CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

If you’re looking to negotiate up to 25% off on a brand-new car, now is the time to focus on remaining 2023 inventory. These cars are just months away from becoming two years old, and dealers are motivated to move them fast. Below are the car brands with the most remaining 2023 models available in late 2024. Make no mistake – these are the most negotiable cars on sale today.

It’s no surprise that Dodge tops the list. Both the Charger and Challenger are now out of production, but thousands of these muscle cars remain on sale, making them prime candidates for huge discounts. Meanwhile, 4.6% of new Dodge Durango inventory are 2023 model years. Even for the Durango, that would be a sky-high figure for any OEM besides Stellantis.

Luxury brand Maserati has struggled with declining sales, and it shows with 19% of their new cars still being 2023 models as of October 2024. Of particular note, 25% of all Maserati Ghiblis on sale are from last year. With more than 400 leftover vehicles across the U.S., Maserati buyers should negotiate steep discounts on these high-end cars.

Like other Stellantis brands, Chrysler is also dealing with leftover stock. The Pacifica, a favorite among families, has over 2,000 2023 models still on dealer lots. Most of these remaining models are Pacifica Hybrids. While the Pacifica is a practical choice, it’s not flying off the shelves, making it a prime candidate for negotiation.

Nearly 7,000 new 2023 Jeeps remain on the market, including a substantial number of Grand Wagoneers—22% of its current inventory. The Grand Wagoneer is by far Jeep’s most expensive model ever. The average selling price for a Grand Wagoneer in 2024 is $102,429. The Jeep Gladiator also has a noticeable portion of its 2023 stock still available.

Here are the other Jeep models with significant 2023 inventory remaining:

| Model | New 2023s (10/2024) | Percent of New Inventory |

|---|---|---|

| Jeep Grand Cherokee | 1,167 | 2.62% |

| Jeep Gladiator | 1,120 | 6.85% |

| Jeep Wrangler | 372 | 1.20% |

| Jeep Compass | 756 | 2.47% |

| Jeep Wagoneer | 274 | 3.88% |

| Jeep Grand Wagoneer | 583 | 22.25% |

Every Jeep model has some 2023 units left, offering a solid opportunity for bargain hunters who are willing to put negotiation know-how to work.

Even in fall 2024, Ford still has nearly 17,000 new 2023 models for sale. Today’s remaining 2023s include popular vehicles like the F-150, F-250 Super Duty, and Mustang Mach-E. With a broad selection of leftover 2023 inventory, Ford dealerships are likely ready to make deals to clear these out before these cars reach their second birthday in 2025.

Mercedes-Benz stands out as a luxury brand with a lingering stock of 2023s, accounting for 2.6% of its U.S. inventory. Higher interest rates have slowed sales, making models across the lineup available for steep discounts. See all remaining 2023 Mercedes-Benz models here.

Here’s a look at how much 2023 inventory the 15 best-selling car brands in America have as of October 2024. We’d wager that Tesla has some remaining 2023 builds awaiting owners, but that data isn’t publicly available. Clearly, Stellantis brands have the most unsold 2023 inventory today.

| Make | New 2023s (10/2024) | Percent of New Inventory |

|---|---|---|

| Jeep | 6,979 | 3.73% |

| Ram | 4,994 | 3.51% |

| Ford | 16,923 | 3.13% |

| Mercedes-Benz | 2,562 | 2.64% |

| BMW | 1,296 | 1.88% |

| Chevrolet | 6,835 | 1.80% |

| GMC | 2,218 | 1.45% |

| Volkswagen | 1,239 | 1.37% |

| Hyundai | 2,762 | 1.32% |

| Nissan | 2,077 | 1.05% |

| Kia | 1,190 | 0.73% |

| Toyota | 1,233 | 0.50% |

| Honda | 877 | 0.43% |

| Mazda | 271 | 0.25% |

| Subaru | 212 | 0.17% |

With 70,000 new 2023 cars still on the market, it’s prime time to negotiate major discounts on last year’s inventory. With these cars becoming nearly two years old, dealers are motivated to clear the lot before 2025 arrives. These remaining 2023 models are the most negotiable cars on sale today. A 25% discount off MSRP is realistic for those looking to buy now.

