CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

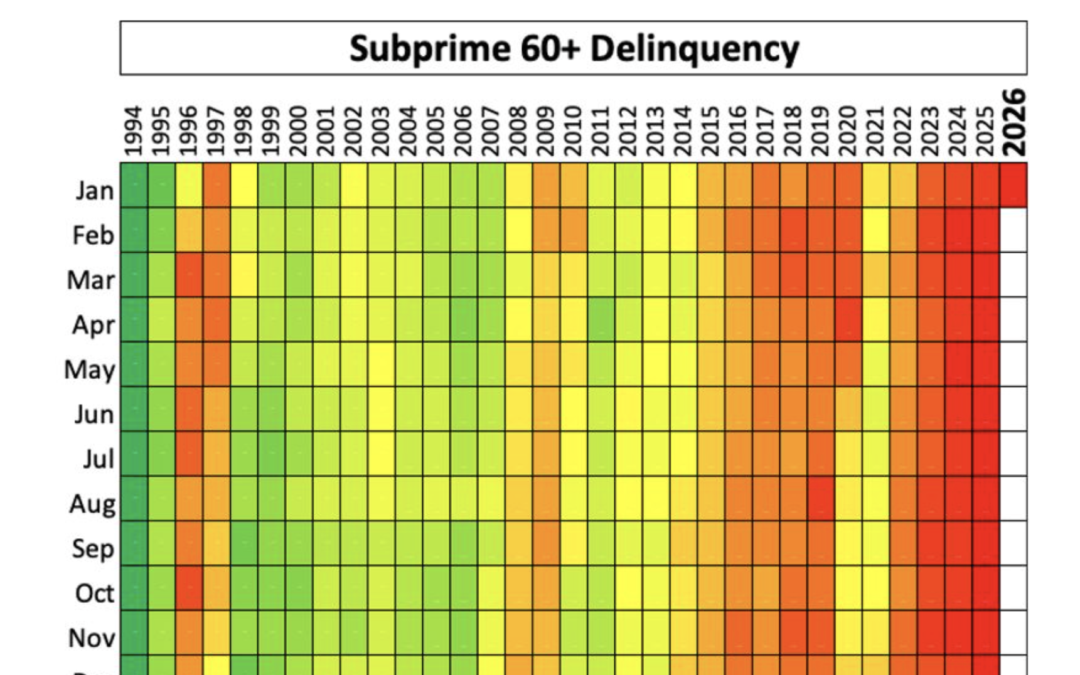

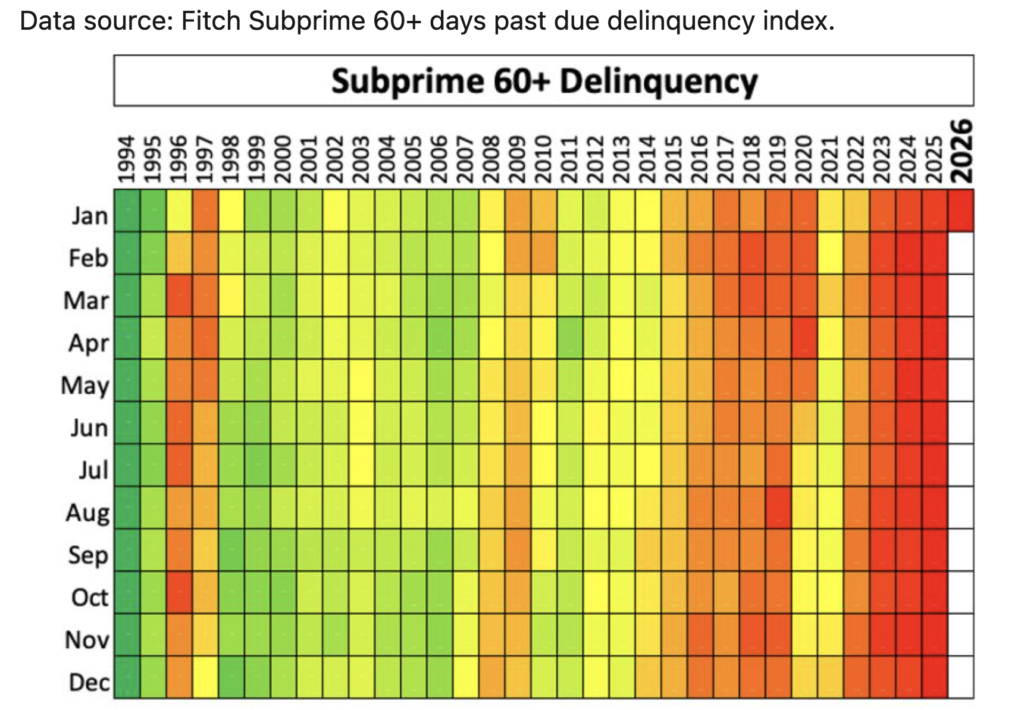

The numbers are in, and they’re alarming. Subprime auto loan delinquencies have reached their highest level in 32 years — a record stretching all the way back to January 1994. According to data published by Fitch and analyzed by industry expert Bill Ploog, the January 2026 figures mark a 385-month record high for 60-plus-day past-due delinquencies among subprime borrowers.

So what does this mean for everyday car buyers, the auto industry, and the future of car prices? Let’s break it down.

A delinquency heat map shared by Ploog covering 385 months of data paints a stark picture. Green represents the lowest delinquency rates for a given month across multiple years, red represents the highest, and yellow marks the midpoint.

For subprime borrowers — those with lower credit scores — the chart has been deep red for nearly four consecutive years, from 2023 through early 2026. That means the percentage of subprime auto loan holders who are 60 or more days behind on their payments is at the worst levels seen in over three decades.

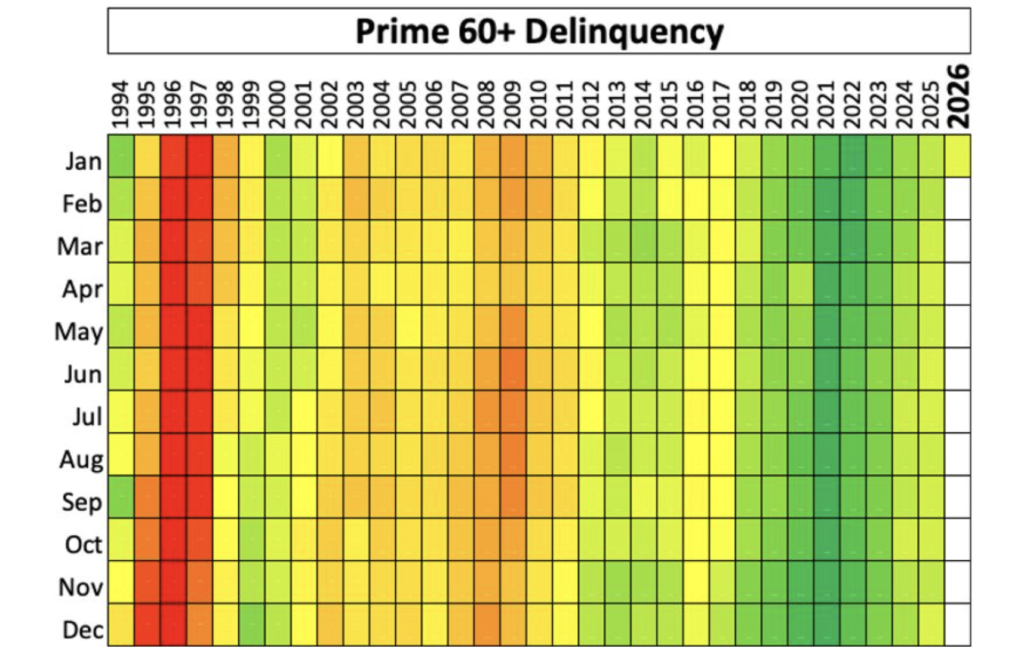

Meanwhile, prime borrowers — those with good credit — are doing just fine. Their delinquency rates remain healthy and stable. The crisis is concentrated squarely among those who can least afford it.

