CarEdge saved me over 4,500 dollars on a brand new Honda Pilot. I can't say thank you enough.

Price intelligence

Find a wide range of vehicle listings with market insights on new and used listings near you.

What can I do with CarEdge?

What can I do with CarEdge?

Get access to exclusive information so you can make an informed car buying decision — all in one place.

Find a wide range of vehicle listings with market insights on new and used listings near you.

Track your vehicle’s value and cash in when the time is right to sell.

Access to our proprietary data to help you find the right car, at the right price. Find these unlocked on every listing after subscribing.

With our expert-led, tech-enabled car buying service, we will locate, negotiate, and deliver your vehicle so you can get a new car hassle free.

Help us personalize your CarEdge experience — it only takes a second.

Your answers help us personalize your CarEdge journey — we’ll follow up with tips and next steps that match your buying timeline.

Florida Governor Ron DeSantis has approved a bill partially banning direct-to-consumer car sales in the state, a move set to make the most pro-dealer state even more of a car dealer’s paradise. The legislation, heavily influenced by the Florida Automobile Dealers Association (FADA), also imposes restrictions on automakers, limiting their ability to penalize dealers who choose to mark up car prices. The new Florida law is being lauded by car dealer associations. Make no mistake: House Bill 637 is bad news for consumers, no matter how you look at it.

The Florida dealer lobby played an instrumental role in drafting and pushing through the bill (HB 637). For dealers, their efforts have paid off. The legislation mandates that traditional automakers must sell their vehicles through approved dealers, reinforcing the conventional car sales model and curbing the growing trend of direct-to-consumer sales.

However, the law includes a specific exception for electric vehicle giant Tesla. Tesla was the first to find success with its direct-to-consumer model. By including an exception for automakers who have never sold via a dealership model, Florida is steering clear of a clash with the #1 EV seller. This exception could potentially pave the way for other electric vehicle brands like Lucid and Rivian to continue their direct-to-consumer sales in the Sunshine State.

FADA President, Ted Smith, addressed this carve-out. “We made a clear delineation between a manufacturer that has never had dealers and maybe never will, and those who have been heavily dependent upon their dealerships to be their marketing and sales presence in Florida.”

Another part of the bill allows dealers to set their own prices without adhering to the manufacturer’s suggested retail price (MSRP). The new law prohibits automakers from penalizing dealers for markups. The bill also explicitly restricts automakers from limiting allocation to dealers who impose markups. Equally, automakers are prevented from rewarding dealers who choose to sell at or below MSRP.

But wait, there’s more. The bill states that manufacturers must pay dealers eight percent of the revenue from any post-purchase electronic vehicle upgrades or activations sold within the first two years of purchase. This includes both one-time and subscription-based upgrades, potentially pushing prices higher for these additional services. Evidently, car buyers will have even more reasons to reconsider subscriptions for heated seats or over-the-air updates for acceleration boosts.

These changes highlight the huge influence of dealer lobbies in the United States. In the most recent election cycle, 85.5% of U.S. Representatives and 57 Senators received campaign contributions from auto dealers. This influence is so great that even the Consumer Financial protection Bureau (CFPB), established in 2011 to protect consumer interests, has a provision prohibiting the agency from directly monitoring dealerships.

Ultimately, the landscape of car buying continues to evolve, with power plays between manufacturers, dealers, and legislators. At CarEdge, we’re committed to helping you navigate car buying to find the best deals.

Browse cars with behind-the-scenes market data with CarEdge Car Search. Ready to unlock the full suite of data for a car you’re serious about? CarEdge Report is your one-stop shop for deal analysis. Get 1:1 expert guidance as you learn how to negotiate the BEST deal with CarEdge Coach.

Stay tuned as we continue to monitor the impact of this new Florida Law on car buyers in Florida and potentially beyond.

The current landscape of the car market is an intricate maze of fluctuating inventory levels and shifting price tags. Your guiding light through this labyrinth? Knowledge, of course. The knowledge that shines the brightest is the understanding of Market Day Supply (MDS). This illuminates the number of days it would take to sell all the inventory of a particular model, assuming no new cars enter the market and the current sales rate holds steady. A high MDS suggests a surplus that may give you, the buyer, some bargaining leverage. In contrast, a low MDS may indicate the sellers have the upper hand.

By exploring CarEdge Data, we’ve highlighted which new cars in 2023 have the best and worst reliability ratings, and what the inventory data tells us about them. We think you’ll agree that these insights are rather fascinating, and provide you with the knowledge to navigate the market like a pro.

Using CarEdge Data, we analyzed nationwide supply and sales data for the ten most reliable cars in America, according to Consumer Reports. Here’s the data, and what it means for buyers.

| CR Reliability Ranking | Make | Model | Starting Price | Market Day Supply | Total For Sale | Total Sold (45 Days) |

|---|---|---|---|---|---|---|

| 1 | Toyota | Corolla Hybrid* | $24,145 | 24 | 11887 | 22588 |

| 2 | Lexus | GX | $59,775 | 56 | 3358 | 2679 |

| 3 | MINI | Hardtop 2 Door and 4 Door | $26,795 | 95 | 2809 | 1329 |

| 4 | Toyota | Prius | $28,445 | 23 | 1314 | 2574 |

| 5 | Mazda | MX-5 Miata | $29,215 | 85 | 1184 | 631 |

| 6 | Lincoln | Corsair | $40,085 | 96 | 3315 | 1550 |

| 7 | Toyota | Corolla* | $22,795 | 24 | 11887 | 22588 |

| 8 | Subaru | Crosstrek | $26,290 | 18 | 238 | 598 |

| 9 | BMW | 3 Series | $44,795 | 67 | 2642 | 1778 |

| 10 | Toyota | Prius Prime | $33,345 | 43 | 630 | 664 |

Firstly, the reliability leaderboard has a strong Toyota presence. Models like the Toyota Corolla Hybrid, Toyota Prius, and Toyota Corolla claim high reliability ratings from Consumer Reports. These models fly off the dealer lots relatively quickly with a Market Day Supply of just 23-24 days, showing the high demand for reliable Toyota cars. Data was unavailable for the Corolla Hybrid, so we have included the latest numbers for the overall Corolla model. These popular, reliable cars will be less negotiable due to higher demand and quicker sell times.

CarEdge’s Ray Shefska made it clear that despite great reliability and high demand, the days of being forced into paying a dealer markup are long gone. “No matter what the dealer tells you, never pay a markup or so-called ‘market adjustment’ for a new Toyota. The car market is very different in 2023 compared to the madness we saw during the chip shortage.”

Next, the MINI Hardtop (2 Door and 4 Door) and Lincoln Corsair, despite their high reliability, have a much longer MDS (95 and 96, respectively), suggesting these reliable models may not be as in-demand. You’ll have more leverage negotiating these prices, especially with industry knowledge and familiarity with how to work a deal.

The Subaru Crosstrek, another model with a high reliability rating, stands out with the lowest MDS among the top 10 reliable cars, indicating the supply can barely keep up with demand. CarEdge Car Coach Justise says that Subaru has been the low-inventory king for many years, and that’s not changing any time soon.

Looking at the price tags, the most reliable vehicles come with a broad range of starting prices, from $22,795 (Toyota Corolla) to $59,775 (Lexus GX). This proves that reliability isn’t necessarily associated with a steep price.

Car buyers aren’t racing to dealer lots for the models known for poor reliability. Unfortunately, American brands dominate the bottom ten.

| Make | Model | Starting Price | Market Day Supply | Total For Sale | Total Sold (45 Days) |

|---|---|---|---|---|---|

| Jeep | Wrangler | $36,990 | 98 | 26726 | 12330 |

| Mercedez-Benz | GLE | $58,850 | 69 | 5700 | 3733 |

| Jeep | Gladiator | $40,785 | 289 | 20945 | 3260 |

| Chevrolet | Silverado 1500 | $36,300 | 93 | 68320 | 33219 |

| GMC | Sierra 1500 | $37,100 | 121 | 30856 | 11477 |

| Chevrolet | Bolt | $27,495 | 35 | 3026 | 3908 |

| Ford | Explorer | $38,355 | 93 | 28323 | 13688 |

| Nissan | Sentra | $21,145 | 60 | 13381 | 10048 |

| Lincoln | Aviator | $54,735 | 178 | 4360 | 1103 |

| Hyundai | Kona Electric | $34,885 | n/a | n/a | n/a |

The Chevrolet Silverado 1500, despite its less than stellar reliability, has a significant volume on sale but a relatively high MDS. The takeaway? It’s plentiful but not necessarily popular.

Two other models, the Jeep Gladiator and Lincoln Aviator, despite their lower reliability, have very high MDS (289 and 178, respectively). It appears these models may be the wallflowers of the dealership lots.

Meanwhile, the Nissan Sentra holds its own despite lower reliability, with a fairly low MDS (60). Its budget-friendly starting price may be a contributing factor.

Interestingly, the Hyundai Kona Electric does not have available market or sales data, shedding little light on its demand or supply status.

As we can see, both highly reliable and less reliable cars come with a wide range of starting prices. This indicates that the cost is not necessarily a reliable indicator of its reliability.

Now, armed with these insights, you can navigate the market better. Whether you’re looking for a reliable titan like the Toyota Corolla, or even considering a less reliable model like the Chevrolet Silverado 1500, understanding the role of market days’ supply can give you the edge in your car-buying journey. Where there’s more inventory, greater negotiability is sure to follow.

Don’t forget to check out CarEdge Car Search, where auto industry insiders see behind-the-scenes data with every new and used car listing!

But we won’t leave you just yet. We want to arm you with more resources to make your journey smoother. One such tool is our free Car Buying Cheat Sheet. This popular resource can enhance your understanding of the market and help you zero in on the perfect car at the perfect price.

For a more detailed understanding, download your first CarEdge Report today. This report offers a comprehensive breakdown of key numbers in a simple and digestible format, setting you up for success at the negotiation table.