Ready to master the art of car price negotiation? Start your Deal School online course today. It’s self-guided and 100% free. We’re simply here to help!

2024’s year-end car deals are set to be some of the best in years. Starting with Black Friday and continuing through December, the best time to buy a car is here. With a surplus of inventory, falling interest rates, and holiday sales, dealers and OEMs are motivated to sell. If you’re in the market for a new car, this is the time to pay attention.

Interest rates are expected to gradually decline in late 2024 after hitting a peak earlier in the year. As rates soften, automakers will be offering low APR deals and special financing options to lure buyers who have held off due to high borrowing costs. This means dealerships will be motivated to offer better terms to close sales by the end of the year. This will especially benefit car buyers looking to finance at lower rates.

👉 Check the best year-end deals available now

In 2024, the auto industry is facing a glut of unsold vehicles. Improving supply chains, rising interest rates, and fewer buyers are creating a buyer’s market. Dealerships are sitting on excess inventory that they need to clear out to make space for 2025 models. As year-end car deals approach, buyers will see more competitive pricing and deeper discounts.

👉 See the most recent new car inventory update

Several automakers are struggling with declining sales in the U.S. market, which will likely trigger bigger incentives for buyers during year-end promotions. For example, Stellantis reported a 20% drop in Q3 2024 U.S. sales, leaving a large inventory to clear by year’s end.

Nissan, with an oversupply of Rogues, Frontiers, and Pathfinders on dealer lots, is already ramping up its discounts. Even Ford has seen flat sales, suggesting that more aggressive offers will be needed to boost year-end purchases. Expect major automakers to offer compelling financing options, cash discounts, and attractive lease deals on their remaining 2024 models.

Each year, the holiday season kicks off some of the best car deals, as both manufacturers and dealers know that consumers are more inclined to make big purchases. December is traditionally a month of heavy promotions, and after years of holiday sales conditioning, buyers often wait for year-end sales. As dealerships try to hit their annual sales targets, holiday incentives mean larger savings for shoppers who know where the deals are.

While the biggest deals usually arrive in late December, 2024’s current zero-percent APR offers and low-payment lease deals make waiting unnecessary for some buyers. If you spot a deal now that fits your needs and budget, locking it in today could be a smart move. With interest rates stabilizing, locking in a great finance offer now might beat the crowds rushing for year-end car sales.

👉 We’re gathering ALL of the best year-end deals here

In summary, 2024’s year-end car deals are expected to be huge. Automakers are pushing to clear high inventory levels as 2025 models rush in, and dealerships are feeling pressure to meet their sales targets. The combination of falling interest rates, manufacturer incentives, holiday promotions, and excess stock makes this December a golden opportunity for car buyers. If you find the perfect deal now, don’t hesitate—but if you can wait, December’s deals could save you even more.

Ready to outsmart the dealerships? Learn more about CarEdge Pro, your ticket to behind-the-scenes car market data.

When consumers buy hybrid or electric cars, they typically do so with a greater purpose. Either they wish to help the planet by limiting the burning of fossil fuels and reducing emissions, or they want to save money at the pump. Many would consider themselves early adopters of new technologies, always eager to try the latest tech. But are hybrids and EVs better for your wallet? Considering resale value, are they a risky purchase? We will take a look at how hybrids and electric vehicles perform when it comes to the latest depreciation numbers.

CarEdge has calculated the annual depreciation of popular car models on sale in the United States. This free data available on the CarEdge Research Hub is extremely valuable for car shoppers. With these insights, it’s possible to determine which cars have historically been relatively good investments, and which ones have been underperformers.

Head to the free Research Hub for all of today’s car depreciation numbers.

Let’s start with the bad news for electric vehicle owners: some models are performing poorly in terms of value retention. Topping the list is the Tesla Model X, which retains just 43.15% of its value after five years, meaning it depreciates by 57%. The Tesla Model S follows closely with a 5-year residual value of 43.49%. Similarly, the Nissan LEAF depreciates by more than half, with a 5-year residual value of just 45.56%. These EVs, despite their fuel efficiency, lose significant value over time, outpacing any potential fuel savings.

