can find one, it’s one of the absolute cheapest ways to get into a new car this year.

See Nissan Versa Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $34,297

Starting MSRP with Destination Fees: $30,295

Predicted 5-Year Depreciation: 37% of value lost

The Camry is one of the more expensive cars on this list, but it’s also one of the most reliable. The extremely low maintenance costs are why the Camry remains in the top 10.

See Toyota Camry Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $34,616

Starting MSRP with Destination Fees: $24,120

Predicted 5-Year Depreciation: 26% of value lost

Not interested in the hatchback? The Corolla sedan remains one of the safest financial bets in the compact segment.

It’s slightly cheaper upfront than the hatchback, and still exceptionally affordable to own.

See Toyota Corolla Cost of Ownership Data

Predicted 5-Year Total Cost of Ownership: $34,718

Starting MSRP with Destination Fees: $27,950

Predicted 5-Year Depreciation: 27% of value lost

To be frank, the HR-V is the CR-V’s less popular sibling. Looks and sales volume aside, it’s still a great, reliable crossover. And it’s one of the few reliable crossovers that can be had for under $30,000.

See Honda HR-V Cost of Ownership Data

If you’re looking for the most affordable cars to own in 2026, the pattern is clear:

It’s easy to focus on MSRP when shopping for a new car, but the sticker price only tells part of the story. Insurance, maintenance, and depreciation can quietly add thousands to your total cost over time, even for a new car. Every model on this list proves that affordable ownership is still possible in 2025, but only if you make a smart purchase.

Whether you’re shopping new or used, don’t just ask what a car costs today—ask what it’ll cost you tomorrow. For deeper insights, explore cost of ownership and depreciation data for every model at CarEdge Research.

If you’ve been watching the car market, you know something’s broken. But here’s what most people don’t realize: car repossessions in 2026 are tracking at levels we haven’t seen since the 2008 financial crisis. For owners at risk of losing their vehicle, this is a statistic that hits close to home. And if you’re a used car buyer, this could be a little-known opportunity to snag a deal.

CarEdge co-founder Ray Shefska here has spent decades in dealerships, and he’s seeing something alarming on the lots right now. Let me break down exactly what’s happening, what dealers aren’t telling you about these repo cars flooding the market, and how you can navigate this situation whether you’re buying or currently at risk of losing your vehicle.

Let’s start with the numbers. According to recent data from Cox Automotive, auto loan delinquencies (60+ days past due) have climbed to 4.8% in early 2026—the highest rate since 2010. Here’s why:

1. Pandemic-Era Loans Coming Due

Remember 2021-2022 when everyone bought cars at inflated prices with six or seven month loans? Those buyers are now 3-4 years into loans, and many are deeply underwater. Their $45,000 electric vehicle or luxury crossover is worth $25,000, but they still owe $38,000. Many are looking for a way out of negative equity, but few are finding an easy solution.

2. Payment Shock Is Real

The average new car payment in 2026 is $748/month. Used cars? $563/month. That’s not a car payment—that’s a second mortgage. When you combine that with inflation in groceries, rent, and insurance, something has to give.

3. Subprime Lending Came Roaring Back

From 2021-2024, lenders loosened standards dramatically. People with 580 credit scores were getting approved at 18-22% APR. Now those loans are imploding. Subprime auto loan delinquencies are above 6.5%. As banks and automaker captive financing companies lose money on more loans, it become tougher for all borrowers to secure a good rate.

If it gets any worse, the entire auto lending system will be under threat.

4. The Trade-In Trap

Industry veteran Ray Shefska sees it all the time: “People come in already $8,000 upside down on their current loan, roll that negative equity into a new $50,000 purchase, and suddenly they’re financing $58,000 at 9% interest. When life happens—job loss, medical bills, divorce—that payment becomes impossible.“

Repossession isn’t just losing your car. For many, having a car repossessed is a financial chain reaction that can follow you for years. Understanding the sequence of events and the full scope of the damage is the first step to avoiding it, or dealing with it if you’re already there.

The Repossession Timeline:

The Financial Damage:

If you know repossession is inevitable, you don’t have to wait for the tow truck to show up in the middle of the night. Voluntary repossession—where you call your lender and arrange to drop the car off yourself—puts you in control of the timing and lets you clear out your belongings on your own terms.

The financial damage is nearly the same either way. Voluntary repo still hits your credit report just like an involuntary one, and you’re still on the hook for any deficiency balance if the car sells at auction for less than you owe. The one practical upside is that you may avoid the repo agent fee ($400–800), which slightly reduces what you’ll owe in the end.

Think of it less as a financial solution and more as a way to manage a bad situation with a little more dignity. If you’ve exhausted your other options—negotiating with the lender, refinancing, or selling the car yourself—voluntary surrender at least lets you exit on your own terms rather than waking up to an empty driveway.

Car dealers have good reasons for not advertising repossessed cars. Many shoppers would be turned off by this revelation. Few drivers want their “new” car to remind them of the financial hardships others have endured. So, how can you find out if a car was repossessed? Let’s get into it.

