CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

It is officially safe to declare; used car prices are finally going down. Finally, we’re seeing a clear trend emerge in used car prices. Now is the time to sell a car (as we’ve seen five weeks in a row of used car price declines and trade-in values will likely drop over the coming weeks), and patience is still required if you’re looking to buy a used car (wait a few more weeks, we expect prices to decline even more).

Thanks to data from Black Book, Cox Automotive, financial institutions, and the experiences of our community, we now have enough data to feel confident in saying that used car prices are going down, and that they will continue to fall. For car buyers, patience is more important than ever. If you’re in the market to buy a car, wait a few more weeks for a better deal.

Let’s dig into what’s happening in the market, and how you can time your sale or purchase.

In 2021 we witnessed the unthinkable; used car values appreciated more than 40%. During the first quarter of 2022, we saw used car prices drop nearly 5% on the wholesale markets. By the time spring rolled around, we experienced another increase in wholesale used car prices, canceling out those previous declines.

While the wholesale market rose and fell, retail used car prices have remained high during the first half of 2022. Consequently, the average monthly car payment is over $700.

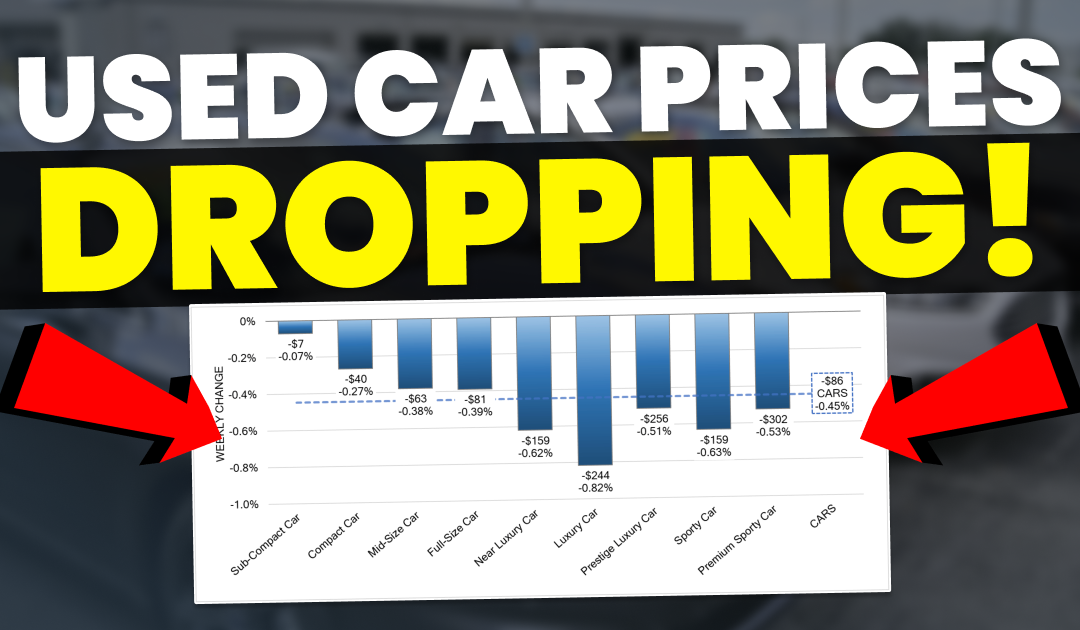

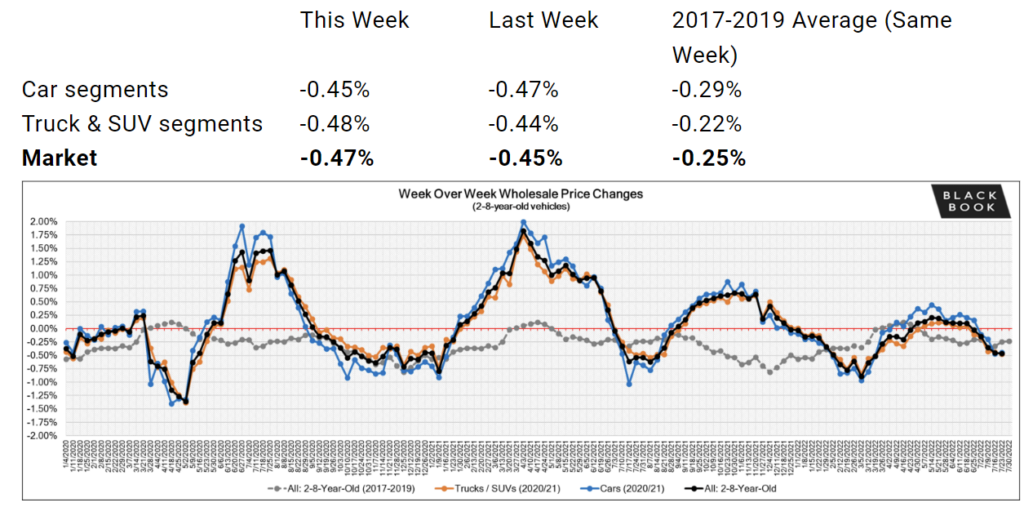

As we settle into summer, we’ve now seen five consecutive weeks of overall market softening. For the first time since the pandemic lows of 2020, used car prices are going down across all market segments.

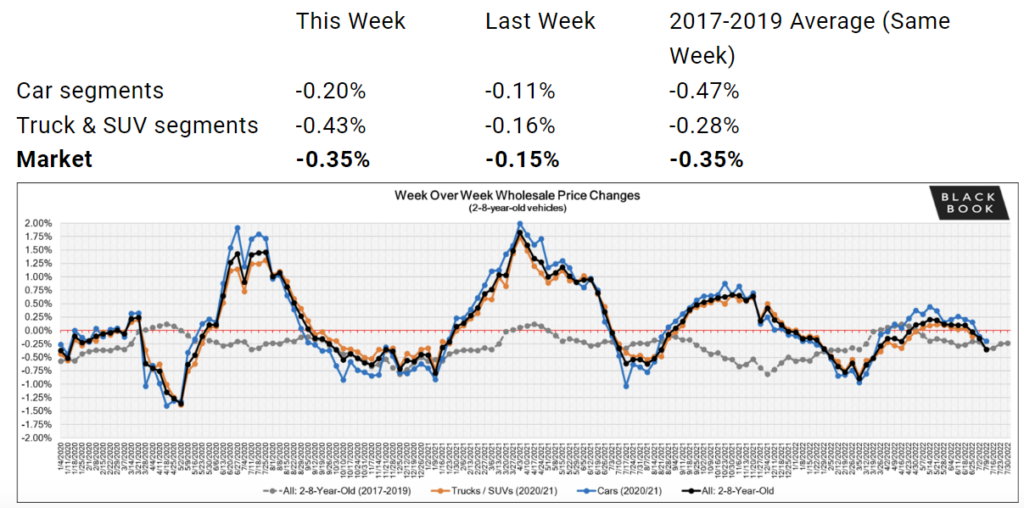

We track weekly wholesale used vehicle prices to provide you with granular market insights that will empower you to make an informed decision if you’re in the market to buy or sell. The past several weeks have brought a much-needed reprieve from month after month of record high used car prices. Notably, wholesale price declines are accelerating. Just last week, used car prices declined by -0.47%. Half of one percent may not cause alarm to some, but remember that this is across just seven days.

When we look at cumulative used car price decreases, the picture becomes more clear. These are the overall used car market price trends from the past five weeks of Black Book’s Market Pro:

-0.02% the week of June 28

-0.15% the week of July 5

-0.35% the week of July 12

-0.45% the week of July 19

-0.47% the week of July 26

That folks, is a trend. Since late June, wholesale used car prices have declined by 1.42% from all-time highs. Now that the trend is clear, our attention turns to how wholesale price declines will translate into lower used car prices for the consumer.

As we’ve heard from members of our community, used car deals can be had. Negotiating on used cars is more feasible now than before because dealers no longer have the option to simply sell a car at the auction for a profit. With wholesale prices dropping and interest rates rising, dealers are once again negotiating on used car prices.

Consumers can leverage this information (plus the likely increase in used car supply thanks to repossessions, and rising interest rates increasing dealer costs) to negotiate a more fair used car deal. Deal School 2.0 is a great free resource if you’re thinking about buying a used car anytime soon and want to save time and money.