On the other end of the spectrum, some hybrids and electrics hold their value exceptionally well. Leading the pack is the Toyota Prius, with a remarkable 5-year residual value of 68.92%, making it one of the best vehicles for resale, hybrid or otherwise. The 2025 Toyota Camry, now exclusively available as a hybrid, also shines with a 5-year residual value of 65.09%. Both models offer exceptional fuel efficiency and long-term financial value, making them solid investments for those who prioritize fuel savings and resale value.

No article about hybrids or electric cars would be complete without a commentary on Tesla. With such, we will tell you that the Tesla Model S – the only Tesla qualifying for 5-year results – ranks 75th overall among luxury cars. The Model S, which cost roughly $90,000 when purchased in 2019, is today worth 43% of it’s value as new, being worth about $40,000 in 2024. Losing $50,000 of value is never fun, but that was the cost of being an early-adopter five years ago. Our take is that Tesla deserves credit for producing a fully-electric car, and still having it be worth something meaningful with its technology 5 years old, and after you’ve put some significant miles on it.

Our take on whether hybrids and electric cars offer good resale value can be summed up with a classic “it depends.” Some models, like the Toyota Prius and Camry Hybrid, have proven to retain their value remarkably well, making them smart investments when paired with fuel savings. On the other hand, vehicles like the Nissan LEAF and Tesla Model X suffer significant depreciation over time, despite their tech-savvy appeal. The smart car shopper will always do their homework, assess depreciation trends, and choose wisely to maximize value retention over time.

Check our the complete rankings of the cars with the best and worst depreciation, updated for 2025.

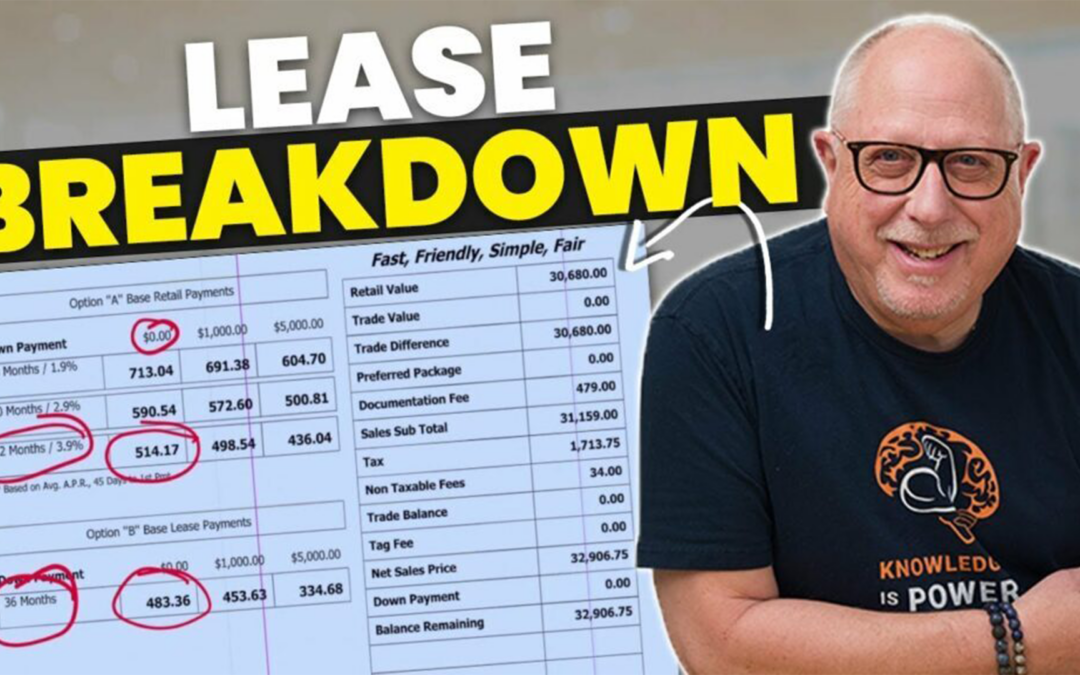

Whether you’re considering a lease for your next car or currently have a car on lease, you’re probably aware that a lease gives you no ownership. However, many dealerships processing end-of-lease returns neglect to mention an important detail. In some cases, when a lease is returned, the car has equity on it worth hundreds or even thousands. It’s called lease equity, and it’s money that should go in your pocket.