And if you’re looking for a personalized touch, CarEdge Coach is your ticket to savings. Our expert car buyers can offer personalized advice and help you negotiate thousands off your next car.

Don’t navigate the car market alone; let CarEdge steer you in the right direction. You’ll be thankful you did.

Navigating the current car market can be a daunting task, with its varying inventory levels and volatile prices. In this context, knowledge truly is power. A critical piece of this knowledge is understanding the Market Day Supply (MDS).

MDS is a measure of the number of days it would take to sell all of a particular model of car, based on the current sales rate, assuming no additional inventory is added. A high MDS suggests an oversupply, potentially giving buyers leverage for negotiation, while a low MDS might indicate a seller’s market, where negotiating could prove tougher.

Using CarEdge Pro, we identified which new cars have the most and least inventory available in December 2025.

Why does inventory matter to car buyers?

Inventory influences negotiability. When there’s a glut of cars, dealers will be more inclined to negotiate with you. Slim pickings? Not so much. This valuable insight can give you an edge in your car buying journey, helping you save money and avoid the hassle.

Here are the fastest and slowest-selling cars and trucks in America right now.

👉 Looking for SUVs, Trucks, or EVs? We’ve got it all.

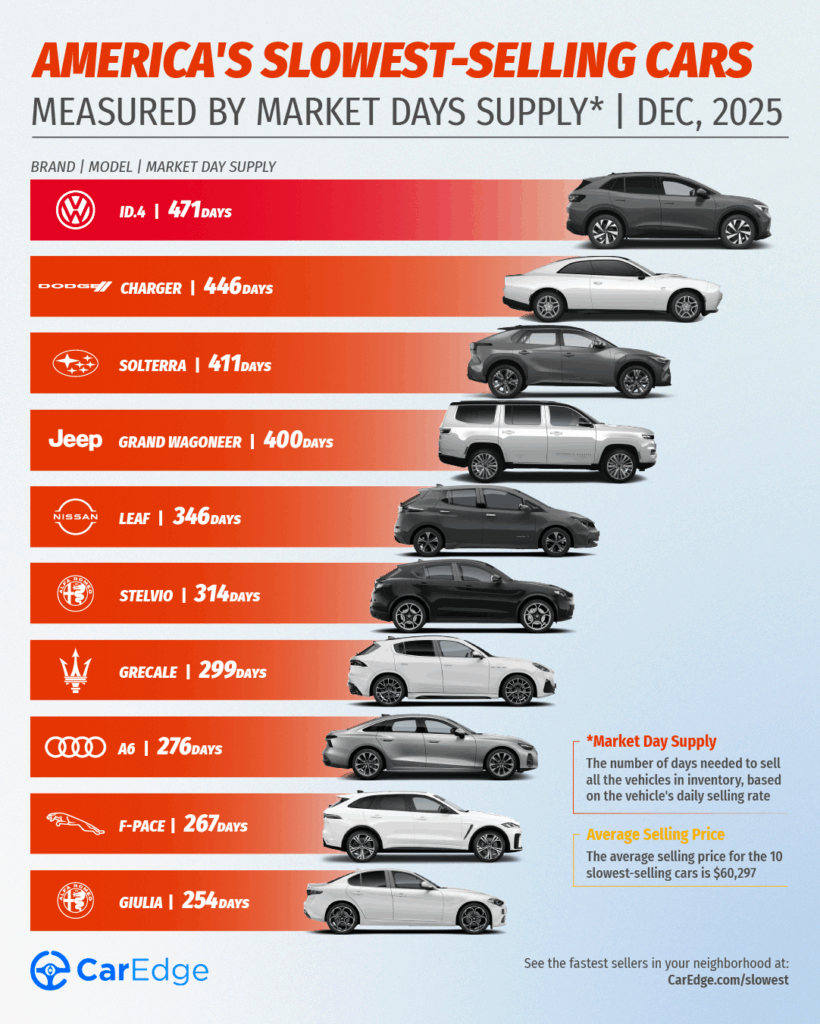

These are the slowest-selling cars in the U.S. right now. Following the expiration of the federal EV tax credit in September, sales of fully-electric vehicles have fallen off a cliff. In fact, the three slowest sellers are all EVs. At the top of the list, the Volkswagen ID.4 is the slowest-selling car in America in December 2025. Five Stellantis models are the top 10, a sharp increase from last month.

The average selling price for the 10 slowest-selling cars is $60,297 in December 2025.

Here are the 10 slowest-selling new cars, in other words, the models with the most inventory today.

| Make | Model | Market Day Supply | Total For Sale | 45-Day Sales | Average Selling Price |

|---|---|---|---|---|---|

| Volkswagen | ID.4 | 471 | 1,371 | 131 | $48,036 |

| Dodge | Charger | 446 | 2,588 | 261 | $56,936 |

| Subaru | Solterra | 411 | 868 | 95 | $41,463 |

| Jeep | Grand Wagoneer | 400 | 1,254 | 141 | $96,557 |

| Nissan | LEAF | 346 | 960 | 125 | $31,076 |

| Alfa Romeo | Stelvio | 314 | 886 | 127 | $57,297 |

| Maserati | Grecale | 299 | 672 | 101 | $82,381 |

| Audi | A6 | 276 | 2,467 | 402 | $64,960 |

| Jaguar | F-PACE | 267 | 2,136 | 360 | $70,204 |

| Alfa Romeo | Giulia | 254 | 554 | 98 | $54,057 |

There’s BIG potential for deals on any of these cars, but only with negotiation know-how.

👉 See local fastest and slowest sellers [free tool]

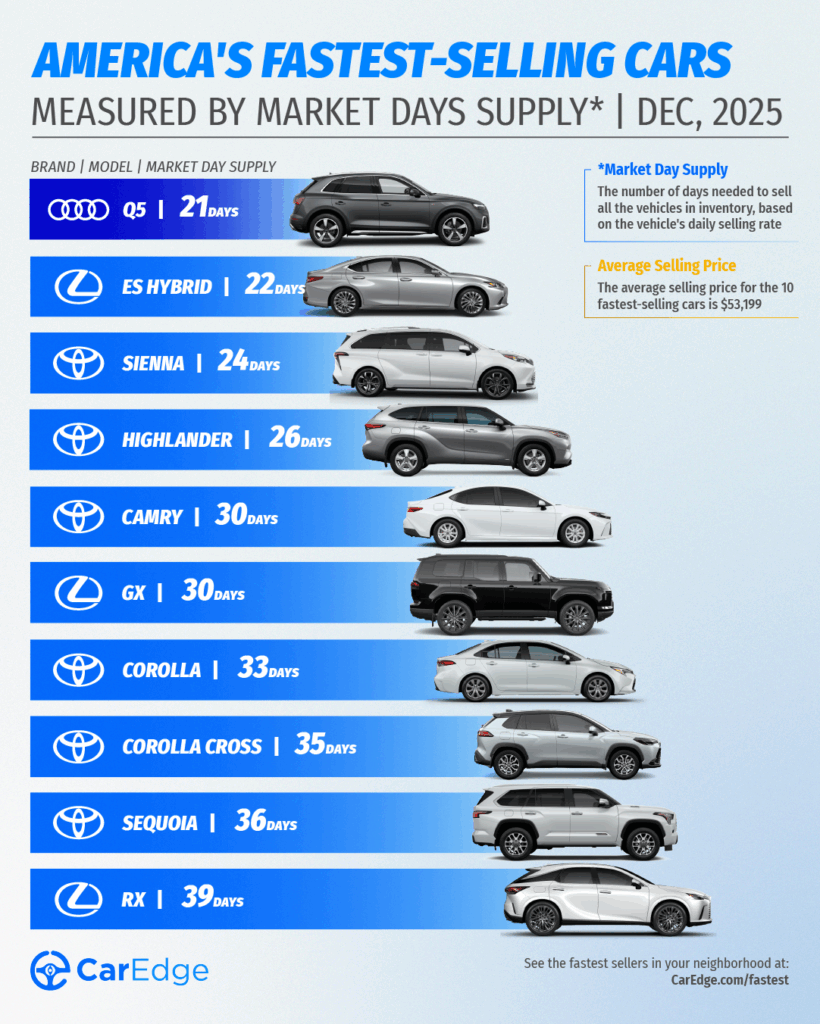

On the other side of the coin, these are the fastest-selling cars today. This month, all but one of the fastest-selling cars and SUVs are Toyota models. Audi’s Q5 has jumped into first place as buyer’s anticipate an incoming shipment of 2026 models. There are only 500 Q5s for sale nationwide currently.

Three Lexus models and six Toyota models occupy the rest of the top 10. The Toyota Sienna, Camry, Highlander, and Corolla are all quick sellers, and are the toughest to negotiate.

If you’re shopping for any of these new cars in 2025, you’ll be up against stiff competition. The average selling price for the 10 fastest-selling cars is $53,199.

Here are the fastest-selling cars in America right now:

| Make | Model | Market Day Supply | Total For Sale | 45-Day Sales | Average Selling Price |

|---|---|---|---|---|---|

| Audi | Q5 | 21 | 546 | 1,198 | $59,913 |

| Lexus | ES Hybrid | 22 | 701 | 1,410 | $52,166 |

| Toyota | Sienna | 24 | 8,769 | 16,221 | $51,910 |

| Toyota | Highlander | 26 | 5,408 | 9,238 | $52,294 |

| Toyota | Camry | 30 | 41,926 | 62,424 | $34,952 |

| Lexus | GX | 30 | 2,505 | 3,708 | $80,358 |

| Toyota | Corolla | 33 | 28,271 | 38,163 | $25,446 |

| Toyota | Corolla Cross | 35 | 15,932 | 20,331 | $31,303 |

| Toyota | Sequoia | 36 | 4,269 | 5,375 | $83,585 |

| Lexus | RX | 36 | 7,307 | 9,189 | $59,257 |

👉 See local fastest and slowest sellers [free tool]

Ready to outsmart the dealerships? Download your 100% free car buying cheat sheets today. From negotiating a deal to leasing a car the smart way, it’s all available for instant download.