Sadly, we don’t expect retail used car prices to plummet tomorrow. There remains a severe shortage of new cars as automakers continue to grapple with the semiconductor chip shortage, the lingering effects of international COVID shutdowns, and now the war in Ukraine. Still, there’s some good news if you’re looking to buy, and a new sense of urgency if you’re considering selling.

Used car prices are going down on wholesale markets, and now we’re anticipating a decline at the retail level. However, patience will be key. Buyers who are able to wait 60 to 90 days are very likely to save money versus buying today. It would not be out of the question to see used car prices decline 5% to 10% in just a few month’s time. This is because retail prices lag wholesale prices, plus there are a few other factors (covered below) that are impacting our forecast.

The past 18 months have been the exception to the rule. Normally, vehicles are depreciating assets. They lose value over time, and that keeps used car prices more affordable. We think days are numbered for ‘car flippers’ who buy and sell for a profit weeks or months later. Used car prices are on an accelerating downward trend, and this means that your car is likely to be worth less one month into the future.

Trade-in values are going to decline, too. Dealers have been shelling out surplus cash for trade-ins over the past year. More often than not, when you trade in a vehicle, the dealer will sell it at auction. We’re seeing wholesale auction prices decline in real time, therefore dealers will be trying to stay ahead of the downward trend by offering sellers less for their trade-in.

If you’re considering selling a vehicle, our advice would be to sell it as soon as possible. Those who wait are very likely to sell for substantially less given the current market trends.

America’s $1.3 TRILLION in auto loan debt is on the minds of financial institutions. They are aware that they just spent the past year and a half financing vehicles at greatly inflated prices, and that the bottom may fall out at any time. If this indeed is the bubble bursting, the looming threat of auto repossessions will make banks and credit unions very nervous.

If a consumer stops making payments and the repo man pays a visit, the bank will be left with an asset that is depreciating rapidly. Auto loan defaults are increasing, but remain below pre-pandemic levels. As of Q1 2022, about 4% of auto loans were 90 days past due. However, subprime borrowers are more likely to default according to the latest data. In March, 8.5% of subprime borrowers defaulted on their car loans, according to Equifax. We have heard from our community members that upcoming Q2 data from financial institutions will show 10%+ delinquency rates for subprime borrowers. We’re watching this closely.

As more repo vehicles make it to the retail market we expect used car prices to continue to soften.

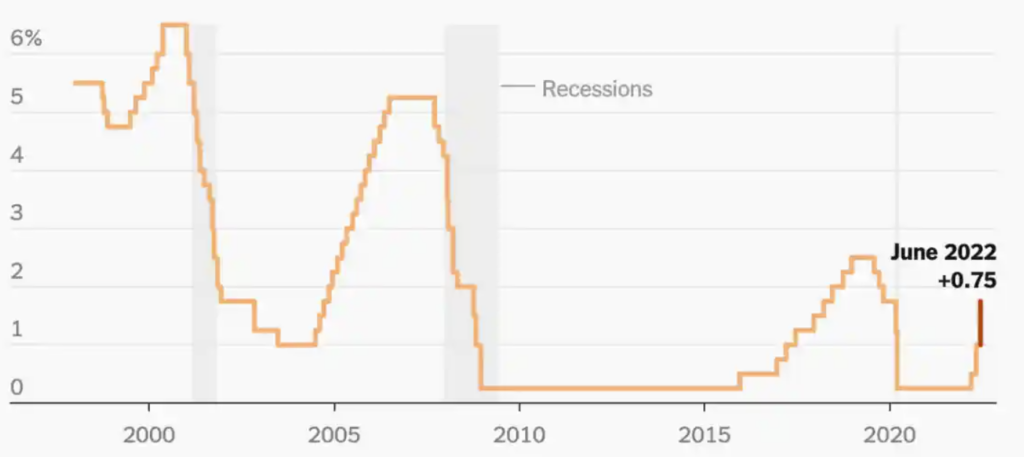

The Federal Reserve has publicly stated that it intends to continue hiking interest rates until inflation is under control. The cost of borrowing money will increase in 2022, and possibly into 2023. Car buyers in the market for higher priced vehicles will feel the effects of higher interest rates most. A 6% interest rate will result in about $6,000 in total interest paid for a $40,000 loan over 60 months, but just $2,400 for a $15,000 loan over the same term.

Just as consumers are feeling the effects of higher interest rates, dealers are too. The cost to finance dealership inventory (you read that correctly, car dealers don’t pay cash for their cars, they finance them just like you and me) is also going up.

When floorplan expenses go up, dealers are more incentivized to sell cars that have been sitting on their lot longer. This is why when you search for cars on CarEdge’s car search we show you the days on the lot. The longer a car has been sitting, the more it is costing that dealership in interest payments. As interest rates rise, dealers will be motivated to sell used cars that are sitting on their lot.

Now is the time to sell a car, and better deals are just around the corner for buyers. At the wholesale level, used car prices have dropped by 1.42% month-over-month, and price declines are accelerating. Across all segments, prices paid for used cars were down roughly half a percent in just seven days last week. We now have the confidence (backed by five weeks of data) to call this a downward trend. Sellers are more likely to get more money for their car if they sell sooner rather than later.

We haven’t seen the effects of declining wholesale prices on retail car prices yet, but we will soon. Retail prices won’t fall off an immediate cliff, but declines will be gradual. For those who can wait two to three months, used car prices are very likely going down, and better deals will finally make it to the sales floor.

What have you seen in your area? Share a comment with us below!

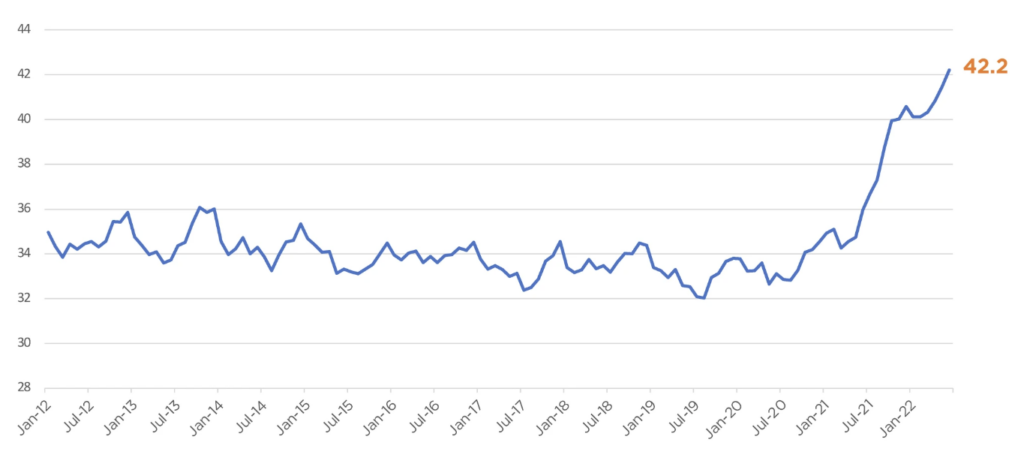

Is all the talk of inflation giving car dealers and automakers an excuse to raise car prices even further? While that would be pure speculation, we do know that a new vehicle now costs more than ever before. New data from Cox Automotive/Moody’s Analytics reveals that just a few weeks after a previous record high was reached, new car prices have forced monthly auto payments to new heights. How high will new car prices climb? Is this simply a new normal that we have to accept? Here’s what the data tell us.

The new report from Cox Automotive and Moody’s Analytics is disheartening to say the least. Today’s out-of-control car prices can be summarized by one statistic: In June, the estimated number of weeks of median income needed to purchase the average new vehicle was up 17% from last year. Median incomes have risen slightly, but rising new car prices have far outpaced income.

The Cox Automotive/Moody’s Analytics Vehicle Affordability Index is driven by the consumer’s vehicle transaction prices, the income of the consumer, amount financed by the consumer, and the interest rate provided by the lender. The result is a value that represents the number of weeks of the median household income in America that would be needed to buy the average new vehicle.