When you lease a car, you don’t get to drive it as much as you want. Rather, the lease is made out for a specific mileage level. Depending on the model and contract, you could be allowed anything from 30,000 miles to 60,000 miles in the three years that you keep the car. If you go over your mileage limit, you will be charged for overages when it’s time to return the car at the end of the 36-month lease period. This can be an expensive miscalculation on your part, so be careful to not exceed your mileage limit, unless you’re prepared to pay up at the end.

Should the opposite happen – if you manage to drive less than you’re allowed – you’ll have ended up paying more for the car than you’ve actually used. It’s this difference that makes up the equity that you have in your car. When the dealership sells the car on the used market, they are likely to get more than they originally hoped for, as they expected the car to have more mileage. They should give you a share of this windfall. Depending on the model and how many miles you’ve managed to save, you could have equity worth a substantial sum of money in the car.

Most dealerships don’t pay cash for the lease equity that your car brings them. Rather, they offer to give you credit that you can put towards your next lease, buying a new car, or even if you decide to buy the leased car outright. That’s always an option. Unfortunately, dealerships are often less than upfront about lease equity, and often fail to bring up the subject in the hope that their customers won’t know enough to ask.

See all of your lease-end options

Before you hand in the key at the end of your lease, it’s important that you look at the odometer and determine how many miles you’ve saved. If you’re under your lease mileage allowance, you should bring it up when it comes time to give back the car. Doing so could save you a lot of money in the form of a hefty discount on your next car.

![Every Honda Recall So Far In 2024 [U.S. Market]](https://caredge.com/wp-content/uploads/2024/09/Honda-CR-V.optimized-1080x675.webp)

Honda has issued several significant recalls over the course of 2024, involving components ranging from software to power steering. The most recent recall involves 1.7 million Honda and Acura models, the largest by far this year. To ensure that Honda and Acura drivers are staying safe, we’re providing this brief overview of every Honda recall so far in 2024. Click on the links for more information on specific Honda recalls.

October 9 Recall: 9 2022-2025 Honda models + Acura Integra

August 16 Recall: 2024 Acura ZDX

July 23 Recall: 2024 Honda Prologue

July 9 Recall: 2024 Honda CR-V

June 5 Recall: Honda Fit and HR-V

May 14 Recall: 2020-2024 Honda Ridgeline

March 14 Recall: 2023 Honda Passport and Ridgeline

February 23 Recall: Honda Odyssey and Acura RDX

February 6 Recall: 2020-2022 Honda and Acura Models

To see if your car is affected by any outstanding Honda recalls, check your VIN for potential recalls using Honda’s free recall checker tool. If an issue is flagged, be sure to schedule an appointment with a Honda service center as soon as possible. Remember, you don’t have to pay for recall fixes!

You should never buy a car without first taking it for a test drive. If you are new to the car buying game, you may not know what to watch out for during a test drive. Here are four things to pay attention to when you test drive any vehicle.

A modern car is loaded with screens, knobs, and buttons. You may not need them most of the time, but you should be confident that they will work if and when you do need them. Before you begin your test drive, try out all of the various tools and accessories in the vehicle, such as windshield wipers, seat adjustments, mirror adjustments, window controls, radio controls, and even the sound system.

If the car salesman tries to rush you, kindly let them know that you will need some time to review everything, and that when you are done, you will seek them out for your test drive. If everything works well, it’s a good sign; if not, you’ve got a list of things to review with them. Remember, you are likely buying the car as-is, so discovering that the defroster motor doesn’t work, after the fact, may cost you.