Ray’s seen thousands of repos come through dealerships, and here’s how they get there:

Route 1: Wholesale Auction (Most Common)

“When a bank repos a car, they want it gone fast,” Ray explains. “It goes to Manheim, ADESA, or another wholesale auction. Dealers bid on these, usually getting them for $3,000-7,000 below clean retail because repos often have issues like missed maintenance, interior damage, sometimes even mechanical sabotage from angry former owners.”

Route 2: Direct Sales to Franchise Dealers

Captive finance arms (Ford Credit, GM Financial, Toyota Financial) often send repos directly to their franchise dealers. “A Ford repo might come straight to a Ford dealership’s used lot,” Ray notes. “These are usually in better shape because they were newer when repossessed.”

Route 3: Buy-Here-Pay-Here Lots

Higher-mileage repos with issues often end up at BHPH dealers who do in-house financing. These lots target the same subprime buyers who lost their cars to repo, creating a dangerous cycle.

Here’s what dealers won’t voluntarily disclose:

1. They’re Not Required to Tell You It’s a Repo

Unlike flood damage or salvage titles, repossession history doesn’t show up on a Carfax or vehicle title. A dealer can legally sell you a former repo without disclosure.

2. Repo Cars Often Have Hidden Issues

“I’ve seen repos come in with 15,000 miles past due for an oil change, bald tires, and check engine lights,” Ray says. “The previous owner knew it was getting taken back—they stopped maintaining it months ago.”

3. The “Auction Fresh” Red Flag

On a Carfax, look for “sold at auction” within the last 30-60 days, especially if there’s only one previous owner. That’s often a repo that got wholesaled.

4. Dealers Mark Them Up Anyway

Just because a dealer bought it cheap at auction doesn’t mean you get a deal. They’ll still mark it up to market rate or higher. Your job is to negotiate knowing they have less money in it.

Research red flags

Check the Carfax or AutoCheck report. A Repossession may show:

At the Dealership, keep an eye out for these signs:

Questions to ask the salesperson

1. “Where did you acquire this vehicle?” (If it came from an auction, that’s normal. Inquire further by asking if it was a bank return. In dealership lingo, repos are often called “bank returns”)

2. “Can you show me the last service records?” (Gaps of 12+ months are a warning sign)

3. “Has this vehicle had a pre-purchase inspection by your service department?” (Many repos don’t get proper reconditioning)

4. “What’s your best out-the-door price?” (Repos have more negotiating room since dealers bought them cheap)

The opportunity is real, but be careful. Here’s Ray’s advice: “The repo surge means there’s legitimate opportunity for educated buyers. Banks are motivated, dealers have inventory they want to move, and you can get a good car for the right price—but you MUST do your homework.”

Some banks sell repos directly to consumers through their websites:

Pros: Skip the dealer markup, often better condition disclosure

Cons: Sold as-is, limited negotiation, you handle all paperwork

Manheim and ADESA occasionally have public auction days. You can inspect vehicles beforehand and bid directly.

What to Bring:

If you play it smart, it’s possible to buy a repossessed car at auction for 20-25% below retail pricing.

If you’ve identified a likely repo at a dealership:

1. Get a Pre-Purchase Inspection: Non-negotiable. Pay $150-200 for an independent mechanic to inspect it thoroughly

2. Use Auction Data: Check recent auction results on sites like Manheim Market Report to see wholesale values

3. Negotiate Based on Condition: “I see this needs new tires ($800), brakes ($400), and hasn’t been serviced in a year. Here’s my offer based on these deferred costs.”

4. Get an Extended Warranty: If you’re buying a higher-mileage repo, negotiate for a dealer warranty or purchase a reputable third-party plan

If you’re not comfortable evaluating a repo, just wait for off-lease inventory. These are vehicles coming back from 2-3 year leases, typically well-maintained, and dealers are motivated to move them too. You get a known history without the repo risk. For many, it’s worth the patience and higher price tag for a known vehicle history.

The good news is that you have more options than you think. If you’re behind on payments and worried about repo, here’s Ray’s advice from someone who’s worked with hundreds of struggling buyers:

Don’t hide. Most lenders would rather work with you than repo your car. Call and ask about:

“The absolute worst thing you can do is ghost your lender,” Ray emphasizes. “Once they assign a repo agent, your options disappear.”

If you’re underwater but not too deep:

1. Get instant offers from Carvana, CarMax, and Vroom

2. Compare to private party value on Facebook Marketplace or Craigslist

3. If you can cover the difference between the offer and your payoff, sell immediately

4. If possible, use the proceeds to buy a $5,000-8,000 reliable used car that you own outright. If that’s not an option, start saving up.

If you can’t make payments and can’t sell, voluntary surrender is better than repossession:

“Voluntary surrender is better than hiding the car and playing games with the repo man,” Ray says. “It shows some responsibility and might make the lender more willing to negotiate on the deficiency.”

If you’re 30-60 days behind but your credit hasn’t tanked yet:

“I’ve helped people who were 60 days behind get into a different vehicle with a $200/month lower payment,” Ray notes. “It’s not ideal—you’re still buried—but it keeps you mobile and out of repo status.”

Used Car Prices Will Stabilize or Decline. Repo inventory flooding wholesale auctions puts downward pressure on used car prices. Good news if you’re buying, bad news if you’re trying to trade in.