When a borrower falls 60 or more days behind on their auto loan payment, banks begin seriously considering repossession. The vehicle gets seized, sent to auction, and sold — often for far less than what’s owed on the loan. It’s a lose-lose scenario: the borrower loses their car and likely takes a devastating hit to their credit, while the lender absorbs a loss.

This isn’t just a rearview mirror metric. Because the data reflects accounts that are already 60-plus days past due, it’s showing us the consequences of lending decisions made months or even years ago. The decisions that got us here were baked in long before the numbers showed up on the chart.

Several converging factors have created what many are calling bubble territory in auto lending:

As Ray Shefska, a 43-year auto industry veteran and co-host of CarEdge Live, put it: “What more clearly do you need to see that suggests there’s a bubble going on?“

Industry voices are increasingly sounding the alarm on ultra-long auto loans. Brian Binstock, a well-known figure in automotive retail, recently posted that 84-month car loans are “a death trap for customers” — and bad for dealers too.

We’ve been warning against 84-month loans for years.

Here’s the logic: when a dealership puts a customer into a 7-year loan, that customer is effectively removed from the market for the better part of a decade. They can’t trade in, they can’t upgrade, and they’re stuck underwater on a depreciating asset.

“Dealers become enamored with short-term profit gains and don’t look at the long-term ramifications,” Ray explained. “When you put people into 84-month and 96-month auto loans, you are essentially taking them out of the market. Two or three years from now, the same dealers are going to be wondering how to get their customers back. You don’t. You can’t.”

This dynamic is compounded by the decline of leasing. During COVID and the chip shortage, manufacturers pulled back on subsidized lease programs. Leasing, which once represented 32–33% of all vehicle sales, dropped to roughly 17–18%. Leasing had the built-in benefit of cycling customers back into the market every three years. Without it, the industry has leaned harder on long-term financing — with devastating consequences.

The subprime auto loan crisis also raises serious questions about the investors buying asset-backed securities (ABS) tied to these loans. Companies like Carvana, whose loan portfolios skew heavily subprime, package and sell these loans to investors on Wall Street.

“Why would you look at these stats, look at that chart, and say ‘Yeah, let’s buy that stuff’?” Zach Shefska asked during the show. “What could possibly go wrong? We are at a 32-year high, and yet it doesn’t set off alarm bells on Wall Street.“

The parallels to the 2008 housing crisis are hard to ignore. Back then, lenders were approving mortgages for anyone who could “fog a mirror.” Today, the same dynamic is playing out in auto lending. If you can prove you have a pulse and a minimal income, there’s likely a lender willing to approve you — often at predatory interest rates and on terms designed to maximize lender and dealer profit at the borrower’s expense.

Here’s where it gets interesting for anyone shopping for a vehicle. If subprime delinquencies continue to climb and more borrowers are effectively locked out of the market — whether through repossession, negative equity, or simply being trapped in a long-term loan — demand for vehicles should eventually decline.

Basic economics says that when demand drops and supply holds steady, prices come down. That could mean more affordable cars in the future — but it’s a long road to get there.

There’s also a manufacturing angle. If automakers recognize that a growing share of buyers are locked into 6-, 7-, or 8-year loans, they may reduce production to avoid flooding dealerships with inventory that has no buyers. That could temper the price relief somewhat.

As Ray noted: “You take these people out of the market, there’s less demand. When you take out demand and keep supply the same, prices should go down. That should be what happens.“

But he also cautioned that financial engineering — creative lending programs designed to squeeze more buyers into the market — could delay or prevent that correction from ever fully materializing.

The auto loan crisis doesn’t exist in isolation. Consumer debt across the board is at record highs. Credit card balances continue to climb month after month, and most cardholders make only minimum payments — a strategy that can take 30 years to pay off a balance.

“We as a society have created this cycle, and we need to break the cycle,” Ray said. “We need to say it’s okay if you don’t have the latest and the greatest. Just have something that works and works well.“

The data tells a story of a system that incentivizes short-term consumption over long-term financial health. Lenders profit from high-interest, long-term loans. Dealers profit from moving units today. Finance managers profit from maximizing their pay plans. And borrowers — especially subprime borrowers — bear the consequences.

The 32-year record in subprime auto loan delinquencies is more than a statistic — it’s a warning signal for the entire auto industry and for consumers alike. The combination of extended loan terms, loose lending standards, record negative equity, and declining borrower creditworthiness has created conditions that many industry experts are calling unsustainable.

Whether this leads to a meaningful correction in car prices, a wave of dealership struggles, or a fundamental rethinking of how auto lending works in America remains to be seen. But one thing is clear: the current trajectory isn’t working for the people it’s supposed to serve. Being informed, making disciplined financial decisions, and living within your means isn’t just good advice — in today’s auto market, it’s essential.

If you’re planning to buy a new or used vehicle this spring, understanding the current state of the car market is essential. With average new car prices hovering near $50,000, used car interest rates exceeding 10%, and wildly different inventory levels across brands and regions, the landscape is anything but simple.

Here’s a comprehensive breakdown of the new and used car markets for spring 2026, including where the deals are, which brands give you the most leverage, and whether now is the right time to buy or sell.

The average transaction price for a new car is now almost $50,000. That staggering figure has a ripple effect across the entire market. Fewer consumers can afford to participate, and those who can are increasingly willing to stretch their budgets. In fact, 20% of new car buyers are now taking on monthly payments of $1,000 or more—a number that becomes even more alarming when you factor in insurance costs that can add another $300 to $500 per month.

The result? Automakers are essentially appealing to a shrinking pool of buyers who can actually afford these vehicles, while a growing number of consumers are being priced out of the new car market entirely.

One of the most important metrics to understand before walking into a dealership is market day supply. Currently, the nationwide new car market day supply sits at 98 days, meaning it would take more than three months to sell all available inventory at the current sales pace. Dealers have roughly 2.7 million new cars in stock.

A 98-day supply is relatively high compared to the pandemic era when inventory was severely constrained. Generally speaking, the higher the day supply, the more leverage you have as a buyer.

But there’s a nuance: not all brands are on the same page.

The differences in inventory across brands are dramatic, and they directly impact how much room you have to negotiate:

What constitutes a “great deal” is entirely relative. A great deal on a Lexus might mean paying MSRP with no added fees, while a great deal on a Volkswagen could mean thousands off the sticker price. Especially for the slowest-selling car in America.

Inventory levels also vary significantly by state. For example, Maine has a 114-day supply of new cars, while Utah has just a 43-day supply. Your local market dynamics—including regional demand, weather patterns, and dealer competition—will influence the deals available to you.

There’s a silver lining in the spring 2026 new car market. Industry expectations point toward lower overall sales, which should translate to more deals for consumers. Additionally, there are still 580,000 leftover 2025 model year vehicles sitting on dealer lots.