The number of median weeks of income needed to purchase the average new vehicle in June increased to 42.2 weeks from 41.5 weeks in May. This is an all-time high that reflects the predicament that consumers needing a car find themselves in. From May to June 2022, median income grew 0.3% at the same time that new car transaction prices increased 1.6%.

The estimated average monthly payment increased 2.2% to $730, which is a new record high. A new car monthly payment now costs as much as rent in many parts of the country. We’re seeing more and more car payments over $1,000 a month.

Gone are the days of zero percent financing. As the Federal Reserve continues to raise interest rates to combat inflation, borrowing money becomes more expensive for everyone from the banks to the consumer. From May to June of 2022, the average auto interest rate increased another 8 basis points.

Higher interest rates affect luxury car buyers and those who put little money down the most. A 6% interest rate will result in about $6,000 in total interest paid for a $40,000 loan over 60 months, but just $2,400 for a $15,000 loan over the same term. Interest rates are a big part of car buying, and they remain dynamic as our economy traverses ups and downs.

Why would automakers offer new car incentives when demand far exceeds supply? To be nice to the consumer? We could only hope for such benevolence from OEMs, but we know that’s not how big business works.

New car incentives are down 59% in just 12 months as supply chain problems squeeze new vehicle inventory to record lows that have struggled to climb back. In the second quarter of 2022, incentives averaged $1,228 industry-wide. That’s a 59% drop year-over-year.

| Q2 2022* | Q1 2022 | QoQ change | Q2 2021 | YoY change | |

|---|---|---|---|---|---|

| BMW | $1,206 | $2,358 | -49% | $4,713 | -74% |

| Daimler | $1,257 | $2,012 | -38% | $3,574 | -65% |

| Ford | $1,193 | $1,824 | -35% | $2,567 | -54% |

| General Motors | $1,847 | $1,974 | -6.40% | $4,399 | -58% |

| Honda | $818 | $1,163 | -30% | $2,167 | -62% |

| Hyundai | $620 | $890 | -30% | $2,102 | -71% |

| Kia | $650 | $1,260 | -48% | $2,549 | -75% |

| Nissan | $1,501 | $1,848 | -19% | $3,502 | -57% |

| Stellantis | $1,893 | $2,413 | -22% | $3,522 | -46% |

| Subaru | $753 | $901 | -17% | $1,339 | -44% |

| Toyota | $803 | $1,025 | -22% | $2,219 | -64% |

| Volkswagen Group | $1,169 | $1,769 | -34% | $3,730 | -69% |

| Industry | $1,228 | $1,631 | -25% | $3,003 | -59% |

Until more cars are sitting on dealer lots, there simply won’t be any reason for manufacturers to offer more new car incentives to buyers. Here’s more of our coverage on manufacturer incentives.

In January of 2020, the industry’s average was 82 days’ supply. By early 2021, that figure had fallen to 66, but it would soon plummet as the chip shortage lasted longer than most expected. In July of 2022, new car inventory is slim with just 21 days’ supply.

Subaru, Mazda, Volvo, Kia and Hyundai have had the lowest new car inventory, and therefore have had the least incentives for buyers. See the latest new car inventory numbers.

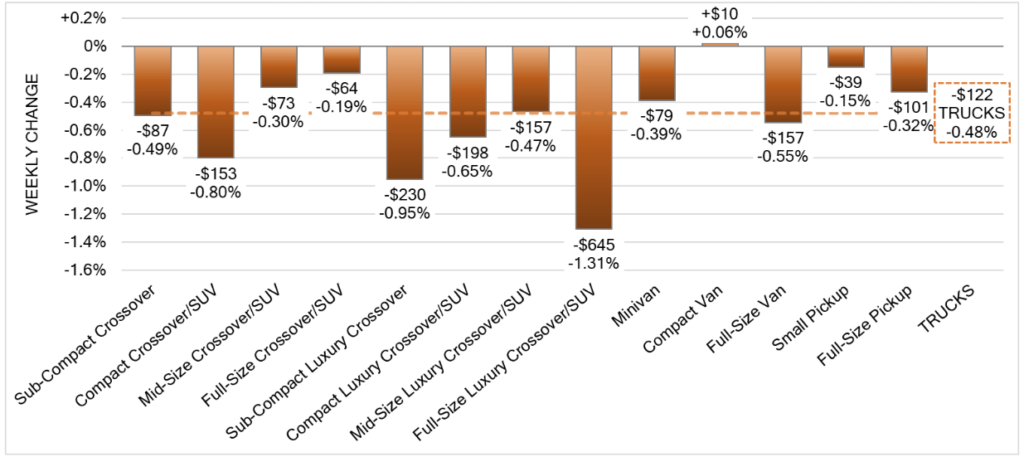

For three consecutive weeks, used car prices have declined at wholesale auctions. This leading indicator suggests that relief may be on the way for consumers in desperate need of a more affordable option. In fact, only full-size vans appreciated last week. All other vehicle segments have seen prices decline at the used wholesale level.

Will used car prices continue to decline? It all depends on new car inventory. When there are more cars on dealer lots, used cars will lose value, and may ultimately come back down to Earth from record highs. This is something to bear in mind if you’re thinking about buying a used car at today’s inflated prices.

CarEdge tracks used car prices with weekly updates. See used car price updates here.

The U.S. Federal Trade Commission is proposing new regulations that would ban anti-consumer sales tactics notoriously common in the auto industry. These shady practices include..

Car dealer lobbyists are NOT HAPPY about this set of proposed regulations! We the consumers have until September 12, 2022 to leave a comment in support of these common sense regulations. Find out how YOU can make your voice heard here. We must fight back against powerful dealers!

In June, the Federal Trade Commission proposed a new set of rules that would ban unscrupulous sales practices that are commonly employed at car dealerships. Among the notoriously anti-consumer practices targeted are the sale of products without benefit, bait-and-switch pricing, forced add-ons, and discriminatory practices for cash buyers.

There’s a reason the annual trustworthiness of profession poll from Gallup ranks car salespeople at the bottom; it’s not because every salesperson is bad, it’s because a few bad apples ruin the bunch. Over the years I have heard countless stories from our community of these aforementioned practices. Still, powerful dealer lobbies are combating the FTC proposal, and it’s become clear that they’re determined to defeat the proposal at all costs.

Fortunately, consumers have a real opportunity to have their voices heard. A public comment period is now open until September 2022, and we’re calling on you to share your opinion with the FTC. It’s clear that auto dealers are already amassing a unified position, and we need to do the same. If consumers show up in numbers, car buying may be transformed for the benefit of we, the people. Time is of the essence, as this narrow window leaves less than two months for the public to share their support.

On June 27th, The Federal Trade Commission proposed a new set of rules that would ban specific auto sales tactics commonly used by car dealers to take advantage of consumers. In an FTC proposal titled Motor Vehicle Dealers Trade Regulation Rule No. P204800, the following auto dealer practices are targeted:

FTC Bureau of Consumer protection Director Samuel Levine explained the reasoning behind the proposed rules. “As auto prices surge, the commission is taking comprehensive action to prohibit junk fees, bait-and-switch advertising and other practices that hit consumers’ pocketbooks. Our proposed rule would save consumers time and money and help ensure a level playing field for honest dealers.”

The average new car transaction is now $47,202, or 72% of the median household income in the United States. Bait-and-switch pricing, forced add-ons and dishonest financing tactics have all contributed to the average monthly car payment soaring to $730, 40% higher than the average payment just five years prior. With car prices at record highs, consumers are fed up with anti-consumer sales tactics that proliferate at many dealerships nationwide.

This is our chance as consumers to unite behind a proposed rule that could change car buying for the better unlike ever before. However, this battle is far from won.

The National Automobile Dealers Association, or NADA, is a nationally-recognized industry and political force that represents over 16,000 auto dealers nationwide. Every year, the NADA and its counterpart for independent dealers spend millions of dollars lobbying politicians to advance legislation that is pro-dealer, too often at the expense of the consumers the auto industry relies on. The power and influence of today’s car dealers can be traced directly to the NADA and NIADA.