Lending Will Tighten (Again). Expect stricter credit requirements, higher down payment demands, and shorter loan terms as lenders react to losses. The 84-month loan at 6.99% for 620 credit scores? That’s disappearing.

Subprime Buyers Will Struggle. If you have damaged credit and need a car, expect to pay 15-22% APR or resort to buy-here-pay-here dealers with even worse terms. Breaking this cycle requires saving for a cheap, reliable car you can own outright.

Opportunity for Cash Buyers. 2026-2027 could be the best time in years to buy a used car with cash or strong credit. Dealers need to move inventory, repos are plentiful, and negotiating leverage is shifting back to buyers.

If You’re Buying:

If You’re Struggling With Payments:

The bigger lesson according to Ray

“The repo crisis of 2026 is a direct result of over-leveraged buyers financing depreciating assets at high interest rates. If you take away one thing, let it be this: just because a bank will approve you for $60,000 doesn’t mean you should borrow it. Buy less car than you can afford, keep the loan term short, and always have an emergency fund. That’s how you avoid becoming a repo statistic, and having a car you no longer drive follow you for years.”

What’s your experience with the current auto loan market? Have you seen repos on dealer lots, or are you navigating a difficult payment situation yourself? Join the conversation at the CarEdge Community.

“We’ve got another buyer coming in an hour.”

“There’s someone else who’s very interested in this car.”

“I need to know if you’re serious because we have other offers.”

Sound familiar? If you’ve spent any time negotiating at a car dealership, you’ve probably heard some version of this classic pressure tactic. CarEdge Co-Founder Ray Shefska, with decades of dealership experience, calls this exactly what it is: manufactured urgency designed to make you panic and pay more.

Here’s how to handle it, and why this tactic rarely means what they want you to think it means.

This pressure play works on basic human psychology: fear of missing out. Nobody wants to lose something they’ve already invested time in, and salespeople know that once you’ve test-driven a car and started imagining yourself in it, you’re emotionally attached.

The dealership’s goal is simple: create artificial urgency to:

In Ray’s experience, this tactic comes out most often when negotiations stall or when you say you need to think about it.

Here’s what Ray wants you to know: In most cases, there is no other buyer.

“When there genuinely is another interested party, the dealership doesn’t need to tell you about it. They’ll just sell it to that person. The fact that they’re spending energy trying to convince you to buy suggests they don’t have a better offer waiting.”

Even when there is another buyer, consider these realities:

Dealerships talk to dozens of people every day. Maybe someone did express interest in that car—but “interest” doesn’t mean they’re qualified, approved for financing, or actually ready to purchase. Most of these “interested buyers” never materialize into actual sales.

A truly in-demand vehicle—especially in 2026’s market where inventory has normalized—doesn’t sit on the lot long enough for this conversation to happen. Hot cars sell within days, often at or above asking price, without negotiation drama.

Unless you’re buying something truly rare (a limited-edition model, a specific classic car, etc.), there are similar vehicles available at other dealerships. The salesperson wants you to forget this fact.

It’s always best to shop the cars that are most negotiable, as determined by local market data. Here’s how we find them.

When a salesperson says another buyer is coming, Ray recommends this simple response:

“I understand. If they buy it before we reach an agreement, I’ll find another one.”

That’s it. Don’t argue. Don’t panic. Don’t try to compete with this phantom buyer. Just acknowledge what they said and demonstrate that you’re not going to be pressured.

Here’s why this response is so effective:

It Calls Their Bluff Without Confrontation

You’re not accusing them of lying, but you’re making it clear their pressure tactic isn’t working. You’re showing confidence in your position and your ability to walk away.

It Reminds Them You Have Other Options

Salespeople sometimes forget that they need the sale too. Your response subtly reminds them that if they lose you over this pressure play, they’ve lost a real buyer chasing a maybe-buyer.

It Keeps You in Control

By remaining calm and non-reactive, you maintain negotiating power. Panic is expensive. Composure saves you money.

It Often Leads to Backtracking

In Ray’s experience, this response frequently results in the salesperson suddenly having more flexibility: “Well, let me talk to my manager and see what we can do for you…”

Funny how that “urgent” other buyer becomes less urgent when you’re willing to walk.

Know the market value of the car you want using resources like:

When you know what the car is actually worth, pressure tactics become background noise.

Walk in with your own financing already secured. This eliminates one pressure point (“We need to see if you qualify”) and often gets you a better rate than dealer financing. Review this guide to financing like a pro before you shop.

Contact 3-5 dealers for the same make and model. Get quotes in writing (email is perfect). This gives you real leverage and makes the “another buyer” tactic meaningless—you literally have other options ready.

Use our Dealership Ratings Based on Real Prices to find the most transparent car dealers near you.

The single most powerful negotiating tool is genuine willingness to leave. If you’re not prepared to walk out, you’ve already lost leverage. Remember: there are other cars, other dealers, other days.

Let’s say you use Ray’s response, walk away, and the dealership actually sells the car to someone else. Now what?

Here’s the truth: You probably dodged a bullet.