With the Federal Reserve holding steady on interest rates, manufacturers are stepping in with subvented financing rates—think 0%, 0.9%, and 1.9% APR—to move aging inventory. Keep in mind, however, that these promotional rates typically require top-tier credit. As your credit score drops, the rates climb. Here’s what it means to be a well-qualified buyer.

Leasing is also making a comeback. About a quarter of new car customers are now choosing to lease, drawn by advertised payments of $250–$350 per month as a more affordable alternative to buying. The best lease deals of the month include zero-down lease deals, even for a few luxury models.

Overall, the spring 2026 new car market lands in neutral-to-fair territory. It’s neither a strong buyer’s market nor a seller’s market. However, it tilts decidedly toward a buyer’s market for leftover 2025 vehicles, where dealers and manufacturers are eager to clear inventory. For current model year vehicles from popular brands, you’ll need to work harder to secure a meaningful discount.

The average transaction price for a used car in 2026 is $26,000. Used car prices are up 18% over the past five years and 4% year-over-year. While that’s roughly half the cost of a new car, don’t be fooled into thinking used vehicles are affordable. The average interest rate on a used car loan is over 10% APR, which significantly inflates the total cost of ownership and monthly payments. For used car buyers with bad credit, APRs easily top 15%.

The used car market has a 49-day supply of inventory—considerably tighter than the 98-day supply on the new car side. While that’s 5% higher than last year, it’s still lower than the 2022–2024 period. In short, used car inventory remains tight.

One of the most fascinating dynamics in today’s used car market is the K-shaped divergence in vehicle values:

Why is this happening? Many consumers who are priced out of the new luxury car market are turning to pre-owned luxury vehicles instead, driving up demand and values in that segment.

The composition of available used car inventory should give buyers pause:

The quality of used cars available today may be at its lowest level ever in terms of mileage, vehicle condition, and dealer preparation. This makes getting a pre-purchase inspection before buying any used car absolutely essential.

Spring is historically when used car values appreciate, and 2026 is no exception. Auction data shows that used car values have already started appreciating 2–3 weeks earlier than normal. This trend is driven by dealers stocking up on inventory ahead of tax return season and the warmer weather that brings more buyers to dealerships.

This has two important implications:

Unlike the neutral new car market, the used car market tilts toward a seller’s market for spring 2026. Tight inventory, rising prices, seasonal appreciation, and high financing costs all work against buyers. If you must purchase a used vehicle this spring, do your homework on local pricing, get pre-approved for financing to avoid dealer markup on rates, and always get an independent inspection.

Whether you’re buying new or used this spring, the single most important thing you can do is research your specific market. National averages tell one story, but your local brand inventory, regional pricing, and available incentives tell another. Arm yourself with data before you set foot on a dealer lot, and you’ll be in a far stronger position to negotiate.

If you’re thinking about trading in your car, when you do it matters almost as much as what you’re trading in. We’re talking about a difference of several hundred dollars based purely on timing. For high-dollar luxury models, large SUVs, and trucks, the difference can reach into the thousands.

Spring 2026 is almost here, and it happens to be the best time of year to get the most for your trade-in. There are some interesting reasons why dealerships pay more for trade-ins during the spring.

In this guide, we’ll break down exactly why spring is your best window, what makes dealers more generous during this season, and how you can position yourself to get every dollar your car is worth.

Here’s what happens every spring: millions of Americans get their tax refunds, and a significant chunk of that money goes toward buying a car. Usually, tax refunds tend to have a more pronounced impact on the used car market compared to the new car market as budget shoppers head out in droves. This is great news for sellers.

Dealers know this, and they start scrambling for inventory in March to meet the surge in demand.

When dealers need inventory, your trade-in becomes more valuable to them. During tax refund season, the prospect of a buyer walking in to buy your trade-in makes dealers more willing to pay you a fair trade-in value. They’d rather buy your car than have to haul more inventory from dealer auctions to their lot.

Dealers are forward-thinking. By April and May, they’re already preparing for summer, which is traditionally one of the busiest car-buying seasons. Families plan road trips, and people simply feel more optimistic when the weather improves. Most of us are more likely to spend money when we’re in a good mood.

Your trade-in in April isn’t just inventory for today—it’s inventory they’re confident they can move quickly over the next few months. That confidence translates into better offers for you.

👉 Review these trade-in tactics for success, no matter when you’re in the market.

Here’s a reality of the car business: every day your trade-in sits on their lot costs them money. Interest on their floor plan financing, depreciation, and opportunity cost all add up. In the business, we call this ‘floorplanning costs’. In spring, dealers know they can turn your trade-in faster, which means less risk. Less risk means they can afford to pay you more.

Compare that to trading in your car in November when their lot might be full and sales are slowing down. Same car, different value, purely based on how quickly they think they can sell it.

This one’s practical: spring weather makes used cars look better and sell faster. Your car is cleaner, buyers can actually inspect it without freezing or getting soaked, and test drives are more pleasant.

Convertibles and sports cars particularly benefit from spring timing—nobody’s excited about a convertible in January, but in April? That’s a different story. Even for regular sedans and SUVs, warmer weather means more foot traffic at dealerships and more impulse purchases.

The spring selling season doesn’t end on June 1st. Early summer continues to be a strong time for trade-ins, though you start to see the window closing as July progresses.

Come June, many families realize that their current vehicle isn’t going to cut it for that big road trip they’ve been planning. SUVs and minivans move quickly during this period. If your vehicle fits that profile, June can be just as good as April.

High school and college graduations create a wave of first-time car buyers in May and June. Parents who promised their kid a car after graduation are shopping, and young adults entering the workforce need transportation. This is definitely more noticeable on the used car market.

By late July, dealers start shifting their focus beyond the summer rush. They’re less interested in taking on trade-ins because they’re trying to clear space for incoming vehicles for the next model year. After all, those typically arrive around autumn. Your trade-in value starts dropping not because your car got worse, but because dealer priorities changed.

If you’re considering a summer trade-in, get it done before the Fourth of July for best results.

These are the worst months for trade-in value. Dealer lots are quieter, buyers are focused on holiday expenses, and bad weather keeps people home. Dealers also know that anyone trading in during these months probably needs to, which weakens your negotiating position.

Winter weather also works against you. Road salt, dirty conditions, and gray skies make every used car look worse than it actually is. It’s silly, but it’s true (especially if you live in a cold climate).

During this period, dealers are laser-focused on moving current-year new inventory before next year’s models arrive. They’re already drowning in cars and the last thing they want is your trade-in adding to the pile. You’ll get lowball offers simply because they don’t have room or attention for your vehicle.

Post-holiday periods are tough because buyers have tapped out their budgets on gifts, travel, and celebrations. Fewer buyers means dealers need less inventory, which means lower trade-in offers for you.

1. Get your car in good shape

Don’t wait until April to think about this. Take February and early March to get your car in the best possible condition:

2. Get multiple offers online

This should be done when you’re finally ready to trade-in. Before you accept any offer, be sure to compare offers from multiple buyers, such as:

Spring timing works in your favor because all of these buyers are competing for the same limited inventory. Use that competition.

3. Time it right

The sweet spot is mid-March through May. Early enough that you’re ahead of the summer rush, but late enough that tax refunds are flowing and dealers are in a mood to buy.

Memorial Day weekend can still work, but you’re cutting it close. After that, you’re into the gradual decline of summer.

4. Consider your vehicle type

Some vehicles have their own timing:

Getting the most for your trade-in is about understanding basic supply and demand. When dealers need inventory and have confidence they can sell it quickly, they pay more for trade-ins. Spring offers that perfect combination of tax refund money, optimistic buyers, good weather, and dealer demand.