Needless to say, the dealer lobby isn’t happy about the FTC’s proposed rules. In a letter to the FTC, the NADA characterized the proposal as unsupported, sloppy and inconsistent. How so? NADA senior vice president Paul Metrey dismissed the proposal as “woefully inadequate” because the regulation is unnecessary in his view, because it would address “things they can go after” already. It’s as if dealers and their powerful lobbies are fully aware of the anti-consumer sales tactics flourishing in the industry, but are content with pushing the limits of regulation until enforcement encroaches on their bottom lines.

Read the full NADA response here.

Another flawed argument promoted by the NADA is that complaints are few and far between. The FTC said it received more than 100,000 auto-related complaints in 2021. To counter that startling statistic, the NADA says there were 42 million new- and used-car sales last year. We all know that car buyers rarely have the time to seek out the procedures to submit a formal FTC complaint. Consumers have jobs, families, and other financial obligations on their minds. Imagine if one out of twenty dishonest car sales resulted in a formal complaint. In reality, reporting is likely even lower.

There’s no way of knowing just how widespread this problem is, yet every day our community of CarEdge members shares tales of shady dealership practices, and dishonest, anti-consumer tactics that cost them time and money. Whether it be comments on YouTube, or essays we receive via email; our millions of monthly viewers are fed up with the status quo, and demand change.

Industry media outlets are picking sides, and some heavyweights are clearly siding with dealer lobbies. Industry news outlet Automotive News published an editorial promoting the talking points disseminated by the NADA and NIADA. They too are calling for interested parties to submit comments during the narrow public comment period.

The FTC’s open commenting period is now open, and it will remain open until September 12, 2022. Anyone can submit a comment to voice support or displeasure with the proposal. In a classic David versus Goliath scenario, dealer lobbyists are facing off against consumers like you and I. With massive auto dealer lobbies and even media outlets calling for dealers to submit comments opposing the proposed rules, it’s up to all of us to make our voices heard. Submit a comment today on Regulations.gov. This should be a priority for all Americans who are sick and tired of car buying being synonymous with deception and dishonesty. We’ll keep you posted on the latest developments.

View Ray’s comment here, or read it below:

As someone who spent 43 years managing automobile dealerships and advocating for better enforcement of rules and regulations regarding dealer advertising and F&I practices, I strongly support your efforts to finally rid America of the unethical practices that many dealerships employ. Business decisions are made by dealerships everyday as to how to advertise the price of a vehicle online. Should we include the destination charge that is part of the MSRP in the price or should we disclose that in the small print? Should we disclose any dealer installed accessories or packages that the customer is expected to pay for in the advertised price or should we only disclose that once they have come into the dealership? Should we disclose all dealer and state fees or again wait until the customer has agreed to buy the car? How should we disclose our F&I offerings, or our rate markups for placing indirect loans? These are all business decisions that truthfully should not have to be made, full disclosure and transparency is not only what consumers want, it is what they are entitled to. You can read many consumer complaints in regards to this issue on our YouTube channel: https://www.youtube.com/c/CarEdge/ videos, just click on just about any video and read what consumers are saying on a daily basis.

One must question what is wrong with a society as a whole when everyone knows that consumers are taken advantage of everyday when purchasing a car or truck and everyone turns a blind eye to it. Law enforcement, consumer protection agencies, State Attorney Generals, the Federal Trade Commission and many other “consumer” protection organizations all know what is going on yet do next to nothing to correct it. The essence of commerce should not be “who can we take advantage of today” but rather how can we operate in a consumer respectful and honest manner. I believe the enactment of these proposals would bring us closer to the later and finally rid our society of the former.

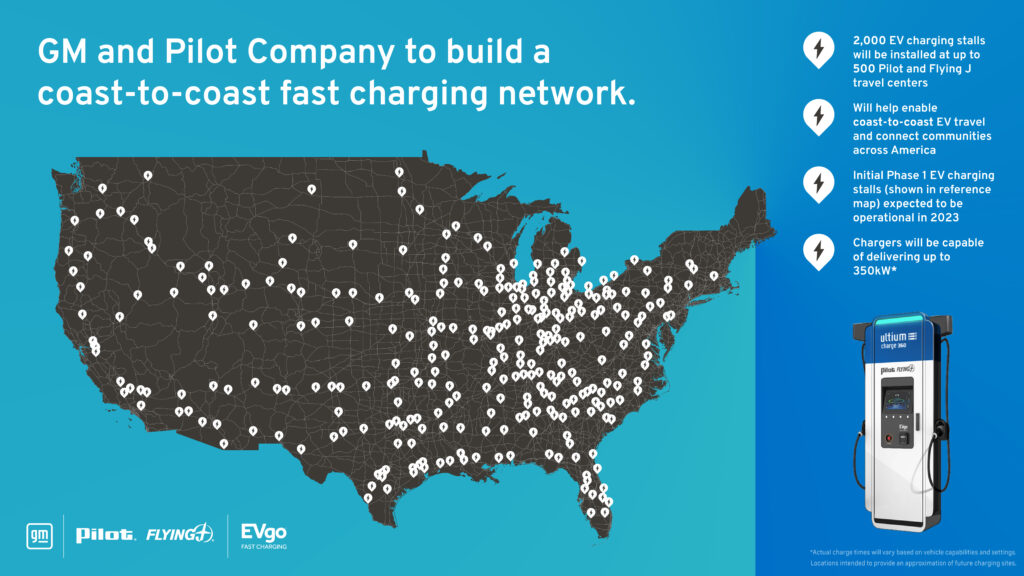

For years, electric vehicle enthusiasts and skeptics alike have said that if electric vehicles were ever to go mainstream, chargers were needed in two places: highway rest areas and truck stops. With today’s announcement from General Motors and the ongoing planning of the national charging network, EV chargers just might end up at both of these high-traffic locations. GM has announced a new partnership with EVgo, America’s third-largest charging network, and Pilot Company to bring EV fast chargers to 500 truck stop locations nationwide.

GM is on the verge of a massive push to EVs, and is counting on its new Ultium battery platform to overcome past issues with America’s most affordable electric car, the Chevrolet Bolt. As long as Tesla’s massive Supercharger network remains exclusively for Tesla owners, GM and other automakers will be faced with the challenge of how to provide adequate fast charging infrastructure for their EV customers.

In a press release, GM said that the new EVgo stations will be accessible to all EV brands. EVgo will install, operate and maintain the new charging stations, and Pilot Company’s Pilot and Flying J travel centers (more commonly known as truck stops) will provide amenities like restrooms and food options.

The latest announcement is separate from the existing collaboration GM has with EVgo to install more than 3,250 fast chargers in American cities and suburbs by the end of 2025. The first charging stations resulting from this new partnership will go live next year.

What exactly is GM’s role in this collaborative effort? From what’s been revealed so far, it appears it’s in the marketing and financing of these charging stations. The EVgo-installed and maintained stations will be co-branded “Pilot Flying J” and “Ultium Charge 360”, according to GM.

With Chevy Bolt sales skyrocketing and the Silverado electric truck almost here, GM’s electric vehicle customers are looking for signs of better charging experiences, and according to the announcement, it sounds like this will go a long way toward a more seamless experience.

“GM customers will receive special benefits like exclusive reservations, discounts on charging, a streamlined charging process through Plug and Charge and integration into GM’s vehicle brand apps providing real-time charger availability and help with route planning.”

Speaking of the Silverado EV and Ultium platform, many of the new EVgo stations will be able to charge at 350 kilowatts, making ultra-fast charging sessions possible in more areas.

One thing that stood out to me was GM’s mention of canopy covers for some of the EVgo charging stations. Plugging in during a thunderstorm fully-exposed to the elements doesn’t make for a fun EV experience, so I welcome this addition to charging stations.

Phase 1 installations (pictured in the map) are supposed to begin operation by the end of 2023. As far as charging infrastructure goes, that’s a quick rollout. Subsequent phases will bring chargers to more locations not announced yet.

Electrify America is currently the charging network of choice for most brands besides Tesla, with over 800 locations in the U.S. Electric vehicle drivers (myself included) are too-often inconvenienced by malfunctioning charging stalls and lines to charge on holiday weekends. With a government-funded national charging network nearing the start of construction, EV drivers are hoping for more reliability, easier access, and less charger downtime. GM’s partnership with EVgo and Pilot could be the pillar that finally brings stability to the EV charging experience. We look forward to this collaboration getting off the ground.