When you are out on a test drive, the sales associate who rides along may try to persuade you to do a quick drive around the block before heading back to the lot. However, this route most likely won’t allow you to gain a complete understanding of the car’s performance. The best way to do so is to test drive it on an unplanned route that includes both highway and city driving. This will allow you to get a better understanding of how the vehicle accelerates, how the brakes perform, and the ease with which it turns in tight corners. Drive the car the way you would drive it everyday.

Smartphone connectivity has become one of the top features that potential car buyers look for. Not all cars have Apple CarPlay or Android Auto. The ease with which you can connect your phone to the vehicle can vary quite a bit from one car to the next. Depending on the car you are in, you may be able to connect your smartphone with a simple touch, or you may have to navigate through menus to accomplish the task. Test the smartphone connectivity as a part of the test drive. There’s nothing more frustrating than not being able to listen to your music when you get a new car.

One important note: don’t forget to unpair your phone when you’re done!

If you are upgrading your car, you may encounter a host of new tech features that weren’t there in your previous vehicle. These may include adaptive cruise control, lane-keep assist, automatic emergency braking, and even more advanced tech like Autopilot. Take the time to understand them and test them out before you make your purchasing decision.

Test driving a car is one of the most important steps in the car-buying process. By taking the time to test all the features, choosing a diverse driving route, connecting your smartphone, and understanding the new technology, you can make a more informed decision and avoid surprises later on. Remember, you’re not just test driving for a quick feel; you’re assessing how well the car fits your daily needs. The more thorough you are, the better chance you have of finding the right vehicle for you.

The term “upside down” doesn’t sound like much fun. Generally speaking, you want to be “right side up”, and that is definitely the case when it comes to an auto loan. Within the auto industry, being upside down in a car loan simply means that the balance on your loan is greater than the value of your car. Below are some helpful tips on how to make certain that you don’t find yourself in this position on your car loan.

If you’re thinking of buying a new car, you have to realize that it will lose value as soon as you drive it off the dealer’s lot. Once you hit the street, that car or truck technically becomes used, and it’s no longer priced like something that is brand-new. The speed at which vehicles lose value is greatest in the first year of ownership, where the average new car loses 23% of its value in just the first 12 months. If you want to avoid being upside-down on a car loan, a new car may not be the best choice for you.

Buying new is nice, but financially, it can set you back. On the other hand you can buy an old clunker, but risk throwing money at repairs. So, where is the sweet spot? Our recommendation is that you should buy a vehicle that is between 2 and 4 years old, is still under its factory warranty, has plenty of useful life left in it, and still looks and drives like new. An average car or truck will decline 38% in value in the first three years, so buying one in this range offers savings of 30-40% off its price compared to new. In other words, someone else’s loss can be your savings.

It also helps to buy a car (whether new or used) that has a good resale value. Research depreciation, maintenance costs, and more with the free CarEdge Research Hub.

In years past, a 5-year loan was the longest loan term offered by lenders. Today, car buyers are lured into the prospect of lower monthly payment; not by getting a better price, but by just stretching out the time period to pay off the vehicle. Loans of 6, 7, and even 8 years, are now common in vehicle financing. This is a dangerous path that car buyers should try to avoid. Learn more about the serious risks of 84-month car loans.

As most are aware, lower credit scores translate into higher loan interest rates, and as a result, higher monthly car payments. As a car shopper, you’ll want to check your credit report ahead of time. Make sure that the report is accurate, and doesn’t have any errors. Importantly, the lower your interest rate, the quicker your loan balance will fall, and the less likely that you’ll be upside down.

If you have the financial flexibility, one of the best ways to ensure that you’re not upside down in a car loan is to make a big down payment when you buy. Another option is to make a larger down payment when you refinance your auto loan.

The more money you put down, the lower your loan balance, and the greater the chance that you won’t have an upside-down car loan. Better yet, your monthly payments will be lower with a larger down payment. Those who put down little or no money for a down payment increase their chances that they will be upside down in their loan for years to come.

Staying financially “right side up” with your car loan comes down to smart choices: avoid long loan terms, consider buying a used vehicle with solid resale value, and put down as much as possible upfront. By being aware of depreciation, improving your credit score, and securing a favorable loan, you can reduce the risk of an upside-down car loan. With the right approach, you can drive away with a deal that works in your favor.