👉 Know before you buy! Estimate your future insurance costs with our free car insurance calculator. We’re here to help!

Here’s a powerful and sobering statistic: In 2023, 30% of used cars have a price tag of under $20,000. Five years ago, 60% of used cars were below that price point. Where have all of the affordable used cars gone, and will they ever return to the market? We’ll take a look at the latest analysis from Edmunds, as well as the latest used car market data from CarEdge. Used car deals can still be had, if you know where to look, and how to negotiate.

The impact of the infamous chip shortage of 2021 and 2022 continues to be felt in the used car market. An astonishing 18 million new cars were never produced during this period, essentially erased from production schedules and not replaced. This production gap has created a ripple effect that will continue to influence the used car market for years to come, and this shift is just one of the significant changes the industry is undergoing.

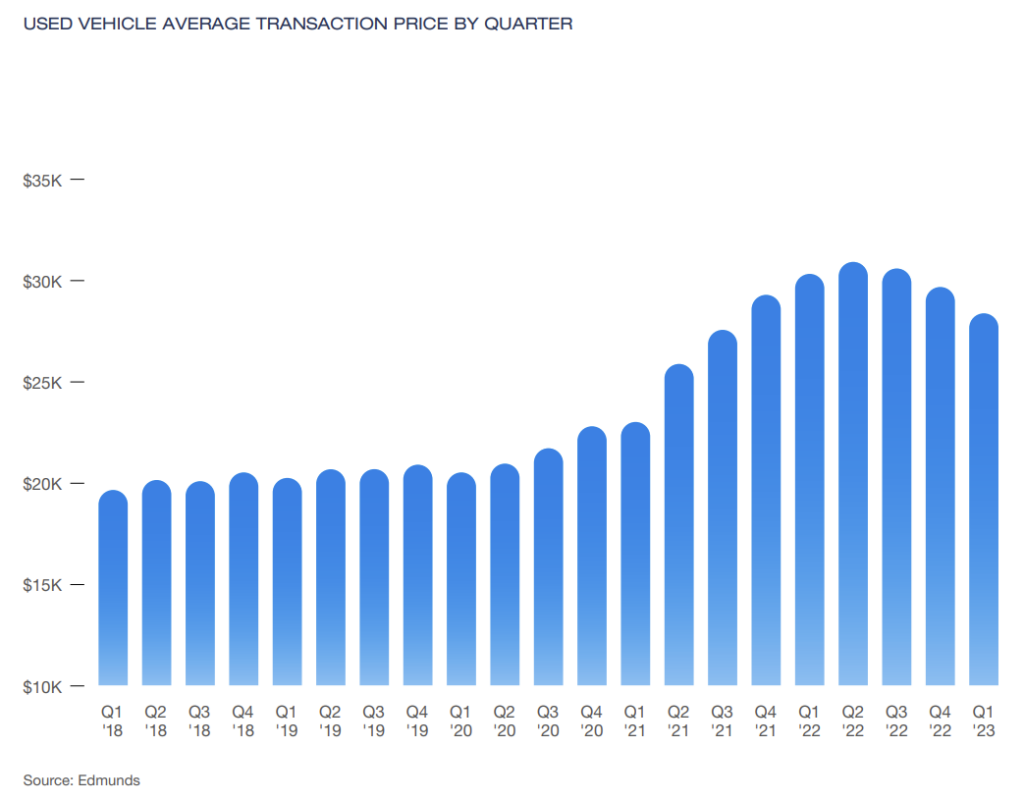

The latest data from Edmunds suggests that we might be facing a new normal rather than a temporary aberration. In terms of pricing, the average used car transaction price fell by 6.4% in the first quarter of 2023 compared to the same period last year. Sounds great, right? Not so fast. Used car prices are still a staggering 44% higher than the average back in 2018. To put it in perspective, the average selling price for a used car in America in Q1 2023 was $28,381, a far cry from the $19,657 average seen five years ago.

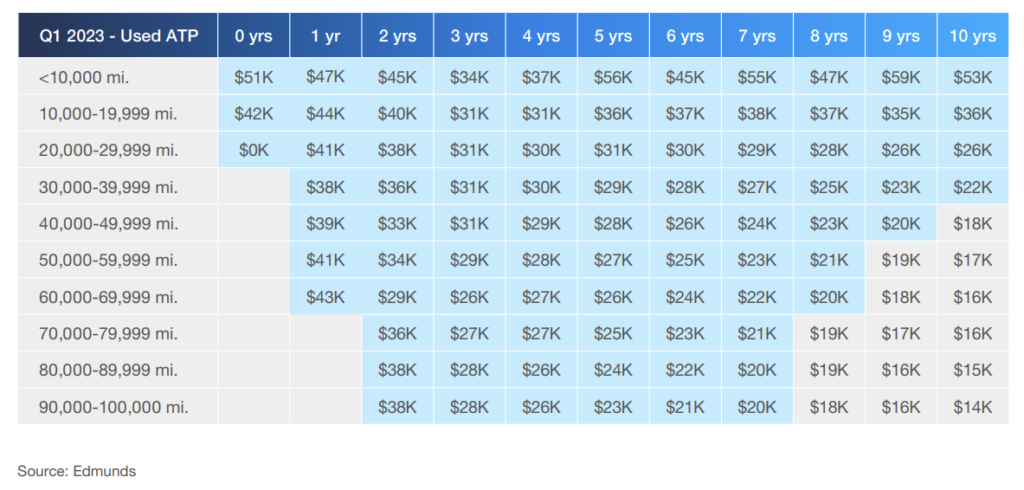

Used cars with a price tag of under $20,000 are hard to come by. The Edmunds data suggests that consumers have to look towards used cars that are at least 8 years old and have over 70,000 miles on the clock before they can find sub-$20,000 prices.

If you’re hoping for a used car that costs $15,000 or less, you’ll likely be considering vehicles that are a decade old or more. On top of that, there’s a huge mismatch in demand versus supply of cheap used cars. People want affordable transportation, but the new car market simply doesn’t offer it. The result is more competition for cheap used cars.

Older vehicles are seeing a surge in popularity despite their age. The reason is simple: they’re the only affordable cars around. Nearly half of all used cars sold today are older models priced under $25,000. In the new car market, a mere 5% of cars are sold for less than that price.

It’s more important than ever for consumers to understand car market trends and adjust their expectations (and budget) when setting out to purchase a used vehicle.

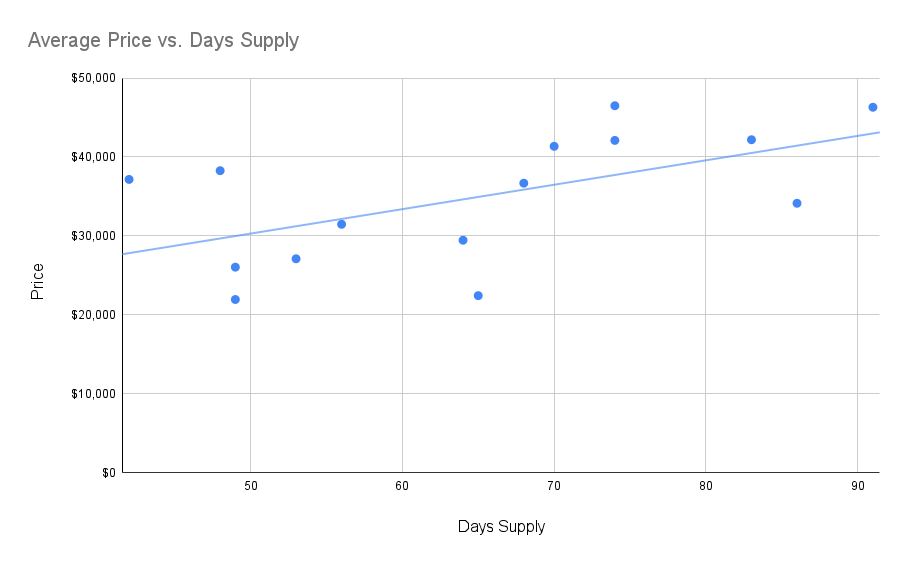

Our team recently launched a new 100% free tool, CarEdge Data Explorer. For the first time ever, local market data is available for every used car model, all in one spot. Using CarEdge Data Explorer, we analyzed used car listings in the five biggest used car markets in the nation: California, Texas, Florida, New York and Pennsylvania. By comparing market days’ supply, an important car market negotiability factor, our team of Car Coaches identified a troubling trend among the most popular age class, used cars that are three years old.

Why should you care about the days’ supply of used cars? Days supply in the car market is calculated by dividing the current unsold inventory of a specific car model by its average daily sale rate, which indicates how many days it would take to sell all the existing inventory at the current sales pace. For example, if there’s a 200 day supply of the 2019 Toyota Camry, that means it would take over six months to sell the existing inventory at current buying rates.

On the other hand, if you’re looking at a car with a 10, 20 or 30 day supply, all existing inventory is likely to be sold within the month. In other words, it’s in high demand. For reference, a typical days’ supply is about 60 days.

Here’s a subset of what we found in Data Explorer:

| Make | Model | Model Year | Days' Supply | Average Price |

|---|---|---|---|---|

| Toyota | Camry | 2020 | 49 | $26,043 |

| Toyota | Corolla | 2020 | 49 | $21,948 |

| Tesla | Model 3 | 2020 | 42 | $37,156 |

| Honda | Accord | 2020 | 53 | $27,103 |

| Nissan | Altima | 2020 | 65 | $22,436 |

| Toyota | RAV4 | 2020 | 56 | $31,471 |

| Honda | CR-V | 2020 | 64 | $29,453 |

| Tesla | Model Y | 2020 | 91 | $46,295 |

| Jeep | Grand Cherokee | 2020 | 86 | $34,133 |

| Toyota | Highlander | 2020 | 48 | $38,263 |

| Ford | F-150 | 2020 | 74 | $42,096 |

| Chevrolet | Silverado | 2020 | 70 | $41,349 |

| Ram | 1500 | 2020 | 83 | $42,181 |

| GMC | Sierra | 2020 | 74 | $46,486 |

| Toyota | Tacoma | 2020 | 68 | $36,680 |

The shortage of affordable used cars on the market is a severe issue that is negatively impacting consumers. High-demand vehicles in the lower price range have far less inventory available, making it increasingly difficult to find a reasonably priced used car, let alone negotiate for a better deal. This situation is the consequence of several economic and industry factors we’ve highlighted, with no quick fix in sight.