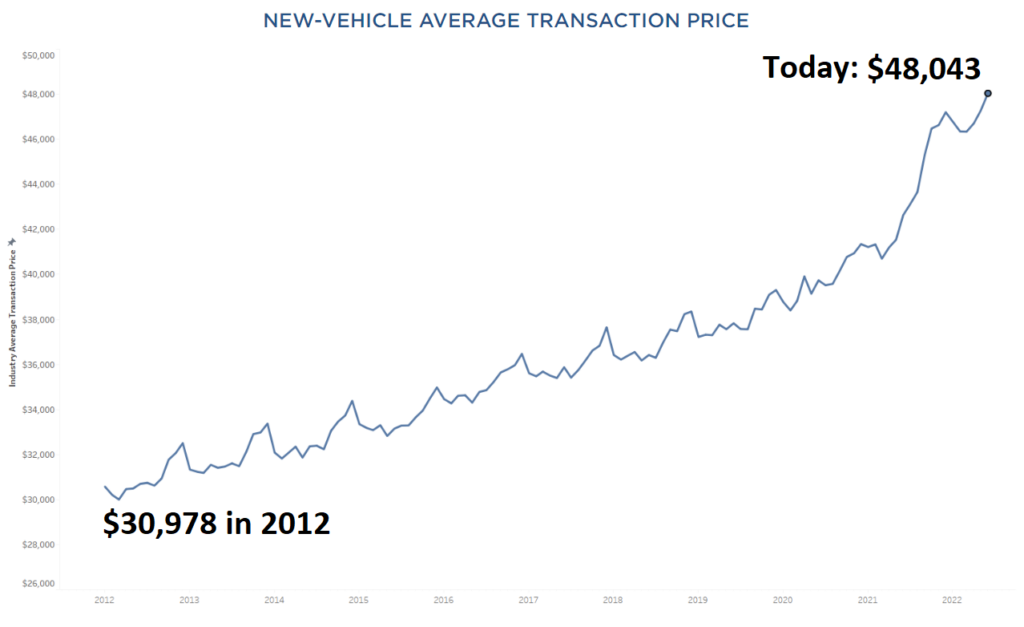

Who can afford a new car in 2022? The latest data from Cox Automotive’s Kelley Blue Book reveals that the wealthy are making up more and more of new vehicle purchases as prices soar out of reach for many. New car prices are at all-time record highs, but could this be the peak? Let’s dive into the details.

Last December, we reported a new record that everyone saw coming, but no one was thrilled about. Six months ago, the average new vehicle transaction price reached $47,202. In June of 2022, the average transaction price (ATP) soared to $48,043, according to Kelley Blue Book’s data. June prices rose 1.9% ($895) from May and were up 12.7% ($5,410) from June 2021.

A bit of perspective brings to Earth just how high new car prices are right now. Ten years ago, the average transaction price of a new car was just $31,000. The average price of a vehicle purchased in 2022 is 54% higher than it was in 2012. That’s INSANE.

Here’s how new car prices have risen over the last decade:

Here we are in the roaring twenties, and it appears that those with the means are going all-out with their vehicle purchases. Today’s data suggests that to many, it’s all about lavish luxury, no matter the price tag. The popularity of luxury autos happens to coincide with America’s total personal debt reaching an all-time high of $14.96 trillion. The average American debt (per U.S. adult) is $58,604, and three-quarters of American households have at least some type of debt.

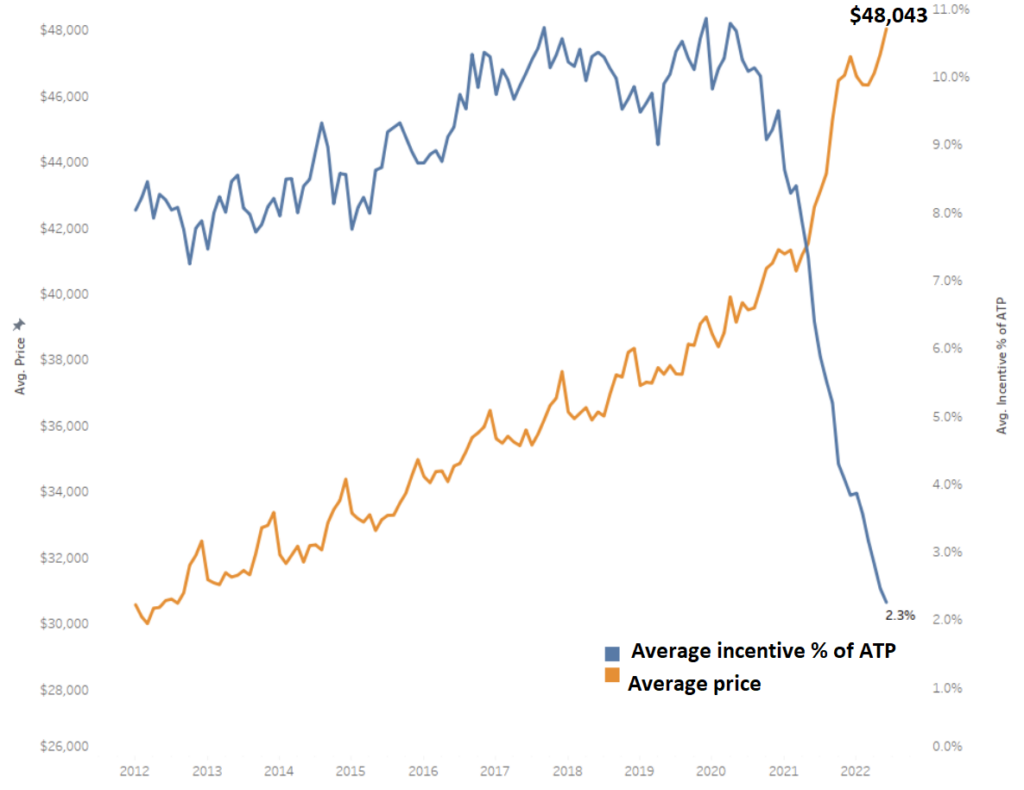

The image below shows the industry average transaction price versus the industry average incentive as $ of ATP. Clearly, manufacturer incentives are evaporating as new cars become more expensive.

Electric vehicles had the lowest incentives (as a percentage of ATP) of 0.4%, and entry-level luxury cars had the highest of 3.4%. Incentives dropped to a record low level in June, averaging only 2.3% of the average transaction price. See the latest new car incentive numbers here.

With an average transaction price of $39,040, hybrid cars saw the largest ATP increase of $3,593. Hybrids have been in the lowest supply lately of any segment. Electric vehicle prices climbed to new records in June, with an ATP of $66,997, an increase of $2,444 since May 2022.

Electric vehicle market share has crept up over the first six months of the year, despite overall vehicle sales sliding. Recently, Bloomberg noted that when other countries attained 5% market share, the floodgates opened to more rapid EV adoption. Will this familiar pattern play out in the United States? With EV transaction prices averaging over $66,000, it’s a bit of a stretch to think EV adoption could happen so quickly. We must not forget that the median household income is around $70,000, just a few thousand dollars more than EVs are selling for today. Electrification is not top of mind for most American households, but the worsening affordability crisis is for many.

Is the car bubble about to pop? Here’s what the latest data shows. We keep close tabs on the latest automaker inventory numbers, and we’re finally starting to see inventory increase, albeit slowly. Wholesale used car prices are another leading indicator of where the car market is headed, and this week we saw a sharp downturn in prices in almost every vehicle class.

In mid-July, wholesale used car prices dropped 0.35% in just one week, the third week in a row of declines. Trucks and SUV prices declined by nearly half of one percent. While this alone may not sound significant, remember that this is week-over-week, not monthly or yearly data. See the full data on used car numbers, updated weekly.

In conclusion, car prices may drop if both of these trends continue. But they’ll have to continue much longer before we see a substantial decline in used and new car prices. If automakers are finally able to overcome supply chain constraints, new vehicle inventory will continue to rise, and dealer lots will have more vehicles. Until that happens, used car prices will remain high. Check back for the latest updates at caredge.kinsta.cloud/guides.