When buying a car, most people focus on the sticker price, but the total cost of owning a car goes far beyond that initial figure. While the purchase price is a major consideration, ongoing costs like insurance, maintenance, depreciation, and financing can add up quickly. Understanding these hidden expenses is crucial for making a smart financial decision. Whether you’re buying new or used, being aware of the true cost of owning a vehicle can save you from unexpected financial strain down the road.

Depreciation represents the value loss of a vehicle from the moment it’s purchased. A car’s value often drops as soon as it’s driven off the lot, and this affects both new and used vehicles. While you don’t pay depreciation directly, it’s important to account for it if you plan to sell your vehicle in the future.

Luckily, calculating depreciation is straightforward. At the CarEdge Research Hub, we provide updated depreciation data to give you a clear picture of your car’s value over time. Check out depreciation rates for your car to make more informed decisions.

In rare cases, vehicles may increase in value due to high demand, such as collector cars. But for the majority of cars, depreciation is inevitable.

When you purchase a vehicle, you will be required to purchase insurance. If you are financing a vehicle, it will be mandatory that you get full coverage insurance. If you purchase a car and pay it in full, you can choose to get liability insurance. Full coverage is going to cost more due to the comprehensive coverage that you get compared to liability insurance. Insurance policies can cost anywhere from $50 up to $300+ per month depending on the vehicle, the type of coverage you get, and your recent driving history.

For those with speeding tickets or accidents on their record, insurance costs may be higher. Always get insurance quotes before purchasing a vehicle to ensure you can afford both the car payment and the insurance premium.

Maintenance and repairs are inevitable parts of car ownership, and these costs can vary depending on the make, model, and age of your vehicle. Regular maintenance like oil changes, tire rotations, and brake checks are essential for keeping your car in top condition and can help you avoid costly repairs down the road.

To reduce long-term costs, follow your vehicle’s maintenance schedule and consider setting aside an emergency fund for unexpected repairs, such as transmission or suspension work. Some repairs are unavoidable, but taking proactive steps can minimize expensive breakdowns.

See average maintenance costs for your car at the CarEdge Research Hub

When financing a car, interest can significantly increase the total cost of ownership. The longer the loan term and the higher the interest rate, the more you’ll end up paying. Let’s break it down with an example:

Imagine you finance a car for $30,000 with a 5% annual percentage rate (APR) over 60 months. Over the course of the loan, you would pay about $3,968 in interest, bringing the total cost of the car to $33,968. If you extend the loan term to 72 months, you’ll pay an additional $1,043 in interest.

To minimize the cost of interest, consider opting for a shorter loan term and shop around for the lowest APR. If possible, improve your credit score to qualify for better rates. Additionally, making a larger down payment can reduce the total loan amount, helping you save on interest over time.

Compare refinancing rates all in one spot

There are a few other expenses that you should take into consideration when it comes to owning a car. State registration fees are a great example of a yearly fee you can count on paying each year you register your vehicle. This will vary state by state, so check with your local DMV to see what your current state registration fees are. Many states levy ‘property taxes’ on vehicles based on the value of the car. These vehicle property taxes can add up to a few thousand dollars per year for luxury vehicles and expensive trucks.

Tires are another maintenance item that can add up over the years. These days, a set of four quality tires can cost $1,000 with installation and disposal fees. Tires increase in cost with larger and more uncommon sizes.

In conclusion, the total cost of owning a car goes far beyond the initial purchase price. Key factors like depreciation, insurance, maintenance, and financing charges can significantly impact your overall expenses. Some cars depreciate faster, others come with higher maintenance costs, and interest rates on car loans can add up over time. Be sure to evaluate all these variables when determining whether a vehicle is the right financial decision for you. By understanding the true cost of ownership, you can make smarter, more informed choices.

It’s time to say goodbye to your old reliable car, but should you sell it privately or trade it in? Both options have their pros and cons, but with the right approach, you can minimize financial losses. Here are 10 tips to help you make the best decision.