In contrast, the market for larger SUVs, and full-size trucks is relatively robust, but these come with a hefty price tag. Although this disparity in the market may provide a wider choice for those who can afford these more expensive models, it leaves budget-conscious consumers with limited options.

A graph of data from Data Explorer of the five top-selling cars, trucks and SUVs shows that lower prices mean less inventory:

Affordable models are harder to come by today. While this reality poses a challenge for buyers, it also emphasizes the need for prospective car owners to be savvy, strategic, and armed with the best information possible to navigate this changing landscape.

We’re on a mission to bring car buyers everywhere more resources and tools to level the playing field when negotiating car deals. Do your own research using the same tools our team uses with CarEdge Data Explorer. See used car inventory in your area, average prices, average mileage and more in all 50 states. Data Explorer is your jumping off point for understanding current market trends. In the face of a challenging market, knowledge and strategy are your best allies in the hunt for an affordable used car.

You know what’s infuriating? The fact that dealers are increasingly shipping their most affordable used cars overseas. Yes, everyone should have access to transportation that’s at an attainable price point. That includes countries in Africa, Central America, and other regions where American used cars are heading. But let’s remember that supply is not meeting the demand for cheap used cars right here at home.

The global market for used light-duty vehicles grew by almost 20% between 2015 and 2019, resulting in over 4.8 million units being exported from the United States to developing countries. Following a slowdown during the pandemic, exports are skyrocketing in 2023.

Interestingly, the growing popularity of electric vehicles is contributing to an affordability crisis in the used car market. Dealers in states such as New York and Florida, where consumers are increasingly purchasing EVs, are turning to international markets to sell their older gas-powered models. Check out this intriguing piece by CNN to learn more about the lucrative international trade of used cars.

Firstly, a significant increase in the number of returned lease vehicles could lead to more affordable used cars. The volume of lease returns dropped from 6.2 million vehicles in 2018 to 5.5 million in 2022. Further, leasing has plummeted from 33% of the new car market in 2020 to only 17% today. This decline in leasing is starting to trickle down into the wider auto market, which affects the used car supply. For those nearing the end of their car lease, our guide spells out your options at the end of a lease.

Secondly, encouraging more trade-ins could help make used cars more affordable. Drivers nowadays are holding on to their cars for longer and being more judicious when it’s time to sell, often opting to sell to private buyers instead of dealerships. Increasing the number of trade-ins could pump more used vehicles into the market, potentially helping to stabilize prices.

Always be sure to compare quotes from online car buyers here before trading in! You could get thousands more for your car.

Lastly, increasing turnover in rental car fleets could also contribute to a more balanced used car market. The average age of rental car fleets has risen from 1.9 years in 2019 to 3 years today. While older rental cars can provide a boost to used car inventory, exercise caution when considering these vehicles due to the potential for heavy use and lack of maintenance during their rental life. For a deeper dive into this topic, check out our guide to buying a rental vehicle.

In summary, the used car market is presenting unprecedented challenges for budget-minded buyers. Today’s market conditions are driven by a confluence of factors. These include a shortage of new vehicles due to a chip crisis, a decline in leased vehicles and trade-ins, and an older rental car fleet. These changes have led to a significant increase in the average price of used cars. Affordable options under $20,000 are increasingly rare and more challenging to negotiate.

Before you kick off car shopping, be sure to explore used car deals and inventory in your area with our newest free tool, CarEdge Data Explorer. We’ve also just launched our ultimate deal analysis tool, CarEdge Report, included with every Data and Coach plan. This tool equips you with comprehensive, up-to-date market insights to give you the upper hand in finding and negotiating the best deals on used cars. At CarEdge, we believe in demystifying car buying, once and for all. Knowledge is power!

Understanding used car dealership profit margins can make buying a car at a fair price easier than you’d think. Thanks to fresh industry data we have insight into the profitability of eight publicly traded dealership groups. And while most used car dealers experienced a decrease in gross profits per used vehicle sold in Q1 2023, there were exceptions — Carmax (+3%), AutoNation (+35%), and Carvana (+52%).

Here’s the breakdown:

So, how does understanding dealership profit margins empower you, the consumer to get a better deal? Let’s dive in.

Fluctuating profit margins in the market hint at competitive dynamics, potentially paving the way for better deals for consumers. This could be an excellent time to consider buying a used car, especially from dealerships that are currently facing profit contractions.

With the knowledge of dealership profit margins, you could have an edge in price negotiations. If a dealership enjoys high-profit margins, there may be more room for negotiation. On the flip side, those with tighter margins might not offer as much price flexibility, but they could be keener on making a sale.

Interestingly the used car dealers with the greatest profit margins are Carvana and CarMax, the two dealer groups that do not allow negotiations. This means that if you are considering purchasing from one of these dealers you need to understand that you are paying a premium, and you likely could save money on a comparable vehicle from another dealer.

Don’t restrict your search to one dealership or group. The disparity in profit margins among dealership groups underscores the value of shopping around. Independent dealerships could also provide attractive deals.

It’s also paramount to research the fair market value of the vehicle you’re interested in. Resources like CarEdge can provide an extensive array of data to help you make an informed decision.

Understanding the days supply of inventory is another valuable piece of information. It indicates how long a dealer’s current stock of used vehicles would last given the current sales rate. The longer a vehicle stays on the lot, the more it costs the dealership in the form of floorplanning costs, which can encourage them to negotiate on price.

Current used inventory days supply for the six groups are:

Unfortunately we do not have a reliable source for days supply for Carvana or CarMax.

This information could influence your buying strategy. Dealerships with a high inventory supply might be more willing to negotiate on price. Timing your purchase when the inventory supply is high could lead to better deals. A high supply might suggest overpricing or less popular models, whereas a low supply could indicate competitive pricing or high-demand models.

Try using the new FREE CarEdge Data Explorer to get a sense for days supply of inventory in your area.

With this knowledge of dealership profit margins and days supply of inventory, you’re well-equipped for your next car buying journey. It may not look like the good old days, but you’re setting the stage for a win-win negotiation. After all, in this new era of car buying, information is your strongest asset.

The art of negotiation is pivotal when it comes to car buying. It’s a game where information is your strongest weapon, and CarEdge is your best ally. Today, we bring you five triumphant tales from the CarEdge Community, each of them a testament to the power of knowledge and the importance of negotiation in the car buying journey. If you’re skeptical about negotiating in today’s car market, these success stories will change your mind!

Joey’s story is one of patience, timing, and understanding the market. He had his eye on a new truck and, armed with insights from CarEdge, he waited for just the right moment to make his move.

“I used CarEdge to check for used deals around me,” Joey recalls, “and negotiated a killer deal. The truck had been on the lot for over 70 days and the dealer was motivated. I waited until the last day of the month and negotiated down to my asking price. I also negotiated GAP down almost 50%. You guys are a wealth of information. If it’s taxable it’s negotiable!”

In fact, timing plays into negotiability in a big way. Savvy car buyers know that dealerships often have monthly, quarterly, and yearly sales targets. At the end of these periods, they are more likely to negotiate to hit their goals.

In addition, the length of time a car sits on a dealer’s lot impacts its price. The longer it stays, the more motivated a dealer becomes to sell, offering a ripe opportunity for negotiation. Understanding these dynamics and the concept of supply and demand in the car market can greatly influence the outcome of your negotiation and lead to BIG savings.

Jon’s negotiation journey led him to an unexpected place: a job offer. Working with CarEdge Finance and Insurance Specialist Kimberly Kline, Jon confidently navigated through the dealership’s pitch.

“When I first arrived, the salesman brought out the offer sheet with three different down payment amounts and three different costs per month,” Jon recounts. “He wanted my initials. I declined. The sales manager then came out asking what I wanted. I said that I wasn’t looking at monthly costs but total out-the-door costs.” That simple, informed request set the tone for the rest of the negotiation.

Jon ended up getting the new truck he wanted with an out-the-door price UNDER MSRP. The Sales Manager was so impressed that Jon says he offered to hire him to sell cars. Was it a serious offer? We wouldn’t be surprised if it was with how skillfully Jon stayed in control of his deal!

In Tampa, Marcus was eager to get his hands on a low-mileage Toyota Avalon Hybrid. He played hardball with several dealerships until he found one ready to play his game. He secured his dream car for an incredible $8,000 below sticker price and also secured a great deal on his trade-in.

“My advice is don’t fall in love with the car ONLY, also fall in love with the deal! You really have to just stick to it and use what you learn from CarEdge,” Marcus advises. His determination, coupled with CarEdge’s resources, brought him the deal he was after.

Check out Marcus’ full breakdown of his deal here.

Knowledge is power, as Navnit demonstrated. When shopping for a 2023 Mazda 3, the best deal he could initially find was $28,500. After using CarEdge’s tools and Deal School, he was sure he could negotiate a better out-the-door price. His thorough understanding of pricing, taxes, and fees flipped the script, with Navnit explaining to the dealer how THEY could meet HIS terms.

Here’s how he says the deal went down.

Dealer: The best I can do is $27,000 plus taxes and title

Me: No, I am looking for $27,000 out-the-door

Dealer: How is that possible?

Me: Well, you can knock off the $800 in dealer-installed accessories, I don’t need the $700 GAP insurance, I can get deals with a doc fee that is $600 lower than yours, and title and then I know I can get a $1500 discount. If not from you, I could from the 3 others that I have emails from.

Dealer: Let me talk to my manager…. ….. The best I can do is $27,500.

Me: Well thank you but that doesn’t work for me. Tell me you can do 27 and we sign today.