If you’re in the market for a GMC Sierra, Buick Enclave, or any of the two brand’s other models, we have some disappointing news for you. At what most would agree is the absolute worst time for automakers to pack more profits into car sales, Buick and GMC are forcing what they consider to be ‘value added’ subscriptions, and it’s not optional. The news from GM is just the latest example of automakers introducing what they call ‘software-derived revenue’, and executives are not being shy with their plans to introduce more of the same in the near future.

Would you consider forcing customers to pay for an add-on they may not want to be anti-consumer, or is that just how the world works these days? It’s one thing to sell a new vehicle with a trial subscription, but it’s another to add a thousand dollars to the price tag for a software subscription the customer may never use.

As of July, General Motors is adding between $905 and $1,675 to Buick and GMC price tags for a 3-year subscription to GM’s OnStar Connected Services. To the uninitiated, this may sound like yet another add-on. But the thing is, GM says it’s not optional. No matter whether you want a 36 month subscription to OnStar or not, GMC and Buick customers will have to pay for it. The only model to receive the full suite of software free of additional charge is the $100,000-plus GMC Hummer EV.

A GM spokesperson confirmed the move to GM Authority, saying, “This offering provides our owners with a full suite of OnStar and Connected Services for three years, providing them with more time to enjoy services such as remote key fob, Wi-Fi data and OnStar safety services. By including this plan as standard equipment on the vehicle, it provides more customer value and a more seamless onboarding experience.”

Manufacturer incentives are already at record lows, and new car inventory is increasing at a snail’s pace. How could you push back against these new forced add-ons? Considering that GMC and Buick’s OnStar ‘Connected Services’ mandatory subscription is tacked on by the automakers themselves, dealers are not likely to negotiate on it. What we can hope for is the return of other kinds of incentives and deals. With more and more signs of the car price bubble beginning to burst, it’s too early to lose hope on that front.

It’s likely that GM will lose some customers for life as a result of this decision. Look at some of the comments we received on our YouTube video covering this topic:

Consumers are fed up, and with good reason. General Motors isn’t the only automaker trying to make car subscriptions mainstream; Volkswagen, Stellantis, Ford, and BMW all have their eyes on increasing software and subscription revenues.

Welcome to microtransaction hell. BMW wants you to subscribe to your heated seats in your new 3 series:

The car will come with all the necessary components, but payment is needed to remove a software block. How wild is that?

GM is taking the tact of “subscriptions are mandatory,” while BMW is shipping cars to customers with all of the necessary hardware to offer functionality, yet imposing a software “paywall”.

So far BMW has not launched this program in the United States, however it’s likely they will at some point. More on this from The Verge.

GM surely isn’t the first to say it or even do it, but this is the boldest forced subscription we’ve seen from a legacy automaker to date. For a decade, Tesla has been offering acceleration boosts, more range, and autonomous driving features as software ‘upgrades’ that controversially don’t get passed on to future owners. Clearly, many buyers don’t mind, as Tesla has dominated EV and overall luxury sales.

Is this yet another example of legacy OEMs going after Tesla, or is it a ploy to introduce new revenue streams for the sake of simply making more money, and charging more for vehicles? Fortunately, there’s no need to speculate, because multiple automaker executives have already shared their intentions with the public.

Not looking forward to paying a monthly subscription for conveniences like remote start or advanced cruise control? Me either. Automotive News Europe recently reported that Stellantis is launching a $23 billion software push to get into the auto subscription business.

Just how big of a business will auto subscription services become? Stellantis, the sixth-largest automaker in the world, says it plans to make $4.5 billion in annual revenue from software subscriptions in the near future. How soon? Mamatha Chamarthi, the head of Stellantis’ software business, says the company can reach their goal by 2026.

Stellantis CEO Carlos Tavares chimed in too. He’s confident that Stellantis’ software business will generate high margins more like those at tech companies than the traditional auto business. He added that in the company’s view, software-based services and subscriptions will help vehicles last longer and have higher resale values. Do you buy that?

The Blue Oval is getting into pay-to-play automotive services, too. The Ford Mustang Mach-E and F-150 Lightning electric vehicles are Ford’s first mass-produced vehicles to be fully-capable of over-the-air updates, and now Ford plans to turn their latest innovation into new revenue streams.

Wes Sherwood of Ford Communications recently told Pickup Truck Talk that Ford knows the value of what they’re bringing to their models. “These subscription services are big business for automakers – to the tune of billions. We see connected vehicle services as a huge opportunity, which is why we are transforming Ford into a software-led company and, for customers, ‘always-on’ ownership experiences where before our relationships were periodic (sales and some service). In fact, we see this market growing to $20 billion by 2030.”

If you want to be a beta tester for Tesla’s ‘Full Self-Driving”, you’ll have to add $12,000 to the price of that shiny new EV. However, Volkswagen, one of Tesla’s most admiring competitors, envisions a subscription-based payment plan for autonomous driving capabilities.

Volkswagen Group’s software unit Cariad believes pay-as-you-go autonomous driving is one way the automaker can monetize future software developments.

“There is a new business model already out there — a subscription model, or function-on-demand — where you can drive autonomously if you want, for the next 50 miles. We would support that, “ Cariad CEO Dirk Hilgenberg told Bloomberg.

Hilgenberg said it was possible to see that the service would allow the automaker the opportunity to offer other services to consumers who are freed from driving the vehicle.

“You have to make sure to have what we call a digital services platform that lets the outside world in — Google, Apple, Amazon — where you can bring your accounts to stream and be entertained, or where you can work with office products, do a videoconference or prepare yourself for the next meeting. This is the product we want to sell. The product is our platform,” he said.

When demand exceeds supply for any product, sellers have the upper hand. New car incentives dropped even further in the summer of 2022. What does fewer incentives mean for car buyers today? This is what the latest data reveals.

The pandemic really put a wrench in the typical ebbs and flows of the automotive industry. Gone are the days of gradual change. Following an unprecedented drop in car sales as COVID took hold in 2020, record demand for cars far outpaced supply in 2021 and into 2022. Today, the lingering semiconductor chip shortage continues to greatly reduce new vehicle inventory. Any time there’s a shortage of new cars, used car prices rise too. Will buying a car ever get cheaper? Well, it hasn’t yet. Here’s the latest auto manufacturer incentive data from the analysts at TrueCar:

| Q2 2022* | Q1 2022 | QoQ change | Q2 2021 | YoY change | |

|---|---|---|---|---|---|

| BMW | $1,206 | $2,358 | -49% | $4,713 | -74% |

| Daimler | $1,257 | $2,012 | -38% | $3,574 | -65% |

| Ford | $1,193 | $1,824 | -35% | $2,567 | -54% |

| General Motors | $1,847 | $1,974 | -6.40% | $4,399 | -58% |

| Honda | $818 | $1,163 | -30% | $2,167 | -62% |

| Hyundai | $620 | $890 | -30% | $2,102 | -71% |

| Kia | $650 | $1,260 | -48% | $2,549 | -75% |

| Nissan | $1,501 | $1,848 | -19% | $3,502 | -57% |

| Stellantis | $1,893 | $2,413 | -22% | $3,522 | -46% |

| Subaru | $753 | $901 | -17% | $1,339 | -44% |

| Toyota | $803 | $1,025 | -22% | $2,219 | -64% |

| Volkswagen Group | $1,169 | $1,769 | -34% | $3,730 | -69% |

| Industry | $1,228 | $1,631 | -25% | $3,003 | -59% |

As you can see, new car incentives are at a 10-year low. In the second quarter of 2022, incentives averaged $1,228 industry-wide. That’s a 59% drop year-over-year.

The latest new car inventory numbers are in, and the update brings a mixed bag of news. Overall new car inventory is up, but not nearly to the extent that is required to return normalcy to car sales. Most automakers are seeing incremental improvements.

In January of 2020, the industry’s average was 82 days’ supply. By early 2021, that figure had fallen to 66, but it would soon plummet as the chip shortage lasted longer than most expected. In July of 2022, new car inventory is slim with just 21 days’ supply.

Until more cars are sitting on dealer lots, there simply won’t be any reason for manufacturers to offer more new car incentives to buyers.

See the latest new car inventory numbers by automaker and model

You’re probably not surprised to hear that a new car costs more than ever before. The average transaction price has hovered around $45,000 for much of the past year. Two years ago, it was $38,000. With inflation AND supply chain bottlenecks, it will be a while before prices stabilize.