If a salesperson asks how much you want for your car, don’t give them a number. Let them make the first offer to avoid limiting your potential trade-in value. If asked, let them know that your primary interest is minimizing your net cost, or trade difference, after an allowance for your trade. Avoid providing any firm numbers, despite their repeated attempts to enquire, as they will be resolute in getting you to throw out the first number.

Trading in your vehicle at the dealership can save you on sales tax. When you trade-in, you subtract the value of your car from the sales price of the new one, and you only pay sales tax on the difference in value. For example, if your trade-in is worth $20,000 and your state has a 5% tax, you could save $1,000 compared to selling it privately.

If you’re just browsing, don’t clean out your car beforehand. A spotless trunk signals you’re ready to buy, potentially weakening your negotiation position.

Dealerships may offer more for your trade-in but mark up the price of the new car. Don’t be fooled by the dealer that simply offers you the highest price for your car, as they may be getting you on the other side. Always look at the total cost.

If selling privately, get the obvious repairs fixed up front, and perform the routine service, like an oil and filter change. If your vehicle needs obvious repairs, private buyers will discount its value by at least 2X of the cost of the repair, as they will be concerned that it can’t be fixed, or that repairs will end up being more costly. Buyers don’t want to inherit a problem; they want a car that they can drive home with confidence, and is trouble-free.

Run a vehicle history report before selling. Surprises on a report could deter buyers or lower your asking price. If you’re the original owner and have never had any problems or accidents, it’s possible to skip this step.

Present your service records and manuals in an organized manner to instill buyer confidence. If you have them, make sure to include the vehicle registration, window sticker and any operating manuals that you received, so that you can present them to any possible buyer.

If your trade-in doesn’t match the dealership’s typical inventory, expect a lower offer. If you are at the BMW dealership, and you’re looking to trade in your 10 year-old Corolla with 120,000 miles, don’t expect a good offer. They won’t want your car, and will sell it straight to a wholesaler. Keep this in mind when thinking about a trade-in.

For safety, meet prospective buyers in public spaces like designated safe meeting zones rather than your home.

If possible, pay off any loans before selling. Having a clean title in hand, goes a long way towards resulting in a seamless transaction, versus having to get a bank involved. Sometimes banks will take weeks to send you a title that is free of liens, and that is enough to sour a lot of car deals. Similarly, make sure that you ask the private buyer how they intend to pay for the car.

Selling or trading your car doesn’t have to be stressful. By fixing minor issues, getting paperwork in order, and strategically timing your sale, you’ll increase your chances of getting a good offer. The more certainty you provide the buyer, the more they’ll be willing to pay. Learn more about resale values with CarEdge Research.

Car buying can be overwhelming, but Deal School is here to help. CarEdge, led by father-son duo Ray and Zach Shefska, has updated the internet’s #1 free car buying course for 2024 and beyond. Designed to empower consumers, Deal School teaches buyers how to navigate the car buying process with confidence, saving money in the process.

👉 Enroll in Deal School for free

Deal School consists of four comprehensive units made up of 22 individual lessons, each designed to prepare you for every step of your car buying journey. Here’s a breakdown of what you’ll learn:

Each unit concludes with a quiz to test your knowledge and ensure you’re ready for real-life negotiations. With CarEdge’s Deal School, the car buying process is not only simplified, but consumers also gain the confidence to negotiate smarter deals, keeping more money in their pockets.

In addition to refreshed lessons with updated information and brand-new recorded lessons with Ray Shefska, Deal School 2024 introduces a free e-book filled with proven strategies to help you get the best deal on your next ride. This e-book is packed with insider knowledge, giving you a major advantage before stepping foot in a dealership. Print it off, take it with you, and shop for your next car with confidence.

CarEdge’s Deal School is the go-to resource for anyone looking to buy a car with confidence. You’ll learn everything from car-buying secrets to mastering the art of negotiation and understanding financing. Once you complete the course, you’ll be ready to secure the best deal on your next vehicle purchase.

👉 Sign up for Deal School today and start saving – It’s FREE!