If you’re planning to trade this year, start preparing your vehicle now. Get it cleaned up, gather your paperwork, and plan to gather some official offers soon. The difference between trading in during the best month versus the worst month can easily be $1,000–$2,000 on a typical vehicle.

Your car isn’t getting any younger, but at least you can control when you trade it in. Make spring 2026 work for you.

👉 Use this trade-in checklist to avoid mistakes and get the best deal

Luxury vehicles are packed with features and performance, but not all of them are built to last. In fact, luxury models tend to rank lower for reliability than their more affordable counterparts. That doesn’t quite make sense, does it? Often, the saying ‘you get what you pay for’ couldn’t be further from the truth.

With repair costs climbing and technology becoming more complex every year, reliability matters more than ever in 2026. Which luxury cars are most reliable in 2026? To answer this question, we can take a look at the luxury sedans, crossovers, and SUVs with the highest reliability scores from Consumer Reports. There are some clear winners.

Here are the most reliable luxury cars and SUVs this year, and what the numbers really mean for buyers.

Consumer Reports bases its reliability ratings on data from hundreds of thousands of vehicle owners. CR tracks reported issues across multiple categories — including powertrains, electronics and infotainment, and more.

Each vehicle receives a predicted reliability score based on historical data, recent redesigns, and reported trouble areas. A higher score means fewer expected problems.

But reliability is only part of the equation. Depreciation, resale value, and ownership costs matter too, and sometimes the most reliable vehicle isn’t the one that makes the most financial sense long term.

For a more complete picture of how these reliable luxury vehicles affect your wallet, we’ve included expected 5-year depreciation for each model. Let’s dive in.

Consumer Reports Reliability Score: 84/100

CarEdge Projected Depreciation: 41% over 5 years

The Lexus IS stands at the top of the luxury sedan rankings this year. Its strong reliability score isn’t surprising. Lexus continues to rely on proven powertrains and incremental updates rather than risky overhauls.

From a financial standpoint, projected depreciation of 41% over five years is competitive for a luxury sedan. That balance of durability and value retention makes the IS one of the safest bets in this segment.

Consumer Reports Reliability Score: 77/100

CarEdge Projected Depreciation: 35% over 5 years

The current-generation ES Hybrid continues to perform extremely well in reliability rankings. While a redesign is coming in 2026, the outgoing model benefits from years of refinement.

The standout number here may actually be depreciation. A projected 35% five-year value loss is excellent for a luxury vehicle.

Consumer Reports Reliability Score: 73/100

CarEdge Projected Depreciation: 40% over 5 years

The BMW 2 Series earns a solid reliability score while still delivering the driving dynamics buyers expect from the brand.

Depreciation sits at 40% over five years, which is fairly typical for luxury performance models.

Consumer Reports Reliability Score: 65/100

CarEdge Projected Depreciation: 46% over 5 years

Audi’s naming structure is shifting for 2026, with electric models taking even numbers, and ICE models getting odd numbers. So, the Audi A4 is now the 2026 Audi A5.

A CR reliability score of 65 is respectable but not class-leading. Depreciation, however, is projected at 46% over five years. Buyers should expect faster value loss than competitors from Lexus, for instance. Even a few BMW models do better.

Consumer Reports Reliability Score: 84/100

Shockingly, the Macan ties for the highest reliability score in the Consumer Reports’ most recent testing. That’s impressive for a performance-oriented luxury crossover.

Porsche has refined this platform over time, and it shows. Porsche shoppers looking for a family-sized sporty SUV without sacrificing dependability should take note.

Depreciation data isn’t yet available, but reliability at this level is uncommon among luxury brands.

Consumer Reports Reliability Score: 81/100

CarEdge Projected Depreciation: 61% over 5 years

Is the Model Y still considered a luxury model? Considering the advanced driver assistance and performance features, we think it’s at home in this category. The Model Y posts a strong reliability score for 2026, but depreciation tells a different story.

With projected five-year value loss at 61%, it carries the steepest depreciation of any model in this group. That doesn’t mean it’s a bad vehicle. It just means buyers should understand the long-term financial trade-offs before buying. In fact, the used market (or a lease) is the smart choice for most drivers.

Consumer Reports Reliability Score: 71/100

CarEdge Projected Depreciation: 41% over 5 years

The Lexus NX remains one of the safer choices in the compact luxury SUV space. Reliability is above average, and depreciation is reasonable.

It’s worth noting that plug-in hybrid models vary in reliability, with the NX PHEV scoring much lower. The NX Hybrid earns higher scores. Buyers should compare powertrains carefully.

Consumer Reports Reliability Score: 71/100

According to Consumer Reports, the Cayenne delivers above-average reliability for a midsize performance SUV in 2026.

While it doesn’t lead the segment, it’s far above competing models from Mercedes-Benz and Audi. Depreciation data is not yet available, but expect ownership costs to vary widely depending on configuration and options.

Consumer Reliability Score: 69/100

CarEdge Projected Depreciation: 33% over 5 years

The Lexus RX may not post the highest reliability score here, but its depreciation projection is the lowest in the group at just 33%.

That combination of strong durability and excellent value retention makes it one of the smartest luxury SUVs for your wallet in 2026. At today’s typical car prices, lower depreciation will often outweigh small reliability score differences.

Consumer Reports Reliability Score: 65/100

CarEdge Projected Depreciation: 59% over 5 years

The BMW X5 lands in the middle for reliability, but depreciation is steep at 59% over five years.

For buyers who lease or plan short ownership periods, this may matter less. But long-term owners should factor both repair risk and resale value into their decision.

A few trends stand out in the latest Consumer Reports reliability rankings and CarEdge depreciation data:

One important takeaway: the most reliable vehicle is not always the best long-term financial decision. Strong resale value can offset slightly lower reliability scores, while steep depreciation can erase the advantage of a high reliability rating.

Luxury buyers in 2026 have solid options, but understanding both durability and value retention is what separates a smart purchase from an expensive one.

See the complete luxury vehicle reliability rankings at Consumer Reports, and check out depreciation forecasts for new and used vehicles at CarEdge.

On February 13, Bloomberg reported that Ford has discussed the possibility of a joint venture with Chinese automakers in recent talks with the Trump administration. According to people familiar with the discussions, such a controversial move could help American automakers compete against rapidly rising Chinese brands.

Sources said Ford CEO Jim Farley raised the topic during meetings with administration officials Jamieson Greer, Transportation Secretary Sean Duffy, and EPA Administrator Lee Zeldin at the Detroit Auto Show.

If Ford partners with a Chinese automaker, it would mark a historic shift for the American auto industry. Here’s how it could unfold in the near term.

According to Bloomberg’s sources, a possible deal would involve both partners sharing profits and technology. Ford would gain manufacturing and technology advantages over domestic competitors, while Chinese automakers would secure entry into the coveted U.S. market.

What would this look like operationally? Given Ford’s recent $19.5 billion in EV write-offs, building new facilities from scratch seems unlikely. Instead, Ford would probably retool an existing plant. The company’s BlueOval City campus in Tennessee is the natural candidate. These brand-new facilities were already designed for next-generation manufacturing. With EV sales falling short of projections, Ford leadership is likely seeking ways to recoup the $5.6 billion invested in the project.

Would these vehicles be sold at Ford dealerships? Given the power of dealership lobbies in America, almost certainly. Don’t expect Ford to pursue direct-to-consumer sales anytime soon, especially after the recent EV struggles.