Dealer: Well in that case you need to finance through us.

Me: Well I already have a loan quote from my credit union at 4.75%. can you do better?

Dealer: Hold on….. We can do 4.3%

And just like that, Navnit showed the dealer who was in control. He ended up getting exactly what he wanted, at the price he had in mind.

“I had to be so vigilant,” says Navnit. “I was asking for printed deposit receipts, previewing buyers’ orders, pointing out the rebates they had added and so much more. But the bottom line, buying a car is so damn hard.”

Print Off This Car Buying Cheat Sheet and Take It With You!

Never Pay These Fake Dealer Fees!

In the world of car buying, sometimes an email can save you thousands. Jonathan worked with CarEdge Car Coach Jerry to draft an email to his dealer, transforming the trade-in valuation of his 2015 Crosstrek from $10,290 to $12,000.

Jonathan shared, “The salesperson called me right away the next morning, and said, ‘What number could you do for your car?’ Instinctively I said, ‘How about $12,000?’ and they agreed. If I had it to do over again, I realize there would have been no harm in replying with $12,500 or even $13,000. Big picture, I’m very happy with the deal. Nothing’s perfect, and I take it as a learning experience for next time.”

Jonathan’s email showcased how thorough research and confidence in your offer can lead to significant savings. He credits his success to the knowledge and support provided by CarEdge: “It was great to have someone in my corner. That night I wrote the salesperson an email.”

His story, along with the others, is a testament to how well-informed car buyers can change the dynamic of a negotiation, flipping it in their favor. Check out Jonathan’s full story for more.

See HUNDREDS more success stories at the CarEdge Community

From waiting for the right time to strike, to firmly and confidently advocating for fair prices, these empowered car buyers show that, armed with the right tools and knowledge, you too can come out on top in the car buying game.

Ready to outsmart the dealerships? Download your 100% free car buying cheat sheets today. From negotiating a deal to leasing a car the smart way, it’s all available for instant download. Get your cheat sheets today!

Don’t be afraid to negotiate on your next car purchase. Remember: If it’s taxable, it’s negotiable. Leverage CarEdge Data and our all-new CarEdge Report to understand local market negotiability like never before. Ready to work 1:1 with a car buying expert? CarEdge Coach is the perfect path to big-time savings.

In 2023, the automotive market continues to navigate the unpredictable seas of supply and demand. A lingering used car shortage from previous years is causing 2-3-year-old in-demand models to skyrocket in price, while new car inventories are bloating due to overproduction. What does this mean for you, the savvy car shopper? Let’s dive in.

The latest data from Cox Automotive shows that in many cases, there’s a shortage of 2-3 year old used cars. For in-demand models that are just a few years old, demand far exceeds supply. Dealers are using this to their advantage (to the surprise of no one…) and are marking them up severely. For the brands we’ll talk about below, 2-3 year-old used cars often cost nearly the same as a brand-new car. There’s a totally opposite situation for NEW cars. For many makes and models, there’s now an oversupply of new cars in 2023, just two years after the car shortages of 2021.

New car available supply (total vehicles on the lot) is up 71% since last year, and dealerships are finding their lots chock-full of shiny new cars.

In terms of days’ supply, today’s market is up 47% since spring 2022. Days’ supply is a common auto industry metric that is calculated by dividing the total number of available vehicles by the average daily sales number from the last 45 days. It’s one of many available insights for every new and used listing with CarEdge Data.

790,000 more vehicles on sale today compared to May 2022 means dealers are more motivated than ever to cut deals and move inventory. However, despite this surge in supply, the average listing price for a new car is still 5% higher than last year.

On the flip side, used car inventory is 13% lower compared to last year. High prices have led buyers to say NO to used cars, resulting in a 4% drop in sales rates and listing prices. However, these prices remain stubbornly above 2021 levels.

With brands like Toyota, Lexus, Kia, Honda, Subaru, Hyundai, BMW, and Land Rover, new car supply shortages are making used models a more attractive option than their new counterparts. How so? Dealers continue to markup these cars in many markets.

On the other hand, brands like Ford, Lincoln, Dodge, Ram, Chrysler, Jeep, and Buick are dealing with a glut of new cars, making new vehicles especially negotiable today, and offering more value than used inventory at nearly the same price AFTER negotiation.

Based on the latest new car inventory, these brands are most negotiable in 2023:

Nationally, these automakers all have current new car inventory well above the historical norm of 60 days’ supply. See local days’ supply for models you’re interested in with CarEdge Data on Car Search.

Using the tools available through CarEdge Data, we analyzed new car inventory by brand in the three largest markets across the nation. Some notable differences are seen across California, Texas, and Florida.

| Brand | Days' Supply (CA) | Days' Supply (TX) | Days' Supply (FL) |

|---|---|---|---|

| Toyota | 39 | 43 | 38 |

| Kia | 44 | 46 | 41 |

| Honda | 46 | 47 | 43 |

| Lexus | 45 | 50 | 45 |

| BMW | 53 | 67 | 57 |

| Land Rover | 70 | 65 | 64 |

| Subaru | 59 | 53 | 55 |

| Hyundai | 66 | 53 | 56 |

| Volkswagen | 63 | 63 | 56 |

| Cadillac | 60 | 57 | 63 |

| Chevrolet | 68 | 64 | 68 |

| Nissan | 65 | 59 | 54 |

| Mercedes | 73 | 68 | 69 |

| Porsche | 82 | 61 | 72 |

| Mazda | 62 | 68 | 68 |

| GMC | 77 | 72 | 73 |

| Audi | 89 | 72 | 62 |

| Acura | 72 | 81 | 60 |

| Genesis | 96 | 95 | 87 |

| Mitsubishi | 91 | 65 | 65 |

| Mini | 81 | 94 | 92 |

| Ford | 80 | 71 | 67 |

| Dodge | 101 | 84 | 92 |

| Lincoln | 104 | 72 | 72 |

| Ram | 147 | 116 | 132 |

| Infiniti | 94 | 88 | 73 |

| Chrysler | 106 | 86 | 87 |

| Jeep | 126 | 103 | 119 |

| Jaguar | 101 | 90 | 81 |

| Buick | 100 | 106 | 84 |

Hyundai, Nissan, Mitsubishi and Audi have much higher inventory on the West Coast, while Toyota, Kia and Honda have higher new car inventory in Texas. Be sure to check local market supply in your area to get the best sense of negotiability.

In terms of segments, compact cars, midsize cars, subcompact cars, compact crossover/SUVs, minivans, and full-size crossover/SUVs are experiencing a supply shortage.

Conversely, full-size pickup trucks, high-end luxury cars, electric vehicles, full-size cars, and uber luxury vehicles are enjoying a much higher days’ supply than average.

New car segments like vans, mid-size SUVs, most luxury cars and traditional hybrids have roughly average inventory right now.

Right now is a great time to be in the market for a new EV. Across all brands, there’s a nearly 90-day supply of new electric vehicles. This can be seen in models such as the Ford Mustang Mach-E, which now has over 150 days’ supply. That’s up over 100% since last year.

Tesla keeps lowering prices, and with the Model Y, has severely undercut prices for the following popular competitors:

In other words, there’s finally serious competition in the EV landscape. Is it a price war? So far, Tesla’s competitors have not fired back with steep price cuts of their own. We’ll see if that changes this summer. However, used Tesla prices have fallen drastically this year.

Remember, the EV tax credit landscape has changed in the past several months. Popular EVs from Hyundai, Kia, Audi and others no longer qualify due to made-in-America requirements. However the most popular electric vehicles in America, which are of course those bearing the Tesla badge, once again do qualify for the first time since 2019. Here’s an updated summary of where things stand with the EV tax credits.

Whether it’s better to buy new or used in 2023 largely depends on the brand and type of car you’re interested in. Industry-wide, new cars are looking better than they have in years. Popular brands are facing an oversupply, and with that comes greater negotiation power.

Ready to outsmart the dealerships? Download your 100% free car buying cheat sheets today. From negotiating a deal to leasing a car the smart way, it’s all available for instant download. Get your cheat sheets today!

With fluctuating inventories and prices, it’s crucial to stay informed and flexible. Use CarEdge Car Search to check the local days’ supply of the makes and models you’re interested in, and make sure to stay updated with the latest market trends to snag the best deal.

Purchasing a new or used car can be an exciting experience. It can also be miserable. When you set out to secure a great deal on your next car, it’s essential to be well-informed about the auto financing process to avoid costly mistakes. To help you navigate the often complex world of car loans and financing, we have compiled a comprehensive guide to auto financing that covers ten essential steps and tips for success, including:

2. Considering down payment options

3. Shopping around for financing

4. Determining the right loan term

5. Understanding manufacturer incentives

6. Exploring Certified Pre-Owned Vehicles

To illustrate how to effectively employ these strategies, we have also created an example conversation between an empowered car buyer and a car dealership Finance Manager. This detailed script guides you through the entire financing process, from the initial introduction to signing the paperwork. By following this example and implementing the advice provided, you’ll be better equipped to secure a favorable loan, save money, and drive away in the car of your dreams.

Your Path to Auto Loan Savings: Credit Scores, Down Payments, and Savvy Financing Strategies

Let’s dive into valuable tips and expert advice from myself, CarEdge Finance and Insurance Specialist Kimberly Kline, and automotive industry veteran and CarEdge co-founder Ray Shefska. We’ll explore the key factors that influence your loan costs, such as credit score, down payment, and loan term, as well as some lesser known considerations that can save you big bucks at the finance office. Study this auto finance cheat sheet before you head to the dealership!

👉 The basics of auto lending: There are three things that lenders look at when determining whether to approve a customer for a loan. Those three things are 1) ability, 2) stability and 3) willingness.

Ability: do you have the ability to actually make the payments? Will your income support the payment? Based on your debt-to-income ratio, do you fall into the guidelines that the banks use to make this determination?

Stability: how long have you been doing what you do? How long have you been on your job, at your address? Do you job hop or move frequently? Have you shown the requisite stability within your field to satisfy the bank’s lending policies?