If they were willing to let you walk over a reasonable negotiation, one of two things happened:

1. They really did have a buyer willing to pay more—which means you would have overpaid to compete

2. They made a strategic mistake—they gambled on pressure and lost a real sale

Either way, you did the right thing. In today’s market, you will find another vehicle. You might even find a better deal at a dealership that doesn’t play these games.

Understanding the current market helps you evaluate these tactics:

Bottom line: The “another buyer” tactic is less credible in 2026 than it was during the shortage years. Dealers have cars to sell, and competition among dealerships is healthy.

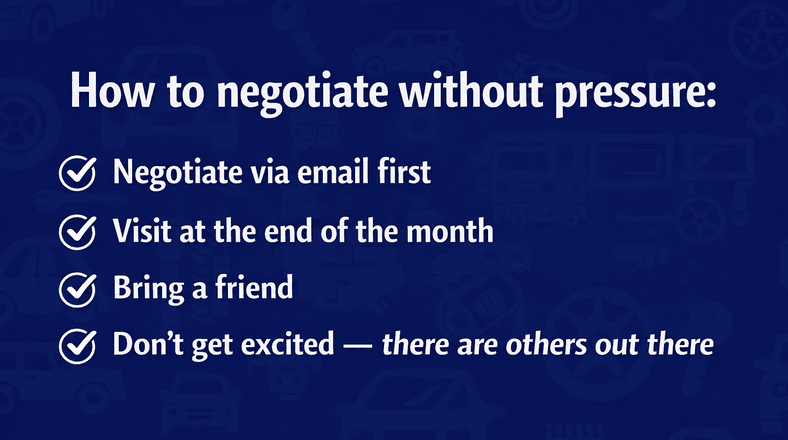

One of the best ways to avoid pressure tactics entirely is to conduct initial negotiations via email. Get quotes from multiple dealers in writing before you ever set foot in a showroom. This eliminates the time pressure and lets you think clearly.

Use these free email templates to get started on the right foot.

Dealerships have monthly quotas. Shopping in the last few days of the month often means salespeople are more motivated to make deals happen—on your terms, not theirs.

A second person helps in two ways: they provide emotional support when pressure tactics emerge, and they give you a built-in reason to pause (“I need to discuss this with my friend”). It’s harder to pressure two people than one.

The more you gush about loving the car, the more leverage the dealership has. Stay neutral and businesslike. You can get excited after you’ve agreed on a fair price.

“Another buyer is coming” is designed to create panic. Your job is to remain calm, remember that you have options, and refuse to be rushed into a decision that costs you thousands of dollars.

Use Ray’s simple response: “I understand. If they buy it before we reach an agreement, I’ll find another one.”

Then stick to your research, your budget, and your willingness to walk away. More often than not, that “other buyer” will mysteriously disappear, and suddenly the dealer will be very interested in working with you on your terms.

And if they do sell it to someone else? You’ll find another car—probably at a better price, at a dealership that doesn’t play games.

Remember: The dealership needs to sell cars. You just need to buy one car. That’s leverage. Use it.

On Friday, February 20, 2026, the U.S. Supreme Court ruled that President Trump exceeded his authority when imposing sweeping global tariffs under the International Emergency Economic Powers Act (IEEPA). The 6-3 ruling puts an end to tariffs imposed under the IEEPA, but it leaves other tariff options on the table for the administration.

That decision immediately reshapes U.S. trade policy, and it has real consequences for automakers, dealerships, and car buyers. It’s important to note that this remains a developing situation, and President Trump has already committed to imposing a new 10% global tariff in coming days.

To understand what happens next, we first need to look at what the tariff environment actually looked like just before the ruling.

Before the Supreme Court decision, vehicle imports into the United States were operating under meaningfully elevated effective tariff rates. Across all imported vehicles, the blended effective tariff rate averaged approximately 15.3%. That reflects the real-world duties being paid at the border after negotiations and adjustments, not just the original headline tariff proposals.

Rates varied by country:

In practice, most North American-built vehicles retained duty-free status, preserving a major supply chain advantage for USMCA-compliant production.

It is important to clarify that these figures represent effective rates, not just headline announcements. Although initial tariff proposals were often higher, negotiations had already reduced many of them to approximately 15% for key allies.

The Supreme Court ruling invalidated tariffs imposed under IEEPA authority. As a result, those specific duties are no longer legally in force unless re-established under a different statutory mechanism. Some have estimated that more than half of the existing tariffs imposed by the U.S. were issued under the IEEPA.

Other trade authorities — such as Section 301 or Section 232 — could be used in the near future to bring back tariffs. At a press announcement on Friday, President Trump said that he will be launching a new 10% tariff using a different legal backing that the overturned IEEPA tariffs. While the Court removed the existing tariff structure, it did not permanently eliminate the possibility of future tariffs on auto imports.

This remains an evolving situation, and the auto industry is certainly following developments closely.