In 2026, the average price of a new vehicle continues to hover around $50,000. With affordability continuing to be the number one challenger for American drivers, a joint venture between Ford and a Chinese automaker would be expected to introduce more affordable, tech-heavy options into the market.

In Europe, Chinese OEMs like BYD offer entry-level EVs for around $25,000 USD. Luxury options are going toe-to-toe with German brands for half the price. In the United States, we could see the ‘affordable EVs’ Farley has long spoken about arrive as a product of this rumored joint venture, with capable, advanced models priced under $30,000.

Chinese automakers like BYD, Chery, and JAC have already established themselves in Latin America. By late 2025, BYD had sold over 80,000 vehicles in Mexico alone, with sales doubling in 2025 as the company opened dealerships nationwide. BYD now has a Tesla-like presence in Mexico, commanding 70% of all EV sales.

Canada reached an agreement with China earlier this year allowing annual imports of 49,000 Chinese EVs at a 6.1% tariff rate—shockingly low by global standards. Canadian Prime Minister Mark Carney is seen as leading an anti-Trump trade coalition, and this automotive deal is viewed as the clearest signal yet. This development is particularly significant given the importance of Canadian manufacturing to American automakers.

The potential Ford-China partnership represents a dramatic departure from traditional American automotive strategy. With Chinese automakers already gaining ground in Latin America, and now entering Canada under favorable terms, U.S. manufacturers face mounting pressure to adapt.

Whether Ford moves forward with this controversial approach or not, one thing is clear: the competitive landscape is shifting, and American automakers can no longer afford to ignore the existential threats coming from China.

Drivers are increasingly getting pushed into the used market. In January, the average transaction price (ATP) for a new vehicle was $49,191, a 1.9% year-over-year increase and an all-time high for January. Adding to the pain, automakers lowered sales incentives last month, with the average package equal to 6.5% of ATP, down from 7.5% in December 2025.

While buying used can mitigate costs, a smooth purchase isn’t guaranteed. There are some risks and traps to watch out for when buying any used car.

Below are a few recent accounts of used car buyers who weren’t so lucky in their shopping experience, along with steps you can take to avoid avoid making their mistakes.

The first used-car buying horror story we’ll highlight is a driver who was quoted for over $7,000 in repairs less than 24 hours after purchasing their vehicle.

According to this driver’s Reddit post, they purchased a 2014 BMW 3 Series with 45,000 miles under assurance that the car was in good condition, with a solid CarFax to boot.

The Reddit user and BMW purchaser wrote: “The following morning on Tuesday, lights come on for brakes and chassis stabilization. I bring it to a reputable shop near me (Virginia) and they say the brakes are completely shot, ABS is leaking fluid everywhere and screws are threaded horribly with damage. The quote was over $7,000 less than 24 hours after purchasing the vehicle. Shop ensured me that the car would not pass inspection in its current state.”

They added: “Note to self, always perform a pre-purchase inspection.”

It only took this driver 30 miles to realize their mistake: they skipped an independent pre-purchase inspection (PPI). A test drive and dealer assurances don’t negate a buyer’s need for a PPI, which can catch issues that a test drive won’t.

Once a PPI reveals issues, a driver can walk or use the information as leverage during negotiations. If a dealer refuses a PPI, you should always walk away, and including a contingency in your contract stating that the vehicle must pass a state inspection within a certain number of days (ex: 3 to 7) adds protection.

A PPI will cost $150 to $250 on average, which is a pittance in comparison to $7,000+ in repairs. This BMW buyer noted that even if they had purchased an extended warranty, which they didn’t, the warranty wouldn’t cover the repairs since they were pre-existing rather than unexpected, which is accurate.

Regarding the buyer noting that the CarFax looked good, a CarFax report covers data such as reported accidents, title issues, and some service records. However, it won’t detail the driver’s mentioned problems, such as fluid leaks, brake condition, or ability to pass a state inspection, underscoring the importance of a PPI. Learn more about the importance of a PPI.

Next, we’ll be looking at a used car shopper who heard a concerning noise when turning a vehicle’s steering wheel during a test drive.

The dealer told this shopper they’d fix the issue under the manufacturer’s warranty, but only after the driver signed the paperwork. This shopper moved forward since the dealer said they’d include a right to rescission in the agreement’s documentation. However, when the dealer’s finance department reviewed the documentation to verify a right to rescission clause upon the buyer’s request, none was found.

On Reddit, this shopper, who ultimately walked, said the dealer created a “We Owe You” document, but the language was a bit loose and could be interpreted in their favor.

Ideally, you shouldn’t sign until an issue is fixed.

Still, this type of agreement isn’t guaranteed, as one Genesis manager replied to this Reddit post: “I will not fix it and have you come back, because by then you bought elsewhere.”

If a dealer insists on you signing first with a repair scheduled later, you’ll need to request a binding, enforceable agreement outlining what will be repaired, who is paying, when it will be completed, and what occurs if the repair isn’t done. Clearly documenting these terms means retaining leverage and avoiding situations where a dealer can delay, minimize, or interpret vague promises to their advantage.

Some used car buyers assume that an extended warranty equals comprehensive protection, but assumptions and lack of verification can leave even those with an extended warranty in the lurch, as was the case with this Reddit user.

The used-car buyer reported purchasing a used Jeep Wrangler from a GM dealer, obtaining an extended powertrain warranty, and having the vehicle’s engine blow from overheating five days later. After getting their Jeep towed to the dealer and claiming the warranty for repairs, an inspector denied the claims due to aftermarket tires, wheels, and lift parts, which the buyer said were pre-existing.

This is another example of a driver that would’ve benefited from a PPI by an independent mechanic. A PPI would’ve typically highlighted the presence of aftermarket parts, which often void warranties, while revealing problems that pre-empted the engine blowout. Any discovered problems could’ve caused this buyer to walk or given them more negotiation leverage.

There’s also the issue of carefully reading a warranty.

Additionally, carefully reviewing the warranty would’ve helped them understand:

Confirming coverage in writing from the dealer or warranty provider solidifies protection.

Avoiding the used-car-buying horror stories above is doable with a bit of knowledge and preparation. However, there’s an easier way to buy in 2026. CarEdge’s Concierge streamlines the process by matching you with a shopping expert who understands your needs, launches your search, completes dealer outreach, and handles negotiations from start-to-finish. How much is your time worth? Say goodbye to the dealership games, and have an expert handle it for you!

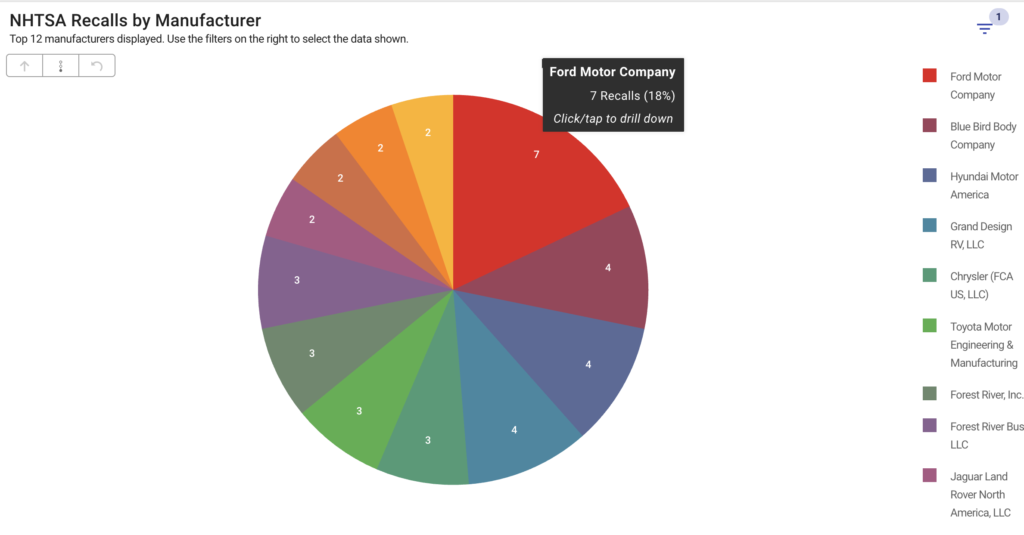

Ford is off to a rough start in 2026. The company just reported its worst earnings miss in four years as EV investments fail to deliver. Making matters worse, Ford is already leading in 2026 automaker recalls at a time when the company is aiming to better its reputation with consumers.