Willingness: how have you handled your past credit obligations? Have you handled them in a timely manner or have you sometimes fallen behind? In other words, have you shown a willingness to pay your bills in a timely fashion?

If you can satisfy those three criteria, then you should be approved for a loan at a good interest rate.

Now, we’ll walk you through the key factors you need to consider when applying for a car loan (with the goal of securing a great rate).

Your credit score plays a significant role in determining your auto loan interest rate. Before shopping for a car, check your credit score and work on improving it. For example, pay off outstanding debts, make timely payments, and keep your credit utilization low. Be cautious of applying for multiple credit cards or loans in a short period, as this may negatively impact your score. Monitor your credit report for errors and dispute them promptly.

👉 Pro Tip: Always let the dealership Finance Manager know that YOU know your credit well! This puts you in a more controlling position.

Aim for a down payment of at least 20% of the car’s purchase price to minimize interest costs and potentially qualify for a lower rate. For instance, on a $30,000 car, a 20% down payment would be $6,000. By saving more for your down payment, you can reduce the loan amount, lower monthly payments, and decrease the likelihood of being upside down on your loan.

👉 Pro Tip: Banks and credit unions like to see a healthy loan-to-value ratio. This means that a higher down payment is always a good thing.

Don’t limit yourself to dealership financing. Once you know your credit score, search online for reputable credit unions that operate in your state (start here with CarEdge). Most credit unions publish their new and used auto loan rates on their website. This gives you an excellent idea of what the best current interest rates are. This arms you with knowledge when it comes to speaking with the Finance Manager. If you find a great deal, speak to the loan officer, and consider applying for a car loan. Even if you decide to finance with the dealership, this pre-approval will come in handy in the dealership finance office. Consider working with CarEdge-approved credit unions for excellent rates, and top-tier customer service.

👉 Pro Tip: protect your credit. Don’t aimlessly apply to credit unions online but if you find one with great rates, always speak with a loan officer first, get all your questions answered on their process and then apply.

While longer loan terms may have lower monthly payments, they also mean you’ll pay more interest over the life of the loan. Opt for a shorter loan term if it fits your budget to save on interest costs. For example, choosing a 48-month loan term instead of a 72-month term on a $25,000 loan at a 5% interest rate can save you over $1,500 in interest payments.

Automakers often offer special financing deals or cash rebates to encourage new car sales. Keep an eye out for these incentives, such as low or 0% APR financing, which can significantly reduce your overall interest costs. Be sure to read the fine print and weigh the pros and cons of these offers before deciding. We keep track of the best manufacturer incentives here.

👉 Pro Tip: Don’t expect the dealership finance manager to advertise the manufacturer promotion. Do your research online before shopping.

If you’re buying a used car, consider a manufacturer-certified Certified Pre-Owned (CPO) vehicle. Manufacturer CPO programs have stricter guidelines and typically offer enhanced warranty coverage. Stay away from third-party CPOs, at least if you’re looking for better rates. Browse certified pre-owned (CPO) car listings at CarEdge Car Search to find the perfect vehicle with local market data.

👉 Pro Tip: Let the dealership Finance Manager know that YOU know there are often APR Incentive rates for manufacturer CPO’s. So speak their language and ask them to “check their rate sheet for subvented rates on the CPO”.

If you are stuck with a higher-than-ideal rate, consider refinancing to save on interest costs and potentially lower your monthly payment. Refinancing involves taking out a new loan to pay off your existing loan, ideally with a lower interest rate. Refinancing matters more today than it has in the recent past. With rates being so high right now, even half of a point could save you big money over the life of the loan! This can be a smart move if your credit score has improved since you initially took out the loan or if you discovered in hindsight that the dealership put you in a higher interest loan.

👉 Pro Tip: When refinancing, check to see if the bank or credit union has any incentives (such as for automatic withdrawals, or career-based incentives for teachers, first responders, military and more).

Dealerships may add a markup to the interest rate they offer on car loans, pocketing the difference as profit. Be aware of this practice and ask for the ‘Buy Rate’ to see how much the dealership is marking up the loan. If you have a pre-approval from a credit union, use it as leverage to negotiate the best rate with the dealer. It’s smart to understand how dealers make money before negotiating.

We’ll explain exactly how to negotiate marked-up interest rates in the next section. Stay tuned!

If your car loan allows for early repayment without penalties, consider making extra payments towards “principal only” to pay the loan off ahead of schedule.

👉 Pro Tip: Use an amortization schedule to see how fast you’ll pay down your loan!

This can save you a significant amount of money on interest charges over the life of the loan. Just be sure to double-check your loan agreement for any prepayment penalties before proceeding.

Now, let’s go over a real-world scenario that will be VERY similar to what you’ll encounter at the dealership. It’s time to apply your knowledge!

Check out our series of car buying roleplay videos for unbeatable insights into what it’s like to make a deal!

The best way to learn how to effectively negotiate in the finance office is to prepare for the situations and conversations you’re likely to encounter. What better way to do that than creating a real-world script with the help of dealership professionals who’ve been through this hundreds of times? The following is an example conversation between an empowered, prepared car buyer and a car dealership auto Finance Manager. Don’t forget to check out the original CarEdge Cheat Sheet to Car Buying for more word-for-word car buying help!

Finance Manager: Hi, I’m the finance manager here at the dealership. I understand you’re interested in purchasing a car today. Is that correct?

You: Yes, that’s correct. I’ve already chosen the car I want, and now I’m looking to finalize the financing.

Finance Manager: Great, let’s start by filling out a credit application.

(Note: The dealership is going to need to run a credit report and will insist on doing so in order to determine what interest rates you may qualify for. People usually only know their overall credit score and not their auto credit score which by its nature is what banks need.)

You: I know my credit well and I have Tier One credit.

👉 Pro Tip: If you have a lower credit score, you can ask for a ‘tier bump’ at this point. A tier bump is essentially when the dealership finance manager would call the lender to ask for a higher rate, despite the buyer’s lower credit.

Finance Manager: That’s a decent score. Now let’s discuss financing options. We have some deals available through our dealership.

You: Thanks, but I’ve already shopped around for financing and have already spoken with my credit union loan officer and I will qualify for their best rate. I’d like to see how your dealership’s rates compare before making a decision. Also, I’ve been approved for a lower rate with a credit union. Can you beat that rate?

👉 Pro Tip: If you’re borrowing over $30,000, consider asking about a ‘large loan discount’, which is sometimes an option for higher borrowing amounts. See the video we shared in Scene One for more information!

Finance Manager: We’ll certainly do our best to match or beat the rate you’ve received from the credit union. Let me check our current offers. Based on your credit score, we can offer you a 60-month loan at an interest rate of 4.5%.

You: I appreciate the offer, but I’d prefer a shorter loan term of 48 months to save on interest costs over the life of the loan. Can you provide a quote for that term and see if you can match or beat the rate I received from the credit union?

Finance Manager: Sure, let me recalculate the rates for a 48-month term and see if we can match or beat your credit union’s rate. Give me a moment.

Alright, I’ve looked into our current offers for a 48-month loan term. We can offer you a 48-month loan at an interest rate of 0.5% lower than the offer from your credit union.

You: That’s great! I appreciate you working with me to secure a better rate. I think I’ll go with this financing option from the dealership. Interest adds up!

Finance Manager: How much do you plan on putting down as a down payment?

You: I’m prepared to make a down payment of 20% of the car’s purchase price to minimize interest costs and avoid the need for GAP insurance. Can you double check if there are any additional manufacturer incentives or offers available that could get me an even lower rate?

You: I noticed that the car I’m interested in is a Certified Pre-Owned (CPO) vehicle. Please check your “rate sheet” for subvented rates on the CPO. Does that qualify me for a lower interest rate?

👉 Pro Tip: It will go a long way to show that you’re familiar with dealership terms like the ones we’ve included here. Don’t miss this FREE resource: The Car Buyer’s Glossary of Terms

Finance Manager: Yes, CPO vehicles typically do qualify for lower rates due to their lower risk. With that in mind, I can offer you a 3.9% interest rate for a 48-month loan with the manufacturer incentive.

You: I appreciate the offer, but what is the rate on my approval that you received? I’d like to see a direct quote from the lender.

(Note: You can ask to see the direct quote from the lender, but know that since this is indirect lending with the dealership acting as an intermediary, they are not required to share that information with you. Their answer simply may be, “this is the rate that I can offer you”.)

Finance Manager: You received a subvented rate of 3.9%.

You: Is that the Buy Rate?

Finance Manager: No, we mark it up by a point.

You: I would really love that Buy Rate. I know my credit union offered 4.0%, but if you can give me 3.5%, I won’t refinance the loan immediately.

Finance Manager: Okay, I can do that.

👉 Pro Tip: The Finance Manager always wants to avoid the charge-back on the refinance. Basically, if you refinance right away, they’re not making any money from selling you the loan.

Finance Manager: Before we finalize the paperwork, I’d like to go over a few additional products we offer that could save you money in the long run. First, we have a Theft protection Package that will reimburse you in case your car is stolen.

You: Thanks for mentioning it, but I’ve already researched that option and I don’t think it’s necessary for my situation. I’ll pass on the Theft protection Package.

Finance Manager: Alright, that’s fine. Another package I’d recommend is our Tire Care Package. It covers tire replacements and rotations, ensuring your tires are always in great condition.

You: I appreciate the suggestion, but I’ve budgeted for tire maintenance separately and will handle it on my own. I won’t be needing the Tire Care Package.

Finance Manager: No problem, I understand. Lastly, we offer an Extended Warranty that covers any unexpected repairs or breakdowns after the manufacturer’s warranty expires. It’s a great way to protect your investment. I can offer this coverage to you for $30/month.

👉 Pro Tip: Finance Managers will not give you the actual price unless you ask for it. They prefer to tell you the monthly payment to downplay the cost.

You: I’ve actually already looked into extended warranties, and I found the same exact coverage through CarEdge for hundreds of dollars less. I’ll be purchasing their warranty instead.