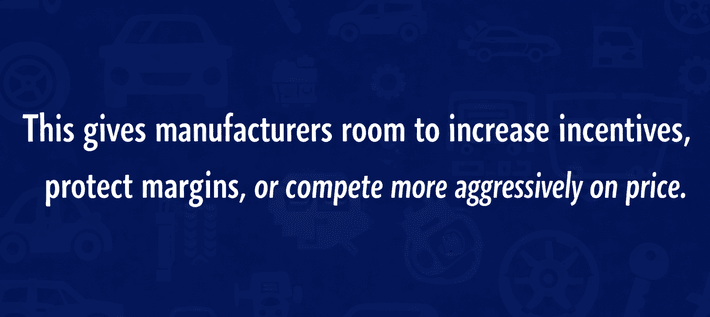

Removing a roughly 15% effective tariff from imported vehicles changes the cost equation meaningfully.

When a vehicle carried a 15% duty at the port of entry, that cost had to be absorbed somewhere. In many cases, it was passed through to consumers in the form of higher MSRPs. In other cases, automakers absorbed reduced incentive spending to offset it. This meant fewer low-APR incentives and cheap lease deals for consumers.

With that layer removed, automakers gain flexibility.

While vehicle prices are not going to fall 15% overnight, eliminating tariff pressure reduces upward pricing momentum. For now, the ruling gives manufacturers room to increase incentives, protect margins, or compete more aggressively on price.

This is welcome news as the industry is expecting sales to stagnate through 2026. With more competitive pricing and incentives now on the table, automakers will have new options to compete for your business.

Parts costs could also ease. Even vehicles assembled in the United States often rely on globally sourced components. If imported parts were previously facing 10–15% duties, removing those costs lowers production expenses and improves manufacturing economics. In a market where affordability remains strained in 2026, even incremental cost relief can matter.

Even the cars and trucks made in America could benefit from the Supreme Court ruling.

Competitive dynamics may also shift. Prior to the ruling, Japanese, Korean, and European vehicles were competing under approximately 15% tariff pressure, while Chinese imports faced even steeper effective burdens. With tariffs invalidated, those imported vehicles regain structural cost competitiveness. That increases pricing pressure on domestic manufacturers and could lead to stronger cross-brand competition. This typically benefits consumers.

There is also the potential for financial adjustments. Companies that paid tariffs may seek refunds, which could improve short-term profitability and potentially support future incentive programs. However, refund processes are often complex and could take time to resolve.

Before the February 20 Supreme Court ruling on President Trump’s global tariff strategy, most major vehicle-exporting countries were operating under an effective tariff environment of roughly 15%. China faced much higher blended rates, and USMCA-compliant vehicles from Canada and Mexico remained duty-free.

With those tariffs now overturned under IEEPA authority, imported vehicles and parts regain cost relief. Production inputs become less expensive, competitive pressure increases, and one of the largest recent cost drivers in the auto market has been removed.

If new car prices come down (even modestly), used car prices could also decline. That would be a win for all car shoppers in 2026. Those looking to sell or trade-in could see their trade-in values drop, however.

Vehicle prices are not going to collapse overnight. But structurally, this ruling removes a major upward force on pricing. For car buyers navigating a still-expensive market in 2026, that represents a meaningful shift — and potentially the first real affordability tailwind the industry has seen in quite some time.

After 43 years on both sides of the dealership desk, CarEdge co-founder Ray Shefska has seen every negotiation tactic in the book. And here’s something most car buyers don’t realize: the questions a salesperson asks in the first five minutes can cost you thousands of dollars before you even start negotiating.

These aren’t just innocent conversation starters. They’re carefully designed information-gathering tools that shift negotiating power away from you and directly into the dealer’s hands. In 2026, with dealership profit margins under pressure and inventory levels normalizing, these tactics are more aggressive than ever.

Let’s break down the five questions you should never answer directly—and exactly what to say instead.

Why This Question Is Dangerous

This seems like friendly small talk, but it’s actually the opening move in a complex strategy. When you tell them what you drive, you’re revealing:

In 2026, with trade-in values fluctuating more than ever due to the stabilizing used car market, this information is particularly valuable to dealers. Check out our guide to trading-in, and stick to your plan!

The Right Response

Instead of answering directly, say:

“I’m here to learn about this vehicle first. Let’s focus on what you have available.”

Or if they push:

“I might have a trade, I might not—depends on the numbers we agree on for this car first.”

Ray’s Pro Tip

“Never let them appraise your trade-in before you’ve negotiated the purchase price of the new vehicle. These are two separate transactions, and combining them only benefits the dealer. Get the best price on the new car first, then introduce the trade-in as a separate negotiation.“

Why This Is the Most Expensive Question

This is the single biggest trap in car buying, and it’s become even more prevalent in 2026 as dealers lean heavily into payment-focused selling. Here’s what happens when you give them a monthly payment target:

In 2026, the average new car loan has stretched to 68 months with the average payment hitting $739. Don’t become another statistic.

The Right Response

Say this instead:

“I don’t shop by monthly payment. What’s your best out-the-door price on this vehicle?”

We’ve been saying it for years: The out-the-door price is the only price you should be negotiating. Use this free calculator to see how it works.

If they persist:

“I have my own financing arranged. I’m only discussing the vehicle price today.”