Less than two months into the new year, Ford has issues seven recalls for Ford and Lincoln models. At the same time, the company is boosting employee bonuses after reporting improvements in “initial quality.”

Two very different headlines. Let’s break it down.

According to the National Highway Traffic Safety Administration (NHTSA), Ford has issued seven recalls in the first 40 days of 2026 alone. Those recalls have already impacted 123,448 vehicles under the Ford Motor Company umbrella.

Models affected this year include the Ford Explorer, Ford Escape, and Ford Transit, among others. Some Lincoln models have also been impacted.

If you own a Ford or Lincoln, it’s worth running your VIN through NHTSA’s free recall lookup tool. Ford CEO Jim Farley has recently hinted that more recalls are likely as the company ‘gets to the root of the problems’, so it would be wise to check your car regularly in 2026.

Ford’s early lead in 2026 follows a difficult 2025. Last year, Ford recorded more than 150 recalls affecting roughly 13 million vehicles, earning the unofficial title of “most-recalled manufacturer.” The year before that, Ford was neck-and-neck with Tesla for the same distinction.

So while it’s still early in 2026, the trend hasn’t exactly reversed.

For context, Hyundai Motor America currently sits in second place this year with four recalls so far.

Here’s where things get interesting. Despite the recall count, Ford leadership recently announced higher companywide bonuses tied to improvements in vehicle quality.

According to reporting from Reuters, CEO Jim Farley told employees during a town hall that bonuses would be set at 130%. The move came after Ford delivered on its goal to improve “initial quality” — a metric that measures repairs in the first 90 days of ownership.

Farley reportedly told employees that initial quality is the best it has been in a decade. He also described the higher payouts as an investment in workers as the company works toward an 8% EBIT margin by 2029.

Ford has struggled for years with high warranty costs and repeated recall campaigns. Farley has previously acknowledged that recalls could rise in the short term as the company works through lingering issues. His argument: initial quality is the better indicator of whether Ford’s turnaround efforts are working. Recalls don’t matter, at least not yet.

On paper, Ford leads the industry in recalls yet again. Internally, leadership says quality metrics are improving in meaningful ways. Strange times indeed for car buyers on the hunt for a reliable, well-built car.

Ford’s early 2026 recall numbers are hard to ignore. Seven recalls in 40 days affecting over 120,000 vehicles is not a good look.

At the same time, the company says its vehicles are performing better in the first 90 days of ownership than they have in a decade, and it’s rewarding employees accordingly.

Both things can be true.

Recalls measure one side of quality. They usually pertain to safety defects and regulatory compliance. Initial quality measures early ownership experience. They don’t always move in lockste, so it will be interesting to see how both evolve in 2026.

For now, Ford remains under a microscope. Whether 2026 becomes another record year for recalls, or the year quality truly turns the corner, is something we’ll be watching closely.

Don’t forget to check your car or truck for recalls. That free tool could become a Ford driver’s best friend if the trend continues this year.

Toyota’s U.S. sales continue to climb in 2026, even as several competitors experience a dip. Even by Toyota standards, four models are outpacing the rest of the lineup by an impressive margin. No matter what the likes of Hyundai, Mazda, or Chevrolet add to their lineups, Toyota continues to widen its lead in the North American market.

If you’re considering any of these models, be prepared to act quickly when you find the right fit. Here’s what’s driving the surge in popularity for these four Toyota models.

January sales surged 72% year-over-year as the Grand Highlander continues to cannibalize Highlander sales. For all of 2025, sales jumped an impressive 91% compared to the debut 2024 model year. These figures include both hybrid and non-hybrid versions.

Why it’s popular: The Grand Highlander offers more space and features than the legendary Highlander. Toyota recently announced that the standard Highlander will go all-electric for 2027. With EV sales still struggling to recover from the “EV winter” following the end of federal tax credits, this shift could push even more buyers toward the Grand Highlander, regardless of how competitive the Highlander EV’s pricing and specs turn out to be.

Sedan sales have plummeted market-wide, dropping from 40% of all light-duty vehicle sales in 2015 to just 10% in 2025. But the Corolla remains a bright spot in an otherwise struggling segment. January sales climbed 12% year-over-year, following a 7% increase for all of 2025.

With world-famous reliability and a starting price of just $24,120 including destination charges, the Corolla continues to be an all-time favorite for commuters. It simply gets the job done.

This month, Toyota is even offering a sub-$250 lease deal on the Corolla. That’s one of the best values on the market.

Last month, Corolla Cross sales jumped 34% compared to January 2025, with Toyota moving 8,542 units of the popular crossover. In 2025, sales climbed 7% over an already strong 2024, blowing the previous record out of the water just four years after the model’s launch. The Corolla has always been popular and reliable, but transforming it into a crossover has proven to be a brilliant move for Toyota’s bottom line.

About a third of the 99,798 units sold in 2025 were hybrids. Negotiating on this popular model will be challenging in 2026, as inventory typically runs well below the market average for Toyota vehicles.

This one’s particularly interesting. After receiving its first major refresh in a decade for the 2025 model year, the Toyota 4Runner has seen sales climb steadily higher. Year-over-year comparisons are tricky, though, since virtually no inventory was available during the first few months of 2025 as dealers awaited initial shipments of the redesigned model.

That said, the numbers tell a compelling story: 2025 sales increased 8% over the previous year, with nearly 100,000 units sold. While not an all-time record, it represents a continued upward trajectory.

There’s a silver lining for 4Runner buyers in 2026: Toyota appears to have more inventory than usual heading into spring. With 57 days of market supply, the 4Runner has better availability than most Toyota models (the brand overall sits at 50 days of supply).

This means negotiating savings on a 4Runner may actually be possible in some cases—especially on the roughly 1,300 leftover 2025 models still sitting on dealer lots. Toyota is also offering competitive manufacturer incentives right now, though deals vary by region, so check availability in your ZIP code.

These four Toyota models prove that even in a competitive market, the right combination of features, value, and reliability can drive continued sales growth. This is great news for Toyota of North America, but it can present new challenges for buyers looking for a deal.

The key takeaway? If one of these models is on your shopping list, don’t wait too long to make your move. Just remember: acting fast doesn’t mean accepting dealer markups or unwanted add-ons. Buying a top-selling car simply means you need to arrive prepared and disciplined (when it comes to your wallet). Stick to your budget, negotiate with confidence, and you’ll drive away in one of Toyota’s hottest sellers without any regrets.

Tired of the dealership games? Learn how CarEdge takes care of it for you.