Finance Manager: Alright, I respect your decision. Let’s move forward and finalize the paperwork for your new car!

(Note: If the finance manager attempts to force you to purchase any of their add-on products, demand to see the contract. Every product includes a contract, and on there, it will clearly state that the product is not required to secure financing.)

👉 Pro Tip: The purchase of products in the finance office cannot be tied to your interest rate. For example, a Finance Manager cannot say “if you get the extended warranty, you’ll get a lower interest rate”.

You can say “No” to everything if you want and sign a Declination Disclosure. However, it is part of Compliance that the Finance Manager lets you know the additional products that are available to 100% of the buyers, 100% of the time.

The Complete List: Never Pay These Fake Dealership Fees

Finance Manager: Here’s your base payment at 3.5% for 48 months. Are you ready to proceed with this offer?

You: Yes, that sounds great. Let’s finalize the paperwork and complete the purchase.

By employing the expert advice provided in the previous responses, the car buyer in this example has successfully navigated the auto financing process, and secured a great deal. Despite the initial offer from the dealership being substantially higher interest rate, the buyer used their knowledge of auto financing to get a better rate. By showing that they understand the process through questioning every aspect of the deal and speaking dealership language, the buyer stayed in control, ultimately saving hundreds to thousands of dollars over the life of the loan.

Check out CarEdge Dealer Reviews to see what deals are near you!

With these car loan tips in hand, you’re well on your way to making the best possible auto financing decisions. But don’t stop there! Join the 100% FREE CarEdge Community to connect with our Car Coaches and thousands of drivers like yourself. Looking for expert tools and assistance? CarEdge Data and CarEdge Coach offer expert guidance and personalized support throughout the car buying process. Our experienced professionals will help you save money, avoid costly mistakes, and achieve your car buying goals.

Don’t go through the car buying process alone – let CarEdge empower you with industry-leading tools and expert coaching. Try CarEdge Data and CarEdge Coach today and drive away with confidence.

Dealership fees add up to hundreds and even thousands of dollars. However, that doesn’t mean you are required to pay them. Unsurprisingly, customer satisfaction with the vehicle purchase experience is declining. Forced add-ons and dealer markups are ruining car buying. In fact, several car dealership fees are outright anti-consumer tactics to squeeze a few extra dollars out of you. With negotiation know-how, car buyers should push back against fake dealership fees, and stay in control of their deal. Let’s take a look at the legitimate fees you can expect, and the fees and add-ons to never pay a car dealership.

When purchasing a vehicle, it’s essential to be aware of the legitimate fees and taxes that make up the out-the-door price. These fees are typically imposed by the government and vary by state or local jurisdiction.

These fees make up the out-the-door price. Find out how much your next car will REALLY cost with this free out-the-door price calculator.

Here’s a closer look at some of the most common legitimate fees and taxes associated with buying a car.

Buying a car comes with various taxes, including city, state, and county sales tax, personal property tax, and often a vehicle license tax, which has to be paid annually. These taxes can vary greatly depending on your location, so it’s crucial to research and understand the tax rates specific to your state and local jurisdiction when budgeting for a vehicle purchase.

The title fee is charged as a cost for the documents required to transfer the title from the seller to the buyer. This fee can range from as low as $4 up to $150, depending on the state you’re in. The title fee is non-negotiable and must be paid to properly transfer ownership of the vehicle.

Tags and registration fees are also imposed by your local government and are non-negotiable. These fees cover the cost of registering the vehicle under the buyer’s name and providing the physical license plates for the car.

Registration fees can vary widely among states. Some states charge a flat fee, while others base their fees on the vehicle’s weight or age. It’s essential to research your state’s registration fees to have an accurate estimate of the overall cost of purchasing a car.

Tag fees relate to the physical plates required for your vehicle. The cost for these plates varies from state to state, so make sure you’re aware of your specific state’s tag fees when budgeting for your car purchase.

Doc fees straddle the line of legitimate and illegitimate. While dealerships may charge a doc fee to offset the cost of non-revenue producing employees, you should always negotiate this fee. Doc fees vary widely from state to state and dealer to dealer, so it’s crucial to research the average doc fee in your area.

Note that the dealer will never actually remove the fee from your buyer’s order, instead they will reduce the selling price of the vehicle by the same amount as the doc fee.

Car Dealer Doc Fee by State in 2023

Now, onto the negotiable dealer fees you should never pay when buying a car.

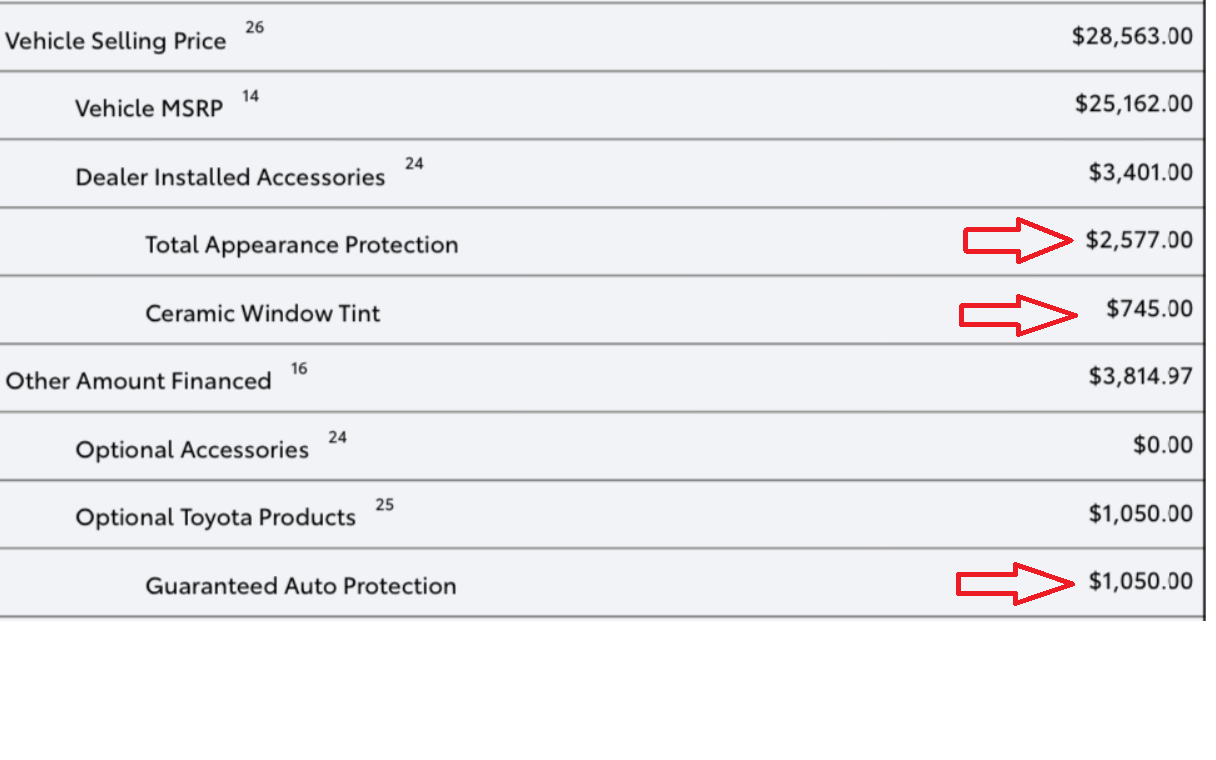

Some dealership fees add no value to your car and should be included with every new and used car at no additional cost. These are essentially fake fees that solely exist to make the dealership more money. Always avoid these fees:

It’s very important to remember that these fees add no value at all to your car, whether new or used. All of these so-called services should be included in the selling price of the vehicle, no ifs, ands or buts. Having trouble negotiating fake fees? Our CarEdge Car Coaches are always here to assist.

These car dealer fees add little value despite potentially costing hundreds or thousands of dollars. If you don’t want the product, these fees or ‘add-ons’ are always negotiable:

All of these add-ons and dealer fees are negotiable. Not a single one of them is required, no matter what a salesperson tells you. They’re not like the taxes, title and registration fees that you should expect to pay.