Ray’s Real-World Example

“I’ve watched salespeople take a customer who said “I can afford $500 per month” and show them vehicles they could have bought for $400 per month with a shorter loan term. That extra $100 over 72 months? That’s $7,200 in unnecessary spending, plus thousands more in interest.“

Why Dealers Ask This Early

This question serves multiple purposes for the dealer:

In 2026, dealer financing kickbacks have actually increased as manufacturers push captive financing programs. The dealer might make $1,500-$3,000 just on your loan—incentive to push you away from your credit union’s better rate.

The Right Response

Keep your cards close:

“I haven’t decided yet. What’s your best price on the vehicle?”

Or more firmly:

“That depends on the deal we work out. Let’s talk about the car first.”

The Strategic Play

Even if you’re paying cash, Ray recommends acting like you’ll finance initially. “Get their best price, then “change your mind” and pay cash. Why? Because dealers often give better prices when they think they’ll profit on financing. Yes, it’s a game—but they taught us how to play it.“

The Pressure Behind This Classic Line

This question appears helpful on the surface, but it’s actually a closing technique designed to:

In 2026, with inventory levels much healthier than the shortage years of 2021-2023, there’s absolutely no reason to be in a rush unless you’ve done your homework and know you’re getting a fair deal.

The Right Response

Shut down the pressure:

“I’m not making a decision today. I’m gathering information and comparing options.”

Or:

“I need to see your best offer first, then I’ll take time to consider it.”

Ray’s Perspective

“When I was selling, this question was explicitly designed to create urgency and get a commitment. Here’s the truth: that “special price” they can offer you today? It’ll be there tomorrow. And next week. The best deals come from patient buyers who don’t fall for artificial deadlines.“

Why This Seems Harmless But Isn’t

This feels like the salesperson is being helpful and understanding your needs, but they’re actually:

In 2026’s market, feature-loaded vehicles carry significantly higher profit margins. That’s why automakers and dealers alike love to sell big trucks and SUVs. That panoramic sunroof and premium audio system? They cost the dealer far less than they’ll charge you.

The Right Response

Stay focused on the vehicle in front of you:

“I’m interested in this specific model we’re looking at. Let’s discuss this one.”

Or:

“I’ve done my research on what I need. What’s your best price on this configuration?”

The Upsell Trap

Ray says to watch out for this trap, and always stick to your budget. “Once you start describing your “dream car,” the salesperson will conveniently discover they have something “even better” that matches your description—at a much higher price point. Stick to your researched vehicle choice and don’t get emotionally sidetracked.“

After spending decades on both sides of the desk, here’s the approach that consistently gets CarEdge readers the best deals:

Step 1: Do Your Homework Before You Arrive

Step 2: Control the Initial Conversation

Step 3: Negotiate One Thing at a Time

Step 4: Be Willing to Walk Away

Dealers in 2026 are increasingly adding “market mandatory accessories” to vehicles before they hit the lot—things like paint protection, nitrogen-filled tires, or wheel locks. These typically cost the dealer $100-$300 but get marked up to $1,500-$3,000.

How to handle it: Negotiate these items down or off entirely. They’re not mandatory—they’re dealer profit centers.

After the backlash against ADM (Additional Dealer Markup) during the shortage years of 2021-2023, some dealers now call these markups “market adjustments” or “market price corrections.” It’s the same thing with a friendlier name.

How to handle it: Any price above MSRP requires justification. You should never pay over MSRP for the vast majority of models in 2026. Most models can be successfully negotiated to 5-10% below MSRP, or even more for leftover 2025 models.

More dealers are using online tools that ask you to input your trade-in info, desired payment, and financing preference before you ever visit. These are the same five questions in digital form.

How to handle it: Use online tools to research and identify vehicles, but don’t provide specific trade-in or financing information until you’re ready to negotiate in person.

A CarEdge reader emailed us last month about her experience buying a 2026 Honda CR-V. She watched our content on YouTube and implemented these exact strategies:

Total savings: $4,800 by simply controlling the information flow and negotiating strategically.

In 2026, the dealers who succeed are those who understand that informed buyers do their homework. The five questions we covered today are designed to extract information from you before you’ve extracted fair pricing from them.

Your goal walking into a dealership should be simple: keep your cards close, deflect these information-gathering questions, and focus relentlessly on one number—the out-the-door price of the specific vehicle you want.

Remember Ray’s golden rule from 43 years in the business: “The person with the most information and the least urgency wins the negotiation.”

Don’t answer these five questions directly. Don’t rush into a deal. Don’t let emotion override research. And for the love of everything, don’t focus on monthly payments.

Do your homework, control the conversation, and negotiate one item at a time. That’s how you drive off the lot with a fair deal—and how you avoid leaving thousands of dollars on the table.

Before your next dealership visit:

1. Print out or screenshot these five questions and responses

2. Research fair market value for your target vehicle

3. Get pre-approved for financing from 2-3 sources

4. If trading in, get appraisals from online buyers like CarMax and Carvana

5. Role-play deflecting these questions with a friend or family member

6. Commit to walking away if you don’t get a fair deal

The 2026 car market is vastly different from the shortage years, and dealers know they need to work harder for your business. Use that to your advantage by being the informed, prepared buyer who knows exactly which questions to deflect—and how to deflect them.