Presidents Day weekend is almost here, and with the holiday comes some noteworthy new car deals. With the average new car price officially hitting $50,000, more drivers are looking into leasing as a solid option. Leasing is a great way to avoid the steep depreciation that comes along with buying any new car.

This month’s standout lease deals are mostly for leftover 2025 inventory. It’s February 2026, yet over half a million 2025 models remain on dealership lots nationwide. There are also some great lease deals for brand-new 2026 models, which is a bit unusual so early in the year. This means it’s still a buyer’s market.

We’ve combed through February offers to find the best Presidents Day lease deals available now. From zero-down luxury leases to sub-$300 payments on trucks and SUVs, these are the offers worth the test drive.

Be sure to check out our Presidents Day deal hub for more offers.

Presidents Day Lease Deal: $499/month for 36 months with $499 due at signing

It’s rare to see any luxury brand offering a zero-down lease deal, so this one is special.

Browse local Lincoln listings or see offer details.

Presidents Day Lease Deal: $479/month for 36 months with $479 due at signing

Browse local F-150 listings or see Ford offer details.

Presidents Day Lease Deal: $385/month for 36 months with $385 due at signing

Note: This offer expires on February 16, 2026.

Browse local Bronco Sport listings or see Ford offer details.

Presidents Day Lease Deal: $363/month for 36 months with $363 due at signing

See Ford Mustang Mach-E deals, or see Ford offer details.

Presidents Day Lease Deal: Lease the Model Y Rear-Wheel Drive from $547/month for 36 months with $0 due at signing. The Premium All-Wheel Drive and Performance are also eligible for this zero-down offer.

Presidents Day Lease Deal: $379/month for 36 months with $1,709 due at signing (Crew Cab 4WD LT with TurboMax engine)

Note: This offer is for current lessees of 2021 or newer Chevrolet vehicles.

See Silverado listings near you, or see Chevrolet offer details.

Presidents Day Lease Deal: $279/month for 36 months with $1,929 due at signing (Custom Crew Cab 2WD)

Note: This offer is for current lessees of any 2021 or newer Chevrolet. Offer valid through March 2, 2026.

See Colorado listings near you, or see Chevrolet offer details.

Presidents Day Lease Deal: Lease the Sportage Plug-In Hybrid from $269/month for 24 months with $3,999 due at signing.

See Kia listings near you, or see Kia offer details.

Presidents Day Lease Deal: Lease the NX 350 AWD for $509/month for 42 months with $3,999 due at signing.

See Lexus listings near you, or see Lexus offer details.

Presidents Day car deals are worth the hype this year, especially if leasing is on your radar. Whether you’re drawn to a zero-down luxury lease or a great deal on a full-size truck, February 2026 is a great time to lease.

Don’t want to negotiate alone? CarEdge Concierge takes the hassle out of leasing. Our automotive experts handle everything—from finding the perfect vehicle and trim to negotiating your best deal with local dealers. We’ll make sure you’re getting the advertised offer (or better) without the back-and-forth.

Learn more about CarEdge Concierge and let us do the heavy lifting this Presidents Day weekend.

The gap between the fastest and slowest-selling pickups is widening in 2026. With some trucks selling in just over a month, and others sitting unsold for over six months, knowing what’s hot (and what’s not) can make or break your next deal.

That’s why understanding Market Day Supply (MDS) is more important than ever for anyone buying or selling a truck in 2026. At CarEdge, we used real-time inventory and sales data to identify the fastest- and slowest-selling trucks each month.

MDS tells us how long it would take to sell all the current inventory of a particular model at the current sales pace, assuming no new units are added. A low MDS means a truck is selling quickly. A high MDS, on the other hand, signals oversupply, and that can mean buyers have more leverage at the dealership.

Whether you’re buying new or considering a trade-in, here’s what the latest market data from CarEdge Pro reveals about the best-selling and worst-selling trucks in America.

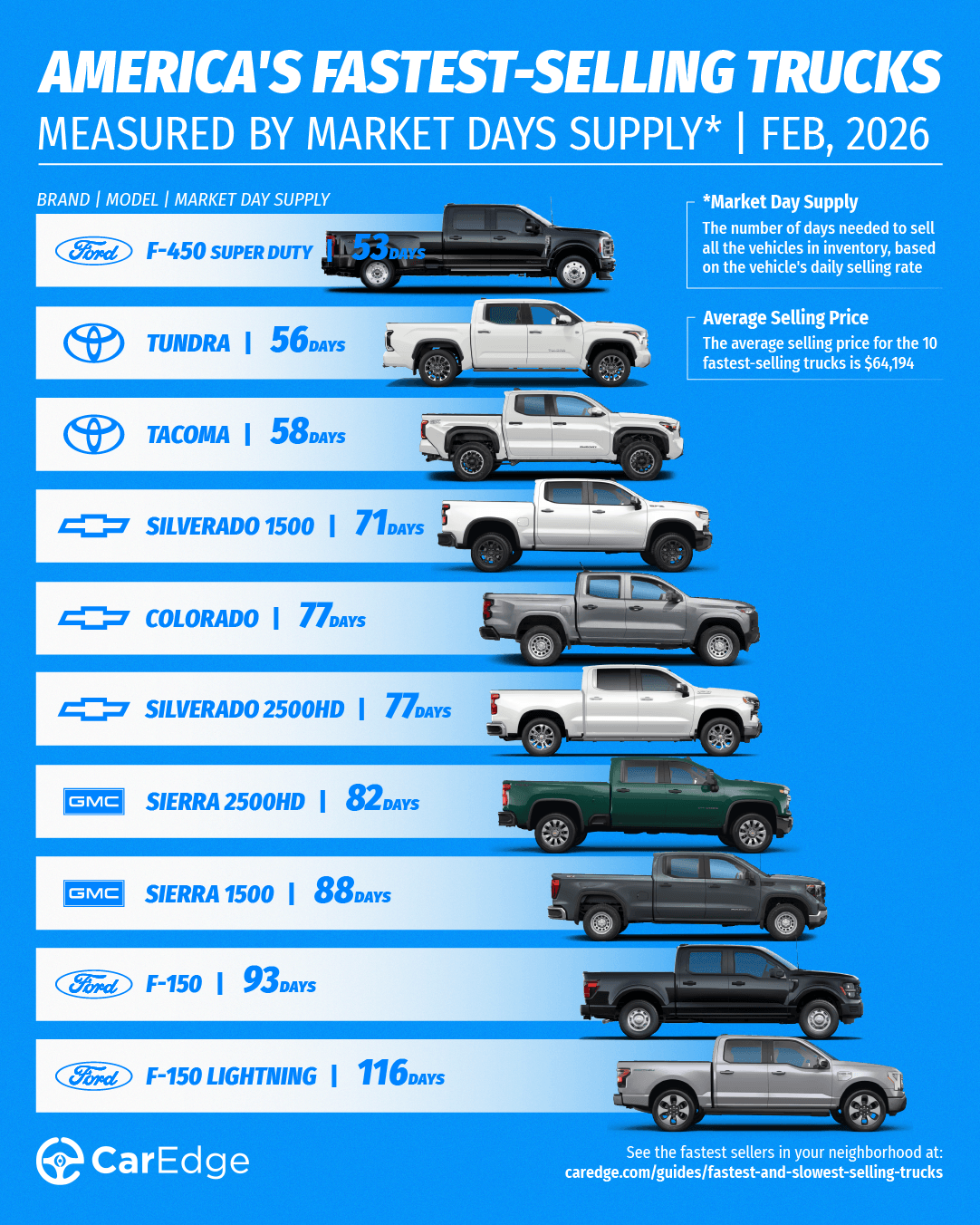

These trucks are in high demand and selling quickly. But if you’re hoping to negotiate a deal on one of these, don’t count on much wiggle room unless you work with a pro.