| Fee or Add-on | Category |

|---|---|

| Wheel Locks | Accessory |

| Spash Guards | Accessory |

| Mud Guards | Accessory |

| Exhaust Tip | Accessory |

| Pinstripes | Accessory |

| Sun Shade | Accessory |

| Floor Mats | Accessory |

| Connectivity Kit | Accessory |

| SAVY Driver | Accessory |

| Trunk Tray | Accessory |

| Pro Pack | Accessory Packages |

| KARR Security System | Car Alarm Products |

| Fusion Security System | Car Alarm Products |

| Diamond Ceramic | Paint Protection |

| Zaktek Ultimate | Paint Protection |

| Zurich Shield | Paint Protection |

| Nano Protection | Paint Protection |

| Cilajet | Paint Protection |

| Clearshield | Paint Protection |

| Premium Exterior Finish | Paint Protection |

| Advanced Ceramic Tech | Paint Protection |

| Enviromental Protection Package | Paint Protection |

| Carefree Paint Protection | Paint Protection |

| Ziebart Diamond Gloss | Paint Protection |

| Door Edge Guard | Paint Protection |

| Clear Door Protection | Paint Protection |

| Clear Shield Package | Paint Protection |

| 3M Protection Package | Paint Protection |

| Clear Bra | Paint Protection |

| Paint Pro Film | Paint Protection |

| Invisa Shield | Paint Protection |

| Key Care/Key Replacement | Lost/Stolen Key replacement |

| Vehicle Prep | Dealer Fee |

| Dealer Prep for Delivery | Dealer Fee |

| Pre-Delivery Service | Dealer Fee |

| Pre-Delivery Inspection | Dealer Fee |

| Reconditioning Fee | Dealer Fee |

| VIN Etch | Etch Theft Deterrent |

| VTR | Etch Theft Deterrent |

| Theft Code Protection | Etch Theft Deterrent |

| Courtesy Guard | Etch Theft Deterrent |

| Express Code | Etch Theft Deterrent |

| Phantom Footprint | Etch Theft Deterrent |

| Dent Protection | Exterior Protection |

| Ding Defender | Exterior Protection |

| Appearance Protection | Exterior Protection |

| ELO-GPS | GPS Theft Deterrent |

| Spartan GPS | GPS Theft Deterrent |

| SWAT GPS | GPS Theft Deterrent |

| LoJack | GPS Theft Deterrent |

| Theft Patrol | GPS Theft Deterrent |

| Fabric Defense | Interior Protection Products |

| Interior All Weather Protect | Interior Protection Products |

| NuVinAir | Interior Protection Products |

| Caltex Reistall | Interior/Exterior Protection Products |

| LuxCare | Interior/Exterior Protection Products |

| Autobond Sealant | Interior/Exterior Protection Products |

| Xzilon Paint and Fabric | Interior/Exterior Protection Products |

| PermaPlate | Interior/Exterior Protection Products |

| Paint and Fabric Defense | Interior/Exterior Protection Products |

| Allstate Paint and Fabric | Interior/Exterior Protection Products |

| Nitrogen Fill | Tire Care |

| Solar Guard Tint | Window Tint |

| Tinted Glass | Window Tint |

| Nano-Ceramic Film | Window Tint |

| Smart Auto Windshield | Windshield Protection Coverage |

| Windshield Repair | Windshield Protection Coverage |

| Crystal Fusion | Windshield Protection Coverage |

| Dupont | Paint & Interior protection |

| Simoniz | Paint & Interior protection |

| Diamond Coat | Paint & Interior protection |

| Safe-Guard/Theft | Theft Deterrent |

| US TheftGuard | Theft Deterrent |

| Data Dots/Nano Dots | Theft Deterrent |

| Theft Prevent | Theft Deterrent |

Our CarEdge Car Coaches help thousands of drivers negotiate better deals on their car purchases every month. We’ve seen it all! Here are three examples of ridiculous dealer add-ons and B.S. fees that we’ve helped to negotiate off of the out-the-door price.

Who on Earth would agree to pay $3,000 for a protection package when you could apply those same products for a few hundred dollars elsewhere? Overpriced paint and protection fees are always negotiable.

Some dealers seem to think that if you can afford a new truck, you won’t mind paying a thousand dollars extra for unwanted dealer add-ons. Always negotiate these fees.

Two grand for a safety and security package? Nope, nope and nope.

And then you have this… a whole slew of dealership fees and add-ons that are VERY hard to justify.

When purchasing a vehicle, it’s crucial to stay in control of your deal and be aware of the various fees you may encounter. By understanding the legitimate fees, being cautious of questionable ones, and avoiding unnecessary dealership fees and add-ons, you’ll ensure that you’re getting the best deal possible on your next car.

Ready to take control of your car buying experience? Let CarEdge Coach guide you through the process, ensuring you avoid unnecessary fees and get the best deal possible, all with three months of 1:1 expert help. If you prefer a DIY approach, CarEdge Data is the perfect tool to help you make informed decisions and secure a great deal on your own terms. Why do we do it? We simply want to change car buying for the better. It’s about time!

Carvana, the nation’s 10th largest car dealer, has become increasingly popular as an online car dealership. However, despite its growing reputation, there are three key reasons why you should avoid buying your next vehicle from Carvana. Plus, we’ll take a look at the many examples of Carvana selling ‘broken cars’ to customers.

Carvana’s gross profit per vehicle has seen a significant increase, as revealed in their latest earnings report. In Q1 2023, their profits per car sold rose by an astounding 61%. Meanwhile, other online car dealers like CarMax and Vroom haven’t experienced the same success.

While Carvana’s total revenue dropped by 25% to $2.6 billion, their gross profit per unit increased. How did they achieve this? By inflating their car prices. Carvana’s financial success is relying on uninformed buyers to make purchases without realizing they’re being overcharged.

Carvana’s prices are just too high. Unfortunately, car buyers should expect to pay a premium for the no-hassle, non-negotiable prices at Carvana. The company obviously tosses a few thousand dollars onto the price tag as an unofficial ‘convenience fee’ of sorts. In some cases, they’re selling used cars at nearly the same price as new ones.

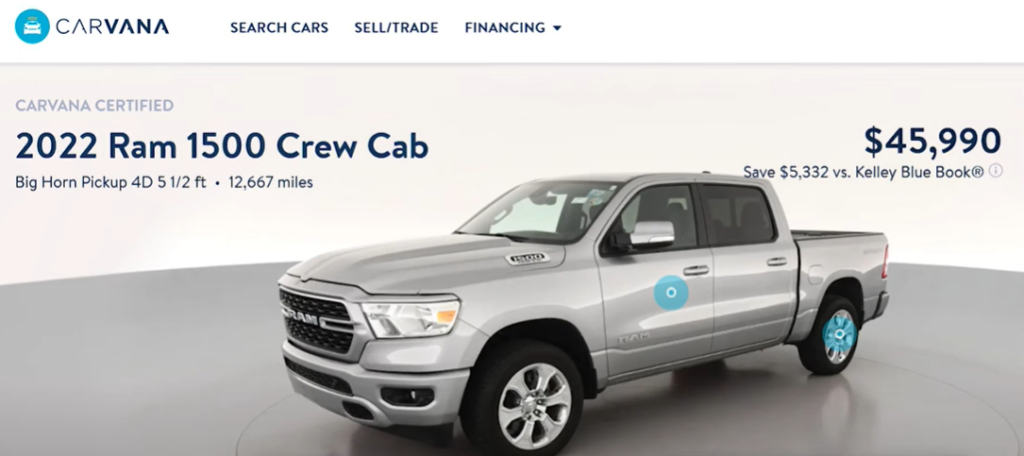

Take a look at this example. Here’s a 2022 Ram 1500 Crew Cab with 12,667 miles on it, and Carvana is asking $45,990. This isn’t 2021, folks. Truck prices have gone down. In fact, our Car Coaches are regularly negotiating over 10% off of MSRP for brand-new trucks.

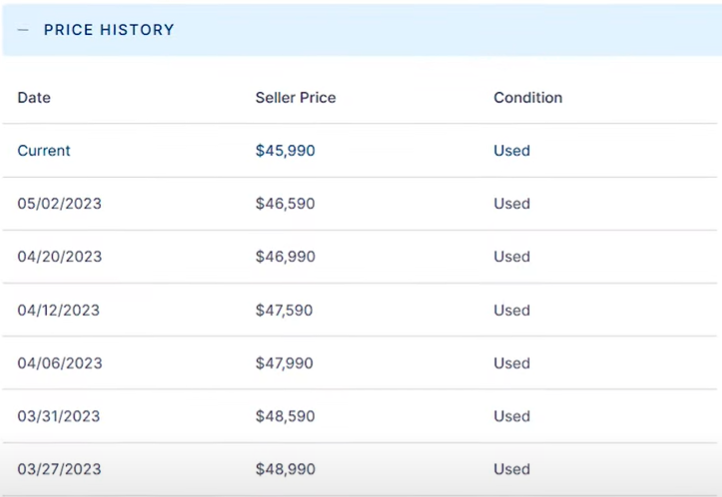

On CarEdge Car Search, we can see that Carvana has been trying to sell this truck for well over a month, and has already dropped the price by $3,000.

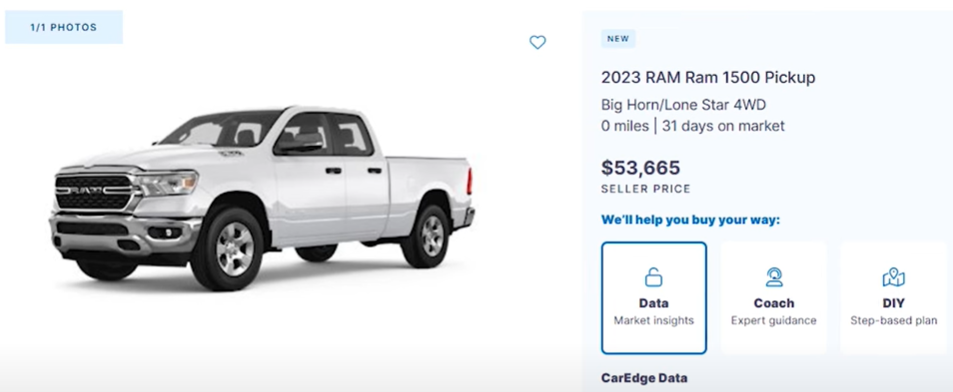

The new 2023 Ram 1500, same trim and all, is within range of the USED Ram truck once current market negotiability is taken into account. And this truck, even if it’s a few thousand dollars more, comes with a full warranty, and is without the mechanical unknowns that come with every used vehicle at Carvana.

Simply put, Carvana’s prices are just too high, but not all buyers will notice. Be sure to check CarEdge Dealer Reviews to see what others have experienced near you.

Carvana has a concerning track record of selling vehicles with serious quality issues. While not every car they sell has problems, it’s a recurring theme that cannot be ignored. Poorly reconditioned cars, or worse, are all too common in their inventory.

These are just a few of the real, horrific issues that Carvana’s customers have had to deal with:

Remember, if you can’t get an independent pre-purchase inspection (PPI), it’s not recommended to buy from that dealer. With Carvana, this is often the case.

Learn more about why getting a pre-purchase inspection is SO important.

In most instances, you’d be better off negotiating a deal on a new car rather than overpaying for the convenience of avoiding negotiations with Carvana. Do your research, compare prices, and make sure to prioritize quality when purchasing your next vehicle. Don’t be lured by the seemingly hassle-free car buying experience Carvana offers, as it could end up costing you more in the long run. Don’t forget to check the latest Carvana reviews at CarEdge Dealer Reviews!

Ready to outsmart the dealerships? Download your 100% free car buying cheat sheets today. From negotiating a deal to leasing a car the smart way, it’s all available for instant download. Get your cheat sheets today!