Happy car shopping, and remember: the best deal is the one where you control the conversation from start to finish.

Whether or not April showers bring May flowers, your tax return could help you buy a car this spring. But before you start spending some serious green on a slick new ride, stop to smell the roses and do your due diligence. Check out these five mistakes spring car buyers make—and how you can avoid the sting of buyer’s remorse.

Starting fresh often spurs spring car buyers to trade in their car at the same dealership where they purchase their new vehicle. Wrapping both deals into one makes getting into a new car more convenient, and many shoppers assume they’re getting a fair deal.

Always treat trading in your current vehicle as a separate transaction from purchasing your new car. That means shopping around for the best offer—even if it involves selling your car at a different dealership than where you make your new car purchase. This advice is especially true in the spring because it’s the best time of the entire year to get the most out of any vehicle you trade in.

Convenience also drives spring car buyers to explore financing only with the dealership they’re purchasing from. Many assume that, similar to their trade-in, dealerships offer the “going rate” and that terms vary little among auto lenders.

In reality, the very opposite is often true: you may find better terms, depending on your credit score and finances. When you’ve settled on the car you want to purchase, reach out to several lenders (at least three, besides the dealership) to see what you qualify for. Negotiating your auto loan outside of the dealership could actually simplify the transaction, so what do you have to lose?

Spring car buyers often focus on the vehicle price listed on a dealership’s website, overlooking additional fees commonly tacked on by dealers. Many of these dealer fees correspond to real costs—including taxes, titling, and registration—but several only surface once buyers begin their paperwork. Dealers use hidden or fake fees to increase their profits at the expense of unsuspecting buyers.

Before you even sit down to fill out paperwork, educate yourself about which dealer fees apply and which you can negotiate. Read the contract carefully to identify any hidden fees that increase the final price. Don’t be afraid to challenge these fees—and walk away from the deal altogether.

It’s common for spring car buyers to break down their overall car-buying budget into a monthly payment. The corresponding number helps them weed through their options to see what they can afford. Car salespeople also tend to focus on this number when locking in a sale.

Maintain your focus on the out-the-door (OTD) price to ensure you don’t overpay for your new car and risk being underwater on your loan. Your monthly payments will change based on how much you put down—a bargaining chip you should absolutely leverage if you have a sizable tax refund—and what loan terms you negotiate. Do the math before you get to the dealership so you know which numbers align with your overall and monthly budget.

Too many spring car buyers boil a new car purchase down to only the final price listed on the invoice. They often exclude additional expenses—such as annual registration, insurance, and maintenance—from their monthly budget. Even if they have enough funds to cover their monthly car payment, those extra expenses can quickly add up.

Cars are investments and require maintenance and general upkeep. While newer cars tend to require less costly maintenance than a vehicle that’s 10 years old or has 100,000+ miles on it, you still need room in your budget for oil changes and tire rotations. Quote out insurance premiums and how much it costs to own your select vehicle—and budget accordingly.

Our latest car market update shows a mixed bag of opportunity for car buyers, depending—among many factors—on the brand and model year they choose. Yet, having cash to even the odds and key insights to guide your decision puts you at an advantage regardless of market conditions.

Spend your hard-earned refund wisely by partnering with a CarEdge Concierge to find the best car deal available. Share your search parameters, and our experts will do all the legwork for you. Start the conversation today to get behind the wheel with greater confidence in your purchase.

If you’ve walked into a Toyota dealership recently and asked about a RAV4, you probably felt your stomach drop. The markups on America’s best-selling SUV are, frankly, insane right now — and dealers are counting on you not knowing any better.

But here’s the thing: you don’t have to pay those inflated prices. CarEdge’s Ray Shefska has spent decades on the dealership side of the desk, and his son and co-founder Zach tracks the pricing data obsessively. Together, we’re pulling back the curtain on exactly what dealers pay for a RAV4, what they’re charging you, and what you should actually agree to spend.

Let’s break it all down.

The Toyota RAV4 has been the best-selling crossover in America for years running, and 2026 is no different. Demand remains sky-high for a few key reasons:

When demand outstrips supply, dealers add “market adjustments” — a polite way of saying they’re tacking on pure profit above MSRP. And right now, those adjustments on certain RAV4 trims are reaching $3,000 to $7,000 or more.

Before you can negotiate effectively, you need to understand the numbers. Here’s the reality that dealers don’t want you to see — the gap between invoice price (what the dealer pays Toyota) and MSRP (the sticker price).

| RAV4 Trim | Invoice Price (Est.) | Base MSRP | Built-In Dealer Margin |

|---|---|---|---|

| LE | $28,800 | $31,090 | $2,290 |

| XLE | $30,200 | $32,590 | $2,390 |

| XLE Premium | $32,500 | $35,090 | $2,590 |

| Adventure | $34,000 | $36,690 | $2,690 |

| TRD Off-Road | $35,200 | $38,090 | $2,890 |

| Limited | $36,800 | $39,790 | $2,990 |

Note: Invoice prices are estimates based on available dealer cost data. Actual invoice may vary slightly by region and installed options.