| Make | Model | Market Day Supply | Total For Sale | 45-Day Sales | Average Selling Price |

|---|---|---|---|---|---|

| Ford | F-450 Super Duty | 53 | 1,555 | 1,318 | $98,065 |

| Toyota | Tundra | 56 | 29,870 | 24,081 | $63,936 |

| Toyota | Tacoma | 58 | 55,275 | 42,861 | $46,088 |

| Chevrolet | Silverado 1500 | 71 | 56,709 | 35,709 | $52,911 |

| Chevrolet | Colorado | 77 | 19,009 | 11,146 | $41,844 |

| Chevrolet | Silverado 2500HD | 77 | 22,335 | 13,120 | $66,488 |

| GMC | Sierra 2500HD | 82 | 17107 | 9420 | $81,410 |

| GMC | Sierra 1500 | 88 | 46,625 | 23,731 | $62,347 |

| Ford | F-150 | 93 | 87,124 | 42,293 | $61,217 |

| Ford | F-150 Lightning | 116 | 4,315 | 1,677 | $67,631 |

Source: CarEdge Pro

The Ford F-450 Super Duty is the fastest-selling pickup truck in February 2026. On average, this heavy duty pickup truck sits on the lot for a little under two months before finding a buyer. Toyota’s Tundra and Tacoma are in second and third place, with trucks from GM far behind.

These trucks will be less negotiable as demand exceeds what’s typical for the truck market. Still, never agree to dealership markups or forced add-ons. Remember, informed shoppers always get the best deals.

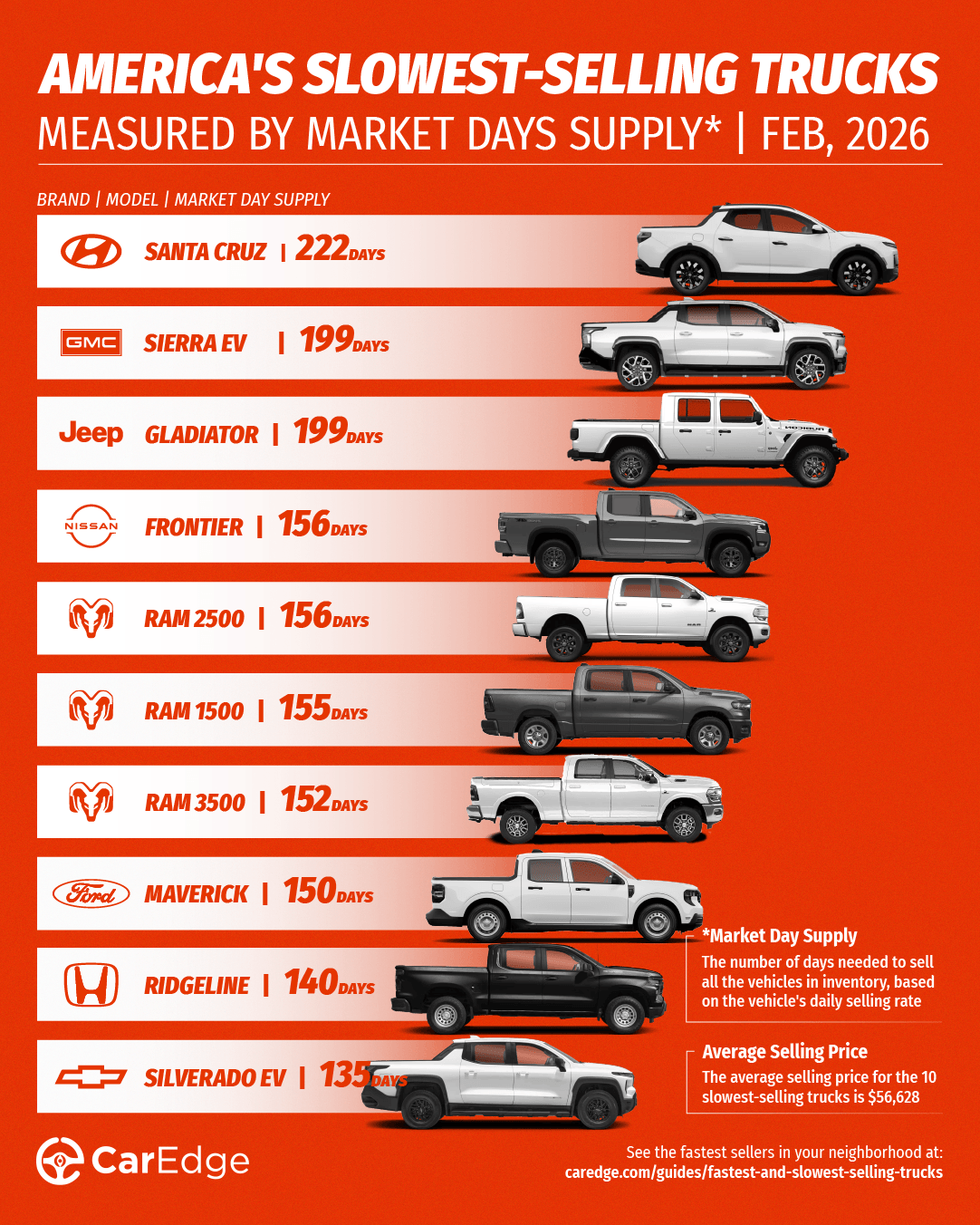

On the flip side, these trucks are struggling to move. Some of these trucks are taking more than six months to sell on average. If you’re in the market, these pickup trucks offer room for negotiation, especially with DIY market insights.

| Make | Model | Market Day Supply | Total For Sale | 45-Day Sales | Average Selling Price |

|---|---|---|---|---|---|

| Hyundai | Santa Cruz | 222 | 10,474 | 2,120 | $36,439 |

| GMC | Sierra EV | 199 | 2,709 | 614 | $81,439 |

| Jeep | Gladiator | 199 | 19,162 | 4,332 | $48,732 |

| Nissan | Frontier | 156 | 21,527 | 6,214 | $39,957 |

| Ram | Ram 2500 | 156 | 31,388 | 9,047 | $68,554 |

| Ram | Ram 1500 | 155 | 66,988 | 19,429 | $60,056 |

| Ram | Ram 3500 | 152 | 10993 | 3263 | $77,020 |

| Ford | Maverick | 150 | 43,224 | 12,933 | $33,930 |

| Honda | Ridgeline | 140 | 11,513 | 3,711 | $45,292 |

| Chevrolet | Silverado EV | 135 | 1,855 | 615 | $74,864 |

Source: CarEdge Pro

The Hyundai Santa Cruz, a truck that was recently sent to the graveyard. Trucks from Stellantis brands (Ram and Jeep) take up four of the bottom 10 spots in February. Sellers can expect these slow-selling trucks to sit on the lot for at least four months, but this creates great chances to negotiate savings for buyers.

As the truck market ebbs and flows, it’s easy to become overwhelmed. Luckily, there are new tools and services available that take the hassle out of buying a truck entirely. Here’s how CarEdge can help.

👉 Negotiate anonymously with CarEdge AI (NEW!)

👉 Have a pro negotiate your deal with CarEdge’s Car Buying Service