Monthly payments are on the rise, too. How much is too much? $500 a month? $750 a month? Maybe even a $1,000 car payment? Right now, the average monthly car payment is $712 a month. Five years ago, it surpassed $500/month for the first time. There’s a worrying trend taking hold today, and it’s one that risks spiraling out of control. A new Edmunds survey finds that 12% of car buyers are paying more than $1,000 each month for their car payment. Yes, a new car now costs as much as a home mortgage for those who choose to spend big.

Other than higher price tags, here are some considerations if you’re in the market for a new car:

Check back for the latest new car incentives. We’ll be updating this page as new numbers come in. Remember, you can still find a deal out there, but it will take a bit more work on your part. The CarEdge team is here to help you every step of the way. As Ray always says, knowledge is power, and CarEdge’s auto experts empower car buyers every day with the know-how that can save thousands of dollars.

Will 2023 bring more affordable EVs with more range and faster charging? These are the five best new electric models coming to a charging station near you.

Later this year, Honda’s first electric vehicle to take to North American roads will be beginning production ramp-up. The Honda Prologue electric crossover is expected to be a 2024 model with a late-2023 arrival. However, we’re looking forward to the Prologue for reasons you might not expect.

Honda waited too long to get into the EV game. While many argue that Honda’s decision to focus on hybrid powertrains was a good move for their sales and bottom line, the delay ultimately resulted in Honda looking for strategic partners as an avenue for electrification. In the case of the 2024 Honda Prologue, Honda is working closely with General Motors to bring the same Ultium powertrain in the Chevrolet Silverado EV into Honda’s first American-made EV. But this won’t be a Chevy Bolt 2.0. The Prologue will benefit from a new, much better generation of EV engineering.

What makes GM’s Ultium electric powertrain so special?

Not only is the Honda Prologue going to be powered entirely by GM’s Ultium electric platform, GM is going to build the Prologue EV from start to finish. This begs the question, is the Prologue even a Honda at all? It’s starting to sound a lot like Chevrolet’s Equinox EV with the Honda nameplate.

Why then are we looking forward to the Honda EV that’s really a Chevy with a Honda badge? It’s all about the hope and promise of the Ultium platform. Here’s why this is worth getting excited about:

Want to know more about the Honda Prologue electric crossover SUV? Here’s our full breakdown of the Prologue.

Ironically, Fisker’s first shot at vehicle production ended when the first batch of Fisker Karma electric sports cars succumbed to the saltwater floods of Hurricane Sandy in 2012. But that didn’t stop Fisker from naming their next vehicle the Fisker Ocean.

The Ocean is an electric crossover that targets three consumer demands that EV automakers have so far struggled to unite under the umbrella of one electric model: over 300 miles of range, versatile capabilities, and affordable pricing. It’s almost as if the Fisker Ocean is on track to be an electric Subaru Forester with goals like that.

Plus, if you’re the type of driver that shies away from commitment, Fisker has a sweet deal for you. The innovative Fisker Flexee Lease option lets you lease the Ocean for $379/month with no term commitment. You can hand back the car at any time. It’s essentially a long-term rental with no strings attached.

The Fisker Flexee Lease requires an initial payment of $2,999, and it includes up to 30,000 miles per year. Maintenance is covered. Sounds like a great deal if you ask me!

Here’s what we love about the 2023 Fisker Ocean:

Learn more about the Fisker Ocean electric crossover in our deep dive review. More to come!

Three out of four car buyers today opt for a crossover, SUV or truck. We’ve all heard it before: sedans are on their way out. Not so, says Hyundai. And judging from the reactions to the IONIQ 6’s design debut, the masses still have an appetite for a sleek sedan, as long as it brings something new to the table.

In a welcome surprise, the IONIQ 6 went on sale months earlier than expected. With up to 361 miles of range and ultra-fast charging speeds adding 200 miles of range in under 20 minutes, this is one of the best. Browse Hyundai IONIQ 6 listings in your area.

Just one year ago, there wasn’t a single electric pickup truck available for purchase. Tesla’s Cybertruck started the electric pickup conversation with the swing of a sledgehammer in 2019, but other automakers are much closer to bringing electric trucks to market. The outdoorsy Rivian R1T has begun deliveries, and the GMC Hummer EV is crab-walking its way into customers’ hands. But these two premium offerings are at a higher price point than what the majority of drivers can afford. Enter the Ford F-150 Lightning (on sale now) and its chief competition, the all-new Chevrolet Silverado EV.

The electric Silverado is not just a standard truck with an electric motor. It’s much more than that, and far more capable.

Is the Silverado EV better than the F-150 Lightning? Here’s how they compare:

| Starting Price | Fully-Loaded | Range | Max Charge Speed | Vehicle-to-Load Output | EV Tax Credit | |

|---|---|---|---|---|---|---|

| Silverado EV | $39,900 | $105,000 | "up to 400 miles" | 350 kW | 10.2 kW max | No (cap reached) |

| F-150 Lightning | $39,974 | $90,874 | 230 to 320 miles | 150 kW | 9.6 kW max | Yes |

Something to keep in mind: F-150 Lightning buyers have already had their hopes dashed by outrageous dealer markups. What was supposed to be a reasonably-priced electric truck is more often selling to the highest bidder. Will the same happen to the Silverado EV late next year? Considering that Ford, not GM, is the automaker publicly working on a way to end EV dealer markups, it appears likely.

Still, this electric truck is going to be awesome. Here’s our full review of the Silverado EV.

Two Chevys on this list? Crazy, right?! GM’s $2.3 billion joint venture with battery engineering powerhouse LG Chem is beginning to work it’s way into products, and we’re thrilled for what’s to come.

Just about all we know of the upcoming Equinox and Blazer EVs is by way of CEO Mary Barra’s online enthusiasm. Here’s what we know so far.

As you can see, there’s not a lot to say about the 2024 Chevy Equinox EV. Why are we so excited about it then? The mere prospect of an affordable EV is almost too good to be true at this point. The average EV sells for $56,000, a whole $10,000 more than the average combustion-powered vehicle. Should consumers in the market for an affordable EV be stuck with the range and charging limits of the Chevy Bolt and Nissan Leaf? We hope GM follows through on their promise to bring a truly desirable budget EV to the masses in 2023.

Average monthly car payments have been increasing ever since the beginning of the chip shortage in 2020. Today, the average monthly car payment for a new car exceeds $700 for the first time ever, while the average monthly car payment for a used vehicle is more than $500.

Over the last 18+ months we’ve covered the tenuis rise of car prices. It’s shocking to think that the average car payment is now closing in on the average mortgage payment in America. Data from Edmunds shows that 12% of new car buyers in June are paying more than $1,000 a month. In 2021 the average home mortgage payment was roughly $1,000 a month. Let that sink in.

Here’s the latest data on new and used car payments, affordability, and which vehicles you should consider if you are looking for a relative “bargain” in today’s market.

Let’s dive in.

Data from J.D. Power/LMC Automotive suggests that the average new car transaction price was $45,844 in June. As compared to data from Cox Automotive, this average transaction price is actually down considerably when compared to prices from the end of 2021 and earlier in 2022.

For example, at the end of 2021 the average transaction for a new vehicle was $47,077 according to Cox Automotive, however the average monthly payment was only $688. This was a function of cheaper interest rates.

Today, the average monthly payment for a new car stands at $712 dollars. That is more than rent for a one bedroom apartment in some cities.

| City | Rent |

|---|---|

| Akron, OH | $640 |

| Wichita, KS | $710 |

| Lubbock, TX | $720 |

| Shreveport, LA | $740 |

| Lexington, KY | $800 |

| El Paso, TX | $860 |

| Baton Rouge, LA | $860 |

| Tallahassee, FL | $860 |

| Oklahoma City, OK | $870 |

| Des Moines, IA | $890 |

Average loan terms for a new car sit at 70 months, with most consumers opting for 6 year financing terms at an average interest rate of just over 5%. Back in December of 2021 the average new car interest rate was under 4%, accounting for the uptick in monthly payment amounts.