That built-in margin of $2,000–$3,000 is already profit for the dealer — before any markup. On top of that, Toyota offers dealers holdback (typically around 2% of MSRP) and potential volume bonuses. So when a dealer tells you they’re “barely making anything” at MSRP, that’s simply not the full picture.

The gas-only RAV4 markups are bad. The hybrid markups are worse. And the RAV4 Prime? That’s where things go completely off the rails.

| Model | MSRP Range | Typical Market Markup (2026) |

|---|---|---|

| RAV4 Hybrid | $33,090 - $41,290 | $2,000 - $5,000 over MSRP |

| RAV4 Prime SE | $44,090 | $3,000 - $7,000 over MSRP |

| RAV4 Prime XSE | $49,590 | $5,000 - $10,000+ over MSRP |

We’ve seen real listings showing RAV4 Prime XSE models with $8,000 to $10,000 “market adjustments” slapped right on the window sticker. That’s a $50,000 compact SUV pushed to nearly $60,000 before taxes and fees.

As Ray puts it: “Just because they CAN charge it doesn’t mean you should pay it. There’s always another dealer.”

Wondering how you can put this knowledge to use saving you money in 2026? Here are the numbers you should walk into the dealership armed with.

For the standard (non-hybrid) RAV4, inventory has improved enough that you should not be paying over MSRP. Period. In fact, depending on your market and willingness to be patient, here’s what to target:

If a dealer won’t budge off a markup on a gas RAV4, walk away. There are plenty of them on lots right now.

Hybrid inventory has improved compared to 2023–2024, but it’s still tighter than the gas model. Your targets:

The Prime is the toughest nut to crack because Toyota allocates so few to each dealer. But that doesn’t mean you should light money on fire:

Knowing the right price is half the battle. Here’s how to actually get it.

Email or message the internet sales departments of at least 5–8 Toyota dealers within a 100-mile radius. Ask for their out-the-door price on the specific trim and color you want. This creates competition and immediately reveals who’s marking up and who’s not.

At CarEdge.com, you can check what others are actually paying for a RAV4 in your area. Real transaction data beats guesswork every time.

Markup culture varies wildly by region. Dealers in the Southeast and parts of the Midwest tend to be more competitive on Toyota pricing than coastal metros. A 3-hour drive could save you $3,000–$5,000 on a RAV4 Prime.

These are the best states for car buying, but keep in mind that you’ll always pay sales taxes to whichever state you reside in.

This is the sneaky markup. Dealers will add nitrogen-filled tires, door edge guards, all-weather mats, and paint protection — items that cost them $200 total — and charge you $1,500–$2,500 as a “dealer accessory package.” This is a markup by another name.

Ask specifically: “What dealer-installed accessories are included, and can they be removed from the price?” If the answer is no, that’s a red flag.

Check out our guide to dealer add-ons and fake fees.

Toyota’s allocation system doesn’t work exactly like Ford or Chevy’s factory ordering, but many dealers will take a priority order or put you on an allocation list at MSRP. If you can wait 6–12 weeks, this is one of the best ways to get a fair price on a Hybrid or Prime.

Just make sure to get your out-the-door price in writing with the dealership when you place the order. You don’t want to play any games when your car finally arrives.

End-of-month, end-of-quarter, and late in the model year (September–November) are when dealers are most motivated to move units and hit manufacturer bonus targets. That $2,000 markup in March might become an MSRP deal in October.

These are the best times to buy a car.

Before you walk into any dealership, write down your maximum price. If the deal doesn’t hit that number, leave. Every single time. The most powerful negotiation tool you have is your willingness to walk away — and dealers can sense it.

As Ray always says: “The dealer needs to sell you a car more than you need to buy one today.”

If RAV4 markups are making your blood pressure spike, it’s worth considering whether a competitor might give you better value right now.

The point isn’t that these vehicles are better than the RAV4 — it’s that paying $5,000+ over MSRP for any vehicle is rarely a smart financial move when comparable options exist at fair prices.

Let’s do the math that dealers hope you won’t do.

Say you pay a $5,000 markup on a RAV4 Hybrid XLE Premium. Here’s what that actually costs you:

And here’s the kicker: that $5,000 markup does not increase your vehicle’s resale value. When you go to sell or trade in, the car is worth the same whether you paid MSRP or $5,000 over. You’re just eating that loss.

The market is always changing, and the data gives us clues about what might be on the horizon for RAV4 shoppers:

The Toyota RAV4 is a fantastic vehicle — there’s a reason it sells in huge numbers year after year. But a good car at a bad price is still a bad deal.

Here’s your takeaway: On a gas RAV4, you should be paying MSRP or less. On a Hybrid, target MSRP. On a Prime, don’t exceed $2,000–$3,000 over MSRP, and expand your search radius before accepting more. Never pay for mandatory dealer-added accessories you didn’t request, get multiple quotes, and always be willing to walk away.

The dealers marking up RAV4s by $5,000+ are banking on two things: your impatience and your lack of information. Now you have the information. Don’t let impatience be the thing that costs you thousands.

For personalized deal analysis and real-time pricing data, check out the tools at CarEdge.com — we’re here to make sure you never overpay.

Have a RAV4 deal you want us to evaluate? Share it in the CarEdge Community forum for others to chime in.