As you very well know, used car prices have skyrocketed ever since the beginning of the chip shortage. For the first time ever, the average used car monthly payment sits above $500. Data for Q1 of 2022 shows an average interest rate of 8.6% and an average loan term of 68 months. We expect data for Q2 to show a significant increase in the interest rate and monthly payment. We would not be surprised to see 9%+ as the average interest rate on a used car loan, and monthly payments in excess of $525 for the first time ever.

Used hybrids and electric vehicles are especially expensive in today’s market, with monthly payments on more fuel efficient vehicles in excess of $700.

Cox Automotive tells us that the average transaction price for a new car was $47,148 in May 2022. Where are the new car values?

Sadly, non luxury vehicles are seeing their prices increase rapidly as more consumers look for “value”. The average price paid for a new non-luxury vehicle in May was $43,338; on average a customer paid $1,000 over MSRP for a new non-luxury vehicle. We are seeing some below MSRP deals on Stellantis brands; Jeep, Ram, Alfa Romeo, Chrysler.

The average luxury car buyer paid $65,379 in May. They also spent about $1,000 over MSRP to get their new car.

The average electric vehicle buyer paid $64,000 in May. The Chevrolet Bolt represents the only real “bargain” in the EV space.

The average truck buyer paid $56,216 in May, while the average van buyer paid $48,671, and the average SUV buyer paid $46,073. The only “value” segment on the list are cars, where the average sedan buyer paid $41,902 in May.

Automakers such as Nissan have average transaction prices of $34,681. Compared to other automakers such as Toyota ($40,036) and Hyundai ($35,988) they represent a relative “steal”.

Ford, Stellantis, and GM have seen their average transaction prices increase significantly. Ford’s average transaction price stands at $49,528. Stellantis is at $53,212, and GM is at $50,854.

As much as I love electric vehicles, their faults are not lost on me. Charging infrastructure lacks, service outside of warranty is costly, and most of all, they’re really expensive. Despite the hurdles facing EVs in 2022, a new Bank of America Merrill Lynch Car Wars study predicts that EVs, PHEVs and hybrids will make up 60% of new models in 2026. With so many new electric cars coming making debuts in 2023 and 2024, time is running out to prepare the masses for the big changes ahead.

Every year, Bank of America Merrill Lynch releases their cleverly-named Car Wars report. The report leverages the bank’s access to big data to forecast automotive industry trends like no other. In the 2022 Car Wars Report, John Murphy, a senior auto analyst at Bank of America Merrill Lynch, told Automotive News that he expects automakers to launch roughly 245 new models over the next four years. That averages out to 61 new models per year — 50 percent higher than the average over the past two decades.

Why the flood of new car models? Simply put, new powertrains inspire new models. No one wants to retrofit a billion-dollar electric powertrain onto a decades-old chassis.

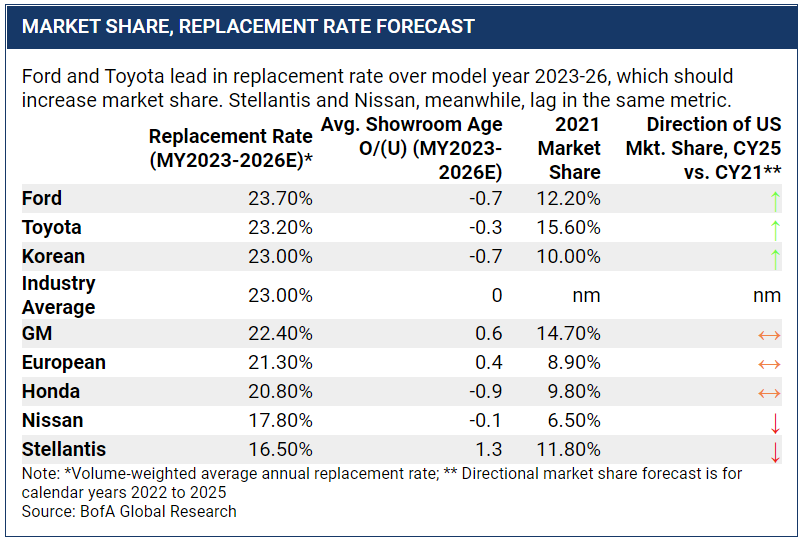

Analysists took the strategies of each major automaker into consideration and shared their market share forecasts for model year 2025. Notably, Stellantis and Nissan are forecast to lose market share despite funneling billions of dollars into new electrified models. General Motors, Honda and European brands are forecast to maintain steady market share in the U.S. market. With the upcoming Silverado EV, Cadillac Lyriq and Equinox EVs just around the corner, it’s not what automakers like to hear at such a crucial moment.

The automakers with the highest model replacement rate fared best in the Car Wars analysis. Ford, Toyota and the Korean automakers have the highest expected replacement rate, and therefore are expected to gain market share.

However it’s what Bank of America thinks about Tesla that’s drawing headlines.

In the annual Car Wars study, Bank of America Merrill Lynch senior auto analyst John Murphy predicts that Tesla’s EV market share will drop from over 70% today to just 11% in 2025. That’s the most pessimistic Tesla forecast we’ve seen in a few years, harkening back to when talking heads from legacy automakers regularly predicted doom and gloom for Tesla.

Why the forecasted 60% drop in market share? Murphy cites the massive push to electrification from the likes of Ford, General Motors, Hyundai and Kia. It’s not clear if Murphy considered the significance of Tesla’s Supercharger Network, top-notch over-the-air update capabilities and high brand loyalty in his forecast. What do you think?

Looking for EV sales numbers? July is here, and that means the second quarter of 2022 has come to an end. As automakers release their Q2 2022 EV sales numbers, be sure to check the latest updates and statistics at CarEdge’s EV market share and vehicle sales report.

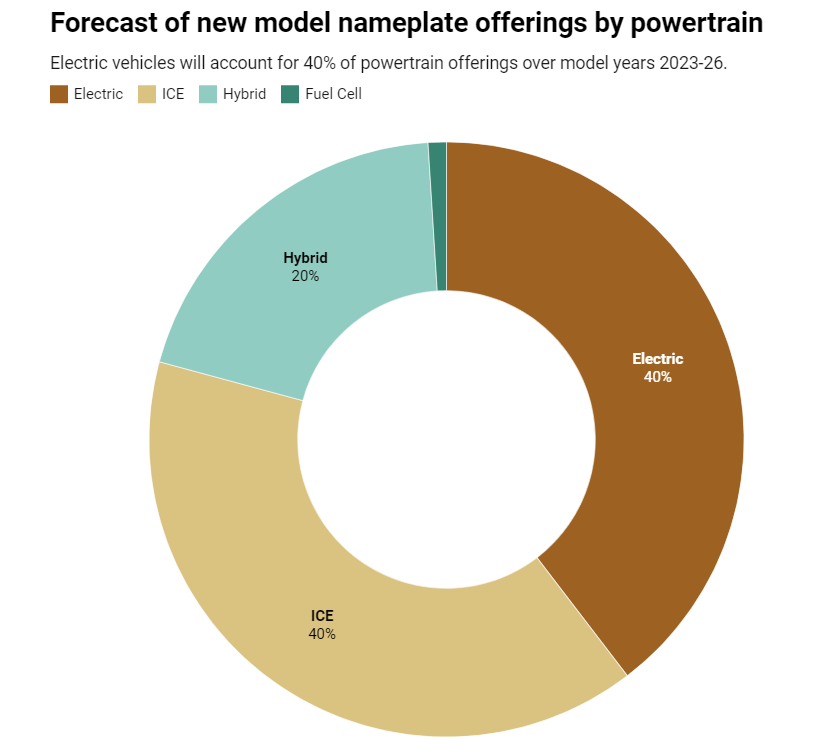

Of the new models introduced between 2023-2026, 60 percent will be either electric or hybrid while 40 percent will be internal combustion. Among notable 2023 electric cars just around the corner are electric trucks, sedans, and a whole lot of crossovers.

Headline-grabbing claims aside, this EV market share forecast is in line with much of the industry’s thinking. In fact, automakers are sure to hope that these numbers become reality, as they are actively investing a cumulative total of roughly $500 billion dollars in electrifying their lineups.

With high-stakes new electric cars in 2023, legacy automakers are definitely taking EVs seriously. Which 2023 electric car are you most excited about?